ASPE at a Glance - Section 1601 - BDO Canada

ASPE at a Glance - Section 1601 - BDO Canada

ASPE at a Glance - Section 1601 - BDO Canada

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

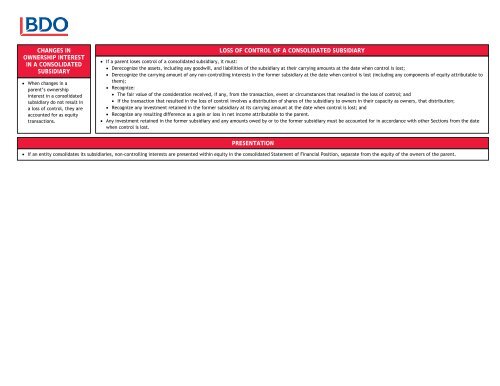

CHANGES INOWNERSHIP INTERESTIN A CONSOLIDATEDSUBSIDIARY• When changes in aparent’s ownershipinterest in a consolid<strong>at</strong>edsubsidiary do not result ina loss of control, they areaccounted for as equitytransactions.LOSS OF CONTROL OF A CONSOLIDATED SUBSIDIARY• If a parent loses control of a consolid<strong>at</strong>ed subsidiary, it must:• Derecognize the assets, including any goodwill, and liabilities of the subsidiary <strong>at</strong> their carrying amounts <strong>at</strong> the d<strong>at</strong>e when control is lost;• Derecognize the carrying amount of any non-controlling interests in the former subsidiary <strong>at</strong> the d<strong>at</strong>e when control is lost (including any components of equity <strong>at</strong>tributable tothem);• Recognize:• The fair value of the consider<strong>at</strong>ion received, if any, from the transaction, event or circumstances th<strong>at</strong> resulted in the loss of control; and• If the transaction th<strong>at</strong> resulted in the loss of control involves a distribution of shares of the subsidiary to owners in their capacity as owners, th<strong>at</strong> distribution;• Recognize any investment retained in the former subsidiary <strong>at</strong> its carrying amount <strong>at</strong> the d<strong>at</strong>e when control is lost; and• Recognize any resulting difference as a gain or loss in net income <strong>at</strong>tributable to the parent.• Any investment retained in the former subsidiary and any amounts owed by or to the former subsidiary must be accounted for in accordance with other <strong>Section</strong>s from the d<strong>at</strong>ewhen control is lost.PRESENTATION• If an entity consolid<strong>at</strong>es its subsidiaries, non-controlling interests are presented within equity in the consolid<strong>at</strong>ed St<strong>at</strong>ement of Financial Position, separ<strong>at</strong>e from the equity of the owners of the parent.