download - BG Group

download - BG Group

download - BG Group

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Data Book<br />

2009<br />

A global portfolio

Our vision<br />

Natural gas is our business.<br />

We are a rapidly growing company, with<br />

expertise throughout the gas chain.<br />

We are a leading natural gas company in the<br />

global energy market – operating responsibly<br />

and delivering value to our shareholders.<br />

We do this by connecting competitively priced<br />

resources to high-value markets.<br />

Cover image<br />

E&P reserves and resources (mmboe)<br />

15 000<br />

12 000<br />

9 000<br />

6 000<br />

3 000<br />

0<br />

8 017<br />

2006<br />

Probable reserves (a)<br />

SEC proved reserves (a)<br />

Risked exploration (a)<br />

Un-booked resources (a)<br />

Total operating profit (b)(c)<br />

(£m)<br />

6 000<br />

5 000<br />

4 000<br />

3 000<br />

2 000<br />

1 000<br />

0<br />

330<br />

E&P<br />

688<br />

10 046<br />

2007<br />

CAGR 36% 1999-2008<br />

833<br />

888<br />

1 287<br />

1 520<br />

2 389<br />

3 103<br />

13 126<br />

2008<br />

99 00 01 02 03 04 05 06 07 08<br />

T&D, LNG, Power and Other<br />

For more information visit<br />

www.bg-group.com/investors<br />

3 248<br />

5 355<br />

Oil and gas production 2008<br />

E&P production volumes<br />

(kboed)<br />

700<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

240<br />

280<br />

CAGR 11% 1999-2008<br />

298<br />

373<br />

428<br />

457<br />

504<br />

Total oil and<br />

gas production %<br />

UK 27<br />

Egypt 25<br />

Kazakhstan 18<br />

Trinidad and Tobago 11<br />

India 7<br />

Tunisia 5<br />

Thailand 4<br />

Bolivia 3<br />

Canada

Contents<br />

Europe and Central Asia<br />

Africa, Middle East and Asia<br />

Americas and Global LNG<br />

Australia<br />

Statistical supplement<br />

UK Upstream 4<br />

UK Downstream 7<br />

Kazakhstan 8<br />

Norway 10<br />

Italy 11<br />

Egypt 12<br />

Tunisia 15<br />

India 16<br />

Thailand 18<br />

Nigeria 19<br />

Oman 20<br />

Algeria 21<br />

Libya 21<br />

Trinidad and Tobago 25<br />

United States of America<br />

and Global LNG 28<br />

Brazil 30<br />

Bolivia 33<br />

Australia 36<br />

Introduction and legal notices 39<br />

Social and environment data 40<br />

<strong>Group</strong> financial data 42<br />

Exploration and Production (E&P) 45<br />

Liquefied Natural Gas (LNG) 51<br />

Transmission and Distribution (T&D) 53<br />

Power Generation (Power) 53<br />

Corporate information 54<br />

Definitions 56<br />

China 22<br />

Singapore 22<br />

Philippines 23<br />

Malaysia 23<br />

Areas of Palestinian<br />

Authority and Israel 24<br />

Madagascar 24<br />

Chile 34<br />

Uruguay 34<br />

Argentina 34<br />

Canada 35<br />

Alaska 35<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

1

2<br />

<strong>Group</strong> at a glance<br />

Our business<br />

<strong>BG</strong> <strong>Group</strong> is engaged in the exploration,<br />

development, production, transmission,<br />

distribution and supply of natural gas and<br />

oil. The <strong>Group</strong> also has a number of power<br />

generation interests.<br />

<strong>BG</strong> <strong>Group</strong>’s operations are organised on a<br />

regional basis and <strong>BG</strong> Advance supports the<br />

regions in achieving technical excellence and<br />

building long-term competitive advantage.<br />

www.bg-group.com<br />

Exploration and Production (E&P)<br />

<strong>BG</strong> <strong>Group</strong> explores for, develops, produces<br />

and markets gas and oil around the world.<br />

The <strong>Group</strong> uses its technical, commercial<br />

and gas chain skills to deliver projects at<br />

competitive cost and to maximise the<br />

sales value of its hydrocarbons.<br />

Liquefied Natural Gas (LNG)<br />

<strong>BG</strong> <strong>Group</strong>’s LNG activities combine<br />

liquefaction and regasification facilities<br />

with the purchasing, shipping,<br />

marketing and sale of LNG.<br />

Transmission and Distribution (T&D)<br />

<strong>BG</strong> <strong>Group</strong>’s T&D activities are focused<br />

in fast-growing markets, developing<br />

both markets and infrastructure for<br />

the delivery of gas.<br />

Power Generation (Power)<br />

<strong>BG</strong> <strong>Group</strong> develops, owns and operates<br />

gas-fired power generation plants.<br />

Total operating profit<br />

£3 512m 2008<br />

£2 387m 2007<br />

Total operating profit<br />

£1 585m 2008<br />

£521m 2007<br />

Total operating profit<br />

£160m 2008<br />

£247m 2007<br />

Total operating profit<br />

£118m 2008<br />

£130m 2007<br />

Alaska<br />

Business Performance – see page 39 for a description.<br />

Total operating profit includes <strong>BG</strong> <strong>Group</strong>’s share of pre-tax results from joint ventures and associates.<br />

Canada<br />

USA<br />

Bolivia<br />

Chile<br />

Americas and Global LNG<br />

Trinidad and<br />

Tobago<br />

Uruguay<br />

Key activities<br />

• Gas producer in Trinidad and Tobago, supplying both<br />

the domestic market and exporting gas as LNG<br />

• Appraising major oil discoveries and continuing<br />

exploration activity in Brazil<br />

• Interests in shale gas in Louisiana and Texas and in<br />

complementary gas-gathering and transportation assets<br />

• Exploration assets in Alaska and Canada<br />

• Regasification capacity in the USA and Chile<br />

• Major global LNG marketer<br />

• Control of Comgás, Brazil’s largest gas distribution company<br />

<strong>BG</strong> Advance<br />

Argentina<br />

Key activities<br />

• <strong>Group</strong> Technical functions: Exploration, Petroleum Engineering<br />

and Developments, Engineering Projects, Operations and<br />

Well Engineering, Commercial and Assurance, Strategy<br />

and Portfolio Development, IT and Technology<br />

• Promoting health, safety, security and environment (HSSE),<br />

and asset integrity across the <strong>Group</strong><br />

• Coordination and development of <strong>BG</strong> <strong>Group</strong> strategy<br />

