Risk and Savings in my Life

This is a public consumer education publication, developed by Bright Media for SAIA, clearly written, encouraging informed consumers to make their lives better by planning for risk, saving, and other actions to take to make a better financial life.

This is a public consumer education publication, developed by Bright Media for SAIA, clearly written, encouraging informed consumers to make their lives better by planning for risk, saving, and other actions to take to make a better financial life.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

RISK AND<br />

SAVINGS<br />

IN MY LIFE<br />

A Community Workbook<br />

RISK AND SAVINGS IN MY LIFE

<strong>Risk</strong> <strong>and</strong> <strong>Sav<strong>in</strong>gs</strong> <strong>in</strong> My <strong>Life</strong>: A Community Workbook<br />

© South African Insurance Association 2011<br />

Developed by Bright Media for the South African Insurance Association<br />

ISBN: 978-0-9814322-8-1<br />

CONTENTS<br />

In this book, you will f<strong>in</strong>d:<br />

• My <strong>Risk</strong> <strong>and</strong> My <strong>Sav<strong>in</strong>gs</strong> Plan<br />

1<br />

1. MY SAVINGS<br />

1.1 Types of <strong>Sav<strong>in</strong>gs</strong><br />

1.2 Mzansi <strong>Sav<strong>in</strong>gs</strong> Accounts <strong>and</strong> your Dreams<br />

3<br />

3<br />

4<br />

2. MY RISK: INSURANCE<br />

2.1. Homeowners Insurance<br />

2.2. Household Contents Insurance<br />

2.3. Motor Insurance<br />

2.4. Consumer Credit Insurance<br />

2.5. Personal Liability Insurance<br />

2.6. All <strong>Risk</strong>s Insurance<br />

2.7 Personal Accident Insurance<br />

6<br />

9<br />

10<br />

11<br />

12<br />

13<br />

13<br />

14<br />

SAIA<br />

Community Consumer Education Project

My <strong>Risk</strong> <strong>and</strong> My <strong>Sav<strong>in</strong>gs</strong> plan<br />

This <strong>Risk</strong> <strong>and</strong> <strong>Sav<strong>in</strong>gs</strong> Workbook will provide you with the <strong>in</strong>formation you need to<br />

plan <strong>and</strong> make good decisions about your personal risk <strong>and</strong> sav<strong>in</strong>gs needs.<br />

You are unique (one <strong>and</strong> only you!) You are <strong>in</strong> charge of your sav<strong>in</strong>gs. You are <strong>in</strong><br />

charge of m<strong>in</strong>imis<strong>in</strong>g your risks. You are different from everyone else <strong>and</strong> you have<br />

your own needs when look<strong>in</strong>g at your risk management <strong>and</strong> sav<strong>in</strong>gs.<br />

This workbook is go<strong>in</strong>g to help you do all these th<strong>in</strong>gs. Why? You never know what is<br />

go<strong>in</strong>g to happen to you or your family. That is why you need to be prepared for the<br />

future.<br />

You are always at risk.<br />

This picture....<br />

....Can become this....<br />

And by manag<strong>in</strong>g your<br />

risks, you CAN get back to<br />

this...<br />

RDP Hous<strong>in</strong>g Photo: Hannelie Coetzee, MediaClubSouthAfrica.com<br />

How? By sav<strong>in</strong>g <strong>and</strong> <strong>in</strong>sur<strong>in</strong>g the th<strong>in</strong>gs you own. You don’t need to be rich to be able<br />

to afford <strong>in</strong>surance. Actually if you cannot afford to replace the th<strong>in</strong>gs that you own,<br />

this is when you need <strong>in</strong>surance! Seriously!<br />

So, this workbook is all about becom<strong>in</strong>g a risk manager <strong>and</strong> tak<strong>in</strong>g control of your<br />

money, so that you will Cover your risks <strong>and</strong> Plan for your future by Sav<strong>in</strong>g.<br />

RISK AND SAVINGS IN MY LIFE<br />

1

How do I plan?<br />

Look at your own needs; what you can afford to save, <strong>and</strong> what you can’t afford to<br />

lose. Now, are you ready to take ACTION?<br />

ACTIVITY 1. Let’s test our knowledge. Please fill <strong>in</strong> the first two columns now<br />

