The Integrated Gas Major - BG Group

The Integrated Gas Major - BG Group

The Integrated Gas Major - BG Group

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>BG</strong> <strong>Group</strong><br />

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

London • 7 th February 2008

<strong>BG</strong> <strong>Group</strong><br />

Welcome<br />

Sir Robert Wilson • Chairman

<strong>BG</strong> <strong>Group</strong><br />

Introduction<br />

Frank Chapman • Chief Executive

Legal Notice<br />

Certain statements included in this presentation contain forward-looking information concerning <strong>BG</strong><br />

<strong>Group</strong>’s strategy, operations, financial performance or condition, outlook, growth opportunities or<br />

circumstances in the countries, sectors or markets in which <strong>BG</strong> <strong>Group</strong> operates. By their nature,<br />

forward-looking statements involve uncertainty because they depend on future circumstances, and<br />

relate to events, not all of which are within <strong>BG</strong> <strong>Group</strong>'s control or can be predicted by <strong>BG</strong> <strong>Group</strong>.<br />

Although <strong>BG</strong> <strong>Group</strong> believes that the expectations reflected in such forward-looking statements are<br />

reasonable, no assurance can be given that such expectations will prove to have been correct.<br />

Actual results could differ materially from those set out in the forward-looking statements. For a<br />

detailed analysis of the factors that may affect our business, financial performance or results of<br />

operations, we urge you to look at the “Risk Factors” included in <strong>BG</strong> <strong>Group</strong> plc’s Annual Report and<br />

Accounts 2006. Nothing in these results should be construed as a profit forecast and no part of<br />

these results constitutes, or shall be taken to constitute, an invitation or inducement to invest in <strong>BG</strong><br />

<strong>Group</strong> plc or any other entity, and must not be relied upon in any way in connection with any<br />

investment decision. <strong>BG</strong> <strong>Group</strong> undertakes no obligation to update any forward-looking statements.<br />

4

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Key messages<br />

• Good 2007 results<br />

• LNG flexibility delivering value<br />

• Earnings outlook to 2009 confirmed<br />

• Total E&P resources now 10 bn boe, up 2 bn boe<br />

• E&P production potential 6-8% CAGR 2005 to 2020<br />

Delivering value to shareholders<br />

5

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Total operating profit<br />

£m<br />

3500<br />

3000<br />

2500<br />

2000<br />

1500<br />

1000<br />

500<br />

0<br />

160<br />

229<br />

330<br />

1997 2000 2003 2006<br />

E&P<br />

Continuing operations excluding disposals, certain re-measurements and impairments<br />

Results prior to 2003 stated under UK GAAP; post 2003 stated under IFRS. 2003, 2004 & 2005 restated for IFRIC 4.<br />

Total operating profit includes <strong>BG</strong>’s share of pre-tax operating results from joint ventures and associates.<br />

Strong record of growth<br />

CAGR 35% 1997-2007<br />

688<br />

833<br />

888<br />

1,287<br />

1,520<br />

T&D, LNG, Power & Other<br />

2,389<br />

3,103<br />

3,248<br />

2007<br />

6

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Key messages<br />

• Good 2007 results<br />

• LNG flexibility delivering value<br />

• Earnings outlook to 2009 confirmed<br />

• Total E&P resources now 10 bn boe, up 2 bn boe<br />

• E&P production potential 6-8% CAGR 2005 to 2020<br />

Delivering value to shareholders<br />

7

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Overview<br />

• Strategy<br />

• 2007 results<br />

• Portfolio for growth<br />

• Conclusions<br />

8

<strong>BG</strong> <strong>Group</strong><br />

Strategy<br />

Frank Chapman • Chief Executive

Strategy<br />

<strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Connect gas to<br />

high value markets<br />

• Build & access markets<br />

• Serve customers<br />

Secure competitively<br />

priced resources<br />

• Equity reserves<br />

• Contracted resources<br />

Skills to succeed across the gas chain<br />

Strategy delivering value<br />

<strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

10

Strategy<br />

Business environment<br />

• High commodity prices<br />

• Cost inflation<br />

• Increased demand for LNG<br />

• Government’s priorities . . .<br />

domestic vs export<br />

• Replacing reserves<br />

<strong>BG</strong> well positioned<br />

Trend <strong>BG</strong> response<br />

• Strong cash conversion<br />

• Long-life, low cost base<br />

• Flexible LNG supply portfolio<br />

• <strong>Integrated</strong> approach & alignment<br />

• Monetise resource base<br />

11

<strong>BG</strong> <strong>Group</strong><br />

2007 results<br />

Ashley Almanza • Chief Financial Officer

2007 results<br />

<strong>Group</strong> highlights<br />

• Good operating performance<br />

• EPS +11% (+17% underlying*)<br />

• Cash flow from operations +10%<br />

• Strong financial position<br />

• Robust outlook<br />

• Dividend +30%<br />

* At constant upstream prices and US$/UK£ exchange rate<br />

Good results, positive outlook<br />

13

2007 results<br />

E&P volumes (mmboe)<br />

219.2 (3.5)<br />

2006 Disposals CATS Underlying<br />

growth<br />

Underlying growth of 5%<br />

(5.5)<br />

10.1 220.3<br />

2007<br />

14

2007 results<br />

E&P benchmarking<br />

$12<br />

$10<br />

$8<br />

$6<br />

$4<br />

$2<br />

$0<br />

Top quartile unit opex performance<br />

Annual unit opex cost trend ($/boe)<br />

2002 2003 2004 2005 2006 2007<br />

<strong>BG</strong> Top quartile Combined Companies Bottom quartile<br />

Source: Evaluate Energy 2007, <strong>BG</strong> <strong>Group</strong><br />

Peer <strong>Group</strong> includes Super <strong>Major</strong>s, US and European <strong>Integrated</strong> <strong>Major</strong>s<br />

