Mandatory rotation of audit firms - ICAEW

Mandatory rotation of audit firms - ICAEW

Mandatory rotation of audit firms - ICAEW

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

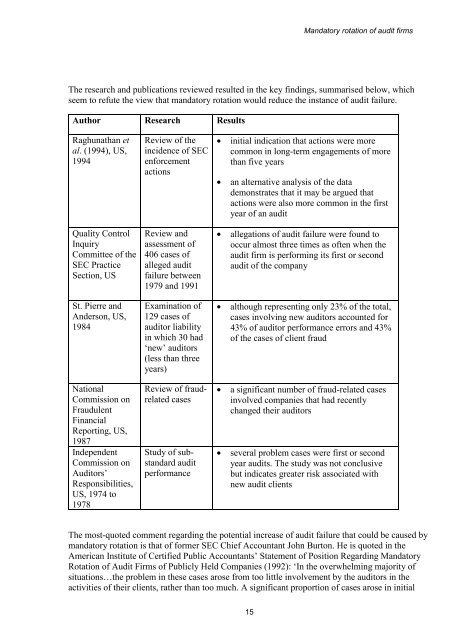

<strong>Mandatory</strong> <strong>rotation</strong> <strong>of</strong> <strong>audit</strong> <strong>firms</strong>The research and publications reviewed resulted in the key findings, summarised below, whichseem to refute the view that mandatory <strong>rotation</strong> would reduce the instance <strong>of</strong> <strong>audit</strong> failure.Author Research ResultsRaghunathan etal. (1994), US,1994Quality ControlInquiryCommittee <strong>of</strong> theSEC PracticeSection, USSt. Pierre andAnderson, US,1984NationalCommission onFraudulentFinancialReporting, US,1987IndependentCommission onAuditors’Responsibilities,US, 1974 to1978Review <strong>of</strong> theincidence <strong>of</strong> SECenforcementactionsReview andassessment <strong>of</strong>406 cases <strong>of</strong>alleged <strong>audit</strong>failure between1979 and 1991Examination <strong>of</strong>129 cases <strong>of</strong><strong>audit</strong>or liabilityin which 30 had‘new’ <strong>audit</strong>ors(less than threeyears)Review <strong>of</strong> fraudrelatedcasesStudy <strong>of</strong> substandard<strong>audit</strong>performance• initial indication that actions were morecommon in long-term engagements <strong>of</strong> morethan five years• an alternative analysis <strong>of</strong> the datademonstrates that it may be argued thatactions were also more common in the firstyear <strong>of</strong> an <strong>audit</strong>• allegations <strong>of</strong> <strong>audit</strong> failure were found tooccur almost three times as <strong>of</strong>ten when the<strong>audit</strong> firm is performing its first or second<strong>audit</strong> <strong>of</strong> the company• although representing only 23% <strong>of</strong> the total,cases involving new <strong>audit</strong>ors accounted for43% <strong>of</strong> <strong>audit</strong>or performance errors and 43%<strong>of</strong> the cases <strong>of</strong> client fraud• a significant number <strong>of</strong> fraud-related casesinvolved companies that had recentlychanged their <strong>audit</strong>ors• several problem cases were first or secondyear <strong>audit</strong>s. The study was not conclusivebut indicates greater risk associated withnew <strong>audit</strong> clientsThe most-quoted comment regarding the potential increase <strong>of</strong> <strong>audit</strong> failure that could be caused bymandatory <strong>rotation</strong> is that <strong>of</strong> former SEC Chief Accountant John Burton. He is quoted in theAmerican Institute <strong>of</strong> Certified Public Accountants’ Statement <strong>of</strong> Position Regarding <strong>Mandatory</strong>Rotation <strong>of</strong> Audit Firms <strong>of</strong> Publicly Held Companies (1992): ‘In the overwhelming majority <strong>of</strong>situations…the problem in these cases arose from too little involvement by the <strong>audit</strong>ors in theactivities <strong>of</strong> their clients, rather than too much. A significant proportion <strong>of</strong> cases arose in initial15