(today’s date). When you have f<strong>in</strong>ished the workbook <strong>and</strong> the sem<strong>in</strong>ar (later), you will<br />

come back <strong>and</strong> answer the questions aga<strong>in</strong>:<br />

Today’s Date:<br />

Later:<br />

Questions Yes No Yes No<br />

I can get Homeowners Insurance if I live <strong>in</strong> a RDP house or <strong>in</strong> a<br />

township?<br />

Household Contents Insurance covers all the th<strong>in</strong>gs that are<br />

<strong>in</strong>side <strong>my</strong> house?<br />

If I buy on credit I need to check <strong>my</strong> monthly payments to see if<br />

that <strong>in</strong>cludes Consumer Credit Insurance?<br />

Do you believe you need to get <strong>in</strong>surance on th<strong>in</strong>gs you own?<br />

Do you believe you have to save money <strong>in</strong> a sav<strong>in</strong>gs account?<br />

Is it right to say that long term <strong>in</strong>surance covers life events such<br />

as death, retirement <strong>and</strong> disability?<br />

Do you know what “manag<strong>in</strong>g your risk” means?<br />

ACTIVITY 2. Look at this checklist of <strong>Risk</strong> Management <strong>and</strong> <strong>Sav<strong>in</strong>gs</strong> options.<br />

Do you already have one of these f<strong>in</strong>ancial products? Do you th<strong>in</strong>k you will need any of<br />

these <strong>in</strong> the future? ...Keep this workbook <strong>in</strong> a safe place to rem<strong>in</strong>d you of your plans.<br />

Mark the column with ✓or ✗ to help you with your plann<strong>in</strong>g.<br />

<strong>Risk</strong> Management & <strong>Sav<strong>in</strong>gs</strong><br />

Options<br />

Already<br />

have<br />

Do need<br />

urgently<br />

Will need <strong>in</strong><br />

the future<br />

Need to f<strong>in</strong>d<br />

out more<br />

Personal Insurance<br />

Household Contents Insurance<br />

Consumer Credit Insurance<br />

Motor Insurance<br />

Homeowners Insurance<br />

Funeral policy / Burial Society<br />

Disability Insurance<br />

<strong>Life</strong> Insurance<br />

Retirement Annuity<br />

Stokvel / Society <strong>Sav<strong>in</strong>gs</strong><br />

<strong>Sav<strong>in</strong>gs</strong> Account<br />

Education Policy<br />

Other:<br />

2 RISK AND SAVINGS IN MY LIFE

1<br />

MY <strong>Sav<strong>in</strong>gs</strong><br />

Why should we save?<br />

Because sav<strong>in</strong>g money can change your life! It really works! If you save you can<br />

prepare for your future, afford those th<strong>in</strong>gs you really want plus it is really empower<strong>in</strong>g<br />

to save money. There are loads of different ways to save money <strong>and</strong> because you are<br />

unique you need to pick the option that will work best for you.<br />

1.1<br />

ACTIVITY 3. Types of <strong>Sav<strong>in</strong>gs</strong><br />

<strong>Sav<strong>in</strong>gs</strong><br />

method<br />

Cash<br />

Burial<br />

Society<br />

Stokvel<br />

Description of sav<strong>in</strong>gs method<br />

Money saved is kept <strong>in</strong> a safe place, e.g. at home.<br />

A group of people save a set amount each month for<br />

group members’ family burial costs.<br />

A group of people save money together each month.<br />

They decide which member will receive the money<br />

each month.<br />

A group of people jo<strong>in</strong>tly open a bank sav<strong>in</strong>gs account.<br />

Money is withdrawn as the group needs it. All the<br />

money, <strong>in</strong>clud<strong>in</strong>g the <strong>in</strong>terest earned, is shared equally.<br />

A person deposits their money <strong>in</strong> a bank<strong>in</strong>g account as<br />

it is earned or on a monthly basis.<br />

It is possible to deposit additional money <strong>in</strong>to a home<br />

loan account <strong>and</strong> use the account as a way of sav<strong>in</strong>g.<br />

Valuable items such as gold cha<strong>in</strong>s, old co<strong>in</strong>s, artwork<br />

<strong>and</strong> collector’s items are bought <strong>and</strong> kept as an<br />

