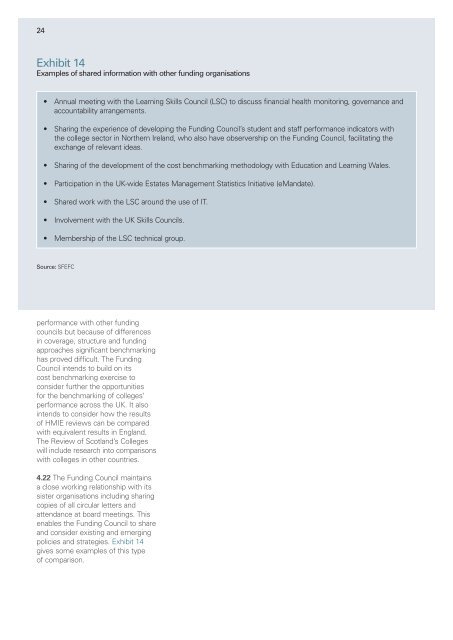

24Exhibit 14Examples of shared information with other funding organisations• Annual meeting with the Learning Skills <strong>Council</strong> (LSC) to discuss financial health monitoring, governance andaccountability arrangements.• Sharing the experience of developing the <strong>Funding</strong> <strong>Council</strong>’s student and staff performance indicators withthe college sector in Northern Ireland, who also have observership on the <strong>Funding</strong> <strong>Council</strong>, facilitating theexchange of relevant ideas.• Sharing of the development of the cost benchmarking methodology with <strong>Education</strong> and Learning Wales.• Participation in the UK-wide Estates Management Statistics Initiative (eMandate).• Shared work with the LSC around the use of IT.• Involvement with the UK Skills <strong>Council</strong>s.• Membership of the LSC technical group.Source: SFEFCperformance with other fundingcouncils but because of differencesin coverage, structure and fundingapproaches significant benchmarkinghas proved difficult. The <strong>Funding</strong><strong>Council</strong> intends to build on itscost benchmarking exercise toconsider further the opportunitiesfor the benchmarking of colleges’performance across the UK. It alsointends to consider how the resultsof HMIE reviews can be comparedwith equivalent results in England.The Review of <strong>Scotland</strong>’s Collegeswill include research into comparisonswith colleges in other countries.4.22 The <strong>Funding</strong> <strong>Council</strong> maintainsa close working relationship with itssister organisations including sharingcopies of all circular letters andattendance at board meetings. Thisenables the <strong>Funding</strong> <strong>Council</strong> to shareand consider existing and emergingpolicies and strategies. Exhibit 14gives some examples of this typeof comparison.

Appendix 1. <strong>Audit</strong> Committeerecommendations25<strong>Audit</strong> Committee recommendationsmade in each of its reports inresponse to the AGS reportsReportSeventh report 2002: Report onOverview of further educationcolleges in <strong>Scotland</strong> 2000/01.<strong>Audit</strong> CommitteerecommendationsWe recommend that the <strong>Funding</strong><strong>Council</strong> takes the concernsexpressed by the ASC into accountwhen considering further refinementand development of its financialcategorisation model.In future overview reports thecommittee will look for positiveevidence that ‘one-off’ additionalpayments have increased the paceof recovery on the colleges involved.Even within its ten-year recovery plan,Inverness College cannot state withconfidence that its financial targetswill continue to be met. We believethat this highlights the fundamentalweakness of a recovery plan ofsuch long duration. We recommendthat the <strong>Funding</strong> <strong>Council</strong> work withInverness College in particular, andother colleges as necessary, to agreeshorter timescales for achievingsustainable financial balance.We recommend that the <strong>Funding</strong><strong>Council</strong> work with colleges to developexplicit agreements on when andhow the results of the council’smanagement review will be realised.We call on the <strong>Funding</strong> <strong>Council</strong>to both publish a step-by-stepprogramme, with appropriatetimescales, for the implementationof the mapping process and toensure that the geographical andindustry sector exercises are properlycoordinated. Completion of theseprojects will form the basis forstrategic planning by colleges.We call on the <strong>Funding</strong> <strong>Council</strong>to publish the timescales for thefinalisation and implementation ofthe new Estates <strong>Funding</strong> Model.ReportFourth report 2004: SFEFC –performance management of thefurther education sector in <strong>Scotland</strong>.<strong>Audit</strong> CommitteerecommendationsAccountabilityAccounting for performance andlines of accountabilityThe committee considers that moretransparent performance information,including information about theperformance of individual colleges,should be made available to theParliament and more widely.While the committee recognisesthe role of college principals asaccountable officers, it considers thatSFEFC’s corporate plan and annualreport should be developed to includeinformation about both the sector asa whole and individual colleges.The committee therefore recommendsthat, in discussion with SEETLLDand the sector, SFEFC develops itscorporate plan to ensure that it containsobjectives, priorities and targets forthe sector and for individualcolleges. A comprehensive review ofperformance against these objectivesand targets for both the sector andindividual colleges should then be setout in SFEFC’s annual report.The committee considers that inresponding to this report, followingdiscussion with SEETLLD asappropriate, SFEFC clarifies thelines of accountability within thesector. The implementation of thecommittee’s recommendationsin regard to enhancing publishedperformance information will ensurethat such information more fullyreflects the relationship betweencolleges, SFEFC, SEETLLD andthe Parliament.EfficiencyUnit prices and unit costsThe committee considers thatwithout an adequate understandingof inputs ie, reliable unit costmeasures, SFEFC runs the risk ofeither asking colleges to do morethan they can afford or jeopardisingquality of outputs across the sector.<strong>Further</strong>more, unless funding istransparently fair and equitable it willnot be possible to identify effectivelyefficiency savings.The committee accepts that the useof unit costs is not straightforwardbut considers that they would,nevertheless, provide a valuablesource of performance informationif they were sufficiently developed.The committee considers thatSFEFC is dragging its feet on thecommitment it made following thecommittee’s 2000 report to refineand utilise unit costs. The committeetherefore recommends that SFEFCsets out a timetable by which itenvisages that it will have datawhich are of use in setting fundinglevels in a fair and equitable mannerand in accurately examining relativeefficiencies within the sector.Quality and value for moneyThe committee welcomes theintroduction of HMIE inspectionsand stresses the importance offollow-up work following eachinspection. The committee furtherwelcomes the improvements SFEFChas made to its corporate plan toallow information on the quality offurther education to be reported toministers and the Parliament.The committee was struck by thefact that, despite a wide variationin the financial health of individualcolleges, HMIE has found that almost