15

2007 results<br />

E&P 2007 total operating profit (£m)<br />

2457<br />

241<br />

2006 Pre E&A &<br />

CATS<br />

(64)<br />

E&A<br />

expense<br />

Continuing operations excluding disposals, certain re-measurements and impairments<br />

Total operating profit includes <strong>BG</strong> <strong>Group</strong>’s share of pre-tax operating results from joint ventures and associates<br />

Good operating performance<br />

2634<br />

(127)<br />

(120)<br />

2387<br />

Underlying CATS As reported<br />

Price/<br />

FX<br />

16

2007 results<br />

2007 proved reserve additions (mmboe)<br />

Underlying performance<br />

Organic reserves<br />

replacement = 107%<br />

172<br />

63<br />

Revisions Developments<br />

& sales<br />

(117)<br />

Underlying organic reserves replacement 107%<br />

(8)<br />

Acquisitions<br />

& disposals<br />

2007<br />

Production<br />

110<br />

Price Net<br />

17

2007 results<br />

E&P benchmarking<br />

$25<br />

$20<br />

$15<br />

$10<br />

$5<br />

$0<br />

Top quartile unit F&D performance<br />

3 year F&D cost trend ($/boe)<br />

2001-03 2002-04 2003-05 2004-06 2005-07<br />

<strong>BG</strong> Top quartile Combined Companies Bottom quartile<br />

Source: Evaluate Energy 2007, <strong>BG</strong> <strong>Group</strong><br />

Peer <strong>Group</strong> includes Super <strong>Major</strong>s, US and European <strong>Integrated</strong> <strong>Major</strong>s<br />

18

2007 results<br />

LNG total operating profit<br />

Step change in performance<br />

Q4<br />

2007<br />

Full Year<br />

2007<br />

Full Year<br />

ΔYOY<br />

Shipping & Marketing £145m £463m +39%<br />

Liquefaction £38m £127m +22%<br />

Business Development (£20m) (£69m) -18%<br />

Total £163m £521m +48%<br />

Continuing operations excluding disposals, certain re-measurements and impairments<br />

Total operating profit includes <strong>BG</strong> <strong>Group</strong>’s share of pre-tax operating results from joint ventures and associates<br />

19

2007 results<br />

T&D total operating profit (£m)<br />

231<br />

2006<br />

25<br />

Comgas<br />

Continuing operations excluding disposals, certain re-measurements and impairments<br />

Total operating profit includes <strong>BG</strong> <strong>Group</strong>’s share of pre-tax operating results from joint ventures and associates<br />

Comgas and India driving performance<br />

12<br />

2<br />

270<br />

(23)<br />

247<br />

India Other<br />

Underlying Interconnector As<br />

disposal reported<br />

20

2007 results<br />

Power total operating profit (£m)<br />

106<br />

2006<br />

Continuing operations excluding disposals, certain re-measurements and impairments<br />

Total operating profit includes <strong>BG</strong> <strong>Group</strong>’s share of pre-tax operating results from joint ventures and associates<br />

Contribution from acquisitions<br />

22 2 130<br />

Acquisitions<br />

(part year)<br />

Other 2007<br />

21

2007 results<br />

E&P: Production<br />

1000<br />

800<br />

600<br />

400<br />

200<br />

0<br />

2005A 2006A 2007A<br />

2009 2012<br />

Growth applies to the end of the period, within the period growth is non-linear<br />

At 2008 reference conditions (see appendix)<br />

Production outlook<br />

<strong>BG</strong> net production (000’s boepd)<br />

Medium term 2007-09 Long term 2010-12<br />

Key projects:<br />

• Buzzard<br />

• Karachaganak<br />

• Trinidad E&P<br />

• Panna/Mukta/Tapti<br />

• Hasdrubal<br />

2005-12<br />

CAGR 6-8%<br />

2009<br />

680-710,000<br />

boepd<br />

Key opportunities:<br />

• Karachaganak<br />

• Tupi<br />

• Bongkot South<br />

• Dolphin<br />

• Bongkot North<br />

• Bream<br />

• Jasmine<br />

• Abu Butabul<br />

• Panna/Mukta/Expansion<br />

• Rosetta<br />

• Hassi Ba Hamou<br />

• Risked exploration<br />

22

2007 results<br />

Production and price effects<br />

Canada<br />

T&T offshore<br />

T&T onshore<br />

Bolivia<br />

Brazil<br />

Norway<br />

Tax royalties PSC /Tax royalties with minor price impact PSC with price impact<br />

PSC price impact less than 15,000 boepd in 2012<br />

UK<br />

Algeria Tunisia<br />

Egypt<br />

Kazakhstan<br />

Oman<br />

India<br />

Thailand<br />

23

2007 results<br />

LNG: Outlook<br />

Liquefaction<br />

Shipping<br />

and<br />

Marketing<br />

* Pre-tax nominal return on capital invested<br />

Capital invested<br />

2009 – £0.8bn<br />

2008 – 13.5 mtpa<br />

2009 – 13.5 mtpa<br />

** EBITDA margin:<br />

• 1 mtpa = 51.7 tbtu<br />

• Portfolio average expressed as a percentage of sales at $7.25/mmbtu Henry Hub<br />