‘<strong>in</strong>vestment’<br />

✓I do<br />

this<br />

now<br />

✓I plan<br />

to do<br />

this<br />

<strong>Sav<strong>in</strong>gs</strong><br />

Clubs<br />

Bank<br />

Home<br />

Loan<br />

Valuables<br />

If you have been a super smart person <strong>and</strong> you already have sav<strong>in</strong>gs maybe it is<br />

time for you to <strong>in</strong>vest those sav<strong>in</strong>gs. Invest<strong>in</strong>g just means that you can put the money<br />

somewhere where it will make you some more money.<br />

But remember don’t put your money <strong>in</strong> a little t<strong>in</strong> under your mattress, this is the worst<br />

th<strong>in</strong>g you can do. What will happen if your house burns down <strong>and</strong> you lose all your<br />

money? Th<strong>in</strong>k—<strong>and</strong> put your money <strong>in</strong> a safe place so that you know you can f<strong>in</strong>d it<br />

aga<strong>in</strong>, like a bank. You have worked hard for it.<br />

RISK AND SAVINGS IN MY LIFE<br />

3

1.2<br />

Mzansi <strong>Sav<strong>in</strong>gs</strong> Accounts<br />

AND your dreams<br />

Have I conv<strong>in</strong>ced you to save money?<br />

I hope so! And an easy way to start is to open a Mzansi <strong>Sav<strong>in</strong>gs</strong> Account. Remember<br />

it is much safer than sleep<strong>in</strong>g on your money. What if your house burns down? What if<br />

you get robbed? At least if it is <strong>in</strong> the bank you know it is kept safe for you!<br />

The Mzansi Account<br />

• This account is designed to meet the sav<strong>in</strong>gs<br />

<strong>and</strong> transactional needs of entry level bank<strong>in</strong>g<br />

clients, especially people who have never had<br />

a bank account before.<br />

• This type of account is available from most commercial banks <strong>in</strong> South Africa,<br />

for everyone over the age of 16 who has never had a bank account before.<br />

• All you need to open a Mzansi Account is a green South African ID <strong>and</strong> a<br />

m<strong>in</strong>imum deposit as specified by the bank you choose (these deposits are low).<br />

• With a Mzansi Account, you have the follow<strong>in</strong>g benefits:<br />

o You get a debit card<br />

o Pay for items at shops where you see the logo displayed<br />

o Withdraw <strong>and</strong> deposit cash at any ATM nationwide<br />

o You get one free cash deposit every month<br />

o You only pay higher transactional fees if you make more than 5 deposits<br />

<strong>and</strong> 5 withdrawals each month<br />

o There are no monthly adm<strong>in</strong>istration fees<br />

o Debit <strong>and</strong> Stop Orders are allowed for this account<br />

o There is usually no m<strong>in</strong>imum balance required. (Each bank has different<br />

requirements so its important to check with your particular bank).<br />

4 RISK AND SAVINGS IN MY LIFE

ACTIVITY 4.<br />

What are your dreams? What do you want to save up for?<br />

My Dreams<br />

RISK AND SAVINGS IN MY LIFE<br />

5

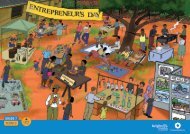

2<br />

MY RISK: INSURANCE<br />

There are a lot of different types of <strong>in</strong>surance <strong>and</strong> if you look at the picture below it<br />

gives you an overview of some of the <strong>in</strong>surance options available.<br />

household<br />

contents<br />

<strong>in</strong>surance<br />

home<br />

owners<br />

<strong>in</strong>surance<br />

consumer<br />

credit<br />

<strong>in</strong>surance<br />

motor<br />

<strong>in</strong>surance<br />

Because you are unique, you need to look<br />

at the column below <strong>and</strong> tick what you own. Next to<br />

that are the relevant <strong>in</strong>surance policies that you need<br />

to <strong>in</strong>vestigate.<br />

personal<br />

<strong>in</strong>surance<br />

all risks<br />

ACTIVITY 5. Underst<strong>and</strong><strong>in</strong>g Insurance Types<br />

