ECONOMETRIC METHODS II TA session 1 MATLAB Intro ...

ECONOMETRIC METHODS II TA session 1 MATLAB Intro ...

ECONOMETRIC METHODS II TA session 1 MATLAB Intro ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>ECONOMETRIC</strong> <strong>METHODS</strong> <strong>II</strong> <strong>TA</strong> Session 1<br />

end<br />

end<br />

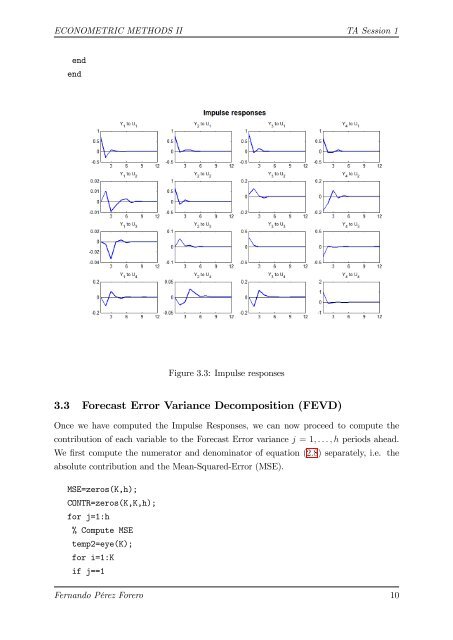

Figure 3.3: Impulse responses<br />

3.3 Forecast Error Variance Decomposition (FEVD)<br />

Once we have computed the Impulse Responses, we can now proceed to compute the<br />

contribution of each variable to the Forecast Error variance j = 1; : : : ; h periods ahead.<br />

We …rst compute the numerator and denominator of equation (2:8) separately, i.e. the<br />

absolute contribution and the Mean-Squared-Error (MSE).<br />

MSE=zeros(K,h);<br />

CONTR=zeros(K,K,h);<br />

for j=1:h<br />

% Compute MSE<br />

temp2=eye(K);<br />

for i=1:K<br />

if j==1<br />

Fernando Pérez Forero 10