• Exchange rate assumption $2:£1<br />

• Excludes business development expenditure<br />

EBITDA margin raised from 18% to 30%<br />

Return *<br />

2008 – 15%<br />

2009 – 16% (was 13%)<br />

Volumes EBITDA margin **<br />

2008 – 30%<br />

2009 – 30% (was 18%)<br />

24

2007 results<br />

Framework for growth<br />

EPS<br />

2006 2009<br />

Schematic representation only<br />

Growth applies to the end of the period, within the period growth is non-linear<br />

* World total energy consumption 2003-2030. Source: EIA 2006<br />

** At $55 Brent conditions, $7.25 Henry Hub<br />

Outlook confirmed<br />

Key growth projects<br />

• Karachaganak<br />

• Buzzard<br />

• US LNG<br />

• Trinidad E&P/ LNG<br />

• Hasdrubal<br />

Based on firm<br />

projects<br />

In <strong>BG</strong> plans**<br />

Energy growth*<br />

Zero growth<br />

25

2007 results<br />

Capital investment 2007-2009 (£ billion)<br />

7.5<br />

0.3<br />

Prior year Exploration Acquisitions Inflation FX<br />

Current<br />

Maintaining capital discipline<br />

0.9<br />

0.7<br />

(0.6)<br />

8.8<br />

26

2007 results<br />

Capital structure and dividend<br />

• Capital investment for 2008 – 2009 £6.3 bn<br />

• Substantial growth in investment opportunities<br />

• Dividend re-based: +30%<br />

Long-term growth, good returns<br />

27

2007 results<br />

Summary<br />

• EPS +11% (+17% underlying*)<br />

• E&P production growth 2005 to 2012: CAGR 6-8%<br />

• LNG margin raised from 18% to 30%<br />

• Growing opportunity set<br />

• Positive outlook for EPS<br />

• Strong financial position, dividend re-based +30%<br />

* At constant upstream prices and US$/UK£ exchange rate<br />

Delivering value to shareholders<br />

28

<strong>BG</strong> <strong>Group</strong><br />

Portfolio for growth

Portfolio for growth<br />

Key country portfolio<br />

USA<br />

Trinidad &<br />

Tobago<br />

Brazil<br />

UK<br />

Norway<br />

Tunisia<br />

Nigeria<br />

Egypt<br />

Core countries Potential core countries<br />

Focusing on developing material countries<br />

Kazakhstan<br />

Oman<br />

India<br />

30

Portfolio for growth<br />

E&P asset base<br />

700<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

<strong>BG</strong> net production (000’s boepd) of assets on stream at end 2006 only<br />

Assets in production in 2006 only<br />

0<br />

2006A 2009 2012 2015<br />

At 2008 reference conditions (see appendix)<br />

Excludes Buzzard as not on stream at end 2006<br />

Existing E&P assets provide a strong base<br />

31

Portfolio for growth<br />

LNG contracted volumes<br />

15<br />

10<br />

5<br />

<strong>BG</strong> contracted volumes mtpa<br />

Contracted volumes only<br />

0<br />

2006A 2009 2012 2015 2018 2021 2024<br />

LNG business underpinned by contracted volumes<br />

32

Portfolio for growth<br />

Global LNG & US: Industry context<br />

• Demand continuing to grow<br />

• Supply projects delayed<br />

– Cost escalation<br />

– Construction industry capacity<br />

– Government priorities<br />

<strong>BG</strong> portfolio : Longevity, cost leadership and global flexibility<br />