Item<br />

House<br />

Furniture<br />

Items bought on credit<br />

Car<br />

Job<br />

Family<br />

✓<br />

I have a...<br />

The Insurance I need to <strong>in</strong>vestigate is...<br />

Homeowners Insurance<br />

Household Contents Insurance<br />

Consumer Credit Insurance<br />

Motor Insurance<br />

Disability Insurance, Retirement Annuity<br />

Funeral Policy, life Insurance<br />

Let’s learn more……….. Knowledge is power.<br />

6 RISK AND SAVINGS IN MY LIFE

What do you know about Insurance?<br />

To manage your risks, you need to know about <strong>in</strong>surance, right? Right! These are the<br />

most important th<strong>in</strong>gs you need to know about <strong>in</strong>surance:<br />

Long Term Insurance<br />

Def<strong>in</strong>ition: Long term <strong>in</strong>surance covers<br />

life events such as death, retirement <strong>and</strong><br />

disability.<br />

Types of Long Term Insurance<br />

• <strong>Life</strong> Insurance<br />

• Funeral Insurance<br />

• Retirement Annuity<br />

• Consumer Credit Insurance (For <strong>Life</strong><br />

Cover, Disability Cover, etc)<br />

Did You<br />

Know?<br />

Zimele Insurance St<strong>and</strong>ards<br />

South Africa’s <strong>Life</strong> Insurance companies<br />

offer life <strong>in</strong>surance products specially<br />

suited to lower-<strong>in</strong>come earners. These lowcost<br />

life <strong>in</strong>surance products must meet what<br />

are referred to <strong>in</strong> the <strong>in</strong>dustry as Zimele<br />

st<strong>and</strong>ards. ‘Zimele’ means to ‘st<strong>and</strong> on your<br />

own two feet’, <strong>and</strong> products meet<strong>in</strong>g these<br />

st<strong>and</strong>ards aim to be fair, easy to underst<strong>and</strong><br />

<strong>and</strong> simple to have. <strong>Life</strong> <strong>in</strong>surance products<br />

sold with the Zimele stamp of approval must<br />

comply with the follow<strong>in</strong>g st<strong>and</strong>ards:<br />

• Policy summaries must be available <strong>in</strong> any<br />

of the 11 official languages.<br />

• Lower-<strong>in</strong>come earners must be able to<br />

buy a policy, pay the premium, or make<br />

changes to the policy at least once a<br />

month with<strong>in</strong> 40km of where they live or<br />

work.<br />

• Low-<strong>in</strong>come earners must be able to lodge<br />

a claim <strong>and</strong> receive payment of the claim<br />

at least every second work<strong>in</strong>g day with<strong>in</strong><br />

80km of where they live or work.<br />

• A share-call l<strong>in</strong>e must be available six<br />

days a week.<br />

Short Term Insurance<br />

Def<strong>in</strong>ition: Short term <strong>in</strong>surance <strong>in</strong>sures<br />

your possessions (e.g. household items<br />

<strong>and</strong> car) aga<strong>in</strong>st th<strong>in</strong>gs that might<br />

happen, such as fire, theft or damage.<br />

Types of Short Term Insurance<br />

• Household Contents Insurance<br />

• Motor Insurance<br />

• Homeowners Insurance<br />

• Personal Insurance<br />

• Consumer Credit Insurance (to replace<br />

or repair items lost or damaged)<br />

Mzansi Insurance St<strong>and</strong>ards<br />

Some short term <strong>in</strong>surance companies <strong>in</strong><br />

South Africa now offer <strong>in</strong>surance products<br />

specifically suited to households with a<br />

lower <strong>in</strong>come—these basic, affordable <strong>and</strong><br />

easy to underst<strong>and</strong> products must meet what<br />

are referred to <strong>in</strong> the <strong>in</strong>dustry as Mzansi<br />

st<strong>and</strong>ards. Policies meet<strong>in</strong>g the Mzansi<br />

st<strong>and</strong>ards aim to provide cover for the home<br />

(dwell<strong>in</strong>g), household goods <strong>and</strong> personal<br />

effects aga<strong>in</strong>st sudden <strong>and</strong> unexpected events<br />

such as fire, lightn<strong>in</strong>g, explosions, flood<strong>in</strong>g<br />

<strong>and</strong> theft.<br />

RISK AND SAVINGS IN MY LIFE<br />

7

More th<strong>in</strong>gs you need to know<br />

1. Promise = Trust<br />

When you take out <strong>in</strong>surance, you are enter<strong>in</strong>g <strong>in</strong>to an agreement of mutual trust.<br />

