20080418 Nieuwsflash 028.indd - Koen Hoefgeest® Optie Advies

20080418 Nieuwsflash 028.indd - Koen Hoefgeest® Optie Advies

20080418 Nieuwsflash 028.indd - Koen Hoefgeest® Optie Advies

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

1 8 a p r i l 2 0 0 8 D e k e u z e v a n W i l l e m M i d d e l k o o p , e i n d r e d a c t i e S a n d e r B o o n n r 0 2 8<br />

1 / 1 7<br />

Nieuws-Flash!<br />

o n t h u l l e n d n i e u w s o v e r f i n a n c i ë l e m a r k t e n , e n e r g i e , g e o p o l i t i e k<br />

<strong>Koen</strong> Hoefgeest is de Nederlandse Jim Cramer. Met een hoop kabaal en<br />

soms overdrijving bespreekt hij de beurzen via teletekst pagina 555 op<br />

RTL 7. Maar net als Jim Cramer weet hij wel aardig waar hij het over<br />

heeft. Na zijn kritiek, dat wij bij RTL Z geen bal verstand hebben waar<br />

die kredietcrisis nu werkelijk over gaat, heb ik hem uitgedaagd een allesomvattende<br />

analyse op te tikken. Dat leverde het volgende betoog van<br />

bijna 1000 woorden en vele grafieken (die hopelijk leesbaar zijn). Het<br />

document is ook op de site te vinden. Het is <strong>Koen</strong>’s persoonlijke mening<br />

maar ik heb geleerd goed naar hem te luisteren.<br />

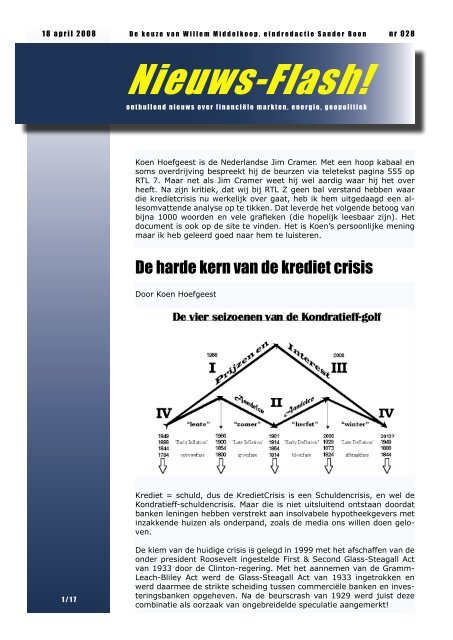

De harde kern van de krediet crisis<br />

Door <strong>Koen</strong> Hoefgeest<br />

Krediet = schuld, dus de KredietCrisis is een Schuldencrisis, en wel de<br />

Kondratieff-schuldencrisis. Maar die is niet uitsluitend ontstaan doordat<br />

banken leningen hebben verstrekt aan insolvabele hypotheekgevers met<br />

inzakkende huizen als onderpand, zoals de media ons willen doen geloven.<br />

De kiem van de huidige crisis is gelegd in 1999 met het afschaffen van de<br />

onder president Roosevelt ingestelde First & Second Glass-Steagall Act<br />

van 1933 door de Clinton-regering. Met het aannemen van de Gramm-<br />

Leach-Bliley Act werd de Glass-Steagall Act van 1933 ingetrokken en<br />

werd daarmee de strikte scheiding tussen commerciële banken en investeringsbanken<br />

opgeheven. Na de beurscrash van 1929 werd juist deze<br />

combinatie als oorzaak van ongebreidelde speculatie aangemerkt!

