Mahler's Guide to Stochastic Models HCMSA-F02-3-2A, Stochastic ...

Mahler's Guide to Stochastic Models HCMSA-F02-3-2A, Stochastic ...

Mahler's Guide to Stochastic Models HCMSA-F02-3-2A, Stochastic ...

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

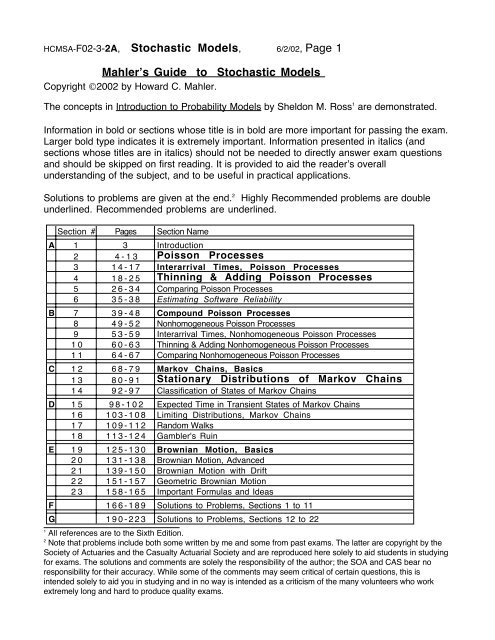

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 1Mahler’s <strong>Guide</strong> <strong>to</strong> S<strong>to</strong>chastic <strong>Models</strong>Copyright ©2002 by Howard C. Mahler.The concepts in Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross 1 are demonstrated.Information in bold or sections whose title is in bold are more important for passing the exam.Larger bold type indicates it is extremely important. Information presented in italics (andsections whose titles are in italics) should not be needed <strong>to</strong> directly answer exam questionsand should be skipped on first reading. It is provided <strong>to</strong> aid the reader’s overallunderstanding of the subject, and <strong>to</strong> be useful in practical applications.Solutions <strong>to</strong> problems are given at the end. 2Highly Recommended problems are doubleunderlined. Recommended problems are underlined.Section # Pages Section NameA 1 3 Introduction2 4-13 Poisson Processes3 14-17 Interarrival Times, Poisson Processes4 18-25 Thinning & Adding Poisson Processes5 26-34 Comparing Poisson Processes6 35-38 Estimating Software ReliabilityB 7 39-48 Compound Poisson Processes8 49-52 Nonhomogeneous Poisson Processes9 53-59 Interarrival Times, Nonhomogeneous Poisson Processes10 60-63 Thinning & Adding Nonhomogeneous Poisson Processes11 64-67 Comparing Nonhomogeneous Poisson ProcessesC 12 68-79 Markov Chains, Basics13 80-91 Stationary Distributions of Markov Chains14 92-97 Classification of States of Markov ChainsD 15 98-102 Expected Time in Transient States of Markov Chains16 103-108 Limiting Distributions, Markov Chains17 109-112 Random Walks18 113-124 Gambler's RuinE 19 125-130 Brownian Motion, Basics20 131-138 Brownian Motion, Advanced21 139-150 Brownian Motion with Drift22 151-157 Geometric Brownian Motion23 158-165 Important Formulas and IdeasF 166-189 Solutions <strong>to</strong> Problems, Sections 1 <strong>to</strong> 11G 190-223 Solutions <strong>to</strong> Problems, Sections 12 <strong>to</strong> 221All references are <strong>to</strong> the Sixth Edition.2Note that problems include both some written by me and some from past exams. The latter are copyright by theSociety of Actuaries and the Casualty Actuarial Society and are reproduced here solely <strong>to</strong> aid students in studyingfor exams. The solutions and comments are solely the responsibility of the author; the SOA and CAS bear noresponsibility for their accuracy. While some of the comments may seem critical of certain questions, this isintended solely <strong>to</strong> aid you in studying and in no way is intended as a criticism of the many volunteers who workextremely long and hard <strong>to</strong> produce quality exams.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 2Course 3 Exam Questions by Section of this Study Aid 3Section Sample 5/00 11/00 5/01 11/0112 10 1134 2 23 295 667 10 4 198910 371112 26 2913 33 40 3 4 7 2 214151617181920 152122 27The CAS/SOA did not release the 5/02 exam.3Excluding questions that are no longer on the syllabus.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 3Section 1, Introduction: 4Assume we let X(t) = the surplus of the Sari Insurance Company at time t.Then as time changes the surplus changes randomly.This is an example of a S<strong>to</strong>chastic Process.For each time t, X(t) is a random variable.If we only look at the surplus at each year end, then this would be a discrete-time s<strong>to</strong>chasticprocess. If instead we were able <strong>to</strong> examine the surplus at any point in time, this would be acontinuous-time s<strong>to</strong>chastic process. Generally, continuous-time processes can beapproximated by discrete-time processes, by taking very small time intervals in a discretetime process. For example, the difference between being able <strong>to</strong> examine the surplus of theSari Insurance Company at the end of each day or at any time is unlikely <strong>to</strong> be of anypractical importance.A s<strong>to</strong>chastic process {X(t), t ∈ T} is a collection of random variables.T is the index set of the s<strong>to</strong>chastic process.So if one can only look at the surplus at each year end, we would have T = {1, 2, 3,...