This self-complete checklist is designed to help you assess ... - PCG

This self-complete checklist is designed to help you assess ... - PCG

This self-complete checklist is designed to help you assess ... - PCG

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

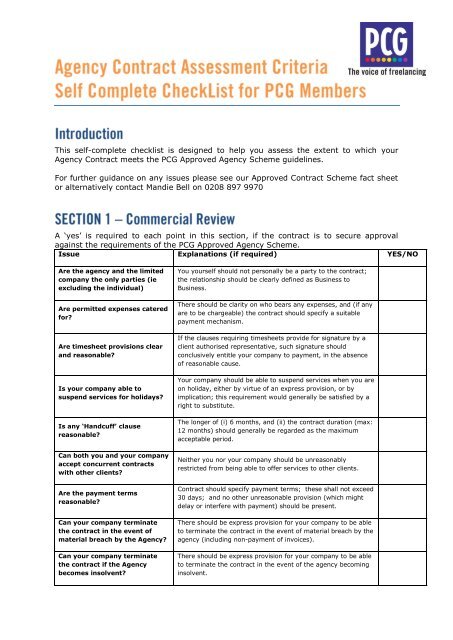

<strong>Th<strong>is</strong></strong> <strong>self</strong>-<strong>complete</strong> <strong>checkl<strong>is</strong>t</strong> <strong>is</strong> <strong>designed</strong> <strong>to</strong> <strong>help</strong> <strong>you</strong> <strong>assess</strong> the extent <strong>to</strong> which <strong>you</strong>rAgency Contract meets the <strong>PCG</strong> Approved Agency Scheme guidelines.For further guidance on any <strong>is</strong>sues please see our Approved Contract Scheme fact shee<strong>to</strong>r alternatively contact Mandie Bell on 0208 897 9970A ‘yes’ <strong>is</strong> required <strong>to</strong> each point in th<strong>is</strong> section, if the contract <strong>is</strong> <strong>to</strong> secure approvalagainst the requirements of the <strong>PCG</strong> Approved Agency Scheme.Issue Explanations (if required) YES/NOAre the agency and the limitedcompany the only parties (ieexcluding the individual)Are permitted expenses cateredfor?Are timesheet prov<strong>is</strong>ions clearand reasonable?Is <strong>you</strong>r company able <strong>to</strong>suspend services for holidays?Is any „Handcuff‟ clausereasonable?Can both <strong>you</strong> and <strong>you</strong>r companyaccept concurrent contractswith other clients?Are the payment termsreasonable?Can <strong>you</strong>r company terminatethe contract in the event ofmaterial breach by the Agency?Can <strong>you</strong>r company terminatethe contract if the Agencybecomes insolvent?You <strong>you</strong>r<strong>self</strong> should not personally be a party <strong>to</strong> the contract;the relationship should be clearly defined as Business <strong>to</strong>Business.There should be clarity on who bears any expenses, and (if anyare <strong>to</strong> be chargeable) the contract should specify a suitablepayment mechan<strong>is</strong>m.If the clauses requiring timesheets provide for signature by aclient author<strong>is</strong>ed representative, such signature shouldconclusively entitle <strong>you</strong>r company <strong>to</strong> payment, in the absenceof reasonable cause.Your company should be able <strong>to</strong> suspend services when <strong>you</strong> areon holiday, either by virtue of an express prov<strong>is</strong>ion, or byimplication; th<strong>is</strong> requirement would generally be sat<strong>is</strong>fied by aright <strong>to</strong> substitute.The longer of (i) 6 months, and (ii) the contract duration (max:12 months) should generally be regarded as the maximumacceptable period.Neither <strong>you</strong> nor <strong>you</strong>r company should be unreasonablyrestricted from being able <strong>to</strong> offer services <strong>to</strong> other clients.Contract should specify payment terms; these shall not exceed30 days; and no other unreasonable prov<strong>is</strong>ion (which mightdelay or interfere with payment) should be present.There should be express prov<strong>is</strong>ion for <strong>you</strong>r company <strong>to</strong> be able<strong>to</strong> terminate the contract in the event of material breach by theagency (including non-payment of invoices).There should be express prov<strong>is</strong>ion for <strong>you</strong>r company <strong>to</strong> be able<strong>to</strong> terminate the contract in the event of the agency becominginsolvent.