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

2 / 1 7<br />

Nieuws-Flash!<br />

Door het samengaan van commerciële banken en investeringsbanken<br />

heeft ‘financial engineering’ en het proces van securitizatie van leningen<br />

een grote vlucht genomen uitmondend in de oprichting van off-balance<br />

Special Purpose Vehikels, zoals de SIV’s, Conduits en VIE’s. En daar ging<br />

het mis.<br />

Door ‘pooling’ (bundeling) van een keur aan leningen en de uitgifte van<br />

Collateral Debt Obligations in tranches met foutieve ratingen vanwege<br />

gerenommeerde ratinginstituten zoals Moody’s, Standard & Poor en Fitch<br />

waarbij het default-risico middels Credit Default Swaps werd verzekerd<br />

bij de zogenaamde Monoline Insurance Companies (Monolines) als MBIA,<br />

Ambac, FGIC, en ACA.<br />

Methodiek<br />

ACA werd in december 2007 delisted van de<br />

NYSE en van de beurs gehaald vanwege een<br />

negatief Eigen Vermogen en de geminimaliseerde<br />

kapitaalswaarde. MBIA, Ambac en Financial<br />

Guaranty Insurance Company vechten<br />

met onorthodoxe hulp van The Illuminati van<br />

de FED voor hun leven.<br />

Door leningen van verscheidene pluimage te ‘poolen’ en onder te verdelen<br />

in fictieve tranches van onderpand voor uit te geven obligaties onstaan de<br />

CDO’s. Deze CDO-tranches zijn door de ratinginstituten voorzien van niet<br />

accurate kwaliteitskeurmerken. The Good, the Not so Good & the Ugly.<br />

So far, so good, ware het niet dat de verkochte CDO’s zelf ook weer als<br />

obligatie (lening met onderpand) zijn gesecuritiseerd door de koper ervan.<br />

En dan wordt de oorspronkelijke obligatie een optie op een obligatie<br />

die de naam obligatie niet meer mag dragen. Het wordt daarmee dan dus<br />

een Collateralized Debt Option!

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

3 / 1 7<br />

Nieuws-Flash!<br />

Herhaal dit proces nog een aantal malen en er ontstaat een kettingbief<br />

in derivaten, een Daisy Chain met een onvoorstelbare hefboom die zich<br />

door de hele bankwereld heeft gevlochten. Om het risico dat een dergelijke<br />

CDO niet wordt terugbetaald te verzekeren zijn de Credit Default<br />

Swaps aangewend. Mocht de schuldenaar immers falen dan neemt de<br />

verzekeraar i.c. de Monoliner de plicht op zich de betalingen op de CDO<br />

te voldoen. Waterdicht… tenzij de Monoliner zelf omkiept!<br />

En dat is nu aan het gebeuren, want een optie op een optie op een optie<br />

op een obligatie gaat de initiële hoofdsom met factor x1000 te boven!<br />

Financiering<br />

Hoe zijn nu al de leningen die ten grondslag liggen aan de originele CDO’s<br />

en de aankoop van de overige CDO’s binnen de ketting gefinancierd?<br />

Oftewel, waar en hoe hebben de bankdieten hun schijnbaar onuitputtelijke<br />

bron om de onderliggende leningen en de aankoop van de CDO’s te<br />

financieren aangeboord? Voor het antwoord op deze vraag dient te rade<br />

te worden gegaan bij de markt zelf, want de markt weet alles en heeft<br />

altijd gelijk.<br />

De crisis brak uit toen het inmiddels omgekiepte Bear Stearns in de zomer<br />

van 2007 als eerste met een bericht naar buiten kwam dat er grote<br />

schade werd geleden op hun kredietportefeuille. Wie - behalve insiders<br />

- had toen ooit gehoord van CDO’s, CDS’s, MBS’s, Option-ARM’s en nog<br />

meer van deze curieuze alfabetsoep?<br />

De credit-spreads van de CDS-contracten zijn sindsdien door het dak geschoten<br />

en de waarde is gekelderd. Ook de aandelenmarkten en koersen<br />

van de Financials zijn sinds de zomer van 2007 afgeslacht. Wat is daar in<br />

hemelsnaam gebeurd?