• Longer-term planning and development of technical<br />

and commercial capabilities<br />

• Managing the <strong>Group</strong>’s technical assurance processes<br />

• Optimising deployment of people across the <strong>Group</strong><br />

Brazil

Norway<br />

UK<br />

Italy<br />

Algeria Libya<br />

Tunisia<br />

Egypt<br />

Nigeria<br />

Areas of PA<br />

Oman<br />

Kazakhstan<br />

Madagascar<br />

India<br />

Key activities<br />

• Interests in more than 15 UK Continental Shelf fields<br />

• Joint operator of the super-giant Karachaganak oil<br />

and gas condensate field in Kazakhstan<br />

• Exploration portfolio in Norway of 20 licences; 15 as operator<br />

• Power generation interests in the UK and Italy<br />

• Dragon LNG terminal in the UK and developing regasification<br />

terminal in Italy<br />

• Gas marketing and pipeline capacity in the UK<br />

Key activities<br />

• Queensland Gas Company Limited, a leading<br />

coal seam gas company<br />

• Total reserves and resources of more than 13 tcf<br />

• Developing two-train 7.4 mtpa LNG project on Curtis Island,<br />

near Gladstone<br />

• Gas supplier to the domestic market<br />

• Power generation fuelled by coal seam gas<br />

China<br />

Thailand<br />

Malaysia<br />

Philippines<br />

Australia<br />

Europe and Central Asia Africa, Middle East and Asia<br />

Australia<br />

† Exclusive right to supply only.<br />

Singapore †<br />

Key activities<br />

• Major gas supplier to the Egyptian and Tunisian markets<br />

• Exporting gas as LNG from Egypt<br />

• Gas production in India and Thailand<br />

• Exploration acreage and/or discovered reserves located in<br />

Algeria, Areas of Palestinian Authority, China, Egypt, Libya,<br />

Madagascar, Nigeria, Oman, Thailand and Tunisia<br />

• Interests in two Indian gas distribution companies<br />

• Power generation activities in Malaysia and the Philippines<br />

Key<br />

Exploration<br />

and Production<br />

Liquefied<br />

Natural Gas<br />

Transmission<br />

and Distribution<br />

Power<br />

Generation<br />

Europe and<br />

Central Asia<br />

Americas and<br />

Global LNG<br />

Africa, Middle<br />

East and Asia<br />

Australia<br />

3<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009

4<br />

Europe and Central Asia<br />

UK Upstream<br />

<strong>BG</strong> <strong>Group</strong> has one of the most significant exploration and<br />

production businesses in the offshore waters of the UK.<br />

<strong>BG</strong> <strong>Group</strong>’s interests are focused on the central North Sea<br />

and the <strong>Group</strong> employs a hub strategy to most effectively<br />

maximise value from its UK portfolio.<br />

Areas of operation<br />

FLOTTA<br />

Atlantic<br />

Blake<br />

Cromarty<br />

Buzzard<br />

www.bg-group.com<br />

ST. FERGUS<br />

ABERDEEN<br />

Key to operations<br />

Gas<br />

<strong>BG</strong> <strong>Group</strong>-<br />

Oil<br />

operated<br />

block<br />

Gas pipeline <strong>BG</strong> <strong>Group</strong><br />

Oil pipeline non-operated<br />

block<br />

0 100km<br />

IRISH SEA<br />

FLOTTA<br />

NORTH SEA<br />

TEESSIDE<br />

ST. FERGUS<br />

ABERDEEN<br />

UK<br />

READING<br />

New information<br />

LONDON<br />

FLAGS<br />

BACTON<br />

• Asset exchange with BP, which<br />

concentrates operations in the<br />

central North Sea<br />

Key dates<br />

WAGES<br />

FRIGG<br />

SAGE<br />

BRITANNIA<br />

FORTIES<br />

FULMAR<br />

NORTH SEA<br />

1993 Everest and Lomond onstream<br />

1997 Armada and J-Block first production<br />

Glenelg<br />

Franklin<br />

Jasmine<br />

Judy/Joanne<br />

LANGELED<br />

CATS<br />

SEAL<br />

Maria<br />

Armada<br />

Seymour<br />

Everest<br />

NORPIPE<br />

Lomond<br />

Elgin<br />

Erskine<br />

Jackdaw<br />

Jade<br />

2001 Blake and Elgin/Franklin<br />

first production<br />

2002 Jade first production<br />

2003 Seymour first gas<br />

2006 Atlantic/Cromarty first gas<br />

2007 Buzzard, West Franklin and<br />

Maria first production<br />

UK: <strong>BG</strong> <strong>Group</strong> 3 year production<br />

Total production mmboe (net)<br />

80<br />

60<br />

40<br />

20<br />

0<br />

Oil & liquids<br />

Gas<br />

55.6<br />

2006<br />

59.2<br />

2007<br />

<strong>BG</strong> <strong>Group</strong> believes there is significant<br />

remaining potential in the UK Continental<br />

Shelf (UKCS). The <strong>Group</strong> is actively pursuing<br />

opportunities around its infrastructure<br />

hubs by identifying nearby exploration<br />

prospectivity and third-party business.<br />

In December 2008, <strong>BG</strong> <strong>Group</strong> announced<br />

an asset exchange with BP which completed<br />

on 31 August 2009. <strong>BG</strong> <strong>Group</strong> acquired BP’s<br />

equity in the Everest, Lomond and Armada<br />

fields and part of BP’s equity in the Erskine<br />

field, all located in the UK central North Sea.<br />

In return, <strong>BG</strong> <strong>Group</strong> transferred its equity<br />

interests and operatorship in fields in the<br />

southern North Sea to BP. This transaction<br />

concentrates <strong>BG</strong> <strong>Group</strong>’s position in the<br />

central North Sea and gives the <strong>Group</strong><br />

control of key infrastructure hubs.<br />

As part of the transaction, <strong>BG</strong> <strong>Group</strong> took<br />

over operatorship of Everest and Lomond.<br />

<strong>BG</strong> <strong>Group</strong> also operates the Armada<br />

(Fleming, Drake and Hawkins), Maria and<br />

Seymour fields in the central North Sea;<br />

and the Blake and Atlantic fields in the<br />

Outer Moray Firth. In addition, <strong>BG</strong> <strong>Group</strong><br />

retains significant non-operated holdings<br />

in the J-Block and Elgin/Franklin areas in<br />

the central North Sea, and the Buzzard<br />

field in the Outer Moray Firth. These are<br />

operated by ConocoPhillips, Total and<br />

Nexen respectively.<br />

60.8<br />

2008<br />

In addition to the core production hubs and<br />

exploration and appraisal interests on the<br />

UKCS, <strong>BG</strong> <strong>Group</strong> has a 51.18% interest in the<br />

Central Area Transmission System (CATS)<br />

offshore pipeline and onshore processing<br />

facilities, a 7.86% stake in the Shearwater<br />

Elgin Area Line (SEAL), and a 15.98% interest in<br />

the SEAL Interconnector Link (SILK) pipeline.

OPERATED ASSETS<br />

Armada Hub Area<br />

The <strong>BG</strong> <strong>Group</strong>-operated Armada gas<br />

condensate fields (Fleming, Drake and<br />

Hawkins) extend over 31 square kilometres<br />

and span five exploration blocks. Production<br />

began in 1997. Following the asset swap with<br />

BP, <strong>BG</strong> <strong>Group</strong> now owns 76.42% in Armada.<br />

The SW Seymour area of the <strong>BG</strong> <strong>Group</strong>operated<br />