} in unitsof years. We would have corresponding random variables X(1), X(2), X(3) , ..., the observedamounts of surplus at years end. If instead we were able <strong>to</strong> examine the surplus at any pointin time, we would have T = {t >0} and X(t), t >0.In the Surplus example, - ∞ < X(t) < ∞, since the surplus can (in theory) be any real number. 5The set of possible values for the random variables is called the state space of thes<strong>to</strong>chastic process. For the surplus example, the state space is the set of real numbers. 6Exercise: The price of s<strong>to</strong>ck at the close of business each day is P(t). What type of s<strong>to</strong>chasticprocess is this? What is the state space? What is the index set?[Solution: This is a discrete-time process. The state space is the positive real numbers. 7Theindex set is the positive integers (in units of days.)]In a s<strong>to</strong>chastic model one must specify the form of the random variables X(t). For example,one could assume the price of a s<strong>to</strong>ck follows a Geometric Brownian motion, sometimescalled a lognormal random walk, <strong>to</strong> be discussed subsequently. In that case, the price of thes<strong>to</strong>ck after t days is S(t) = S(0) exp(X 1 + X 2 + ...+X t ) =S(0)exp(X 1 )exp( X 2 ) ...exp(X t ), where X 1 , X 2 , ..., X t , are independent identically distributednormal variables, each with mean µ and standard deviation σ.4Many students will get a better understanding of some s<strong>to</strong>chastic processes by learning how <strong>to</strong> simulate them.See “Mahler’s <strong>Guide</strong> <strong>to</strong> Simulation.”5Small or negative amounts of Surplus would indicate an insurer in serious trouble or insolvent.6Ignoring as usual, that the smallest unit of currency is $.01.7Ignoring that S<strong>to</strong>ck Prices are quoted in some smallest unit.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 4Section 2, Poisson Processes 8A (homogeneous) Poisson Process has a constant claims intensity λ withindependent increments. The number of claims 9observed in time interval(0, T) 10 is given by the Poisson Distribution with mean Tλ.For example, assume we have a Poisson Process on (0,5) with λ = .03. Then the <strong>to</strong>tal numberof claims is given by a Poisson Distribution with mean (5)(.03) = 0.15.Exercise: For a Poisson Process with λ = .7, what is the chance of exactly 3 claims by time 2?[Solution: Poisson Distribution with mean: (2)(.7) = 1.4. f(3) = 1.4 3 e -1.4 /3! = 11.3%.]Thus if you understand the Poisson frequency distribution 11 , you understand the(homogeneous) Poisson Process. However, in the case of a (homogeneous) PoissonProcess one normally keeps track of both the <strong>to</strong>tal number of claims and the times they eachoccurred. If one had three claims, one would also want <strong>to</strong> know the three times at which theyoccurred.Mathematical Assumptions:The specific mathematical assumptions for a Poisson Process on the interval (0, T) withclaims intensity λ, are:1. The process starts at time = 0; at time = zero there are a <strong>to</strong>tal of zero claims.2. The number of claims occurring in disjoint subintervals of (0, T) are independent. 123. The mean number of claims expected in any subinterval of (0, T) is λ times the widthof the subinterval. 134. As a subinterval gets very small, the chance of more than one claim occurring in thatsubinterval quickly goes <strong>to</strong> zero.Prob[ more than one claim in interval of length h] / h, goes <strong>to</strong> zero as h goes <strong>to</strong> zero. 148See Section 5.3 of an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross. Also see Section 6.4.1 of Loss<strong>Models</strong>, not on the syllabus.9Ross refers <strong>to</strong> “events.” I will usually refer <strong>to</strong> “claims”, which is the most common application of these ideas foractuaries.10Note that by changing the time scale and therefore the claims intensity, one can always reduce <strong>to</strong> amathematically equivalent situation where the interval is (0,1) .11See “Mahler’s <strong>Guide</strong> <strong>to</strong> Frequency Distributions.”12Increments are independent.13Increments are stationary, with claims intensity lambda.14P[N(h) ≥ 2] = o(h).