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

4 / 1 7<br />

Nieuws-Flash!<br />

Triple A 2007(AAA) Double A 2006 (AA)<br />

Primo July 2007 duiken de CDS-contracten op basis van de ABX-index<br />

plotseling de afgrond in. De ABX-index bestaat uit een serie van Credit<br />

Default Swaps gebaseerd op 20 obligaties met als onderpand subprimehypotheken.<br />

Een daling van deze index wijst er op dat investeerders vermoeden<br />

dat er verhoogd risico bestaat dat de houders van de leningen<br />

niet worden terugbetaald. Bovenstaande charts laten het koersverloop<br />

zien van de CDS op basis van de 2007 AAA en 2006 AA-tranches. Onderstaande<br />

chart laat zien dat de waarde tegen het einde van 2007 met<br />

respectievelijk 30 en 60 basispunten is gedaald.

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

5 / 1 7<br />

Nieuws-Flash!<br />

En nu komt de grote clou! De USD, die sinds 2005 ten opzichte van de<br />

JapYEN met +21% is gestegen in verband met de Carry Trades waarbij<br />

de doelvaluta standaard onder druk komt te staan, krijgt begin juli 2007<br />

plotseling klappen te verwerken. En met het inklappen van de USD/JPY<br />

storten ook de aandelenmarkten hand-in-hand af, like Twin-Brothers.

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

6 / 1 7<br />

Conclusie<br />

Nieuws-Flash!<br />

Er kan derhalve geen andere conclusie worden getrokken, dan dat de<br />

Dollar/Yen Carry Trades, al dan niet via het hanteren van Interest Rate<br />

Swaps, dienst hebben gedaan als bronfinanciering van de wereldwijde<br />

monstrueus dodelijke Derivaten-Kettingbrief.<br />

Leg dit valutapaar op de grafieken van de aandelenbeurzen en de link is<br />

gelegd. USD/JPY omhoog = beurs omhoog en vice versa. Elke beweging<br />

van dit valutapaar wordt inmiddels slaafs door de aandelenmarkten gevolgd.<br />

Zelfs intraday is de relatie onmiskenbaar aanwezig.<br />

Met het klappen van de Carry Trades is dus ook de Derivaten-Kettingbrief<br />

geklapt. En een Kettingbrief die is geklapt, kan nooit meer op poten worden<br />

gezet.<br />

Kortom, met $2,5 biljoen (2.500.000.000.000) aan onderliggende waarde<br />

CDO’s en $50 biljoen (50.000.000.000.000) in de CDS Market zal deze<br />

KredietCrisis nooit meer kunnen worden opgelost en derhalve dan ook<br />

daadwerkelijk uitmonden in de door het IMF al gevreesde algehele financiële<br />