Seymour field (<strong>BG</strong> <strong>Group</strong> 57%) was<br />

appraised successfully and drilled from the<br />

Armada platform, with first production in<br />

2003. A second well in the NW Seymour area<br />

was brought into production in 2006. Plans<br />

for further development are under review.<br />

In 2003, <strong>BG</strong> <strong>Group</strong> assumed operatorship,<br />

on behalf of a consortium with Total and<br />

Centrica, of the fallow Maria 16/29a-11Y<br />

discovery. Appraisal drilling identified and<br />

confirmed the viability of the discovery.<br />

Sidetrack drilling then confirmed an<br />

extension into the adjacent Maria Horst<br />

prospect. Maria (<strong>BG</strong> <strong>Group</strong> 36%) was<br />

developed via two sub-sea wells and<br />

tied back to the Armada platform, with<br />

production beginning in December 2007.<br />

The commingled stream of Armada,<br />

Seymour and Maria gas is exported via<br />

the CATS pipeline to Teesside. Liquids are<br />

transported through the Forties Pipeline<br />

System (Forties) to the Kinneil processing<br />

plant at Grangemouth. In 2008, a combined<br />

peak rate of 227 mmscfd and 17 544 bopd<br />

was achieved.<br />

The Rev field, a third-party two-well sub-sea<br />

development in the Norwegian sector of the<br />

North Sea, has been tied back to the Armada<br />

platform. Production began in January 2009.<br />

<strong>BG</strong> <strong>Group</strong> receives a tariff payment for<br />

processing this production.<br />

Everest and Lomond<br />

On 31 August 2009, <strong>BG</strong> <strong>Group</strong> took over<br />

operatorship of the Everest field, and<br />

increased its interest to 80.46%. Everest<br />

is situated in the central North Sea and<br />

first production began in 1993. An average<br />

production rate of 91 mmscfd and 2 783 bopd<br />

was achieved in 2008. Gas is exported via the<br />

CATS pipeline. Produced liquids go via Forties<br />

to Kinneil.<br />

On 31 August 2009, <strong>BG</strong> <strong>Group</strong> took over<br />

operatorship of the Lomond field, and<br />

increased its equity stake to 83.33%. Lomond<br />

is situated in the central North Sea and<br />

first production began in 1993. An average<br />

production rate of 92 mmscfd and 1 702 bopd<br />

was achieved in 2008. In addition, production<br />

from the Erskine field is processed on the<br />

Lomond facility. Gas is exported via the<br />

CATS pipeline. Produced liquids go via<br />

Forties to Kinneil.<br />

Everest and Lomond were developed in<br />

parallel. From October 2008, <strong>BG</strong> <strong>Group</strong>’s<br />

equity gas from the two fields has been<br />

sold uncontracted into the UK market.<br />

Atlantic/Cromarty<br />

<strong>BG</strong> <strong>Group</strong> has a 75% interest in the Atlantic<br />

field in the Outer Moray Firth, and 10% in<br />

the adjacent Cromarty field. The fields have<br />

been developed with three wells and a long<br />

sub-sea multi-phase flow pipeline, the<br />

Western Area Gas Evacuation System<br />

(WAGES), tied into the Scottish Area Gas<br />

Evacuation (SAGE) terminal at St Fergus.<br />

Production began in 2006. As expected,<br />

wells have been on intermittent production<br />

in 2009 and plans for end-of-life operations<br />

are in progress.<br />

Blake<br />

<strong>BG</strong> <strong>Group</strong> has a 44% interest in, and is<br />

operator of, the Blake field, which is located<br />

100 kilometres from Aberdeen in the Outer<br />

Moray Firth. Production started in 2001.<br />

The field was developed in two phases. The<br />

first phase was the Blake Channel, which<br />

is a sub-sea development of six producing<br />

wells and two water-injection wells, tied<br />

back to an existing floating production,<br />

storage and off-loading (FPSO) vessel located<br />

over the Ross field some 9.5 kilometres away.<br />

Development of the second phase, Blake<br />

Flank, was completed and production<br />

commenced from two wells in 2003.<br />

This sub-sea development is tied back<br />

through the existing Blake facilities to<br />

the Ross FPSO vessel. An average total field<br />

rate of 16 225 bopd was achieved in 2008.<br />

Jackdaw<br />

In 2008, exploration and appraisal work<br />

continued on the Jackdaw discovery in<br />

the central North Sea. Jackdaw (<strong>BG</strong> <strong>Group</strong>operated)<br />

straddles Blocks 30/2a (pre-tertiary,<br />

<strong>BG</strong> <strong>Group</strong> 44.1%) and 30/2c (<strong>BG</strong> <strong>Group</strong> 35%).<br />

Results from the exploration and appraisal<br />

programme wells are being utilised to<br />

evaluate potential development concepts.<br />

Partners Armada (%)<br />

<strong>BG</strong> <strong>Group</strong> (operator) 76.42<br />

Total 12.53<br />

Centrica 11.05<br />

Partners Everest (%)<br />

<strong>BG</strong> <strong>Group</strong> (operator) 80.46<br />

Hess 18.67<br />

Total 0.87<br />

Partners Lomond (%)<br />

<strong>BG</strong> <strong>Group</strong> (operator) 83.33<br />

Hess 16.67<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

5<br />

EUROPE AND CENTRAL ASIA

6 Europe and Central Asia<br />

UK Upstream continued<br />

Partners Erskine (%)<br />

<strong>BG</strong> <strong>Group</strong> 32.00<br />

Chevron (operator) 50.00<br />

BP 18.00<br />

Partners Buzzard (%)<br />

<strong>BG</strong> <strong>Group</strong> 21.73<br />

Nexen (operator) 43.21<br />

PetroCanada 29.89<br />

Edinburgh Oil and Gas Limited 5.16<br />

Figures rounded to 2 decimal places.<br />

NON-OPERATED ASSETS<br />

Elgin/Franklin area<br />

The Elgin/Franklin high-pressure/<br />

high-temperature (HPHT) gas condensate<br />

fields are located in the central North Sea.<br />

The fields began production in 2001. A total<br />

of 16 wells, seven from Elgin and nine from<br />

the Franklin platforms (including the two<br />

wells from the West Franklin field), produced<br />

at an average rate of 388 mmscfd and<br />

73 000 bopd during 2008. Total operates<br />

the Elgin/Franklin fields in which <strong>BG</strong> <strong>Group</strong><br />

has a 14.11% interest.<br />

A separate field, West Franklin (<strong>BG</strong> <strong>Group</strong><br />

14.11%), started production in 2007 and a<br />

further well was brought into production in<br />

2008. In 2008, the West Franklin B appraisal<br />

well identified additional potential reserves.<br />

Ultimate resources have been significantly<br />

increased and are now estimated at close<br />

to 200 mmboe with additional drilling.<br />

The HPHT Glenelg field (<strong>BG</strong> <strong>Group</strong> 14.7%), in<br />

Block 29/4d, started production in 2006. The<br />

www.bg-group.com<br />

field has been developed through a single<br />

high-departure well drilled from the Elgin<br />

wellhead platform.<br />

Elgin/Franklin, West Franklin and Glenelg<br />

gas is exported through SEAL, a common<br />

export pipeline shared with the nearby<br />

Shell-operated Shearwater field, to the<br />

onshore gas reception facilities at Bacton<br />

in Norfolk. Liquids are exported through<br />

Forties to the Kinneil processing plant<br />

at Grangemouth.<br />

J-Block and Jade Area<br />

The ConocoPhillips-operated Judy/Joanne<br />

(J-Block) (gas condensate/oil) and Jade (gas<br />

condensate) fields are located in the central<br />

North Sea. <strong>BG</strong> <strong>Group</strong> has a 30.5% interest in<br />

J-Block and 35% in Jade. Production began<br />

from J-Block in 1997 and from Jade in 2002.<br />

The Joanne field is a sub-sea development<br />

tied back to the manned Judy platform<br />

through two 5.5 kilometre pipelines. The<br />

Judy/Joanne fields currently produce from<br />

16 wells. Jade was developed using a normally<br />

unmanned wellhead platform and currently<br />

produces from seven wells. Production from<br />

Jade is exported via a sub-sea pipeline to the<br />

Judy platform where it is commingled and<br />

processed with Judy and Joanne production.<br />

The combined gas stream is then exported<br />

via the CATS pipeline to Teesside and the<br />

combined liquids stream exported via Norpipe<br />

to the Norsea oil terminal at Teesside. The<br />

2008 combined average production rate from<br />

the fields was 336 mmscfd and 26 900 bopd.<br />

In 2008, exploration and appraisal work<br />

continued on the Jasmine discovery,<br />

9 kilometres east of the Judy platform.<br />

The Jasmine discovery straddles Blocks 30/6<br />

and 30/7a (<strong>BG</strong> <strong>Group</strong> 30.5%). The Jasmine<br />

development will comprise a wellhead<br />

platform, with separate bridge-linked<br />

accommodation, tied back via a multi-phase<br />

pipeline and a new riser platform to the<br />

existing Judy production facilities. First<br />

production is anticipated in 2012.<br />

Buzzard<br />

<strong>BG</strong> <strong>Group</strong> has a 21.73% interest in the<br />

Nexen-operated Buzzard oil field, located<br />

in the Outer Moray Firth, 100 kilometres<br />

north-east of Aberdeen. The field was<br />

discovered in 2001 and came onstream<br />

in 2007.<br />

The facilities consist of a complex of three<br />

bridge-linked platforms, with oil export via<br />

Forties and gas export via the Frigg system.<br />

With total estimated ultimate resources<br />

exceeding 700 mmboe, the field is one of the<br />

largest discovered in the UKCS in more than<br />

ten years. 2008 average production was<br />

207 000 boed gross. In early 2008, <strong>BG</strong> <strong>Group</strong><br />