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 5Independence of Claim Times:Exercise: Assume we know a claim from a Poisson Process has occurred on the interval(0, T). What is the distribution of the time of that claim?[Solution: Since the claims intensity is a constant, the claim time is uniformly distributed on(0,T).]If we know we have a <strong>to</strong>tal of n claims from a Poisson Process on (0,T), thenthe n claim times are independently uniformly distributed on (0,T), due <strong>to</strong> theconstant independent claims intensity. 15For example, assume we have a Poisson Process on (0,5) and we observe 4 claims. Thenthe 4 times of the claims are independent and each is uniform on (0,5).Exercise: Claims follow a Poisson process. Harry, Hermione, and Ron each make a claimsometime during the period 0 <strong>to</strong> 100. If Harry’s claim is at time 37 and Hermione’s claim is attime 82, what is the chance that Ron’s claim occurs between the other two?[Solution: The three claim times are independent. Ron’s claim time is uniform on (0, 100).The probability that it is in (37, 82) is: (87 - 32)/100 = 45%.]A similar result applies if we know the nth claim occurred at time S n . Then the arrival times ofthe first n-1 claims are uniformly distributed on (0,S n ) 16 . For example, assume we have aPoisson Process and we observe the 6th claim at time 1.7564. Then the times of the first fiveclaims are independent and each is uniform on (0, 1.7564).We may wish <strong>to</strong> order the claim times. If we know we have a <strong>to</strong>tal of n claims from a PoissonProcess on (0,T), then we get the same distribution as the order statistics for a uniformdistribution on (0,T). 17Specifically, the distribution function of the r th earliest claim out of N isgiven by a sum of binomial terms involving the distribution and survival functions of theuniform distribution on (0,T):N ( N ) N ( N )H r (x) = ∑ ( ) F(x) j S(x) N-j = ∑ ( ) (x/T) j (1-x/T) N-jj = r ( j ) j = r ( j )Exercise: Assume we have a Poisson Process on (0,10) and we observe 7 claims. What isthe distribution for the time of the fifth earliest claim?[Solution: Use the above formula with r=5, N =7 and T = 10:7 ( 7 )∑ ( ) (x/10) j (1-x/10) 7-j = 21(x/10) 5 (1-x/10) 2 + 7(x/10) 6 (1-x/10) + (x/10) 7 .j = 5 ( j )Comment: The rth order statistic can also be written as: β(r, N+1-r; F(x)) = β(5, 3; x/10).]15Symmetry establishes that each claim time is uniformly distributed on (0,T). Due <strong>to</strong> independent increments theclaim times are independent. See p. 265 in an Introduction <strong>to</strong> Probability <strong>Models</strong> .16See Proposition 5.4 in an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross.17See Theorem 5.2 in an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 6Exercise: Assume we have a Poisson Process on (0,10) and we observe 7 claims. What isthe probability that the time of the fifth earliest claim is less than 6.5?[Solution: The distribution for the time of the fifth earliest claim is:21(x/10) 5 (1-x/10) 2 + 7(x/10) 6 (1-x/10) + (x/10) 7 =21(.65) 5 (.35) 2 + 7(.65) 6 (.35) + (.65) 7 = .2985 + .1848 + .0490 = .5323 .Comment: β(5, 3; x/T) = β(5, 3; .65) = .5323. ]Order Statistics 18 :Assume one draws 7 independent claims from the distribution function F(x). Then the chancethat all the claims will be less than or equal <strong>to</strong> 1000, is F(1000) 7 . Therefore, the chance thatthe maximum of the 7 claims is less than or equal <strong>to</strong> 1000 is F(1000) 7 .In general, given N claims, the chance that the maximum claim is less than or equal <strong>to</strong> x is:F(x) N . This is an example of an order statistic. In general one wants <strong>to</strong> find the distribution (orcorresponding probability density) function for the rth ordinal out of N claims. The distributionfor the Nth ordinal out of N claims is: H N (x) = F(x) N .Exercise: N independent claims are drawn from the distribution F(x). What is the chance thatthe second largest of N claims is less than or equal <strong>to</strong> x?[Solution: If the second largest of N claims (the N-1 ordinal) is less than x, then there are twodisjoint possibilities; either exactly N-1 claims are less than or equal <strong>to</strong> x or exactly N claimsare less than or equal <strong>to</strong> x. Each of these possibilities has a probability given by a binomialterm. The probability that exactly N-1 claims out of N are less than or equal <strong>to</strong> x is:NF(x) N-1 {1-F(x)} = NF(x) N-1 S(x). The probability that exactly N claims out of N are less than orequal <strong>to</strong> x is: F(x) N . Thus the distribution for the second largest of N claims is:H N-1 (x) = F(x) N + NF(x) N-1 S(x).]In general the distribution function of the r th smallest claim out of N is given by a sum ofbinomial terms involving the distribution and tail probability functions of claims 19 :N ( N ) r -1 ( N )H r (x) = ∑ ( ) F(x) j S(x) N-j = 1 - ∑ ( ) F(x) j S(x) N-jj = r ( j ) j = 0 ( j )Exercise: What is the distribution function of the 6th smallest claim out of 9 independentclaims?[Solution: H 6 (x) = 84F(x) 6 S(x) 3 + 36F(x) 7 S(x) 2 + 9F(x) 8 S(x) + F(x) 9 .]18See for example page 57 of an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross, not on the syllabus, orKendall’s Advanced Theory of Statistics, Volume 1 (1994) by Stuart & Ord, or Introduction <strong>to</strong> MathematicalStatistics by Hogg & Craig.19Where the survival function S(x) = 1 - F(x).