systeemcrisis, die in het beste geval zal leiden tot een depressie en<br />

in het slechtste geval tot een revolutie.<br />

Bron: www.hoefgeest.nl

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFSS<br />

FFFFS<br />

7 / 1 7<br />

Nieuws-Flash!<br />

Petraeus points to war with Iran<br />

Vergeet Iran niet..<br />

The neocons may yet get their war on Iran.<br />

Ever since President Nouri al-Maliki ordered the attacks in Basra<br />

on the Mahdi Army, Gen. David Petraeus has been laying the<br />

predicate for U.S. air strikes on Iran and a wider war in the Middle<br />

East.<br />

Iran, Petraeus told the Senate Armed Services Committee, has<br />

“fueled the recent violence in a particularly damaging way through<br />

its lethal support of the special groups.”<br />

No, it is not Iran that wants a war with the United States. It is<br />

the United States that has reasons to want a short, sharp war<br />

with Iran.<br />

Lees verder<br />

http://www.vdare.com/buchanan/080410_petraeus.htm<br />

Retailing chains caught in<br />

a wave of bankruptcies<br />

Het gaat niet goed met de economie in de VS. En dat is inderdaad een<br />

understatement.<br />

The consumer spending slump and tightening credit markets are<br />

unleashing a widening wave of bankruptcies in American retailing,<br />

prompting thousands of store closings that are expected to<br />

remake suburban malls and downtown shopping districts across<br />

the country.<br />

Since last fall, eight mostly midsize chains — as diverse as the<br />

furniture store Levitz and the electronics seller Sharper Image<br />

— have filed for bankruptcy protection as they staggered under<br />

mounting debt and declining sales.<br />

But the troubles are quickly spreading to bigger national companies,<br />

like Linens ‘n Things, the bedding and furniture retailer with<br />

500 stores in 47 states. It may file for bankruptcy as early as this<br />

week, according to people briefed on the matter.<br />

Even retailers that can avoid bankruptcy are shutting down stores<br />

to preserve cash through what could be a long economic<br />

downturn.<br />

Lees verder<br />

http://www.nytimes.com/2008/04/15/business/15retail.html?_r=3&oref<br />

=slogin&ref=business&pagewanted=print&oref=slogin&oref=slogin

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFFS<br />

FFFFS<br />

8 / 1 7<br />

Nieuws-Flash!<br />

Goldman Sachs and Wells Fargo warn<br />

‘delusional’ investors on stocks<br />

Het is dan ook niet vreemd dat er stemmen opgaan die aandelenkopers<br />

waarschuwen voor overmatig optimisme..<br />

Wall Street faces the growing risk of an equities bloodbath in coming<br />

months as the credit crunch spreads to the wider economy<br />

and earnings crumble, according to a pair of grim reports issued<br />

by Goldman Sachs and Wells Fargo.<br />

David Kostin, the chief US investment guru for Goldman Sachs,<br />

expects the S&P 500 index of Wall Street equities to plummet a<br />

further 15pc over the “near term” as companies scramble to lower<br />

their outlook for this year.<br />

“Although only a few firms have reported first quarter results,<br />

early signs are awful. We expect a swath of lowered Street faces<br />

the growing risk of an equities bloodbath in coming months as<br />

the credit crunch spreads to the wider economy and earnings<br />

crumble, according to a profit guidance,” he said in a research<br />

note published today, entitled ‘Fasten Seatbelts’.<br />

Scott Anderson, chief economist at Wells Fargo, is equally pessimistic,<br />

describing the bullish views of some market players as<br />

“bordering on delusional”.<br />

Lees verder<br />

http://www.telegraph.co.uk/money/main.jhtml?xml=/money/2008/04/14/bcngold114.xml<br />

