ley 125/91, modificada por la ley 2421/04 rentas de actividades ...

ley 125/91, modificada por la ley 2421/04 rentas de actividades ...

ley 125/91, modificada por la ley 2421/04 rentas de actividades ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

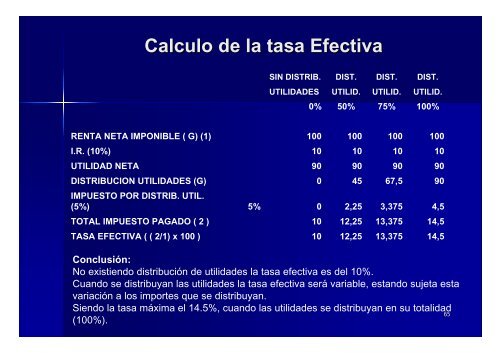

RENTA NETA IMPONIBLE ( G) (1)<br />

I.R. (10%)<br />

UTILIDAD NETA<br />

DISTRIBUCION UTILIDADES (G)<br />

IMPUESTO POR DISTRIB. UTIL.<br />

(5%)<br />

TOTAL IMPUESTO PAGADO ( 2 )<br />

TASA EFECTIVA ( ( 2/1) x 100 )<br />

Calculo <strong>de</strong> <strong>la</strong> tasa Efectiva<br />

5%<br />

SIN DISTRIB.<br />

UTILIDADES<br />

0%<br />

100<br />

10<br />

90<br />

0<br />

0<br />

10<br />

10<br />

DIST.<br />

UTILID.<br />

50%<br />

100<br />

10<br />

90<br />

45<br />

2,25<br />

12,25<br />

12,25<br />

DIST.<br />

UTILID.<br />

75%<br />

100<br />

10<br />

90<br />

67,5<br />

3,375<br />

13,375<br />

13,375<br />

DIST.<br />

UTILID.<br />

100%<br />

Conclusión:<br />

No existiendo distribución <strong>de</strong> utilida<strong>de</strong>s <strong>la</strong> tasa efectiva es <strong>de</strong>l 10%.<br />

Cuando se distribuyan <strong>la</strong>s utilida<strong>de</strong>s <strong>la</strong> tasa efectiva será variable, estando sujeta esta<br />

variación a los im<strong>por</strong>tes que se distribuyan.<br />

Siendo <strong>la</strong> tasa máxima el 14.5%, cuando <strong>la</strong>s utilida<strong>de</strong>s se distribuyan en su totalidad<br />

65<br />

(100%).<br />

100<br />

10<br />

90<br />

90<br />

4,5<br />

14,5<br />

14,5