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 7While one can get the probability density function of the rth claim out of N by differentiatingthe above distribution function, it is easier <strong>to</strong> do so from first principles. For example, what isthe density function at x of the 6th smallest claim out of 9? If the 6th smallest claim is x, whichhas probability f(x), then there are 6-1 = 5 claims smaller than x, with probability F(x) 5 and9 - 6 = 3 claims larger than x, with probability S(x) 3 .Multiplying the different probabilities, ignoring the number of combinations, gives a densityfunction proportional <strong>to</strong>: F(x) 5 S(x) 3 f(x) = F(x) 5 (1-F(x)) 3 F′(x). If one makes a change ofvariables y = F(x), then this is proportional <strong>to</strong> (the density of) a Beta Distribution 20 :y 5 (1-y) 3 / β(6, 4).In general, the probability density function of the r th smallest claim out of N is given by:h r (x) = F(x) r-1 S(x) N-r f(x) / β(r, N+1-r) = F(x) r-1 S(x) N-r f(x) N!/{(r-1)! (N-r)!}Thus the Distribution Function of the r th smallest claim out of N can also be written as a BetaDistribution with respect <strong>to</strong> F(x), with parameters r and N+1-r:H r (x) = β(r, N+1-r; F(x))Exercise: What is the probability density function of the 3rd smallest claim out of 10 claims?[Solution: h 3 (x) = F(x) 3-1 S(x) 10-3 f(x) / β(3, 10+1-3) = F(x) 2 S(x) 7 f(x) / β(3, 8) =F(x) 2 S(x) 7 f(x) (3+8-1)!/ {(3-1) ! (8-1)!} = 360 F(x) 2 S(x) 7 f(x).]Exercise: What is the distribution function of the smallest claim out of 7 claims?[Solution: If the smallest out of x claims is larger than x, then all the claims are. This hasprobability S(x) 7 . Therefore the chance that the smallest claim is less than or equal <strong>to</strong> x isH 1 (x) = 1 - S(x) 7 .Note that one can also get the same answer by using one of the general formulas:1 -1 ( 7 )H 1 (x) = 1 - ∑ ( ) F(x) j S(x) 7-i = 1 - S(x) 7 .]j = 0 ( j )Exercise: 7 independent claims are drawn from a Pare<strong>to</strong> distribution,F(x) = 1 - (θ/(θ+x)) α . What is the distribution function of the smallest claim out of 7 claims?[Solution: S(x) = 1 -F(x) = (θ/(θ+x)) α . H 1 (x) = 1 - S(x) 7 = 1 - (θ/(θ+x)) 7α .]Exercise: 7 independent claims are drawn from a Pare<strong>to</strong> distribution, with α = 3 and θ = 100.What is the probability that the smallest claim out of these 7 claims is greater than 15?[Solution: H 1 (x) = 1 - S(x) 7 = 1 - (θ/(θ+x)) 7α . 1 - H 1 (15) = (100/(100+15)) 21 = 5.3%. ]20See “Mahler’s <strong>Guide</strong> <strong>to</strong> Loss Distributions.” The complete Beta function β(a,b) = (a-1)!(b-1)!/(a+b-1)!.As stated in “Mahler’s <strong>Guide</strong> <strong>to</strong> Frequency Distributions”, the Distribution Function of the Binomial Distribution withparameters m and q, is the Beta Distribution, β(m-x, x+1; 1-q). Therefore,Hr(x) = 1 - β(N-(r-1) , (r-1) + 1 ; 1-F(x)) = 1 - β(N+1-r , r ; 1-F(x)) = β(r, N+1-r; F(x)).

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 8Counting Processes 21 :A s<strong>to</strong>chastic process is a counting process if:1. Its state space is the nonnegative integers.2. It is nondecreasing with time.So a counting process is what an actuary would call a claims frequencyprocess. N(t) is the number of claims 22that have occurred by time t. N(t) - N(s) is the numberof claims that have occurred in the interval (s,t]. A Poisson Process is an example of acounting process.A claims frequency process has independent increments if the number of claims intwo disjoint periods of time are independent of each other. For example, for practicalpurposes the number of dental claims a large insurer gets this week are probablyindependent of the number of dental claims it gets next week. Thus we could model thisfrequency process with independent increments. However, the number of claims for the fluthis week might be correlated with the number of claims for the flu last week.A claims frequency has stationary increments if the number of claims expected in any timeinterval is proportional <strong>to</strong> the length of that interval. Stationary increments are equivalent <strong>to</strong> aconstant claims intensity.A (homogeneous) Poisson Process has stationary and independentincrements. If exposure levels are changing, then we would be unlikely <strong>to</strong> have stationaryincrements and therefore unlikely <strong>to</strong> have a (homogeneous) Poisson Process.21See Section 5.3.1 of an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross.22Ross uses “events.” In actuarial applications an event is usually, but not always, a claim.