Issue Explanations (if required) YES/NOCan <strong>you</strong>r company terminatethe contract on giving notice ofa reasonable period?Are any clauses requiring <strong>you</strong> or<strong>you</strong>r company <strong>to</strong> act in the bestinterest of the clientreasonable?Are Professional Standards andperformance requirementsreasonable?Are Liability and Limitationrequirements reasonable?Are Confidentialityrequirements reasonable?Is Copyright & IntellectualProperty prov<strong>is</strong>ion adequate?Are suitable prov<strong>is</strong>ions madefor variations <strong>to</strong> contract?Is there a suitable GoverningLaw e.g. Engl<strong>is</strong>h Law, stated inthe contract?Are all other commercial termsreasonable?Your company should be able <strong>to</strong> terminate the contract with anotice period not exceeding one month.If any clauses are present that require <strong>you</strong>r company or <strong>you</strong>personally <strong>to</strong> act in the best interest of the client, they shouldnot be reasonable.Any such prov<strong>is</strong>ions should not be unreasonable.Where there <strong>is</strong> a liability prov<strong>is</strong>ion, it shall be reasonable; andwhere an amount of required or adv<strong>is</strong>ed insurance cover <strong>is</strong>specified, <strong>to</strong>tal liability shall be limited <strong>to</strong> that amount.Such prov<strong>is</strong>ions should not be unreasonable and should excludeinformation already known <strong>to</strong> <strong>you</strong> (independent of anyd<strong>is</strong>closure by the client), and should exclude information in thepublic domain.Contract should make clear that ownership of any of <strong>you</strong>r/<strong>you</strong>rcompany’s own IPR which <strong>you</strong> may intend <strong>to</strong> use with theClient’s agreement in the course of the contract should retainedby <strong>you</strong>/<strong>you</strong>r companyContract should expressly say that any change should be inwriting and signed by both parties.Contract should make clear what law <strong>is</strong> intended <strong>to</strong> apply <strong>to</strong> it.<strong>Th<strong>is</strong></strong> could include anything that seems either out of place in acontract of th<strong>is</strong> type, and/or which <strong>is</strong> commercially unbalanced<strong>to</strong> a point where it significantly changes the obligations or r<strong>is</strong>ks,or that <strong>you</strong> do not understand, or of which <strong>you</strong> do notunderstand the implications

Now please read through the following section and answer accordingly.The extent <strong>to</strong> which the contract sat<strong>is</strong>fies the generally accepted tests for IR35friendliness should be considered, with particular reference <strong>to</strong> the aspects set out in thequestions below.Whilst naturally desirable, it <strong>is</strong> not always necessary for there <strong>to</strong> be a ‘yes’ on eachindividual question, provided the overall position indicates at least a ‘probable yes’.For example, it <strong>is</strong> unders<strong>to</strong>od that there are many scenarios where substitution <strong>is</strong>unreal<strong>is</strong>tic. A ‘no’ on that <strong>is</strong>sue alone would not necessarily result in the contract beingconsidered <strong>to</strong> fail, provided the other aspects relevant <strong>to</strong> IR35 were sufficiently strong,and showed a clear intent for a ‘non-employment’ type of relationship between theindividual contrac<strong>to</strong>r and the client.Issue Requirements Yes/NoIs the contractclearly “forservices” ratherthan “of service”?Is a prov<strong>is</strong>ion forsubstitutionclearly defined?Is there Mutualityof Obligationbetween <strong>you</strong> andthe Client?The services <strong>you</strong> are <strong>to</strong> provide should be specified as such, and not by reference <strong>to</strong>a role or position titleYou should have a substantially unfettered right <strong>to</strong> substitute – ie without priorapproval, subject only <strong>to</strong> a right of the client <strong>to</strong> object <strong>to</strong> any individual onreasonable and objectively defined grounds, and on the bas<strong>is</strong> that <strong>you</strong> remainresponsible for sourcing and paying the substitute, and for the overall quality ofwork.Basic: There should be no obligation on <strong>you</strong> as an individual <strong>to</strong> provide servicespersonally, and no unqualified reciprocal obligation <strong>to</strong> pay for services actuallyprovided 2 .Extended: The bas<strong>is</strong> for payment shall be for services actually provided, withoutany obligation on the part of the agency <strong>to</strong> provide work or pay in lieu, and withoutany obligation on <strong>you</strong>r part <strong>to</strong> accept and undertake such work as may be offered.In particular, the contract should not entitle <strong>you</strong> <strong>to</strong> payment in lieu of notice. 3Are there nounreasonableControl elementsenshrined in thecontract?The particular interest here <strong>is</strong> control of a particular type – whether <strong>you</strong> agree ‘thatin the performance of the service <strong>you</strong> will be subject <strong>to</strong> the other’s control in asufficient degree <strong>to</strong> make that other master.’ The degree of control should becapable of being d<strong>is</strong>tingu<strong>is</strong>hed from an employee undertaking similar tasks.Your position should be that of an independent professional, accepting responsibilityfor the services <strong>you</strong> provide, and not subject <strong>to</strong> the direction and control of theClient, save where a necessary consequence of the services themselves1 IR35 status <strong>is</strong> defined not just by contractual terms, but also working relationships. It <strong>is</strong> adv<strong>is</strong>able <strong>to</strong> confirmworking relationships in a Real Arrangement Letter – see <strong>PCG</strong> Guide <strong>to</strong> IR352 In the absence of mutuality at th<strong>is</strong> Basic level, the authorities suggest that the hypothetical relationshipimposed by the leg<strong>is</strong>lation cannot be one of ‘employment’.3 Absence of mutuality at th<strong>is</strong> extended level would generally be regarded as a pointer away from thehypothetical relationship imposed by the leg<strong>is</strong>lation being one of ‘employment’. Where there <strong>is</strong> a degree ofmutuality at both levels, it would generally be regarded as a pointer <strong>to</strong>wards the hypothetical relationshipbeing one of ‘employment’