Housing woes in U.S.<br />

spread around globe<br />

Met zoveel slecht nieuws is het ook niet eenvoudig optimistisch te blijven<br />

(over de economie)..<br />

DUBLIN — The collapse of the housing bubble in the United States<br />

is mutating into a global phenomenon, with real estate prices<br />

swooning from the Irish countryside and the Spanish coast to<br />

Baltic seaports and even parts of northern India.<br />

This synchronized global slowdown, which has become increasingly<br />

stark in recent months, is hobbling economic growth worldwide,<br />

affecting not just homes but jobs as well.<br />

In Ireland, Spain, Britain and elsewhere, housing markets that<br />

soared over the last decade are falling back to earth. Property<br />

analysts predict that some countries, like this one, will face an<br />

even more wrenching adjustment than that of the United

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFSS<br />

9 / 1 7<br />

Nieuws-Flash!<br />

States, including the possibility that the downturn could become<br />

a wholesale collapse.<br />

“The problems in the U.S. are being transmitted to Europe,” said<br />

Michael Ball, professor of urban and property economics at the<br />

University of Reading in Britain, who studies housing prices.<br />

“What’s happening now is an awful lot more grief than we expected.”<br />

Lees verder<br />

http://www.nytimes.com/2008/04/14/business/worldbusiness/14real.<br />

U.S. foreclosures jump 57% as homeowners<br />

walk away<br />

Op deze ontwikkeling wijzen wij al een tijdje in de Nieuws-Flash! Het<br />

neemt nu steeds serieuzere vormen aan.<br />

April 15 (Bloomberg) -- U.S. foreclosure filings jumped 57 percent<br />

and bank repossessions more than doubled in March from a<br />

year earlier as adjustable mortgages increased and more owners<br />

gave up their homes to lenders.<br />

More than 234,000 properties were in some stage of foreclosure,<br />

or one in every 538 U.S. households, Irvine, California-based RealtyTrac<br />

Inc., a seller of default data, said today in a statement.<br />

Nevada, California and Florida had the highest foreclosure rates.<br />

Filings rose 5 percent from February.<br />

About $460 billion of adjustable-rate loans are scheduled to reset<br />

this year, according to New York-based analysts at Citigroup<br />

Inc. Auction notices rose 32 percent from a year ago, a sign that<br />

more defaulting homeowners are ``simply walking away and<br />

deeding their properties back to the foreclosing lender’’ rather<br />

than letting the home be auctioned, RealtyTrac Chief Executive<br />

Officer James Saccacio said in the statement.<br />

Lees verder<br />

http://www.bloomberg.com/apps/news?pid=20601087&sid=aN3CfG7wY<br />

MuI&refer=home

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFFS<br />

1 0 / 1 7<br />

Nieuws-Flash!<br />

A blunt former Fed chairman takes on<br />

Bernanke. Take heed of what he says<br />

Paul Volcker, voormalig Fed voorzitter, ziet het beleid van Bernanke niet<br />

zitten.<br />

A few days ago an unusual event took place: Paul Volcker, the<br />

mythical U.S. Federal Reserve Board chairman from the Reagan<br />

years, criticized the policy of the current Fed chairman, Ben Bernanke,<br />

in a speech to the Economic Club of New York.<br />

Just so you grasp how extraordinary this was, you should first understand<br />

that normally a past Fed chairman scrupulously avoids<br />

saying anything at all about current Fed policy - for the simple<br />

reason that the current Fed chairman’s words are one of his most<br />

important tools: They can sway markets.<br />

This ability does not fade entirely when a Fed chairman leaves.<br />

So when a past Fed chairman speaks, his words can clash with<br />

those of the present one and make that one’s job difficult. Out of<br />

professional courtesy, past Fed chairmen therefore keep quiet;<br />

Mr. Volcker especially - the man who hiked interest rates to 20<br />

per cent to kill inflation, at the cost of a deep recession. But last<br />

week Mr. Volcker spoke his mind bluntly. He said, in effect, that<br />

the current Fed is not doing its job.<br />

This would have been unusual enough. But Mr. Volcker went<br />

further. Not only is the Fed not doing its job, he said, but it is<br />

doing the wrong job: It is defending the economy and the market,<br />

instead of defending the dollar. And just to stick the knife in,<br />

Mr. Volcker added that this bad job now will make the real job<br />

- defending the greenback - much harder later. It’ll cause even<br />

greater economic suffering.<br />

In plain words, Mr. Volcker implied that the current Fed is not<br />

only incompetent, but that its actions are dangerous.<br />

Lees verder<br />

http://www.theglobeandmail.com/servlet/story/LAC.20080412.STBUY-<br />

SIDE12/TPStory/Business

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFSS<br />

1 1 / 1 7<br />

Nieuws-Flash!<br />

Petition to Abolish the Federal Reserve<br />

We the undersigned now call on Congress to Abolish the Federal Reserve<br />

System. The latest boom, mania and subsequent bust in the stock market,<br />

real estate, asset prices and now credit around the world are the<br />

direct result of easy money policies of the FED designed to enhance the<br />

profits of certain financial special interests.<br />

Lees verder<br />

http://www.petitiononline.com/fed/petition.html<br />

The Black Death of financial collapse<br />

Een voormalig ambassadeur is pessimistisch..<br />

The financial and economic crisis now upon us is by far the most<br />

menacing of the past century - even more so than the Great<br />

Depression of the 1930s. It is not just a “subprime” crisis; it is<br />

systemic - affecting the entire financial system. It is also global,<br />

affecting various countries in various ways but affecting them<br />

all. In achieving a certain “globalization”, we have been uniquely<br />

successful in globalizing collapse, chaos and misery. It is a globalization<br />

