Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

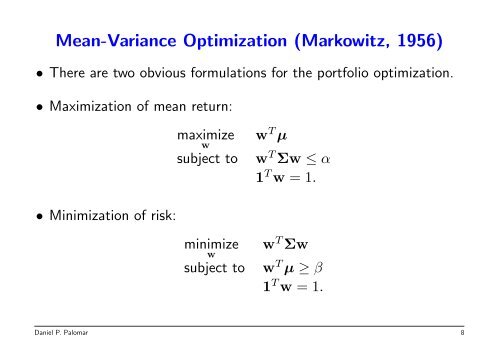

Mean-Variance Optimization (Markowitz, 1956)• There are two obvious formulations for the portfolio optimization.• Maximization of mean return:maximizewsubject tow T µw T Σw ≤ α1 T w = 1.• Minimization of risk:minimizewsubject tow T Σww T µ ≥ β1 T w = 1.Daniel P. Palomar 8