and partners sanctioned the Buzzard<br />

Enhancement Project, an additional<br />

processing platform to remove hydrogen<br />

sulphide and extend plateau production.<br />

This is due to be installed in 2010.<br />

Erskine<br />

Following the asset swap with BP, <strong>BG</strong> <strong>Group</strong><br />

owns a 32% interest in the Chevron-operated<br />

HPHT Erskine field. Gas and liquids produced<br />

from the field are processed on the Lomond<br />

platform, with the gas then transported via<br />

the CATS pipeline, and liquids via Forties.<br />

OFFSHORE PIPELINES<br />

CATS<br />

<strong>BG</strong> <strong>Group</strong> has a 51.18% interest in the CATS<br />

pipeline and terminal, which is operated by<br />

BP. The 404 kilometre CATS offshore pipeline<br />

became operational in 1993, and transports<br />

gas to Teesside from the Everest, Lomond,<br />

Andrew, Armada, Seymour, Judy/Joanne,<br />

Jade, Erskine, Banff, Eastern Trough Area<br />

Project (ETAP), Maria and Montrose Arbroath<br />

fields (all in the central North Sea). In January<br />

2009, CATS also started transporting gas<br />

from the Rev field, in the Norwegian sector<br />

of the North Sea. The pipeline has a peak<br />

gas capacity of around 1 700 mmscfd.<br />

Onshore, the CATS Teesside terminal includes<br />

two trains of gas processing equipment,<br />

with a total capacity of around 1 200 mmscfd.<br />

Train 1 became operational in 1997 and<br />

Train 2 was brought onstream in 1998.<br />

SEAL and SILK<br />

<strong>BG</strong> <strong>Group</strong> has a 7.86% interest in SEAL, a<br />

480 kilometre gas export pipeline to Bacton.<br />

With capacity of around 1 150 mmscfd of<br />

dry gas, it has been transporting gas from<br />

the Elgin/Franklin and Shearwater fields<br />

since 2001.<br />

<strong>BG</strong> <strong>Group</strong> also has a 15.98% interest in the<br />

900 metre SEAL Interconnector Link (SILK)<br />

pipeline that provides direct access from SEAL<br />

to the UK-Continent Interconnector pipeline.<br />

Easington Catchment Area and Amethyst<br />

As part of the asset exchange agreement<br />

with BP, <strong>BG</strong> <strong>Group</strong> has transferred its<br />

exploration and production interests in<br />

the southern North Sea to BP. These include<br />

the Easington Catchment Area fields<br />

(Apollo, Artemis, Mercury, Minerva, Neptune,<br />

Wollaston and Whittle) and the Amethyst<br />

field. <strong>BG</strong> <strong>Group</strong> also transferred its<br />

operatorship of the Apollo, Artemis, Mercury,<br />

Minerva and Neptune fields to BP.

UK Downstream<br />

<strong>BG</strong> <strong>Group</strong>’s UK Downstream activities encompass LNG<br />

importation, energy marketing and power generation.<br />

<strong>BG</strong> <strong>Group</strong> sells gas on a wholesale basis and exports gas<br />

for sale to, and purchases gas for import from, mainland<br />

Europe via the Interconnector. The <strong>Group</strong> owns interests<br />

in two gas-fired power stations.<br />

Areas of operation<br />

New information<br />

• Dragon LNG operational<br />

Key dates<br />

LARNE<br />

Premier Power<br />

BELFAST<br />

IRISH SEA<br />

Dragon LNG<br />

Seabank<br />

1997 Premier Power Limited converted<br />

from oil to natural gas<br />

2001 Seabank Phases 1 and 2 entered<br />

full operation<br />

2003 600 MW CCGT plant at Premier<br />

Power completed<br />

2007 Equity stake in Interconnector<br />

(UK) Limited sold<br />

ABERDEEN<br />

TEESSIDE<br />

UK<br />

READING<br />

CATS<br />

EASINGTON<br />

LANGELED<br />

SEAL<br />

BACTON<br />

LONDON<br />

Key to operations<br />

Gas pipeline<br />

0 200km<br />

Shareholders Dragon LNG (%)<br />

INTERCONNECTOR<br />

ZEEBRUGGE<br />

<strong>BG</strong> <strong>Group</strong> 50<br />

PETRONAS 30<br />

4Gas 20<br />

DRAGON LNG<br />

In third quarter 2009, the Dragon LNG import<br />

terminal at Milford Haven in Wales became<br />

operational, with the terminal receiving its<br />

first commissioning cargo in July 2009.<br />

Ownership of the terminal is <strong>BG</strong> <strong>Group</strong> 50%,<br />

PETRONAS 30% and 4Gas 20% and there are<br />

20-year arrangements in place governing<br />

the use of capacity rights (<strong>BG</strong> <strong>Group</strong> 50%,<br />

PETRONAS 50%), allowing <strong>BG</strong> <strong>Group</strong> and<br />

PETRONAS to each send out up to 3 bcm<br />

(106 bcf) gas per year, from around 2.2 mtpa<br />

LNG. <strong>BG</strong> <strong>Group</strong> has contracted pipeline<br />

capacity with National Grid. <strong>BG</strong> <strong>Group</strong>’s<br />

intention is to use the Dragon terminal<br />

capacity when UK prices are internationally<br />

attractive, sourcing the LNG from its global<br />

supply portfolio.<br />

ENERGY MARKETING<br />

In 2008, <strong>BG</strong> <strong>Group</strong> produced 5.2 bcm gas<br />

from the UK Continental Shelf (UKCS), the<br />

equivalent of approximately 6% of UK gas<br />

demand. The <strong>Group</strong> sells gas on a wholesale<br />

basis principally at the UK National Balancing<br />

Point under contracts with varying durations.<br />

<strong>BG</strong> <strong>Group</strong> is an active participant in the entry<br />

capacity auctions held by National Grid and<br />

in the on-the-day commodity market and<br />

other electronic trading systems that help<br />

shippers balance their supply and demand.<br />

<strong>BG</strong> <strong>Group</strong> owns both import and export<br />

capacity in the Interconnector pipeline,<br />

which it uses to ship gas to take advantage<br />

of market price differentials and for sub-lets<br />

to third parties.<br />

PREMIER POWER LIMITED<br />

<strong>BG</strong> <strong>Group</strong> purchased Premier Power in 1992<br />

and converted Ballylumford power station<br />

to gas. The power station near Larne, has a<br />

potential maximum capacity of 1 316 MW.<br />

The power station is gas-fired with dual-fuel<br />

capability and is owned and operated by<br />

Premier Power, a wholly owned subsidiary<br />

of <strong>BG</strong> <strong>Group</strong>. The 600 MW CCGT plant was<br />

commissioned in 2003. Output from Premier<br />

Power is sold into the Irish Single Electricity<br />

market, both directly and via sales to NIE<br />

Energy, and in total satisfies around 9% of<br />

the island of Ireland’s demand and represents<br />

around 12% of installed Irish capacity.<br />

SEABANK POWER LIMITED<br />

Built in two phases, Seabank is a 1 130 MW<br />

CCGT power station near Bristol. It is owned<br />

and operated by Seabank Power, a 50:50 joint<br />

venture between <strong>BG</strong> <strong>Group</strong> and Scottish<br />

and Southern Energy. Phase 1 of Seabank<br />

(750 MW) entered full commercial operation<br />

in 2000 and Phase 2 (380 MW) in 2001.<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