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 9Mixing Poisson Processes:For example, assume that the number of s<strong>to</strong>rms during a year is given by a Poisson Process.However, during “good” years, λ(t) = 10, while during “bad” years λ(t) = 25. Assume furtherthat good and bad years occur at random, with each year independent of the others. Assume2/3 of years are good and 1/3 are bad.Then if we know whether a year is good or bad, then the number of claims during that year isPoisson Distributed with mean either 10 or 25. In any case, within any year, the process hasstationary and independent increments.Over the long term, the expected number of s<strong>to</strong>rms per year is: (2/3)(10) + (1/3)(25) = 15.The chance of a year picked at random having n s<strong>to</strong>rms is:(2/3)(e -10 10 n / n!) + (1/3)(e -25 25 n / n!), a weighted average of the densities of the twoPoisson Distributions. The resulting distribution is not a Poisson. 23Over the long term, the increments are neither stationary nor independent. If one hasobserved a large number of s<strong>to</strong>rms over the first half of a year, one is more likely <strong>to</strong> be in a“bad” year and thus see more s<strong>to</strong>rms over the remainder of the year. 24Exercise: In the above example, what is the chance of observing exactly 9 s<strong>to</strong>rms over thefirst half of a year?[Solution: If it is good year, the number of s<strong>to</strong>rms over the first half year is Poisson with mean5. Thus the chance of observing 9 s<strong>to</strong>rms is e -5 5 9 / 9! = 3.63%. If instead it is bad year, thenumber of s<strong>to</strong>rms over the first half year is Poisson with mean 12.5. Thus the chance ofobserving 9 s<strong>to</strong>rms is e -12.5 12.5 9 / 9! = 7.65%. Therefore, the a priori chance of observing 9s<strong>to</strong>rms over the first half year is: (2/3)(3.63%) + (1/3)(7.65%) =4.97%.]Exercise: In the above example, assume you have seen 9 s<strong>to</strong>rms over the first half of a year.What is the posterior chance of it being a good year? Use Bayes Theorem. 25[Solution: The a priori chance of a good year is 2/3. If it is good year, the chance of observing9 s<strong>to</strong>rms is 3.63%. The a priori chance of observing 9 s<strong>to</strong>rms over the first half year is 4.97%.Thus using Bayes Theorem, the posterior chance of it being a good year is (2/3)(3.63%)/4.97% = 48.7%. Similarly, the posterior chance of it being a bad year is (1/3)(7.65%)/ 4.97% =51.3%.]Exercise: In the above example, assume you have seen 9 s<strong>to</strong>rms over the first half of a year.How many s<strong>to</strong>rms do you expect <strong>to</strong> see of the final half of the year?[Solution: The posterior chance of it being a good year is 48.7%. The posterior chance of itbeing a bad year is 51.3%. If it is a good year, we expect <strong>to</strong> see 5 s<strong>to</strong>rms over the next halfyear. If it is a bad year, we expect <strong>to</strong> see 12.5 s<strong>to</strong>rms over the next half year.Thus the expected number of s<strong>to</strong>rms over the next half year is (.487)(5) + (.513)(12.5) = 8.85.]23See “Mahler’s <strong>Guide</strong> <strong>to</strong> Frequency Distributions.”24See Exercise 64 on page 299 of Introduction <strong>to</strong> Probability <strong>Models</strong>.25Bayes Theorem is discussed with Credibility on Course 4. See Theorem 2.16 in Loss <strong>Models</strong>.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 10o(h)A function f(x) is said <strong>to</strong> be o(h), if the limit as h approaches zero of f(h)/h is zero. 26In other words as h approaches zero, f(h) goes <strong>to</strong> zero more quickly than h. For example, f(x)= x 1.5 is o(h). Thus x is of lower order of magnitude than x 1.5 .On the other hand, √x is not o(h).For a Poisson Process, the chance of having more than 1 claim in an interval of length h, iso(h). In other words, as the length of an interval approaches zero, the chance of having morethan one claim in that interval also approaches zero, faster than the length of that intervalapproaches zero.Prob[ more than one claim in an interval of length h]/h, goes <strong>to</strong> zero as h goes <strong>to</strong> zero.For a Poisson Process, the chance of having 1 claim in an interval of length h, isλh + o(h). In other words, as h goes <strong>to</strong> zero,Prob[one claim in interval of length h]/h, goes <strong>to</strong> λ as h goes <strong>to</strong> zero.A function f(x) is equivalent <strong>to</strong> x as x goes <strong>to</strong> zero, f(x) ~ x, if the limit as h approaches zero off(h)/h is one. For example, sin(x) ~ x, as x approaches zero.A function f(x) is said <strong>to</strong> be O(h), if there is a positive constant K, such that for all sufficientlysmall h, |f(h)/h| ≤ K. For example, f(x) = x(1 + a/x) x is O(h), since the limit as x goes <strong>to</strong> zero of(1 + a/x) x is e a . If a function is either o(h) or equivalent <strong>to</strong> h as h goes zero, then it is also O(h).26See Definition 5.2 of an Introduction <strong>to</strong> Probability <strong>Models</strong> by Sheldon M. Ross.