33

Portfolio for growth<br />

Global LNG & US: Costs<br />

1000<br />

World-wide liquefaction capex ($/tpa)<br />

800<br />

600<br />

400<br />

200<br />

0<br />

1998 2002 2006 2010<br />

Start up year<br />

Source: Poten & Partners, <strong>BG</strong><br />

Greenfield projects<br />

Expansion projects<br />

<strong>BG</strong> liquefaction projects*<br />

* <strong>BG</strong> investment<br />

Long-term, low cost advantage<br />

1000<br />

800<br />

600<br />

400<br />

200<br />

US regasification capex ($/mscfd)<br />

1998 2002 2006 2010<br />

Start up year<br />

Source: Public data, <strong>BG</strong><br />

Greenfield projects<br />

Expansion projects<br />

<strong>BG</strong> regasification projects*<br />

* <strong>BG</strong> investment<br />

34

Portfolio for growth<br />

Global LNG & US: Supply<br />

mtpa<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

NLNG<br />

Train 7<br />

Contracted<br />

to 2023<br />

Australia<br />

Existing Future<br />

Building on material long-term base supply<br />

OKLNG<br />

& Brass<br />

Egypt<br />

& T&T<br />

Other term supply<br />

Nigerian LNG T4/5<br />

Equatorial Guinea<br />

Egyptian LNG T2<br />

Atlantic LNG T4<br />

Atlantic LNG T2/3<br />

35

Portfolio for growth<br />

Global LNG & US: Markets<br />

USA<br />

Mexico<br />

Chile<br />

Existing import capacity<br />

Existing liquefaction<br />

Trinidad<br />

UK<br />

Spain<br />

Current and future equity positions<br />

Nigeria<br />

Belgium<br />

Italy<br />

Egypt<br />

Flexible portfolio delivering volumes to premium markets<br />

EG<br />

Future import capacity<br />

Future liquefaction<br />

India<br />

S. Korea<br />

Taiwan<br />

In 2007, <strong>BG</strong> supplied 3.5 mtpa, or<br />

approximately 50%* of all Atlantic<br />

Basin volumes into Asia<br />

* Source: <strong>BG</strong>/CERA<br />

Japan<br />

Markets supplied in 2007<br />

Australia<br />

Long-term purchases (contracted)<br />

36

Portfolio for growth<br />

Global LNG & US: US portfolio<br />

Lake Charles<br />

Houston<br />

LNG<br />

Atlanta<br />

Cypress<br />

Masspower<br />

Elba Island<br />

Miami<br />

Lake Road<br />

New York<br />

Boston<br />

LNG<br />

Dighton<br />

Regasification<br />

Storage<br />

Strong US integrated position creates additional value<br />

Power<br />

Transport Markets<br />

37

Portfolio for growth<br />

Global LNG & US: Conclusions<br />

• Strong competitive position<br />

– Large, long-life supply base<br />

– Low cost structure<br />

– Flexible portfolio, serving global markets<br />

– <strong>Integrated</strong> US portfolio<br />

• Market-led strategy<br />

• Capturing value globally<br />

Sustainable competitive advantage<br />

38

Portfolio for growth<br />

UK: Jasmine<br />

30/6-7<br />

Discovery<br />

well<br />

30/6-7<br />

2008<br />

sidetracks<br />

30/6-6<br />

Jasmine<br />

discovery<br />

well<br />

30/6-6z<br />

sidetrack<br />

30/6-7 well<br />

Jasmine<br />

West<br />

Jasmine<br />

Northern Terrace<br />

Undrilled Potential<br />

Jasmine<br />

Northern<br />

Terrace<br />

Jasmine<br />

West<br />

Julia<br />

Horst<br />

<strong>Major</strong> discovery, with significant upside<br />

• <strong>BG</strong> 30.5%<br />

• Jasmine area appraisal ongoing<br />

• Jasmine West<br />

– Gross reserves 100-176-275 mmboe<br />

– Sidetrack well planned in 2008<br />

– Concept selection underway<br />

– Planned on stream 2011<br />

• Northern Terrace well success<br />

– Discovery well 30/6-7<br />

– Gross reserves 20-100+ mmboe<br />

– Sidetrack well planned in 2008<br />

39

Portfolio for growth<br />

UK: Jackdaw<br />

30/2a Lower<br />

Courageous<br />

30/2c Jade<br />

Jade<br />

Northern<br />

appraisal well<br />

30/2a-6<br />

Jackdaw<br />

30/2c<br />

UK<br />

30/3a<br />

Lower<br />

30/3b<br />

Norway<br />

Important HPHT discovery, appraisal underway<br />

• <strong>BG</strong> operator 30/2c and 30/2a<br />

• <strong>BG</strong> increased equity in Jackdaw<br />

– 30/2a <strong>BG</strong> 43.1% (from 34.4%)<br />

– 30/2c <strong>BG</strong> 36.0%<br />

• Gross reserves 20-140-250 mmboe<br />

• First appraisal well drilling<br />

• Second appraisal well in 2009<br />

• Well head platform development<br />

• Planned on stream 2013<br />

40

Portfolio for growth<br />

UK: Buzzard<br />

45<br />

30<br />

15<br />

Producers<br />

Injectors<br />

Field limit<br />

Dec 2007<br />

Field limit in 2003<br />

Southern terrace<br />

Northern panel<br />

Central panel<br />

Southern panel<br />

<strong>BG</strong> net production (000’s boepd)<br />

Enhancing reserves and production<br />

2km<br />

Further potential<br />

0<br />

2007A 2009 2011 2012 2013 2015<br />

At 2008 reference conditions (see appendix)<br />

• <strong>BG</strong> 21.73%<br />

• <strong>Major</strong> oil field, on stream 2007<br />

• Peak production 220,000 boepd<br />

• Field area extended<br />

• Gross reserves 600+ mmboe<br />