7<br />

EUROPE AND CENTRAL ASIA

8 Europe and Central Asia<br />

Kazakhstan<br />

<strong>BG</strong> <strong>Group</strong> has been active in Kazakhstan for over 17 years.<br />

It is joint operator of the giant Karachaganak gas<br />

condensate field, where it has a 40-year concession, and<br />

is a shareholder in the Caspian Pipeline Consortium (CPC).<br />

The CPC pipeline links reserves in western Kazakhstan<br />

to the Black Sea, providing access to world markets.<br />

Areas of operation<br />

Key to operations<br />

Gas and<br />

Oil/Condensate<br />

Gas pipeline<br />

Oil pipeline<br />

0 400km<br />

BLACK SEA<br />

New information<br />

• Upstream and downstream<br />

co-operation agreements<br />

with KazMunayGas signed<br />

• Agreement on the principle of the<br />

CPC pipeline expansion reached<br />

by CPC shareholders<br />

www.bg-group.com<br />

ASTRAKHAN<br />

BOLSHOI CHAGAN<br />

CASPIAN SEA<br />

AKTAU<br />

ORENBURG<br />

UKRAINE<br />

Atyrau Samara<br />

pipeline<br />

Karachaganakto-CPC<br />

pipeline<br />

KAZAKHSTAN<br />

RUSSIA<br />

CPC<br />

ATYRAU<br />

NOVOROSSIYSK<br />

CPC<br />

GEORGIA<br />

Key dates<br />

Karachaganak<br />

TENGIZ<br />

1996 2% stake in restructured<br />

CPC acquired<br />

1997 Karachaganak PSA signed<br />

2001 CPC fully operational<br />

2003 First liquids from new<br />

Karachaganak facilities<br />

2004 Phase II Karachaganak<br />

development completed<br />

First exports via Novorossiysk<br />

on the Black Sea<br />

2006 Oil exports commenced via<br />

the Atyrau Samara pipeline<br />

Kazakhstan: <strong>BG</strong> <strong>Group</strong> 3 year production<br />

Total production mmboe (net)<br />

40<br />

30<br />

20<br />

10<br />

0<br />

Oil & liquids<br />

Gas<br />

36.3<br />

2006<br />

39.6<br />

2007<br />

KARACHAGANAK<br />

Karachaganak, discovered in 1979, is one of<br />

the world’s largest gas and condensate fields.<br />

Located in north-west Kazakhstan, it holds<br />

estimated hydrocarbons initially in place of<br />

9 billion bbls of condensate and 48 tcf of<br />

gas, with estimated gross reserves of over<br />

2.4 billion bbls of condensate and 16 tcf<br />

of gas.<br />

Production from the Karachaganak field<br />

began in 1984. Since the signing of the Final<br />

Production Sharing Agreement (FPSA) in<br />

1997, the Karachaganak partners have made<br />

substantial investment in wells, facilities and<br />

pipelines. In addition to its size, Karachaganak<br />

presents the operators with formidable<br />

challenges due to extreme climate swings<br />

(+/- 40 degrees centigrade) and the<br />

requirement to reinject high pressure sour<br />

gas. <strong>BG</strong> <strong>Group</strong>’s share of production from<br />

Karachaganak in 2008 was a record<br />

39.8 mmboe.<br />

The FPSA envisaged a phased development<br />

programme, of which Phase I and the<br />

initial investment for Phase II have been<br />

completed. Phase II, which came onstream<br />

in 2004, involved investment to enhance<br />

the existing facilities, construct new gas<br />

and liquids processing and gas injection<br />

facilities, work-over of more than 100 wells,<br />

construct a 120 MW power station and lay<br />

a new 650 kilometre pipeline to connect<br />

the field to the CPC pipeline at Atyrau.<br />

39.8<br />

2008<br />

Until 2004, virtually all production was<br />

sold into Russia, but now most liquids are<br />

exported to the west (currently around 70%),<br />

with some condensate and all raw gas<br />

continuing to be sold into Russia. Since 2004,

condensate exports are mainly via the CPC<br />

pipeline and, since 2006, additional oil<br />

exports are routed via the Atyrau Samara<br />

pipeline leading into the Russian Transneft<br />

system, enabling sales to achieve<br />

international prices.<br />

The Phase IIM drilling programme consisted<br />

of 16 production wells, the first of which<br />

came onstream in 2004. A fourth<br />

stabilisation train project, sanctioned in<br />

2006, is due to be completed in 2010 and<br />

onstream in first quarter 2011. It includes<br />

13 wells and is expected to increase western<br />

export volumes to more than 10 mtpa and<br />

develop gross reserves of 300 mmboe.<br />

In relation to the next phase of development,<br />

<strong>BG</strong> <strong>Group</strong> and its partners have initiated<br />

discussions with KazMunayGas on<br />

alternative phasing of the original project<br />

expenditure. This is to ensure that the full<br />

capital commitment is not made at the peak<br />

of the cost cycle. The first stage will involve<br />

a new drilling programme and is expected<br />

to increase gas injection and gas sales.<br />

KAZMUNAYGAS AGREEMENTS<br />

In December 2008, <strong>BG</strong> <strong>Group</strong> announced<br />

an agreement with JSC National Company<br />

KazMunayGas (KMG) and KMG subsidiary<br />

KazMunayGas Exploration and Production<br />

to co-operate in exploring a range of<br />

upstream opportunities. The agreement<br />

sets out the principles of a joint study of<br />

the hydrocarbon reserves potential of<br />

specific areas in Kazakhstan and other<br />

countries. The companies are working in<br />

partnership to identify opportunities across<br />

a range of potential oil and gas exploration<br />

and production projects. A joint team<br />

examines specifically targeted regions<br />

and recommends prospective acreage<br />

to partners for their consideration.<br />

A second, downstream, co-operation<br />

agreement has been signed with KMG to<br />

examine ways to increase gas utilisation<br />

in Kazakhstan. Work is underway on a CNG<br />

pilot project in Almaty aimed at increasing<br />

gas usage and improving the environment<br />

by reducing vehicle emissions. Further work<br />

has commenced on gas industry regulation.<br />

CASPIAN PIPELINE CONSORTIUM<br />

The CPC was formed to build a pipeline<br />

system to transport oil from western<br />

Kazakhstan to the Black Sea near<br />

Novorossiysk in Russia. The pipeline system,<br />

which commenced operations along its<br />

full length in 2001, consists of a new-build<br />

line, new marine terminal facilities near<br />

Novorossiysk and an upgraded pipeline. The<br />

system currently has a capacity of 33 mtpa.<br />

<strong>BG</strong> <strong>Group</strong> has a 2% equity share in the<br />

pipeline but is entitled to 2.75 mtpa<br />

(55 000 bopd) of capacity (around 10% of<br />

the total) which is used to transport liquids<br />

from Karachaganak. Karachaganak, operating<br />

via the Karachaganak Petroleum Operating<br />

Company (KPO), began delivering liquids<br />

into CPC in 2004. In 2008, liquids from<br />

Karachaganak yielded 7.5 million tonnes<br />

gross (<strong>BG</strong> <strong>Group</strong> 2.5 million tonnes).<br />

In December 2008, the CPC shareholders<br />

reached agreement on the principles of<br />

the CPC pipeline expansion, to increase its<br />

throughput capacity from its current 33 mtpa<br />

to 67 mtpa. The expansion project includes<br />

the addition of 10 pump stations in Russia<br />

and Kazakhstan, six crude oil storage tanks<br />

near Novorossiysk and a third single-point<br />

mooring at the CPC Marine Terminal.<br />

The shareholders are working towards<br />

