STEP Skills Development and Competitions - DepEd

STEP Skills Development and Competitions - DepEd

STEP Skills Development and Competitions - DepEd

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>STEP</strong> <strong>Skills</strong> <strong>Development</strong> <strong>and</strong> <strong>Competitions</strong><br />

CONTEST PACKAGE ASSESSMENT PROCEDURE/SPECIFIC INSTRUCTIONS RESOURCES<br />

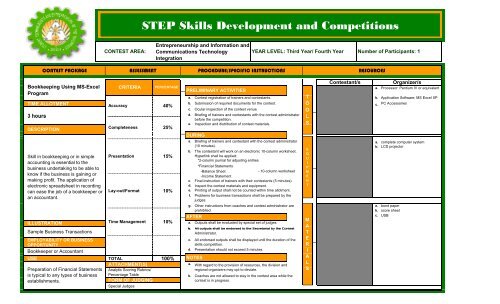

Bookkeeping Using MS-Excel<br />

Program<br />

TIME ALLOTMENT<br />

3 hours<br />

DESCRIPTION<br />

Skill in bookkeeping or in simple<br />

accounting is essential to the<br />

business undertaking to be able to<br />

know if the business is gaining or<br />

making profit. The application of<br />

electronic spreadsheet in recording<br />

can ease the job of a bookkeeper or<br />

an accountant.<br />

ILLUSTRATION<br />

Sample Business Transactions<br />

EMPLOYABILITY OR BUSINESS<br />

OPPORTUNITY<br />

Bookkeeper or Accountant<br />

USE<br />

Preparation of Financial Statements<br />

is typical to any types of business<br />

establishments.<br />

CONTEST AREA:<br />

Entrepreneurship <strong>and</strong> Information <strong>and</strong><br />

Communications Technology<br />

Integration<br />

YEAR LEVEL: Third Year/ Fourth Year Number of Participants: 1<br />

CRITERIA<br />

PERCENTAGE<br />

Accuracy 40%<br />

Completeness 25%<br />

Presentation<br />

Lay-out/Format<br />

Time Management<br />

TOTAL<br />

ATTACHMENT(S)<br />

Analytic Scoring Rubrics/<br />

Percentage Table<br />

FORM OF JUDGING<br />

Special Judges<br />

15%<br />

10%<br />

10%<br />

100%<br />

PRELIMINARY ACTIVITIES<br />

a.<br />

b.<br />

c.<br />

d.<br />

e.<br />

c.<br />

d.<br />

e.<br />

f.<br />

Contest registration of trainers <strong>and</strong> contestants.<br />

Submission of required documents for the contest.<br />

Ocular inspection of the contest venue<br />

Briefing g of trainers <strong>and</strong> contestants with the contest administrator<br />

before the competition.<br />

Inspection <strong>and</strong> distribution of contest materials.<br />

DURING<br />

a.<br />

b.<br />

Briefing of trainers <strong>and</strong> contestant with the contest administrator<br />

(10 minutes).<br />

The contestant will work on an electronic 10-column worksheet.<br />

Hyperlink shall be applied:<br />

*2-column journal for adjusting entries<br />

*Financial Statements<br />

-Balance Sheet<br />

- 10-column worksheet<br />

-Income Statement<br />

Final instruction of trainers with their contestants (5 minutes).<br />

Inspect the contest materials <strong>and</strong> equipment.<br />

Printing of output shall not be counted within time allotment.<br />

Problems for business transactions shall be prepared by the<br />

judges.<br />

T<br />

O<br />

T<br />

O<br />

O<br />

L<br />

S<br />

T<br />

Contestant/s Organizer/s<br />

g. Other instructions from coaches <strong>and</strong> contest administrator are<br />

a.<br />

prohibited.<br />

b.<br />

c.<br />

AFTER<br />

a. Outputs shall be evaluated by special set of judges.<br />

bb.<br />

All outputs shall be endorsed to the Secretariat by the Contest<br />

Administrator.<br />

c.<br />

d.<br />

All endorsed outputs shall be displayed until the duration of the<br />

skills competition.<br />

Presentation should not exceed 5 minutes.<br />

NOTES<br />

a.<br />

b.<br />

With regard to the provision of resources, the division <strong>and</strong><br />