• Sweetening platform in 2010<br />

• Potential to extend plateau<br />

41

Portfolio for growth<br />

UK: Production<br />

200<br />

150<br />

100<br />

50<br />

0<br />

<strong>BG</strong> net production (000’s boepd)<br />

50 mmboe<br />

Producing Assets<br />

2006A 2009 2012 2015<br />

At 2008 reference conditions (see appendix)<br />

Further<br />

potential<br />

Delivering<br />

projects<br />

Potential to continue extending “plateau”<br />

• Delivering projects<br />

– Jasmine on stream 2011<br />

– Jackdaw on stream 2013<br />

– Other incrementals 2009+<br />

• “Plateau” of 50 mmboe to 2012<br />

• Further potential<br />

– Field upsides<br />

– Exploration<br />

42

Portfolio for growth<br />

Kazakhstan: Karachaganak<br />

Karachaganak performing strongly<br />

• Tenth anniversary of FPSA<br />

• Record production performance<br />

• Operations improvement projects<br />

• Fourth stabilisation train<br />

– Tie in during 2008 shutdown<br />

– On schedule for 2009<br />

• Western export capacity<br />

– Actual 2007: 9 mtpa<br />

– Post fourth train: 10.3 mtpa<br />

– Planned with Phase III: 16.1 mtpa<br />

• Long term Orenburg GSA in-place<br />

43

Portfolio for growth<br />

Kazakhstan: Karachaganak Phase III & beyond<br />

250<br />

200<br />

150<br />

100<br />

50<br />

0<br />

<strong>BG</strong> net production (000’s 000’s boepd) boepd<br />

2006A 2009 2012 2015 2018<br />

Phase II<br />

Phase IIM & de-bottlenecking<br />

4th Train & expanded Phase III with LPG<br />

Full Potential<br />

At 2008 reference conditions (see appendix)<br />

Overall profile inline but splits will change<br />

• Phase III being progressed<br />

– Development concept agreed<br />

– <strong>Gas</strong> sales 16 bcma confirmed<br />

– Expanded to include LPG<br />

– FEED over 50% complete<br />

Phase III expanded and being optimised during FEED<br />

– Gross reserves 2.4 bn boe<br />

– Sanction 2008; on stream 2012<br />

• Further potential in Karachaganak<br />

44

Portfolio for growth<br />

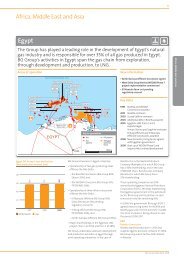

Egypt: E&P and LNG<br />

Seismic image<br />

El Burg<br />

<strong>BG</strong> 70%<br />

50km<br />

Damietta<br />

El Manzala<br />

<strong>BG</strong> 100%<br />

Port Said<br />

Excellent track record and enhanced outlook<br />

• Egypt gas production in 2007<br />

– <strong>BG</strong> fields produce over 40% of total<br />

– Split ca 50/50 domestic/LNG<br />

• WDDM Phase IV on stream<br />

• Rosetta Phase III on stream, Q1 ’08<br />

• Prospect inventory enhanced<br />

• Exploration drilling 2008<br />

– El Burg & El Manzala<br />

– Potential for early development<br />

45

Portfolio for growth<br />

Trinidad & Tobago<br />

Long-term production base with growth potential<br />

• Operational improvements<br />

• ECMA Dolphin<br />

– New domestic sales, 1.2 tcf<br />

– Start July 2009, 220 mmscfd<br />

– De-bottlenecking<br />

– Also, ca 1 tcf of uncontracted gas<br />

• NCMA – 3c/d Poinsettia project<br />

– Plateau maintenance<br />

• Farm-in to Block 5c (<strong>BG</strong> 30%)<br />

– Three wells<br />

– Successful tests on first well<br />

46

Portfolio for growth<br />

India<br />

Panna<br />

Mukta<br />

Tapti<br />

Gujarat <strong>Gas</strong><br />

Existing E&P assets<br />

<strong>BG</strong> in 0India<br />

Existing Distribution assets<br />

Mahanagar <strong>Gas</strong><br />

KG-OSN-2004/1<br />

New E&P acreage<br />

Expanding the portfolio across the gas chain<br />

• E&P volumes 2006-7 grew 33%<br />

• Secured KG–OSN–2004/1<br />

– 3D seismic in 2008<br />

• Delivered 5 LNG cargoes<br />

• Set up gas marketing business<br />

• T&D volumes 2006-7 grew 9%<br />

47

Portfolio for growth<br />

India<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

<strong>BG</strong> net production 000’s boepd<br />

<strong>BG</strong> net production (000’s boepd)<br />

Mukta Existing<br />

Panna Plan<br />

Panna Existing<br />

Tapti Existing<br />

Panna/Mukta Potential<br />

Mukta Plan<br />

Tapti Plan<br />

2006A 2009 2012 2015 2018<br />

At 2008 reference conditions (see appendix)<br />

• Panna (<strong>BG</strong> 30%)<br />

Significant potential in existing producing assets<br />

– Gross HIIP 1.7 bn boe<br />

– Added 2 WHP’s and 15 wells<br />

– Started 2 WHP’s, 9 wells, 21 infills<br />

• Mukta (<strong>BG</strong> 30%)<br />

– Gross HIIP 900 mmboe<br />

– New 3D seismic underway<br />

– Re-drilling 3 wells in process<br />

– Evaluating further development<br />

• Tapti (<strong>BG</strong> 30%)<br />

– Completion of mid-Tapti project<br />

– Further compression & satellites<br />

– Extends plateau<br />

48

Portfolio for growth<br />

Tunisia<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

<strong>BG</strong> net production (000’s boepd)<br />

Hasdrubal<br />

Miskar Infill/<br />

Debottlenecking<br />

Miskar<br />

2006A 2009 2012 2015 2018<br />

At 2008 reference conditions (see appendix)<br />