sanctioning the expansion by the end of<br />

2009. The expansion will be phased and<br />

its completion is expected to occur in 2013.<br />

Karachaganak export routes<br />

Atyrau Samara<br />

2 mtpa<br />

3.3 mtpa<br />

CPC<br />

7.6 mtpa*<br />

7 mtpa<br />

Stabilised oil<br />

Karachaganak<br />

field<br />

Un-stabilised oil<br />

Capacity 2009<br />

Planned capacity<br />

2013<br />

* Firm capacity of 6.5 mtpa plus access to additional capacity.<br />

Partners Karachaganak (%)<br />

<strong>BG</strong> <strong>Group</strong> (joint operator) 32.5<br />

Eni (joint operator) 32.5<br />

Chevron 20.0<br />

LUKoil 15.0<br />

Shareholders CPC (%)<br />

<strong>BG</strong> <strong>Group</strong> 2.00<br />

Russian government 24.00<br />

Kazakh government 19.00<br />

Chevron 15.00<br />

LUKARCO 12.50<br />

ExxonMobil 7.50<br />

Rosneft-Shell 7.50<br />

CPC Company 7.00<br />

Eni 2.00<br />

Oryx 1.75<br />

KPV 1.75<br />

Orenburg<br />

8 bcm<br />

16 bcm<br />

Orenburg<br />

4 mtpa<br />

4 mtpa<br />

Gas<br />

re-injection<br />

Small Refinery<br />

0.4 mtpa<br />

0.6 mtpa<br />

Gas<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

9<br />

EUROPE AND CENTRAL ASIA

10 Europe and Central Asia<br />

Norway<br />

<strong>BG</strong> <strong>Group</strong> entered Norway in 2004, with the award of<br />

PL297 in the North Sea. The <strong>Group</strong> now has 20 licences<br />

(15 as operator), gained predominantly through licensing<br />

rounds and located in four core areas.<br />

Areas of operation<br />

PL396<br />

PL395<br />

PL534<br />

PL393<br />

New information<br />

• Two licences in the 20th Licensing<br />

Round awarded<br />

• Bream appraisal well completed<br />

www.bg-group.com<br />

UK<br />

PL522<br />

PL392<br />

PL388<br />

PL374S<br />

PL373S<br />

PL274BS<br />

Langeled<br />

Pipeline<br />

PL467S<br />

PL423S<br />

PL391<br />

PL382<br />

PL390<br />

KRISTIANSUND<br />

NYHAMNA<br />

NORWAY<br />

HAUGESUND<br />

STAVANGER<br />

PL407<br />

PL292B<br />

PL292<br />

PL143<br />

PL297<br />

Key dates<br />

Key to operations<br />

Gas<br />

Oil<br />

Gas pipeline<br />

Pipeline – proposed<br />

or under construction<br />

Oil pipeline<br />

<strong>BG</strong> <strong>Group</strong>operated<br />

block<br />

<strong>BG</strong> <strong>Group</strong><br />

non-operated block<br />

0 500km<br />

SWEDEN<br />

2004 First licence, PL297, awarded<br />

Opened office in Stavanger<br />

2006 Eight licences in the 19th<br />

Licensing Round awarded<br />

2007 Operatorship of the Bream<br />

licence (PL407) awarded<br />

2008 Discoveries made at Pi North,<br />

Ververis and Jordbær<br />

SOUTHERN NORTH SEA<br />

(6 licences, 5 operated)<br />

This was the entry point into Norway, with<br />

<strong>BG</strong> <strong>Group</strong> applying its UK Central Graben<br />

expertise and experience across the<br />

Norwegian median line area. Many of the<br />

plays being explored in Norway are similar<br />

to those developed and matured in the UK.<br />

In 2008, a discovery of a gas and oil<br />

accumulation was declared on Pi North<br />

(PL292) (<strong>BG</strong> <strong>Group</strong> 60% and operator). Field<br />

development studies have been initiated to<br />

progress a potential development of the<br />

discovery. Given its proximity to the median<br />

line, a tie-back to existing UK infrastructure<br />

such as the Armada platform is probable.<br />

In third quarter 2009, an appraisal well was<br />

completed on the Bream oil discovery on<br />

licence PL407 (<strong>BG</strong> <strong>Group</strong> 40% and operator).<br />

In late 2009, <strong>BG</strong> <strong>Group</strong> expects to spud the<br />

high-pressure/high-temperature Mandarin<br />

prospect (<strong>BG</strong> <strong>Group</strong> 96% and operator), with<br />

completion expected in first half 2010.<br />

NORTH TAMPEN<br />

(4 licences, 3 operated)<br />

In 2008, a discovery was made on the<br />

Jordbær exploration well (PL373S)<br />

(<strong>BG</strong> <strong>Group</strong> 45% and operator). The Jordbær<br />

discovery, where gross reserves are estimated<br />

at 60-110 mmboe, is regarded as a potential<br />

play opener, with a number of similar<br />

prospects in <strong>BG</strong> <strong>Group</strong>-held licences in the<br />

vicinity. Analysis is ongoing and further<br />

drilling is planned in fourth quarter 2009.<br />

MID-NORWAY<br />

(6 licences, 5 operated)<br />

<strong>BG</strong> <strong>Group</strong> drilled its first commitment well<br />

in this area in 2007 and in 2008 completed<br />

three large operated 3D surveys. A new<br />

licence (PL522) was awarded to <strong>BG</strong> <strong>Group</strong><br />

(40% and operator) in the 20th Licensing<br />

Round. Seismic will be acquired in 2009.<br />

BARENTS SEA<br />

(4 licences, 2 operated)<br />

<strong>BG</strong> <strong>Group</strong> completed its first Barents Sea<br />

well in 2007 with the Nucula well in PL393<br />

(<strong>BG</strong> <strong>Group</strong> 20%). It was declared an oil and<br />

gas discovery. In 2008, an appraisal well<br />

found hydrocarbons. The licence remains<br />

under assessment for potential future<br />

opportunities. In July 2008, <strong>BG</strong> <strong>Group</strong><br />

completed its second exploration well in<br />

the Barents Sea, on the Ververis prospect on<br />

licence PL395 (<strong>BG</strong> <strong>Group</strong> 30%). The well was<br />

declared a discovery and post-well analysis<br />

is ongoing. A new licence (PL534) (<strong>BG</strong> <strong>Group</strong><br />

40% and operator) was awarded in the 20th<br />

Licensing Round.

Italy<br />

<strong>BG</strong> <strong>Group</strong> has been active in Italy since 1992. Current<br />

activity in Italy includes: E&P, where <strong>BG</strong> <strong>Group</strong> holds one<br />

exploration permit in the Po Valley; LNG, where <strong>BG</strong> <strong>Group</strong><br />

is developing a LNG import terminal on the south-eastern<br />

coast; and Power, where <strong>BG</strong> <strong>Group</strong> owns and operates<br />

five co-generation plants.<br />

Areas of operation<br />

TURIN<br />

RIVALTA<br />

Key dates<br />

Po Valley<br />

MILAN<br />

Key to operations<br />

Gas<br />

Oil pipeline<br />

Oil<br />

<strong>BG</strong> <strong>Group</strong><br />

Gas pipeline<br />

non-operated<br />

block<br />

0 250km<br />

ROME<br />

1998 Serene S.p.A. power stations<br />

began operation<br />

2004 EPC contract for Brindisi<br />

LNG awarded<br />

2005 Construction of Brindisi<br />

LNG began<br />

2007 Acquired remaining 66.32%<br />

equity in Serene S.p.A. power<br />

plants taking ownership to 100%.<br />

Renamed <strong>BG</strong> Italia Power S.p.A.<br />

ITALY<br />

SULMONA<br />

CASSINO<br />

NAPLES<br />

SLOVENIA<br />

TYRRHENIAN SEA<br />

ADRIATIC SEA<br />

TERMOLI<br />

MELFI<br />

CROATIA<br />

HUNGARY<br />

BOSNIA &<br />

HERZEGOVINA<br />

Brindisi LNG<br />

BRINDISI<br />

LNG<br />

<strong>BG</strong> <strong>Group</strong> is proposing the development of<br />

an 8 bcma (6 mtpa) LNG import terminal<br />

in the outer harbour of the port of Brindisi<br />

(<strong>BG</strong> <strong>Group</strong> 100%).<br />

<strong>BG</strong> <strong>Group</strong> will have the rights to 80% of the<br />

