Turning Your Data into Insights

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

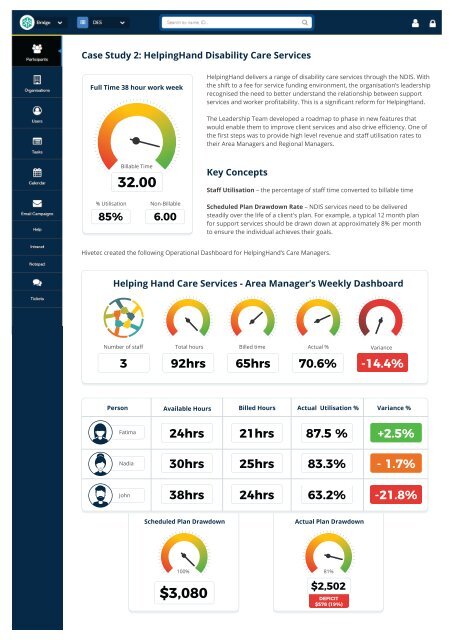

Case Study 2: HelpingHand Disability Care Services<br />

Full Time 38 hour work week<br />

HelpingHand delivers a range of disability care services through the NDIS. With<br />

the shift to a fee for service funding environment, the organisation’s leadership<br />

recognised the need to better understand the relationship between support<br />

services and worker profitability. This is a significant reform for HelpingHand.<br />

The Leadership Team developed a roadmap to phase in new features that<br />

would enable them to improve client services and also drive efficiency. One of<br />

the first steps was to provide high level revenue and staff utilisation rates to<br />

their Area Managers and Regional Managers.<br />

Billable Time<br />

32.00<br />

Key Concepts<br />

Staff Utilisation – the percentage of staff time converted to billable time<br />

% Utilisation<br />

85%<br />

Non-Billable<br />

6.00<br />

Scheduled Plan Drawdown Rate – NDIS services need to be delivered<br />

steadily over the life of a client's plan. For example, a typical 12 month plan<br />

for support services should be drawn down at approximately 8% per month<br />

to ensure the individual achieves their goals.<br />

Hivetec created the following Operational Dashboard for HelpingHand’s Care Managers.<br />

Helping Hand Care Services - Area Manager’s Weekly Dashboard<br />

Number of staff<br />

Total hours<br />

Billed time<br />

Actual %<br />

Variance<br />

3<br />

92hrs<br />

65hrs<br />

70.6%<br />

-14.4%<br />

Person<br />

Available Hours<br />

Billed Hours<br />

Actual Utilisation %<br />

Variance %<br />

Fatima<br />

24hrs<br />

21hrs<br />

87.5 %<br />

+2.5%<br />

Nadia<br />

30hrs<br />

25hrs<br />

83.3%<br />

- 1.7%<br />

John<br />

38hrs<br />

24hrs<br />

63.2%<br />

-21.8%<br />

Scheduled Plan Drawdown<br />

Actual Plan Drawdown<br />

100%<br />

$3,080<br />

81%<br />

$2,502<br />

DEFICIT<br />

$578 (19%)