Miskar North<br />

Exploration<br />

Optimising Miskar, developing Hasdrubal<br />

• Miskar (<strong>BG</strong> 100%)<br />

– 3 infill wells drilled in 2007<br />

– 3 infill wells in 2008/09<br />

– 5% de-bottlenecking by 2009<br />

– Miskar North drilling<br />

• Hasdrubal (<strong>BG</strong> 50%)<br />

– Offshore platform / 6 wells<br />

– Project ca 45% complete<br />

– On stream 2009<br />

49

Portfolio for growth<br />

Thailand: Bongkot<br />

30<br />

20<br />

10<br />

0<br />

<strong>BG</strong> net production (000’s boepd)<br />

BN Phase 3E, 3F, 3G, 3H<br />

Bongkot North (BN) Existing<br />

Full potential<br />

Bongkot South<br />

2006A 2009 2012 2015<br />

At 2008 reference conditions (see appendix)<br />

Growing production into the next decade<br />

• Bongkot North (<strong>BG</strong> 22.22%)<br />

– Record production in 2007<br />

– Continuing to extend plateau<br />

– Licence extended to 2023<br />

– Three E&A wells in 2008<br />

• Bongkot South (<strong>BG</strong> 22.22%)<br />

– Five successful E&A wells in 2007<br />

– Licence extended to 2023<br />

– Gross reserves 1.2 tcf, 22 mmbbls<br />

– CPP, 13 WHPs, ca 100 wells<br />

– Sanction 2008, first gas 2011/12<br />

50

Portfolio for growth<br />

Nigeria<br />

OKLNG<br />

OPL 332<br />

Upstream<br />

focus area<br />

OPL 286-DO<br />

50km<br />

Two further<br />

farm-ins*<br />

Opportunities in LNG and E&P<br />

• OKLNG (<strong>BG</strong> 14.25%)<br />

– Four trains, ca 5.5 mtpa each<br />

– Shareholders Agreement signed<br />

– Technical and cost reviews<br />

• OPL 332 (<strong>BG</strong> 45% & operator)<br />

– Frontier block, E&A drilling 2009<br />

• OPL 286-DO (<strong>BG</strong> 66% & operator)<br />

– Boi discovery ca 100 mmboe gross<br />

– Gross unrisked potential > 1bn boe<br />

– E&A drilling in 2008 and 2009<br />

• Two further farm-ins*<br />

* Subject to Government approval<br />

51

Portfolio for growth<br />

Oman: Abu Butabul<br />

Multi tcf discovery under appraisal<br />

• <strong>BG</strong> 100%, 30 year EPSA<br />

• Gross GIIP 2-11-17 tcf<br />

• Field 3D seismic acquired<br />

• Two rigs secured for appraisal<br />

• Appraisal drilling commenced<br />

– 6-8 wells in 2007/8<br />

– Vertical wells, proppant fracs<br />

• Targeting production end 2010/11<br />

– FEED in 2008<br />

– Initial offtake of 150-250 mmscfd<br />

• Exploration area seismic acquired<br />

52

Portfolio for growth<br />

Norway<br />

Exploration drilling<br />

Appraisal drilling<br />

Jordbaer<br />

North<br />

Sea<br />

PI North<br />

Bergen<br />

Nucula<br />

discovery<br />

Norwegian<br />

Sea<br />

Mandarin<br />

Ververis<br />

Barents<br />

Sea<br />

Trondheim<br />

Bream discovery<br />

Oslo<br />

Tromso<br />

Significant year for <strong>BG</strong> in Norway<br />

• <strong>BG</strong> 22 licences, 14 operated<br />

• Drilling 4 prospects in 2008<br />

– 3 <strong>BG</strong> operated<br />

– Mandarin & Jordbaer high impact<br />

• Rigs secured<br />

• Further drilling in 2009<br />

• Bream (<strong>BG</strong> 40% & operator)<br />

– Key appraisal well 2008<br />

• Assessing Nucula discovery<br />

53

Portfolio for growth<br />

Australia: Queensland <strong>Gas</strong> Co (QGC) alliance<br />

Australia<br />

QGC assets in<br />

Walloon Fairway<br />

Surat Basin<br />

Adelaide<br />

Melbourne<br />

Canberra<br />

Entry into Australia<br />

Proposed<br />

LNG plant<br />

Sydney<br />

Brisbane<br />

200 km<br />

• <strong>BG</strong>/QGC alliance<br />

– 20% of assets / 9.9% shares<br />

– Consideration £299m<br />

– Option for further 10% of assets<br />

• High quality, low cost CSG* play<br />

• Early stage of exploitation<br />

• Over 7 tcf resource potential<br />

• Domestic market growth<br />

• Proposed 3-4 mtpa LNG plant<br />

* CSG = Coal Seam <strong>Gas</strong><br />

54

Portfolio for growth<br />

Brazil: Comgas<br />

Gás Natural da Bolivia<br />

GASBOL<br />

Piracicaba<br />

Sumaré<br />

São Paulo state<br />

Indaiatuba<br />

Gása para a Região Sul<br />

GASBOL – Fase 2<br />

100km<br />

Rio Claro<br />

Limeira<br />

Minas Gerais<br />

Valinhos<br />

Americana<br />

Braganca<br />

Campinas<br />

Jundiai<br />

Castelo<br />

Itatiba<br />

São Paulo<br />

Campinas II<br />

RMSP<br />

São Paulo<br />

Santos<br />

Bacia de Santos<br />

GASAN<br />

Legend<br />

Expansion Projects in place<br />

Future Expansion Projects<br />

Taubaté<br />

São José dos Campos<br />

Bacia de<br />

Santos<br />

GASPAL<br />

Rio de Janeiro<br />

Atlantic Ocean<br />

Good potential for continued growth<br />

• Brazil’s largest gas distributor<br />

– 2007 gas sales 13.8 mmcmd<br />

– Over 570,000 customers connected<br />

• Customer growth 8.7% pa 2002-07<br />

• Good economic outlook<br />

• Potential to grow market<br />

– Geographic expansion<br />

– Focus on residential & commercial<br />

• Regulatory tariff review 2009<br />

55

Portfolio for growth<br />