capacity in the terminal on a priority basis,<br />

while the remainder will be subject to<br />

regulated third-party access. The terminal<br />

is strategically located to receive LNG from<br />

the Mediterranean and Atlantic Basins and<br />

the Gulf States.<br />

In February 2007, the Brindisi LNG site<br />

was seized in connection with a criminal<br />

investigation by Italian authorities into<br />

allegations of improper conduct related<br />

to the authorisation process. Criminal<br />

charges have been brought against certain<br />

current and former employees of <strong>BG</strong> <strong>Group</strong>,<br />

and against <strong>BG</strong> Italia S.p.A.. Construction<br />

work has been suspended since February<br />

2007 and the site has been seized by the<br />

Italian authorities.<br />

In January 2008, <strong>BG</strong> <strong>Group</strong> filed an<br />

Environmental Impact Assessment (EIA).<br />

This followed the suspension of the original<br />

Article 8 authorisation in October 2007.<br />

Approval of the EIA and revalidation of the<br />

Article 8 authorisation is awaited.<br />

The timing of first deliveries to the Brindisi<br />

terminal is dependent on how soon access<br />

to the site can be restored, approval of the<br />

EIA and resolution of the various outstanding<br />

legal matters.<br />

POWER<br />

<strong>BG</strong> Italia Power S.p.A., a wholly owned<br />

<strong>BG</strong> <strong>Group</strong> subsidiary, owns and operates<br />

approximately 400 MW of co-generation<br />

at five locations. 100 MW power stations<br />

are located at Melfi, Termoli and Cassino,<br />

with 50 MW stations at Sulmona and Rivalta.<br />

The plants have been in operation for 11 years<br />

and are located to supply steam to Fiat Auto<br />

plants and other adjacent steam offtakers.<br />

<strong>BG</strong> Italia Power S.p.A. supplies around<br />

2 600 GWh per year of electricity to the<br />

grid operator, GRTN, and 400 000 tonnes<br />

of steam, primarily to Fiat.<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

11<br />

EUROPE AND CENTRAL ASIA

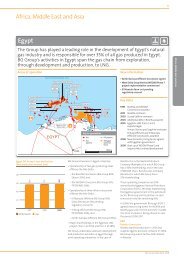

12 Africa, Middle East and Asia<br />

Egypt<br />

Egypt is a core part of <strong>BG</strong> <strong>Group</strong>’s global portfolio and a<br />

cornerstone of its Atlantic Basin LNG strategy. <strong>BG</strong> <strong>Group</strong><br />

is also one of the largest investors in Egypt’s natural gas<br />

business. <strong>BG</strong> <strong>Group</strong>’s activities in Egypt span the gas chain<br />

from exploration, through development and production,<br />

to downstream projects in LNG.<br />

Areas of operation<br />

Scarab Saffron<br />

Sapphire<br />

Saurus<br />

Sequoia<br />

Rashid -1,-2,-3<br />

ALEXANDRIA<br />

New information<br />

• Start-up of the West Delta Deep Marine<br />

(WDDM) Phase V project<br />

• Start-up of the Sequoia field unitised<br />

development project<br />

• North Gamasa Offshore Concession<br />

was awarded (and is awaiting signature)<br />

www.bg-group.com<br />

MEDITERRANEAN SEA<br />

SimSat P2<br />

Solar<br />

Serpent<br />

IDKU<br />

EGYPT<br />

North Gamasa<br />

Offshore<br />

Egyptian LNG<br />

Trains 1 & 2<br />

Rashid North<br />

CAIRO<br />

Simian Sienna<br />

SimSat P1<br />

Sienna-Up<br />

DAMIETTA LNG<br />

Key dates<br />

PORT SAID<br />

Key to operations<br />

Gas<br />

Gas<br />

pipeline<br />

El Burg Offshore<br />

El Manzala Offshore<br />

Oil pipeline<br />

<strong>BG</strong> <strong>Group</strong>operated<br />

block<br />

0 100km<br />

1995 Rosetta and WDDM<br />

Concessions awarded<br />

2001 Rosetta onstream<br />

2003 Scarab Saffron onstream<br />

2004 Additional 40% in Rosetta<br />

Concession acquired<br />

2005 Egyptian LNG Trains 1 and<br />

2 exports began<br />

Simian, Sienna and Sapphire<br />

onstream<br />

El Burg Offshore and El Manzala<br />

Offshore Concessions awarded<br />

2008 New domestic pricing terms agreed<br />

with Egyptian government<br />

Egypt: <strong>BG</strong> <strong>Group</strong> 3 year production<br />

Total production mmboe (net)<br />

80<br />

60<br />

40<br />

20<br />

0<br />

Oil & liquids<br />

Gas<br />

62.4<br />

2006<br />

56.6<br />

2007<br />

<strong>BG</strong> <strong>Group</strong>’s business in Egypt comprises:<br />

• Operatorship of two gas-producing areas<br />

offshore the Nile Delta:<br />

– the Rosetta Concession (<strong>BG</strong> <strong>Group</strong> 80%,<br />

Edison 20%); and<br />

– the WDDM Concession (<strong>BG</strong> <strong>Group</strong> 50%,<br />

PETRONAS 50%);<br />

• Operatorship of three other concessions<br />

offshore the Nile Delta:<br />

– El Manzala Offshore (<strong>BG</strong> <strong>Group</strong> 100%);<br />

– El Burg Offshore (<strong>BG</strong> <strong>Group</strong> 70%,<br />

PETRONAS 30%); and<br />

2008<br />

– North Gamasa Offshore (<strong>BG</strong> <strong>Group</strong> 100%)<br />

(concession awarded and is awaiting<br />

signature);<br />

• Major shareholdings in the Egyptian LNG<br />

project (Train 1 at 35.5% and Train 2 at 38%).<br />

<strong>BG</strong> <strong>Group</strong> undertakes upstream development<br />

and production activities in Egypt through<br />

joint operating companies. In the case of<br />

Rosetta, this is the Rashid Petroleum Company<br />

(Rashpetco) in which <strong>BG</strong> <strong>Group</strong> has a 40%<br />

shareholding, and in the case of WDDM, this<br />

is Burullus Gas Company (Burullus) in which<br />

<strong>BG</strong> <strong>Group</strong> has a 25% shareholding.<br />

These operating companies are 50% owned<br />

by the Egyptian General Petroleum<br />

Corporation (EGPC), the body representing<br />

the Egyptian government in the petroleum<br />

sector. <strong>BG</strong> <strong>Group</strong> and its partners in each<br />

concession hold the remaining 50%.<br />

57.2

UPSTREAM PRODUCTION<br />

Rosetta Concession<br />

Rosetta started production in 2001 and<br />

supplies Egypt’s domestic network. In 2004,<br />

<strong>BG</strong> <strong>Group</strong> acquired a further 40% interest<br />

in Rosetta.<br />

In first quarter 2008, <strong>BG</strong> <strong>Group</strong> delivered<br />