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 11Problems:2.1 (1 point) A Poisson Process has a claims intensity of 0.3.What is the probability of exactly 2 claims from time 0 <strong>to</strong> time 10?A. 22% B. 24% C. 26% D. 28% E. 30%2.2 (1 point) A Poisson Process has a claims intensity of 0.3.Given that there have been 2 claims from time 0 <strong>to</strong> time 10, what is the probability of exactly 2claims from time 10 <strong>to</strong> time 20?A. 22% B. 24% C. 26% D. 28% E. 30%2.3 (3 points) A Poisson Process has a claims intensity of 0.3.Given that there have been 2 claims from time 0 <strong>to</strong> time 10, what is the probability of exactly 2claims from time 6 <strong>to</strong> time 16?A. 19% B. 21% C. 23% D. 25% E. 27%2.4 (1 point) A Poisson Process has a claims intensity of .15.One observes two claims during the time interval (0, 5).What is the probability that the first claim occurs before time 1?A. 36% B. 37% C. 38% D. 39% E. 40%2.5 (3 points) Claims occur via a Poisson Process with unknown constant intensity λ.Claims are reported after a lag. The lag from occurrence <strong>to</strong> report is given by an ExponentialDistribution with a mean of .6. 480 claims that occurred between time 0 and time 1 havebeen reported by time 1.25. Estimate λ.A. Less than 680B. At least 680, but less than 690C. At least 690, but less than 700D. At least 700, but less than 710E. At least 7102.6 (1 point) A Poisson Process has λ = 0.6.What is the probability of exactly 3 claims from time 5 <strong>to</strong> time 9?A. 19% B. 21% C. 23% D. 25% E. 27%2.7 (3 points) A Poisson Process λ = 0.6.If there are three claims from time 2 <strong>to</strong> time 8, what is the probability of exactly 3 claims fromtime 5 <strong>to</strong> time 9?A. 19% B. 21% C. 23% D. 25% E. 27%2.8 (2 points) Claims are given by a Poisson Process with λ = 7. What is probability that thenumber of claims between time 5 and 15 is at least 60 but no more than 80?Use the Normal Approximation.(A) 73% (B) 75% (C) 77% (D) 79% (E) 81%

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 12Use the following information for the next two questions:The android Data is stranded on the planet Erehwon.• Data uses energy uniformly at a rate of 10 gigajoules per year.• If Data’s s<strong>to</strong>red energy reach 0, he ceases <strong>to</strong> function.• Data gets his energy from dilithium crystals.• Data gets 6 gigajoules of energy from each dilithium crystal.• Data finds dilithium crystals at a Poisson rate of 2 per year.• Data can s<strong>to</strong>re dilithium crystals without limit until needed.• Data currently has 8 gigajoules of energy s<strong>to</strong>red.2.9 (4 points) What is the probability that Data ceases <strong>to</strong> function within the next 2.5 years?(A) 30% (B) 33% (C) 36% (D) 39% (E) 42%2.10 (3 points) What is the expected number of gigajoules of energy found by Data in thenext 2.5 years?(A) 20 (B) 22 (C) 24 (D) 26 (E) 28Use the following information for the next four questions:Claims follow a Poisson Process with λ = 81.Bob and Ray each make a claim during the year 2002.2.11 (1 point) What is the probability that Ray made his claim before Bob?(A) 1/16 (B) 1/6 (C) 1/4 (D) 1/3 (E) 1/22.12 (1 point) What is the probability that Ray made his claim during the first quarter of 2002?(A) 1/16 (B) 1/6 (C) 1/4 (D) 1/3 (E) 1/22.13 (1 point) What is the probability that Bob and Ray each made their claims during the lastquarter of 2002?(A) 1/16 (B) 1/6 (C) 1/4 (D) 1/3 (E) 1/22.14 (1 point) If Ray made his claim on July 23, 2002, what is the probability that Bob madehis claim during May or June 2002?(A) 1/16 (B) 1/6 (C) 1/4 (D) 1/3 (E) 1/22.15 (3 points) Claims are given by a Poisson Process with λ = 7. What is probability that thenumber of claims between time 5 and 11 is greater than the number of claims from time 11 <strong>to</strong>15? Use the Normal Approximation.(A) 87% (B) 89% (C) 91% (D) 93% (E) 95%2.16 (3 points) Claims are given by a Poisson Process with λ = 5. What is probability that thenumber of claims between time 2 and 10 is greater than the number of claims from time 7 <strong>to</strong>16? Use the Normal Approximation.(A) 17% (B) 19% (C) 21% (D) 23% (E) 25%

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 132.17 (1 point) Claims are given by a Poisson Process. The fifth loss occurred at time 31.What is the chance that the first loss occurred by time 18?(A) 95% (B) 96% (C) 97% (D) 98% (E) 99%2.18 (2 points) Claims are given by a Poisson Process. The fifth loss occurred at time 31.What is the chance that the second loss occurred by time 18?(A) 74% (B) 76% (C) 78% (D) 80% (E) 82%2.19 (2 points) Claims are given by a Poisson Process. The fifth loss occurred at time 31.What is the chance that the third loss occurred by time 18?(A) 40% (B) 42% (C) 44% (D) 46% (E) 48%2.20 (1 point) A Poisson Process has a claims intensity of 0.4 per day. How many wholenumber of days do we need <strong>to</strong> observe, in order <strong>to</strong> have at least a 95% probability of seeingat least one claim?(A) 8 (B) 9 (C) 10 (D) 11 (E) 122.21 (2 points) A Poisson Process has a claims intensity of 0.4 per day. How many wholenumber of days do we need <strong>to</strong> observe, in order <strong>to</strong> have at least a 95% probability of seeingat least two claims?