Brazil: Santos Basin overview<br />

BM-S- 13<br />

BM-S- 47<br />

50 km<br />

BM-S- 52<br />

Rio de Janeiro<br />

BM-S- 50<br />

Parati<br />

BM-S- 9<br />

Carioca<br />

BM-S- 10<br />

Tupi<br />

BM-S- 11<br />

<strong>Major</strong> new hydrocarbon province<br />

• Santos Basin Pre-Salt<br />

– 300 km offshore<br />

– Water depth 2,000m+<br />

– Salt layers up to 2,000m thick<br />

– Carbonate reservoirs<br />

• <strong>BG</strong> well results to date<br />

– Four out of four successful wells<br />

– Exhibit excellent reservoir quality*<br />

* Test rates limited by equipment<br />

56

Portfolio for growth<br />

Brazil: Tupi<br />

Iracema<br />

Tupi-1<br />

Tupi Sul<br />

World class oil discovery<br />

20 km<br />

• <strong>BG</strong> equity 25%; area 1,200 sq kms<br />

• Gross HIIP now 12-30+ billion boe<br />

• Tupi & Iracema likely one structure<br />

• Multiple stacked reservoirs<br />

• Well rates 10-20,000+ boepd<br />

• Oil 28 o API<br />

• GOR 1100-1200 scf/stb<br />

• Re-entry & EWT Tupi Sul 2008/9<br />

• Further appraisal wells 2009<br />

57

Portfolio for growth<br />

Brazil: Tupi schematic section<br />

NW<br />

Sag<br />

Upper Rift<br />

Upper Rift<br />

Lower Rift<br />

Basement<br />

Tupi Sul established three reservoirs<br />

Tupi-1 Tupi Sul<br />

3 km<br />

SE<br />

58

Portfolio for growth<br />

Brazil: Tupi notional development sequence<br />

FPSO<br />

spread<br />

Flexible, phased approach to development<br />

EWT to assess long term deliverability & producibility<br />

e.g. 1 or 2 wells initially, then further use for appraisal<br />

Gross production up to 20,000 bopd; Date 2009+<br />

Production pilot to assess water & gas injection performance<br />

e.g. 3 Producers, 1 gas injector & 1 water injector<br />

Gross production 50-100,000 bopd and gas utilisation; Date 2011+<br />

Initial development module utilising large scale FPSO<br />

e.g. 10+ wells & gas export infrastructure<br />

Gross production 100-200,000 bopd and 100-200 mmscfd of gas; Date 2013+<br />

Full field development using multiple FPSO’s 5-10 modules<br />

e.g. 10+ wells per FPSO & gas export infrastructure<br />

Gross production 500-1,000,000 bopd and 500-1,000 mmscfd of gas; Date 2015+<br />

59

Portfolio for growth<br />

Brazil: 2008 drilling and key prospects<br />

BM-S- 13<br />

<strong>BG</strong> 60%<br />

BM-S- 52<br />

<strong>BG</strong> 40%<br />

Corcovado (1), (2)<br />

BM-S- 47<br />

<strong>BG</strong> 50%<br />

Saleta (1)<br />

(1) Planned 2008 drilling<br />

(2) Key prospects<br />

BM-S- 50<br />

<strong>BG</strong> 20%<br />

BM-S- 10<br />

<strong>BG</strong> 25%<br />

Parati<br />

Carioca<br />

Good prospect inventory with two very significant prospects<br />

Tupi<br />

Tupi<br />

BM-S- 11<br />

<strong>BG</strong> 25%<br />

Iara (1)<br />

BM-S- 9<br />

<strong>BG</strong> 30%<br />

“Iguaçu Complex” (2)<br />

Guará (1)<br />

60<br />

60

Portfolio for growth<br />

E&P: E&A progress<br />

• Completed 20 wells, 12 successes<br />

• Key successes<br />

Building future growth<br />

Drilling 2007 Seismic 2007<br />

– Tupi Sul and Carioca (Brazil)<br />

– Jasmine Northern Terrace (UK)<br />

– Bongkot South (Thailand)<br />

– Margarita/Huacaya (Bolivia)<br />

New Licences 2007<br />

• Over 4,600 sq km gross acreage<br />

acquired<br />

– UK, T&T, India, Norway & Canada<br />

Canada<br />

T&T<br />

Brazil<br />

Algeria<br />

• 3D: 10,500 sq kms<br />

• 2D: 14,500 line kms<br />

UK<br />

Norway<br />

Libya<br />

Nigeria<br />

New seismic<br />

Oman<br />

China<br />

61

Portfolio for growth<br />

E&P: 2008 E&A preview<br />

Alaska<br />

1 well<br />

1 well<br />

T&T<br />

4 wells<br />

1 well<br />

Canada<br />

3 wells<br />

Brazil<br />

3-4 wells<br />

Tunisia<br />

1 well<br />

1 well<br />

Tunisia Algeria<br />

Tunisia 2-3 wells<br />

3 wells<br />

UK<br />

4 wells<br />

1 well<br />

Nigeria<br />

1 well<br />

Norway<br />

3 wells<br />

1 well<br />

Libya<br />

1-2 wells<br />

Oman<br />

6-8 wells<br />

Egypt<br />

1-2 wells<br />

Over 40 E&A wells planned to complete in 2008<br />

India<br />

0-1 well<br />

Summary of wells<br />

New plays<br />

Play extenders<br />

Appraisal/Near term<br />

production<br />

Thailand<br />

3 wells<br />

4-6<br />

17-19<br />

20-23<br />

62

Portfolio for growth<br />

E&P: Prospect inventory<br />

Other<br />

Egypt<br />

Nigeria<br />

Total risked exploration resources: 3,356 mmboe<br />

UK<br />

Norway<br />

China<br />

Brazil<br />

Deepwater<br />

Offshore Conventional<br />

Onshore<br />

Well balanced inventory, around 75% of resources are operated<br />

63

Portfolio for growth<br />

E&P: Reserves and resources<br />

10000<br />

mmboe<br />

8000<br />

6000<br />

4000<br />

2000<br />

0<br />

7,071<br />

2,440<br />

1,211<br />

1,236<br />

2,184<br />

2005 2006 2007<br />

SEC Proved Reserves Probable Reserves Un-booked Resources Risked Exploration<br />