This is very important. You, the client, trust that the <strong>in</strong>surance company will cover<br />

what they say they would cover <strong>and</strong> with their promise, <strong>and</strong> the <strong>in</strong>surance company<br />

trust that everyth<strong>in</strong>g you told them about yourself <strong>and</strong> your possessions is true.<br />

2. You can choose between Broker Insurance <strong>and</strong> Direct<br />

Insurance<br />

Just make sure that the broker or company is licensed under the F<strong>in</strong>ancial Advisory<br />

<strong>and</strong> Intermediary Services (FAIS) Act. This is very important because you don’t want<br />

to pay your hard earned money over to a fraud! Make sure that you are given a<br />

license number.<br />

3. There are three documents <strong>in</strong>volved with your policy<br />

a) The Proposal/Application Form:<br />

o This form could be completed by fill<strong>in</strong>g <strong>in</strong> the actual forms, or onl<strong>in</strong>e, or<br />

by e-mail, or by giv<strong>in</strong>g all the <strong>in</strong>formation about yourself to a call centre.<br />

o NB – When giv<strong>in</strong>g <strong>in</strong>formation on this form make sure that it is true<br />

<strong>and</strong> correct as that is what they will have on their records (well, until<br />

you make any changes that is).<br />

b) The Policy:<br />

o This document has all the legal <strong>in</strong>formation which applies to everyone.<br />

c) The Schedule:<br />

This document is specific to you <strong>and</strong> it should tell you:<br />

o What the costs are, <strong>in</strong>clud<strong>in</strong>g what your broker earns on that policy.<br />

o How your contract differs from a st<strong>and</strong>ard one. It must state all<br />

‘exclusions’, ‘endorsements’ <strong>and</strong> ‘warranties’. (See po<strong>in</strong>t 4 below for<br />

explanations of these terms.)<br />

4. You need to underst<strong>and</strong> the follow<strong>in</strong>g terms<br />

o Exclusions: Th<strong>in</strong>gs you do not want covered.<br />

o Endorsements: Th<strong>in</strong>gs that must be covered.<br />

o Warranties: This must be <strong>in</strong> place for the <strong>in</strong>surance to be valid (legal).<br />

o Excess: This is the ‘first amount payable’ by you when you put <strong>in</strong> a claim.<br />

Remember, the larger the excess, the lower your premiums.<br />

Example of how these terms would be used: Let’s say you are <strong>in</strong>sur<strong>in</strong>g<br />

your car. You have a brass emblem of your favourite soccer team’s logo mounted<br />

on your bonnet. You have a cheap car radio that came with the car <strong>and</strong> you have<br />

an alarm system <strong>in</strong>stalled. So you decide to ‘exclude’ the car radio because it isn’t<br />

worth much anyway; you ‘endorse’ the brass soccer logo because you live for<br />

soccer; <strong>and</strong> you ‘warrant’ that the alarm system will be used. Now, if someone<br />

breaks <strong>in</strong>to your car <strong>and</strong> steals the car radio, it is not covered. If someone breaks<br />

off the soccer brass logo, no problem, you will be paid out. If your car is stolen <strong>and</strong><br />

it is discovered that your alarm system was not <strong>in</strong> work<strong>in</strong>g order, you have not lived<br />

up to your warranty <strong>and</strong> you will not be paid out. Quite simple actually!<br />

8 RISK AND SAVINGS IN MY LIFE

2.1<br />

Homeowners <strong>in</strong>surance<br />

home<br />

owners<br />

<strong>in</strong>surance<br />

Yipee you f<strong>in</strong>ally got<br />

your RDP house or you<br />

have worked your whole<br />

life to build your house<br />

from noth<strong>in</strong>g.<br />

So why do you not have <strong>in</strong>surance on your house? Imag<strong>in</strong>e someth<strong>in</strong>g happens to<br />

your house <strong>and</strong> you have noth<strong>in</strong>g. Don’t risk that. Rather read this!<br />