which, in our short-sighted negligence, we never envisaged.<br />

Lees verder<br />

http://www.atimes.com/atimes/Global_Economy/JD10Dj03.html

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFFS<br />

FFFFS<br />

1 2 / 1 7<br />

Nieuws-Flash!<br />

Swaps tied to losses became `Frankenstein’s<br />

monster’<br />

De derivatenberg is niet meer onder controle..<br />

April 15 (Bloomberg) -- The credit-default swap market has become<br />

a lesson in being careful what you wish for now that Wall<br />

Street has taken $245 billion of losses partly tied to such exotica.<br />

Rather than dispersing risk and lowering borrowing costs as former<br />

Federal Reserve Chairman Alan Greenspan predicted, the<br />

contracts have exacerbated the debt crisis. What was intended<br />

as a way for lenders to protect against defaults spawned a market<br />

covering $45 trillion of bonds and loans where no one knows<br />

how much is traded and speculators who bet on deteriorating<br />

credit quality end up forcing that reality.<br />

Some credit-default indexes have morphed into what Wachovia<br />

Corp. analysts led by Glenn Schultz call ``Frankenstein’s monster’’<br />

because they now often drive prices in the so-called cash<br />

bond market, rather than the other way around.<br />

Lees verder<br />

http://www.bloomberg.com/apps/news?pid=20601087&sid=aMX2xgJrr<br />

GB8&refer=home<br />

Credit swaps top $62 trillion in rush to<br />

hedge losses<br />

En hoewel de controle over de deriatenberg kwijt is, vluchten beleggers<br />

nog steeds en masse naar de schijnzekerheid van derivaten..<br />

April 16 (Bloomberg) -- Credit-default swaps worldwide expanded<br />

to cover $62.2 trillion of debt in 2007 as investors rushed to protect<br />

against losses triggered by the collapse of the U.S. subprime<br />

mortgage market.<br />

Contracts outstanding rose 37 percent in the second half of 2007<br />

from $45.5 trillion in the first half, the New York-based International<br />

Swaps and Derivatives Association said today. The market,<br />

which has grown from $34.5 trillion in 2006, doubled in each<br />

of the previous three years as traders used the derivatives as a<br />

cheaper and easier way to invest in corporate debt.<br />

Lees verder<br />

http://www.bloomberg.com/apps/news?pid=20601087&sid=aWx6Laelq<br />

cxA&refer=home

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

FFFFS<br />

1 3 / 1 7<br />

Nieuws-Flash!<br />

Oil surges as investors hunt an ‘anti-dollar’<br />

Over een paar weken komt mijn nieuwe boek `De Permanente Oliecrisis`uit.<br />

Met een beetje geluk klopt de timing dit keer weer. Hoe de dollarcrisis tot<br />

een oliecrisis heeft geleid …<br />

Oil prices have surged to almost $115 a barrel as China builds<br />

up stocks before the Olympics and hedge funds pour money into<br />

commodity futures as a way to exploit the collapse of the dollar.<br />

The Opec producers cartel yesterday defied calls from Gordon<br />

Brown for a boost in output to help ease the global shortage,<br />

sticking to its target of 32 million barrels per day (bpd) for the<br />

next three months.<br />

There is some evidence that Opec has actually cut output by<br />

350,000 bpd since the start of the year -- a hostile move in the<br />

current climate. It blames the latest spike on “speculators,” claiming<br />

that world demand will fall 1.4 million bpd to 85.7 million<br />

this quarter as the US grapples with recession.<br />

Societe Generale said the near $30 spike in prices since early<br />

February is largely due to money pouring into commodity index<br />

funds, now worth some $200 billion. Crude has taken on a “safehaven”<br />

role for investors fleeing the dollar, or those betting that<br />

central banks will let rip with excess liquidity.<br />

Lees verder<br />

http://www.telegraph.co.uk/money/main.jhtml?xml=/money/2008/04/17/cnoil1...<br />