Reserves/Resources as at year end<br />

*Based on 2007 production of 220.3 mmboe and cumulative reserves/resources<br />

Added over 2 bn boe in 2007<br />

CAGR 19%<br />

8,017<br />

2,713<br />

1,772<br />

1,383<br />

2,149<br />

10,046<br />

3,356<br />

3,122<br />

1,529<br />

2,039<br />

Reserves/<br />

Production*<br />

46 Years<br />

30 Years<br />

16 Years<br />

9.3 Years<br />

64

Portfolio Portfolio for growth growth<br />

E&P: Reserves Sustainable and production resourcesgrowth<br />

2000<br />

1500<br />

1000<br />

500<br />

0<br />

2005 2005A 2020<br />

Within the period growth is non-linear<br />

At 2008 reference conditions (see appendix)<br />

Total Strong resource sustainable base production supports 8% outlook growth<br />

1.6 million boepd<br />

CAGR 8%<br />

10,046<br />

mmboe<br />

3,356<br />

1.2 million boepd<br />

CAGR 6% 3,122<br />

1,529<br />

2,039<br />

SEC Proved Reserves<br />

Probable Reserves<br />

Un-booked Resources<br />

Risked Exploration<br />

65

<strong>BG</strong> <strong>Group</strong><br />

Conclusions

<strong>The</strong> <strong>Integrated</strong> <strong>Gas</strong> <strong>Major</strong><br />

Key messages<br />

• Good 2007 results<br />

• LNG flexibility delivering value<br />

• Earnings outlook to 2009 confirmed<br />

• Total E&P resources now 10 bn boe, up 2 bn boe<br />

• E&P production potential 6-8% CAGR 2005 to 2020<br />

Delivering value to shareholders<br />

67

<strong>BG</strong> <strong>Group</strong><br />

Appendix

Appendix<br />

Key assumptions<br />

REFERENCE CONDITIONS<br />

• Brent Oil price US $55/bbl<br />

• US Henry Hub $7.25/mmBtu<br />

• US/UK exchange rates of $2:£1<br />

• Prepared under International Financial Reporting Standards<br />

• All production includes fuel gas<br />

PRINCIPAL RISKS<br />

• <strong>Major</strong> recession or significant political upheaval in the major markets in which we operate<br />

• Failure to ensure the safe operation of our assets world-wide<br />

• Implementation risk, being the challenges associated with delivering capital intensive projects on time and on<br />

budget, including the need to retain and motivate staff<br />

• Commodity risk, being the risk of significant fluctuation in oil and/or gas prices from those assumed<br />

• Foreign exchange risk, in particular the US$:UK£ exchange rate being significantly different to that assumed<br />

• Technical, commercial, economic, regulatory and country risk<br />

For a detailed discussion of these and other risk factors, please refer to the Risk Factors included in <strong>BG</strong> <strong>Group</strong>’s Annual<br />

Report and Accounts 2006.<br />

Actual performance could differ materially from that shown. Accordingly, no assurances can be given that such<br />

performance will be achieved.<br />

69

Appendix<br />

Glossary<br />

∆ Increase or (decrease)<br />

$ United States dollar<br />

£ UK pounds sterling<br />

£m Million UK pounds sterling<br />

‘000 Thousand<br />

2D Two dimensional seismic<br />

3D Three dimensional seismic<br />

API American Petroleum Institute<br />

bcma Billion cubic metres per annum<br />

billion or bn One thousand million<br />

boe Barrels of oil equivalent<br />

boepd Barrels of oil equivalent per day<br />

bopd Barrels of oil per day<br />

ca circa<br />

CAGR Compound Annual Growth Rate<br />

Capex Capital expenditure<br />

CATS Central Area Transmission System<br />

CPP Central Processing Platform<br />

E&A Exploration and Appraisal<br />

E&P Exploration and Production<br />

EBITDA Earnings Before Interest, Tax, Depreciation, Amortisation<br />

ECMA East Coast Marine Area<br />

EPS Earnings per share<br />

EPSA Exploration & Production Sharing Agreement<br />

EWT Extended Well Test<br />

F&D Finding and Development costs<br />

FEED Front End Engineering and Design<br />

FPSA Final Production Sharing Agreement<br />

FPSO Floating Production Storage and Offloading<br />

FX Foreign Exchange<br />

GAAP Generally Accepted Accounting Principles<br />

GIIP <strong>Gas</strong> Initially In Place<br />

GOR <strong>Gas</strong> Oil Ratio<br />

GSA <strong>Gas</strong> Sales Agreement<br />

HIIP Hydrocarbons initially in place<br />

HPHT High pressure high temperature<br />

IFRIC International Financial Reporting Interpretation<br />

Committee<br />

IFRS International Financial Reporting Standards<br />

km Kilometres<br />

LNG Liquefied Natural <strong>Gas</strong><br />

LPG Liquid Petroleum <strong>Gas</strong><br />

m Metres<br />

mmboe Million barrels of oil equivalent<br />

mmbtu Million British thermal units<br />

mmcmd Million cubic metres per day<br />

mscfd Thousand standard cubic feet per day<br />

mmscfd Million standard cubic feet per day<br />

mtpa Million tonnes per annum<br />

NCMA North Coast Marine Area<br />

Opex Operating costs<br />

pa Per annum<br />

PSC Production Sharing Contract<br />

scf/stb Standard cubic feet per stock tank barrel<br />

SEC US Securities and Exchange Commission<br />

sq km Square kilometres<br />

T&D Transmission and Distribution<br />

T&T Trinidad & Tobago<br />

tbtu Trillion British thermal units<br />

tcf Trillion cubic feet<br />

tpa Tonnes per annum<br />

WDDM West Delta Deep Marine<br />

WHP Well Head Platform<br />

YOY Year on Year<br />

70