You can afford Homeowners Insurance. Some Mzansi-type <strong>in</strong>surance policies could be<br />

as little as R20 –R50 per month. This depends on the company.<br />

Why do you need Homeowners Insurance? Well because it covers the bricks, mortar,<br />

roof <strong>and</strong> fitt<strong>in</strong>gs <strong>in</strong> your house. All the th<strong>in</strong>gs that will stay put if you turn your house<br />

upside down. So <strong>in</strong> case the paraff<strong>in</strong> stove burns down the whole house you will be<br />

able to claim from your Homeowners Insurance policy <strong>and</strong> be able to rebuild your<br />

home.<br />

Aga<strong>in</strong> it is up to you to phone an <strong>in</strong>surance company <strong>and</strong> <strong>in</strong>sure your property for<br />

the right value. It is also your responsibility to ensure that your house is <strong>in</strong> a good<br />

condition <strong>and</strong> not fall<strong>in</strong>g apart. If you don’t look after <strong>and</strong> love your house with the<br />

necessary ma<strong>in</strong>tenance then your <strong>in</strong>surance company might not pay out your claim if<br />

say the roof collapses.<br />

But if you look after your house <strong>and</strong> ensure that it is <strong>in</strong>sured at the correct amount the<br />

<strong>in</strong>surance will gladly pay for damages to your property.<br />

RISK AND SAVINGS IN MY LIFE<br />

9

household<br />

contents<br />

<strong>in</strong>surance<br />

2.2<br />

Household contentS<br />

<strong>in</strong>surance<br />

If you turn your house upside down, there will be a lot of th<strong>in</strong>gs that will fall out. Now all<br />

these th<strong>in</strong>gs that fall out will be covered by Household Contents Insurance. This means<br />

that if you have a burglary <strong>and</strong> your television, clothes <strong>and</strong> couches get stolen, you<br />

can claim from your Household Contents Insurance policy. Some Mzansi-type <strong>in</strong>surance<br />

policies may be as little as R20–R50 per month. This depends on what you <strong>in</strong>sure.<br />

Now be smart, walk through your house <strong>and</strong> make a list of all the items <strong>in</strong> your house<br />

(only the ones that will fall out if you turn your house upside down). This list is called<br />

an <strong>in</strong>ventory <strong>and</strong> you can use this list to make sure that you have the correct amount of<br />

<strong>in</strong>surance <strong>and</strong> you are not over-<strong>in</strong>sured or under-<strong>in</strong>sured. Don’t make that mistake, it is<br />

costly.<br />

Then the <strong>in</strong>surance company needs to know that you are also from your side do<strong>in</strong>g<br />

everyth<strong>in</strong>g you can to protect your belong<strong>in</strong>gs. So <strong>in</strong>sure that you have burglar bars,<br />

security gates <strong>and</strong> if you can afford an alarm system that is even better. Keep the<br />

security features <strong>in</strong> good condition else you might have a problem if you want to<br />

claim. If you keep th<strong>in</strong>gs honest <strong>and</strong> <strong>in</strong> good work<strong>in</strong>g order from your side then the<br />

<strong>in</strong>surance company will pay out your claim.<br />

Important th<strong>in</strong>gs to remember about Household Contents<br />

Insurance:<br />

• Know what your <strong>in</strong>surance company covers! Read your policy <strong>and</strong> make sure you<br />

ask questions if you don’t underst<strong>and</strong> someth<strong>in</strong>g.<br />

• Check that your security systems, as you specified <strong>in</strong> your <strong>in</strong>surance policy, are <strong>in</strong><br />

work<strong>in</strong>g order.<br />

• Make changes to your policy as your needs change, for example you bought<br />

another TV—so you need to add that to your policy.<br />

10 RISK AND SAVINGS IN MY LIFE

2.3<br />

Motor <strong>in</strong>surance<br />

Okay, so you have just<br />

been able to afford to buy<br />

yourself a small second<br />

h<strong>and</strong> car. Do you th<strong>in</strong>k<br />

it is not worth gett<strong>in</strong>g<br />

<strong>in</strong>surance just because<br />

it is old <strong>and</strong> second<br />

h<strong>and</strong>?<br />

Don’t th<strong>in</strong>k that!<br />

If you cannot afford<br />

to replace the car when it gets stolen<br />

you need to learn more about Motor<br />

Insurance.<br />

motor<br />

<strong>in</strong>surance<br />

First you can get the whole deal, a Motor Insurance<br />

Policy that will cover everyth<strong>in</strong>g:<br />

Collision: When you have an accident;<br />

Fire: if your car burns down;<br />

Theft: If your car is stolen.<br />

But if you cannot afford the whole sh<strong>in</strong>y Motor<br />

Insurance Policy there is also Motor Insurance<br />

called 3rd Party Fire <strong>and</strong> Theft. This option is<br />

usually cheaper, it can be under R100 depend<strong>in</strong>g<br />

on your car <strong>and</strong> policy, <strong>and</strong> it will cover the<br />