Lezermail<br />

Hierbij een artikel waarvan de schrijver aangeeft dat de huidige bearmarkt<br />

niet zomaar afgelopen is. Daarnaast geeft hij interessante inormatie<br />

over George Soros, die op 77-jarige leeftijd uit zijn pensionering is gestapt<br />

en blijkbaar het roer van zijn hedgefund weer heeft overgenomen.<br />

Om daarmee zijn visie, dat we ons bevinden in een barstende financiële<br />

superbubble, te vertalen in nieuwe shortposities. Wellicht iets voor een<br />

volgende nieuwsflash?<br />

http://www.wallstreetwindow.com/content/node/6373<br />

George Soros heeft weer een interessant boek uitgegeven The credit<br />

risk of 2008 and what it means. Hij pleit hierin oa. dat de ongereguleerde<br />

CDS (Credit default Swaps) markt/instrumenten gereguleerd moeten<br />

worden. Het ontbreekt in die instrumenten aan het stellen van een ge

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

1 4 / 1 7<br />

Nieuws-Flash!<br />

zonde leverage en een margin verplichting die voor ons particulieren wel<br />

geldt bijvoorbeeld met het aankopen van optie en futures. Vervolgens<br />

ziet hij een ineenstorting van de financiële markten niet snel gebeuren<br />

doordat regeringen, met name de US en UK, banken die dreigen<br />

om te vallen gaan steunen. Zie Bear Stearns (gereguleerde overname)<br />

en NorthernRock (eigenlijk een nationalisatie). Om faillissement en/of<br />

nationalisatie te voorkomen gaan financiële instellingen (die problemen<br />

hebben) zich herkapitaliseren. Er schijnt 54 triljoen uit te staan in die<br />

CDS instrumenten. In hoeverre kan een regering (lees US treasury/FED)<br />

dit financieren/volhouden zodat markten niet instorten?<br />

The Face of a Prophet<br />

http://www.nytimes.com/2008/04/11/business/11soros.html?ei=5065&<br />

en=5c25ed573f393193&ex=1208577600&partner=MYWAY&pagewante<br />

d=print<br />

Een geniaal stripje dat de kredietcrisis uitlegt:<br />

http://www.slideshare.net/guesta9d12e/subprime-primer-277484/<br />

Misschien leuk voor in de nieuws-flash.<br />

Groet, Tom<br />

Ik lees met veel plezier je berichten, de waarde van de woning is direct<br />

afhankelijk van de betaalbaarheid van de lasten, door de woonquote<br />

van 6 keer inkomen naar 4,5 keer inkomen terug te draaien “ter bescherming<br />

van de consument”zie je dat de prijzen 25% moeten dalen<br />

om vervolgens weer “betaalbaar” te zijn. Dus ook de huizenmarkt wordt<br />

naar een dieptepunt gestuurd door het centrale beleid.<br />

P.s… ik heb zeer veel respect voor jou en je collega’s die het aandurven<br />

om tegen de grote geldlobby´s in te gaan.<br />

Met vriendelijke groet,<br />

Robert<br />

Erkend Hypotheek Adviseur<br />

Beste Willem Middelkoop,<br />

Even om bij de les te blijven wat grafiekjes van de H3 release van<br />

de FED. Daarin is te zien dat de dramatische, nooit eerder vertoonde<br />

veranderingen in de non-borrowed reserves van Amerikaanse banken<br />

zich voortzet... Huidige stand Non Borrowed Reserves Amerikaanse<br />

banken: - $ 98.981.000.000 ten opzichte van een Total Reserves van $<br />

44.969.000.000.<br />

Normaal gesproken is het bedrag dat bijgeleend wordt (1959 - 2008)<br />

gemiddeld 3% van de totale reserves, met uitschieters van 23% en<br />

19% in 1984 en 1974. ((total reserves - non borrowed reserves)/total<br />

reserves).

