<strong>AIA</strong> <strong>Growth</strong> <strong>Fund</strong> 2During the month, the <strong>Fund</strong> took advantage of the strong equity performance in early May to lighten our equity weightings. We took profit selectivelyon REITs and property names which have performed well and met our target price objectives. Equity purchases totaled $18.6M while sales were$22.1M. In May, we added to DBS Group and took profit on Overseas Union Enterprise specifically.The first quarter earnings season is largely over with modest downward revisions in overall corporate earnings for 2013. Among the notable 1Q2013reports in May, Noble reported a sharp miss in 1Q2013 earnings while Genting <strong>Singapore</strong> also reported earnings which were below expectations.Meanwhile, Golden Agri, First Resources and Wilmar managed to buck the weaker trend in earnings by reporting better than expected 1Q2013numbers due to stronger volume growth and processing margins.While we remain cautiously optimistic on equities in general, we also recognize our return expectations in selective stocks/sectors such as financialsand property REITs have been met and target prices achieved. We are also increasingly cautious on the lofty valuations some of the defensiveyield names have traded up to. As a result, over the past few months, we have taken profit on the sector, reducing our positions in Suntec REIT,Capitamalls Asia, Yanlord and Overseas Union Enterprise, where we felt have discounted most of the upside from asset yield compression andare looking less attractive in terms of valuations.Looking forward, we remain more constructive on companies leveraged towards a cyclical growth recovery as we see an improving externalenvironment and the potential for earnings upgrades in 2013/2014. In this regard, we remain positive in selective growth cyclicals primarily Ezion,Wilmar, Neptune Orient Lines and have also closed our underweight in palm oil through Golden Agri.In fixed income, the risk of the U.S. Treasury yields moving higher on better U.S. economic data and on expectations of asset purchase taperingthat could happen as soon at Q3, will keep <strong>Singapore</strong> rates choppy with an upward bias. Expectations of additional supply in SGS given theupcoming issuances of the 10-year and 20-year in the next two months will also add to investor caution.Performance Indicator Bid-to-bid, net dividends reinvested, SGD, from Inception to 31 May 2013. Source: <strong>AIA</strong> <strong>Singapore</strong>Period 1 Month 3 Months 6 Months 1 Year 3 Year^ 5 Year^ 10 Year^ SinceInception^<strong>Fund</strong> (bid-to-bid) -2.14% 0.98% 6.36% 16.08% 5.79% 2.14% 10.35% 5.33%Benchmark -2.57% 0.87% 4.86% 14.54% 6.78% 3.71% 9.11% 3.86%Note: Performance of the fund is in SGD without taking into considerationthe fees and charges payable through deduction of premium or cancellationof units and with net dividends reinvested.^ Annualised returns# Current benchmark: 70% FTSE AW Sing (Total Return) Index & 30% JPMorgan Sing Govt Bond Index All (The combined benchmark is reflectiveof the fund’s investment focus)Price Indexed2752502252001751501251007550Oct-95Mar-96Aug-96Jan-97Jun-97Nov-97Apr-98Sep-98Feb-99Jul-99Dec-99May-00Oct-00Mar-01Aug-01Jan-02Jun-02Nov-02Apr-03Sep-03Feb-04Jul-04Dec-04May-05Oct-05Mar-06Aug-06Jan-07Jun-07Nov-07Apr-08Sep-08Feb-09Jul-09Dec-09May-10Oct-10Mar-11Aug-11Jan-12Jun-12Nov-12Apr-13<strong>AIA</strong> <strong>Growth</strong> <strong>Fund</strong> --- Benchmark #Top Ten Holdings* As of 31 May 2013Holding (%)DBS GROUP HOLDINGS LTD COMMON STOCK NPV 9.32OVERSEA-CHINESE BANKING CORP L COMMON STOCK NPV 6.53UNITED OVERSEAS BANK LTD COMMON STOCK NPV 6.08SINGAPORE TELECOMMUNICATIONS L COMMON STOCK NPV 5.88KEPPEL CORP LTD COMMON STOCK NPV 4.62WILMAR INTERNATIONAL LTD COMMON STOCK NPV 4.26CAPITALAND LTD COMMON STOCK NPV 4.24KEPPEL LAND LTD COMMON STOCK NPV 2.90SINGAPORE EXCHANGE LTD COMMON STOCK NPV 2.19EZION HOLDINGS LTD COMMON STOCK NPV 2.14______________________________________________________________Total 48.16%

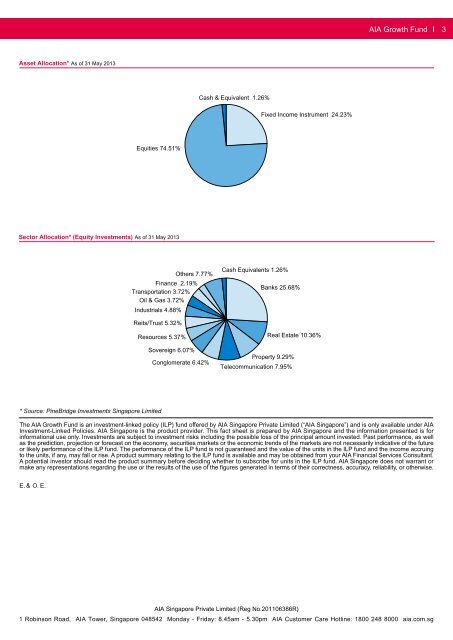

<strong>AIA</strong> <strong>Growth</strong> <strong>Fund</strong> 3Asset Allocation* As of 31 May 2013Cash & Equivalent 1.26%Fixed Income Instrument 24.23%Equities 74.51%Sector Allocation* (Equity Investments) As of 31 May 2013Others 7.77%Finance 2.19%Transportation 3.72%Oil & Gas 3.72%Industrials 4.88%Cash Equivalents 1.26%Banks 25.68%Reits/Trust 5.32%Resources 5.37%Sovereign 6.07%Conglomerate 6.42%Telecommunication 7.95%Real Estate 10.36%Property 9.29%* Source: PineBridge Investments <strong>Singapore</strong> LimitedThe <strong>AIA</strong> <strong>Growth</strong> <strong>Fund</strong> is an investment-linked policy (ILP) fund offered by <strong>AIA</strong> <strong>Singapore</strong> Private Limited (“<strong>AIA</strong> <strong>Singapore</strong>”) and is only available under <strong>AIA</strong>Investment-Linked Policies. <strong>AIA</strong> <strong>Singapore</strong> is the product provider. This fact sheet is prepared by <strong>AIA</strong> <strong>Singapore</strong> and the information presented is forinformational use only. Investments are subject to investment risks including the possible loss of the principal amount invested. Past performance, as wellas the prediction, projection or forecast on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the futureor likely performance of the ILP fund. The performance of the ILP fund is not guaranteed and the value of the units in the ILP fund and the income accruingto the units, if any, may fall or rise. A product summary relating to the ILP fund is available and may be obtained from your <strong>AIA</strong> Financial Services Consultant.A potential investor should read the product summary before deciding whether to subscribe for units in the ILP fund. <strong>AIA</strong> <strong>Singapore</strong> does not warrant ormake any representations regarding the use or the results of the use of the figures generated in terms of their correctness, accuracy, reliability, or otherwise.E. & O. E.<strong>AIA</strong> <strong>Singapore</strong> Private Limited (Reg No.201106386R)1 Robinson Road, <strong>AIA</strong> Tower, <strong>Singapore</strong> 048542 Monday - Friday: 8.45am - 5.30pm <strong>AIA</strong> Customer Care Hotline: 1800 248 8000 aia.com.sg