regional organizers may opt to deviate.<br />

Coaches are not allowed to stay in the contest area while the<br />

contest is in progress.<br />

E<br />

Q<br />

U<br />

I<br />

P<br />

M<br />

E<br />

N<br />

T<br />

M<br />

A<br />

T<br />

E<br />

R<br />

I<br />

A<br />

L<br />

S<br />

a.<br />

b.<br />

c.<br />

Processor: Pentium IV or equivalent<br />

Application Software: MS Excel XP<br />

PC Accessories<br />

a. complete computer system<br />

b. LCD projector<br />

bond paper<br />

score sheet<br />

USB

ANALYTIC PERFORMANCE SCORING RUBRICS FOR ELECTRONIC SPREADSHEET<br />

CRITERIA PERFORMANCE INDICATOR<br />

95 90 85 80<br />

A. ACCURACY 40% • Entries were properly • Entries were properly • Entries were properly • Entries were properly<br />

<strong>and</strong> accurately recorded. recorded but with 1-3 recorded but with 4-7 recorded but with 8-10<br />

inaccurate data.<br />

inaccurate data.<br />

inaccurate data.<br />

• Entries were recorded • Entries were recorded • Entries were recorded • Only few entries were<br />

B. COMPLETENESS 25% completely in an<br />

completely but 1-3<br />

completely but 4-6<br />

recorded <strong>and</strong> in an<br />

appropriate column <strong>and</strong> entries were recorded in entries were recorded in inappropriate column<br />

manner.<br />

an inappropriate column an inappropriate column <strong>and</strong> manner.<br />

<strong>and</strong> manner.<br />

<strong>and</strong> manner.<br />

• Exhibited good voice • Exhibited good voice • Exhibited fair voice • Exhibited fair body<br />

C. PRESENTATION 15% projection, appropriate projection, appropriate projection, fair body language with more than<br />

body language, correct body language with one language with 3-5<br />

5 incorrect grammar <strong>and</strong><br />

grammar <strong>and</strong><br />

or two incorrect<br />

incorrect grammar <strong>and</strong> punctuation.<br />

punctuation.<br />

grammar <strong>and</strong><br />

punctuation.<br />

punctuation.<br />

• All parts of the 10- • All parts of the 10- • Some parts of the 10- • Most parts of the 10-<br />

D. LAY-OUT/<br />

column worksheet were column worksheet were column worksheet were column worksheet were<br />

FORMAT 10% sequentially arranged sequentially arranged sequentially arranged not sequentially<br />

<strong>and</strong> indention on other but 1-2 indentions on but 3-5 indentions on arranged <strong>and</strong> indention<br />

parts was observed. some parts were not some parts were not on some parts was not<br />

observed.<br />

observed.<br />

observed.<br />

• Finished the output 10 • Finished the output 5 • Finished the output • Was not able to finish<br />

E. TIME<br />

minutes before the<br />

minutes before the<br />

within the given time. the output within the<br />

MANAGEMENT 10% allotted time.<br />

allotted time.<br />

given time.

Sample Problems on Business Transactions<br />

The following is the unadjusted trial balance of P.D. trading on December 31,<br />

2007, the end of the accounting period.<br />

Cash P 10,000.00<br />

Accounts Receivable 40,000.00<br />

Allowance for Bad Debts P 400.00<br />

Notes Receivable 12,000.00<br />

Inventory, January 1 22,000.00<br />

Furniture <strong>and</strong> Equipment 25,000.00<br />

Accumulated Depreciation 10,000.00<br />

L<strong>and</strong> 115,000.00<br />

Accounts Payable 60,000.00<br />

Notes Payable-bank debt in 2 years 20,000.00<br />

Mortgage Payable-due in 5 years 50,000.00<br />

P.D., Capital 99,000.00<br />

Sales 360,000.00<br />

Sales Returns <strong>and</strong> Allowance 11,000.00<br />

Purchases 280,000.00<br />

Freight In 6,200.00<br />

Salaries 36,000.00<br />

Rent Expense 24,000.00<br />

Insurance 4,800.00<br />

Other Operating Expenses 12,000.00<br />

Interest Expense 1,800.00<br />

Interest Income 600.00<br />

Total P 600,000.00 P 600,000.00<br />

Additional information for adjustments:<br />

a. Estimated bad debts are 2 ½% of accounts receivable.<br />

b. A note receivable P8,000.00, 60-day 6% is dated Nov. 16, 2007.<br />

c. The furniture <strong>and</strong> equipment were acquired on Jan. 1, 2005 <strong>and</strong> are<br />

estimated to last two years from December 31, 2007.<br />

d. The note payable to bank is 15% note dated Sept. 1, 2007.<br />

e. Accrued interest on mortgage is P1,500.00.<br />

f. Accrued salaries 1,200.00.<br />

g. Prepaid rent P8,000.00<br />

h. Unexpired insurance P600.00.<br />

i. Prepaid interest expense P300.00.<br />

j. Prepaid interest income P100.00.<br />

k. Inventory, December 31, 2007, P62,440.00.