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

1 5 / 1 7<br />

Humor<br />

WALL STREET ACCOUNTING:<br />

Nieuws-Flash!<br />

Op dit moment wordt er een bedrag ter grootte van 340% van de totale<br />

reserves van de banken bijgeleend. zie grafieken op http://www.<br />

federalreserve.gov/releases/h3/Current/<br />

Met vriendelijke groet, Michiel<br />

Hallo Willem,<br />

Ik ben een 4ejaars student economie, fiscale economie en rechten<br />

aan de Erasmus Universiteit Rotterdam en volg de nieuwsflash en heb<br />

ook het boek “als de dollar valt” al meerdere malen gelezen. Nu zag ik<br />

laatst een artikel dat vrij duidelijk is en veel informatie verschaft over<br />

waarom de consumenteninflatie ondanks de enorme geldgroei zo (relatief)<br />

extreem laag is, en waarom dit de komende tijd zeer goed om<br />

zou kunnen slaan naar een hoge consumenteninflatie. De belangrijkste<br />

reden is volgens het artikel dat al het extra geld is geparkeerd in<br />

beleggingsproducten, die de consumenteninflatie jarenlang laag hield.<br />

Tevens wordt in het artikel ook de Amerikaanse situatie besproken<br />

waar is gestopt met het verzamelen en verstrekken van informatie<br />

over de M3 geldhoeveelheid en de risico’s die dit met zich meebrengt.<br />

Het was voor mij in ieder geval een heel duidelijk en informatief artikel.<br />

Het artikel is vrij toegankelijk via: http://www.eur.nl/few/economieopinie/artikelen/april_2008/monetaire_struisvogelpolitiek/<br />

of www.<br />

eur.nl en dan naar economische faculteit en dan het artikel ‘Monetaire<br />

struisvogelpolitiek’.<br />

Vriendelijke groet, Rick<br />

There are two sides of the balance sheet - the left side and the right side.<br />

On the left side, there is nothing right, and on the right side, there is nothing<br />

left!

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

1 6 / 1 7<br />

Plaatje<br />

Nieuws-Flash!<br />

Op dit plaatje is in een oogopslag te zien wat de kredietcrisis tot nu toe<br />

voor gevolgen heeft gehad voor de bankbalans van de Fed. De hoeder<br />

van de dollar is minder solide geworden..<br />

Video<br />

Jim Sinclair, voormalig adviseur van Paul Volcker, wordt op CNN (jawel,<br />

CNN!) geïnterviewd over goud.<br />

http://www.youtube.com/watch?v=pyB_NmlNFqU

1 8 a p r i l 2 0 0 8 n r 0 2 8<br />

1 7 / 1 7<br />

Quote<br />

Nieuws-Flash!<br />

“Capital must protect itself in every way...Debts must be collected and<br />

loans and mortgages foreclosed as soon as possible. When through a<br />

process of law the common people have lost their homes, they will be<br />

more tractable and more easily governed by the strong arm of the law<br />

applied by the central power of leading financiers. People without homes<br />

will not quarrel with their leaders. This is well known among our principal<br />

men now engaged in forming an imperialism of capitalism to govern the<br />

world. By dividing the people we can get them to expend their energies in<br />

fighting over questions of no importance to us except as teachers of the<br />

common herd.”<br />

Taken from the Civil Servants’ Year Book, “The Organizer” January 1934<br />

‘But the euro does have growing strengths. At current market exchange<br />

rates, the European Union is now larger economically than the US. New<br />

central and eastern European members are bringing enormous dynamism<br />

and flexibility. At the same time, the ECB has gained considerable credibility<br />

from its handling of the global credit crisis. Indeed, if the euro zone<br />

can persuade Great Britain to become a full-fledged member, thereby<br />

acquiring one of the world’s two premier financial centers (London), the<br />

euro might really start to look like a viable alternative to the dollar…’<br />

Kenneth Rogoff, Harvard professor<br />

Willem Middelkoop is uitgever van de Middelkoop Discovery Alert. Een Engelstalige<br />

emailservice over nieuwe grondstofontdekkingen voor ervaren<br />

beleggers. (www.discovery-investing.com).<br />

Privé-advies is alleen mogelijk op afspraak. Aanmelden via www.willemmiddelkoop.nl