follow<strong>in</strong>g:<br />

3rd party damage: So if you drive <strong>in</strong>to a Golf<br />

GTi with your little second h<strong>and</strong> car, the damage<br />

to the Golf GTi will be covered by your <strong>in</strong>surance<br />

company but not the damage to your car. But phew!<br />

Luckily you don’t have to pay to fix the Golf GTi;<br />

Fire: If fire destroys your car the <strong>in</strong>surance will replace your car;<br />

Theft: if your car gets stolen, you will be paid out to replace your car.<br />

What will the <strong>in</strong>surance<br />

company ask for when you<br />

apply for Motor Insurance:<br />

• Where does the vehicle<br />

live? The more security<br />

there is, the lower the<br />

premium.<br />

• Who normally drives it?<br />

Give the drivers age <strong>and</strong><br />

gender.<br />

• Is the vehicle used for<br />

bus<strong>in</strong>ess or for private use?<br />

If bus<strong>in</strong>ess, what type of<br />

bus<strong>in</strong>ess.<br />

• Does it have theft<br />

protection. They would ask<br />

you what type of protection<br />

example a gear lock,<br />

immobiliser, alarm system<br />

etc.<br />

And if you really can’t afford any of the above have a look at only gett<strong>in</strong>g 3rd Party<br />

Motor Insurance then at least you know you will not be pay<strong>in</strong>g to fix the damages to<br />

somebody else’s car for the rest of your life!<br />

RISK AND SAVINGS IN MY LIFE<br />

11

2.4<br />

Consumer credit <strong>in</strong>surance<br />

Now this is<br />

one you need<br />

to know about.<br />

Because all of us<br />

sometimes buy<br />

th<strong>in</strong>gs on credit.<br />

Consumer Credit<br />

Insurance is <strong>in</strong>surance you are required to buy when you buy th<strong>in</strong>gs on credit. This<br />

<strong>in</strong>surance will settle the outst<strong>and</strong><strong>in</strong>g amount owed by you to the credit provider. In<br />

addition, it can also <strong>in</strong>clude replac<strong>in</strong>g or repair<strong>in</strong>g an item. You may not even know<br />

that you have this <strong>in</strong>surance because this <strong>in</strong>surance premium is often <strong>in</strong>cluded <strong>in</strong> your<br />

monthly <strong>in</strong>stalment for the goods that you bought on credit. It is your responsibility to<br />

f<strong>in</strong>d out if the place you are buy<strong>in</strong>g the goods from <strong>in</strong>cludes this cover <strong>in</strong> the amount<br />

you need to pay back every month. This is important to know. Why? Because if<br />

someth<strong>in</strong>g happens to you or the items you bought it might be covered by Consumer<br />

Credit Insurance <strong>and</strong> you might be able to claim from this <strong>in</strong>surance <strong>and</strong> then you will<br />

be debt free. Seriously!<br />

Be wise when claim<strong>in</strong>g<br />

When someth<strong>in</strong>g happens to you <strong>and</strong> you need to make a claim on the Consumer<br />

Credit Insurance, you will need the follow<strong>in</strong>g:<br />

• Identity document AND<br />

• For loss or damage of goods:<br />

o You must report the theft to the police <strong>and</strong> they will give<br />

you a case number, hold on to this case number.<br />

o Affidavit<br />

• For Death:<br />

12 RISK AND SAVINGS IN MY LIFE<br />

o Death certificate<br />

o Bank Statement—for additional beneficiary<br />

payment (if this applies)<br />

consumer<br />

credit<br />

<strong>in</strong>surance<br />

When can you claim:<br />

1. Loss or damage of<br />

goods purchases<br />

on credit<br />

2. Death<br />

3. Disability<br />

4. Retrenchment<br />

• For Retrenchment:<br />

o UIF document or card<br />

o Retrenchment documentation from your former employer<br />

o A copy of your employment contract for contract workers<br />

o If you are self-employed, you also need a copy of your bus<strong>in</strong>ess registration papers.