Issue Requirements Yes/NoOtherThe other character<strong>is</strong>tics of the relationship, as evidenced by thecontract, shall present a picture of a person in business on h<strong>is</strong> ownaccount 4 .The other prov<strong>is</strong>ions of the contract shall be more cons<strong>is</strong>tent with a<strong>self</strong>-employed relationship than with employmentIf (as <strong>is</strong> generally the case) the agency-client contract <strong>is</strong> notintended <strong>to</strong> be d<strong>is</strong>closed <strong>to</strong> the contrac<strong>to</strong>r, the agency-contrac<strong>to</strong>rcontract should include assurances (a) that it accurately reflects allprov<strong>is</strong>ions in the agency-client contract which are intended <strong>to</strong> bebinding on the contrac<strong>to</strong>r, and (b) that no prov<strong>is</strong>ion in the agencyclientcontract <strong>is</strong> incons<strong>is</strong>tent with the intended relationship (asexpressed in th<strong>is</strong> contract) between the contrac<strong>to</strong>r and client.Never not lose sight of the fact that contract terms are but one element of the IR35<strong>assess</strong>ment, and the contract terms may be ineffective in achieving an outside IR35position if the parties (particularly the Individual and the Client) conduct theirrelationship in a manner incons<strong>is</strong>tent with those terms!It <strong>is</strong> for the parties entering any particular contract <strong>to</strong> sat<strong>is</strong>fy themselves that itadequately reflects their intended commercial intent, and it <strong>is</strong> the responsibility of themember company <strong>to</strong> correctly <strong>assess</strong> the IR35 position in relation <strong>to</strong> any particularcontract, and <strong>to</strong> account for tax accordingly, after taking such expert advice as <strong>is</strong>considered appropriate.Please bear in mind that th<strong>is</strong> Checkl<strong>is</strong>t <strong>is</strong> intended for general guidance only, and canonly indicate whether the contract may be considered <strong>to</strong> comply with the <strong>PCG</strong> ApprovedAgency Scheme guidelines. It should not be relied on when taking a dec<strong>is</strong>ion as <strong>to</strong>the IR35 status of any particular engagement. No responsibility <strong>is</strong> accepted by the<strong>PCG</strong> for any dec<strong>is</strong>ions taken on the bas<strong>is</strong> of th<strong>is</strong> Checkl<strong>is</strong>t.4 <strong>Th<strong>is</strong></strong> may include such fac<strong>to</strong>rs as Equipment Helpers financial r<strong>is</strong>k / opportunity <strong>to</strong> profit from soundmanagement responsibility for investment and management degree of integration (‘part & parcel’) degree of control termination prov<strong>is</strong>ions mutual intentions