(A) 11 (B) 12 (C) 13 (D) 14 (E) 152.22 (2 points) Claims are received by the Symphonic Insurance Company via a PoissonProcess with mean .017. During the time interval (0, 100) it receives three claims, one fromBeethoven, one from Tchaikovsky, and one from Mahler. The claim from Beethoven wasreceived at time 27 and the claim from Mahler was received at time 91. What is probabilitythat the claim from Tchaikovsky was received between the other two claims?(A) 64% (B) 66% (C) 68% (D) 70% (E) 72%Use the following information for 3, 11/01 questions 10 and 11:For a tyrannosaur with 10,000 calories s<strong>to</strong>red:(i) The tyrannosaur uses calories uniformly at a rate of 10,000 per day.If his s<strong>to</strong>red calories reach 0, he dies.(ii) The tyrannosaur eats scientists (10,000 calories each) at a Poisson rate of 1 per day.(iii) The tyrannosaur eats only scientists.(iv) The tyrannosaur can s<strong>to</strong>re calories without limit until needed.2.23 (3, 11/01, Q.10) (2.5 points)Calculate the probability that the tyrannosaur dies within the next 2.5 days.(A) 0.30 (B) 0.40 (C) 0.50 (D) 0.60 (E) 0.702.24 (3, 11/01, Q.11) (2.5 points)Calculate the expected calories eaten in the next 2.5 days.(A) 17,800 (B) 18,800 (C) 19,800 (D) 20,800 (E) 21,800

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 14Section 3, Interarrival Times, Poisson ProcessesExercise: What is the probability that the waiting time until the first claim is less than or equal<strong>to</strong> 10 for a Poisson Process with λ = .03?[Solution: The number of claims by time 10 is Poisson with mean: (10)(.03) = 0.3.Waiting time is ≤ 10 ⇔ At least one claim by t = 10. Prob[0 claims by time 10] = e -0.3 .Prob[1 or more claims by time 10] = 1 - e -0.3 = 25.9%.]In this case, the distribution function of the waiting time until the first claim is:F(t) = 1 - e -.03t , an Exponential Distribution with mean 1/.03. In general, for a Poisson Processwith claims intensity λ, the waiting time until the first claim has an ExponentialDistribution with mean 1/λ.Interarrival Times:The interarrival times are the times between claims. T 1 is the waiting time until the firstclaim. T 2 is the time from the first claim until the second claim. T 3 is the time from the secondclaim until the third claim, etc.Exercise: What is the probability that the waiting time from the third claim <strong>to</strong> the fourth claim isless than or equal <strong>to</strong> 10 for a Poisson Process with λ = .03?[Solution: Interarrival time from 3rd <strong>to</strong> 4th claim ≤ 10 ⇔ # claims ≥ 1 in interval of length 10.The number of claims over a time interval of length 10 is Poisson with mean: (10)(.03) = 0.3.Prob[0 claims] = e -0.3 . Prob[1 or more claims] = 1 - e -0.3 = 25.9%.]In general, the interarrival time between claim n and n+1 has an Exponential Distribution withmean 1/λ. Due <strong>to</strong> the constant, independent claims intensity, we can start a new PoissonProcess, with claims intensity λ, when the nth claim occurs; therefore, the wait until the nextclaim is Exponential with mean 1/λ. This interarrival time is independent of what happenedbefore. For a Poisson Process with claims intensity λ, the interarrival times areindependent Exponential Distributions each with mean 1/λ.For example, assume we have a Poisson Process with λ = .03, with an unrestricted timehorizon. Then the waiting time <strong>to</strong> the first claim is Exponential, with θ = 1/.03 = 33.33. Thesecond interarrival time is an independent Exponential, with θ = 33.33.Each interarrival time is an independent Exponential, with θ = 33.33.Waiting Times:The waiting time until the second claim is the sum of the waiting time for the first claim, plusthe interarrival time from the first <strong>to</strong> the second claim. Thus the waiting time until the secondclaim is the sum of two independent Exponential Distributions, each with mean 1/λ.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 15The waiting time until the nth claim is the sum on n independent Exponential Variables, eachwith mean 1/λ. Therefore, the waiting time until the nth claim follows a GammaDistribution with parameters 27 α = n and θ = 1/λ. The mean time until the nth claim isn/λ. Note that if we restrict the Poisson Process <strong>to</strong> (0,T), then there may be fewer than nclaims; in other words the time until the nth claim could be greater than T.For example, assume we have a Poisson Process with λ = .03, with an unrestricted timehorizon. The waiting time until the 4th claim is given by a Gamma Distribution, as per Loss<strong>Models</strong>, with parameters α = 4 and θ = 33.33. The mean waiting time until the 4th claim is themean of the Gamma Distribution, αθ = (4)(33.33) = 133.33.Exercise: Assume we have a Poisson Process with λ = .03. What is the probability that wehave observed at least 4 claims by time 100?