2.5<br />

Personal liability<br />

<strong>in</strong>surance<br />

What?<br />

This covers damage or <strong>in</strong>jury to persons<br />

or property of non-members of your<br />

household.<br />

For example: Your dog bites the aerial<br />

<strong>in</strong>stallation man when he enters the<br />

property to <strong>in</strong>stall it. A friend comes<br />

to visit you <strong>and</strong> slips on the floor <strong>and</strong><br />

<strong>in</strong>jures his back.<br />

WISE TIP<br />

It would be wise to have some Personal<br />

Liability <strong>in</strong>cluded <strong>in</strong> the Household<br />

Contents of your Homeowners<br />

Insurance or with your Motor<br />

Insurance. Check whether these are<br />

<strong>in</strong>cluded before buy<strong>in</strong>g more Personal<br />

Liability Cover—it is very <strong>in</strong>expensive,<br />

around R10 per month.<br />

2.6<br />

All riskS <strong>in</strong>surance<br />

This applies to th<strong>in</strong>gs you<br />

move around with you for<br />

example your h<strong>and</strong>bag,<br />

cellphone, bicycle,<br />

sunglasses etc.<br />

ANYWHERE!<br />

Your loss is covered<br />

anywhere!<br />

SPECIFY!<br />

You must specify<br />

exactly what you want<br />

covered!<br />

personal<br />

<strong>in</strong>surance<br />

all risks<br />

RISK AND SAVINGS IN MY LIFE<br />

13

2.7<br />

Personal accident<br />

Now this is all about you. What will happen if you are <strong>in</strong> a taxi accident <strong>and</strong> disabled<br />

for life <strong>and</strong> you cannot work? Personal Accident covers you aga<strong>in</strong>st disablement<br />

(caused by an accident) <strong>and</strong> provides for your loved ones <strong>in</strong> the<br />

event of your death.<br />

PERSONAL<br />

ACCIDENT<br />

14 RISK AND SAVINGS IN MY LIFE

Remember!<br />

1 You are unique <strong>and</strong> need to f<strong>in</strong>d solutions that will suit<br />

your needs.<br />

2 If you don’t underst<strong>and</strong> ask questions.<br />

3 If you can afford it, get <strong>in</strong>surance to suit your needs <strong>and</strong><br />

m<strong>in</strong>imise your risks.<br />

4 Only buy <strong>in</strong>surance from a registered service provider.<br />

5 Be smart—save money!<br />

Useful Contact Numbers<br />

• Always ask questions. Make sure you underst<strong>and</strong> what f<strong>in</strong>ancial products you have<br />

selected. You must update your <strong>in</strong>formation <strong>and</strong> can change your product as your<br />

life changes. Contact your <strong>in</strong>surer FIRST.<br />

• If you are not satisfied with your <strong>in</strong>surance company’s decision, contact the<br />

Ombudsman for Short-term Insurance (OSTI): phone on (011) 726 8900, email to:<br />

<strong>in</strong>fo@osti.co.za, or write to: PO Box 32334, Braamfonte<strong>in</strong>, 2017<br />

• If you have any compla<strong>in</strong>ts after you have dealt with an <strong>in</strong>surance company,<br />

contact FAIS Ombud: (012) 470 9080, <strong>in</strong>fo@faisombud.co.za.<br />

• If you are still not satisfied, you can contact the F<strong>in</strong>ancial Services Board (FSB):<br />

0800 202 087. The FSB will only h<strong>and</strong>le a compla<strong>in</strong>t if the law has been broken.<br />

For additional <strong>in</strong>formation, contact the South African<br />

Insurance Association on (011) 726-5381

KE NAKO!<br />

It is time to be <strong>in</strong> control of your future:<br />

PLAN to SAVE<br />

SAVE for the FUTURE<br />

INVEST <strong>in</strong> INSURANCE,<br />

when this is relevant to you,<br />

to cover the risk of LOSS <strong>and</strong> DAMAGE<br />

to your goods,<br />

your property <strong>and</strong><br />

your life.<br />

SAIA<br />

Developed <strong>and</strong> produced on behalf of<br />

the South African Insurance Association<br />

9 780981 432281