[Solution: The waiting time until the fourth claim is given by a Gamma Distribution with α = 4and θ = 33.33. Thus F(100) = Γ[4; 100/33.33] = Γ[4; 3] = 0.352768, by computer.Alternately, the number of claims in the time period from 0 <strong>to</strong> 100 is Poisson Distributed withmean (.03)(100) = 3. Therefore, the chance of zero claims in this interval is e -3 . The chance ofone claim in this time interval is 3e -3 . The chance of two claims in this time interval is 3 2 e -3 /2.The chance of three claims in this time interval is 3 3 e -3 /6. Thus the chance of at least 4 claimsin the time interval is: 1 - {e -3 + 3e -3 + 3 2 e -3 /2 + 3 3 e -3 /6 } = 1 - .647232 = 0.352768.]In general, assume claims are given by a Poisson Process with claims intensity λ. Then theclaims in the interval from (0, t) are Poisson Distributed with mean tλ. One can calculate thechance that there are least n claims in two different ways. First, the chance of at least n claimsis a sum of Poisson densities:n -1 ∞1 - F(n-1) = 1 - Σ e −λt λt i / i! = Σ e −λt λt i / i!.i = 0 i = nOn the other hand, the waiting time until the nth claim is a Gamma Distribution with α = n andθ = 1/ λ. Thus the waiting time until the nth claim has distribution Γ[n ; λ t].A Formula for the Incomplete Gamma Function;Comparing the two results when t = 1, the Incomplete Gamma Function with integer shapeparameter can be written in terms of a sum of Poisson densities 28 :n -1 ∞Γ[n ; λ ] = 1 - Σ e −λ λ i / i! = Σ e −λ λ i / i!.i = 0 i = nFor example, Γ[3; 3.5] = 1 - {e -3.5 + 3.5e -3.5 + 3.5 2 e -3.5 /2} = 1 - .320847 = .679153.27As per Appendix A of Loss <strong>Models</strong>.28See Theorem A.1 on page 570 in Appendix A of Loss <strong>Models</strong>.

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 16Problems:3.1 (1 point) A Poisson Process has a claims intensity of .05.What is the mean time until the first claim?A. 5 B. 10 C. 15 D. 20 E. 253.2 (1 point) A Poisson Process has a claims intensity of .05.What is the mean time until the tenth claim?A. 50 B. 100 C. 200 D. 300 E. 4003.3 (1 point) A Poisson Process has a claims intensity of .05.What is the probability that the time until the first claim is greater than 35?A. Less than 14%B. At least 14%, but less than 15%C. At least 15%, but less than 16%D. At least 16%, but less than 17%E. At least 17%3.4 (1 point) A Poisson Process has a claims intensity of .05. What is the probability that thetime from the fifth claim <strong>to</strong> the sixth claim is less than 10?A. Less than 36%B. At least 36%, but less than 38%C. At least 38%, but less than 40%D. At least 40%, but less than 42%E. At least 42%3.5 (2 points) A Poisson Process has a claims intensity of .05. What is the probability that thetime from the eighth claim <strong>to</strong> the tenth claim is greater than 50?A. Less than 28%B. At least 28%, but less than 30%C. At least 30%, but less than 32%D. At least 32%, but less than 34%E. At least 34%3.6 (2 points) For a claim number process you are given that the elapsed times betweensuccessive claims are mutually independent and identically distributed with distributionfunction: F(t) = 1 - e -t/2 , t ≥ 0.Determine the probability of exactly 3 claims in an interval of length 7.A. Less than 23%B. At least 23%, but less than 25%C. At least 25%, but less than 27%D. At least 27%, but less than 29%E. At least 29%

<strong>HCMSA</strong>-<strong>F02</strong>-3-<strong>2A</strong>, S<strong>to</strong>chastic <strong>Models</strong>, 6/2/02, Page 173.7 (2 points) Claims follow a Poisson Process. The average time between claims is 5.What is the probability that we have observed at least 2 claims by time 9?A. Less than 53%B. At least 53%, but less than 55%C. At least 55%, but less than 57%D. At least 57%, but less than 59%E. At least 59%3.8 (2 points) Claims follow a Poisson Process. The average time between claims is 5.What is the probability that we have observed exactly 2 claims by time 9?A. Less than 23%B. At least 23%, but less than 25%C. At least 25%, but less than 27%D. At least 27%, but less than 29%E. At least 29%3.9 (1 point) Claims occur via a homogeneous Poisson Process. The expected waiting timeuntil the first claim is 770 hours. If the claims intensity had been 5 times as large, what wouldhave been the expected waiting time until the first claim?A. 154 hours B. 765 hours C. 770 hours D. 3850 hours E. None of the above.3.10 (2 points) For a Poisson Process with λ = 5. What is the probability that we haveobserved at least 3 claims by time 1.2?A. Less than 93%B. At least 93%, but less than 95%C. At least 95%, but less than 97%D. At least 97%, but less than 99%E. At least 99%3.11 (Course 151 Sample Exam #2, Q.7) (0.8 points)For a claim number process {N(t), t ≥ 0} you are given that the elapsed times betweensuccessive claims are mutually independent and identically distributed with distributionfunctionF(t) = 1 - e -3t , t ≥ 0.Determine the probability of exactly 4 claims in an interval of length 2.(A) 0.11 (B) 0.13 (C) 0.15 (D) 0.17 (E) 0.19