first gas from the Rosetta Phase III field<br />

development plan which completed in third<br />

quarter 2008. The project consists of five<br />

wells tied back to the first two phases of<br />

Rosetta. The next phase of development<br />

is that of the Sequoia field.<br />

Sequoia<br />

The unitised development (Rosetta<br />

Phase IV/WDDM Phase VI) of the Sequoia<br />

field (<strong>BG</strong> <strong>Group</strong> 62.99%) which lies across<br />

the boundary of the WDDM and Rosetta<br />

Concessions was sanctioned in second<br />

quarter 2008. It consists of six sub-sea wells:<br />

three wells on each of WDDM and Rosetta<br />

which are tied back to existing infrastructure.<br />

First gas came onstream in August 2009, with<br />

production delivered to both the domestic<br />

and export markets.<br />

WDDM Concession<br />

<strong>BG</strong> <strong>Group</strong> and partners have drilled<br />

34 successful exploration and appraisal<br />

wells in WDDM since 1997, discovering<br />

14 gas fields: Scarab, Saffron, Simian, Sienna,<br />

Sapphire, Serpent, Saurus, Sequoia, SimSat-P1<br />

and SimSat-P2. Additional development<br />

leases were granted in 2007 for the Solar,<br />

Sienna-Up, Mina and Silva discoveries.<br />

Scarab Saffron<br />

Scarab Saffron started production in 2003<br />

and supplies gas to the domestic market and<br />

Damietta LNG. <strong>BG</strong> <strong>Group</strong> currently supplies<br />

900 mmscfd under the domestic GSA.<br />

Under an agreement signed with EGAS in<br />

2004, gas has been de-dedicated for five<br />

years from the domestic GSA so that, since<br />

February 2005, some of the gas has been<br />

processed through the Damietta LNG plant<br />

for a tolling fee. In 2009, this amounts to<br />

150 mmscfd. <strong>BG</strong> <strong>Group</strong> through its wholly<br />

owned subsidiary <strong>BG</strong> Gas Marketing (<strong>BG</strong>GM)<br />

and its WDDM partner PETRONAS lift the<br />

corresponding volume (1 mtpa) of LNG.<br />

<strong>BG</strong>GM lifted its first cargo from Damietta<br />

in March 2005.<br />

Scarab Saffron was the first deep water<br />

sub-sea development in Egypt. These<br />

facilities consist of eight sub-sea wells<br />

connected to a sub-sea manifold, in turn<br />

connected by pipelines to an onshore<br />

processing terminal. Electrical and hydraulic<br />

lines connect the wells to the onshore control<br />

room. The fields are located approximately<br />

90 kilometres from the shore and in water<br />

depths of more than 700 metres.<br />

Simian, Sienna and Sapphire<br />

The Simian and Sienna fields produced first<br />

gas in 2005, for supply to Egyptian LNG<br />

Train 1 at Idku. The Sapphire field produced<br />

first gas in 2005, for supply to Egyptian LNG<br />

Train 2. The Simian, Sienna and Sapphire<br />

fields are located in WDDM approximately<br />

120 kilometres offshore Idku, near Alexandria,<br />

in the Mediterranean Sea. The facilities<br />

consist of 16 sub-sea wells tied into the<br />

existing WDDM gas gathering network and<br />

a shallow water control platform. The<br />

onshore processing facilities form part of<br />

the Idku Gas Hub where the Egyptian LNG<br />

facilities are located.<br />

WDDM Phase IV and Phase V<br />

The WDDM fields have undergone a number<br />

of development phases to maximise<br />

hydrocarbon recovery. Phase IV brought<br />

onstream seven additional wells during<br />

2008, bringing the total number of sub-sea<br />

wells in WDDM to 31.<br />

In May 2009, <strong>BG</strong> <strong>Group</strong> started incremental<br />

gas production through WDDM Phase V, a<br />

compression project in this concession. The<br />

project includes installation of two onshore<br />

gas turbine-driven compression sets, new<br />

absorption towers and associated equipment<br />

to extend plateau production from WDDM<br />

reservoirs. The project was designed to boost<br />

the pressure of processed gas into the grid,<br />

allowing field operations at lower pressures.<br />

<strong>BG</strong> <strong>Group</strong> is currently evaluating future<br />

phases of WDDM that will extend the<br />

current production plateau. The <strong>Group</strong><br />

sanctioned Phase VII in 2009.<br />

Concession Field<br />

<strong>BG</strong> <strong>Group</strong><br />

Interest (%) Supplying DCQ gross<br />

Rosetta Rosetta 80% Domestic market 345 mmscfd<br />

WDDM Scarab Saffron 50% Domestic market 750 mmscfd<br />

WDDM1 Scarab Saffron 50% Damietta LNG (Union<br />

Fenosa JV Co SEGAS)<br />

150 mmscfd<br />

WDDM Simian, Sienna, Sapphire, Sequoia 50% Egyptian LNG Train 1 565 mmscfd<br />

WDDM Simian, Sienna, Sapphire, Sequoia 50% Egyptian LNG Train 2 565 mmscfd<br />

1 <strong>BG</strong> <strong>Group</strong> and PETRONAS lift the corresponding volume of LNG.<br />

Partners (%)<br />

Rosetta Concession*<br />

Rashid Petroleum Company<br />

40<br />

WDDM Concession*<br />

Burullus Gas Company<br />

25<br />

El Burg Concession*<br />

<strong>BG</strong> <strong>Group</strong><br />

Edison<br />

EGPC<br />

PETRONAS<br />

* <strong>BG</strong> <strong>Group</strong> operator.<br />

80 20<br />

10 50<br />

50 50<br />

50 25<br />

70 30<br />

In September 2008, the Government<br />

(through EGPC) agreed new pricing terms<br />

for the gas sold into the domestic market.<br />

The price increase is being phased in over<br />

the period 2008-2011.<br />

EXPLORATION<br />

El Manzala Offshore and El Burg<br />

Offshore Concessions<br />

In 2005, <strong>BG</strong> <strong>Group</strong> signed El Burg Offshore<br />

and El Manzala Offshore concession<br />

agreements for the exploration of gas and<br />

oil with the Egyptian Natural Gas Holding<br />

Company (EGAS). Exploration drilling on<br />

El Manzala Offshore and El Burg Offshore<br />

commenced in 2008. <strong>BG</strong> <strong>Group</strong> is currently<br />

planning the forward exploration programme<br />

for these areas for 2010.<br />

North Gamasa Offshore Concession<br />

In April 2009, <strong>BG</strong> <strong>Group</strong> was awarded 100%<br />

of Block 1 (North Gamasa Offshore). The block<br />

covers an area of 281 square kilometres and<br />

is located 20 kilometres from the coast in<br />

shallow water. The initial work programme<br />

will most likely involve the acquisition of 3D<br />

seismic data.<br />

North Sidi Kerir Deep Concession<br />

<strong>BG</strong> <strong>Group</strong> notified EGAS of its intention to<br />

relinquish its interest in the North Sidi Kerir<br />

Deep Concession, effective July 2009.<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

13<br />

AFRICA, MIDDLE EAST AND ASIA

14 Africa, Middle East and Asia<br />

Egypt continued<br />

DOWNSTREAM PROJECTS<br />

Egyptian LNG<br />

<strong>BG</strong> <strong>Group</strong> and partners supply Trains 1 and 2<br />

of Egyptian LNG with gas from the Simian,<br />

Sienna and Sapphire fields in WDDM,<br />

producing a total of 7.2 mtpa of LNG.<br />

The 3.6 mtpa output from Train 1 has been<br />

sold to GDF SUEZ under a 20-year SPA. The<br />

first LNG cargo was lifted in May 2005.<br />

The 3.6 mtpa output of Train 2 has been<br />

sold to <strong>BG</strong>GM, a wholly owned <strong>BG</strong> <strong>Group</strong><br />

subsidiary, under a 20-year agreement.<br />

<strong>BG</strong>GM, may deliver this output to its capacity<br />

at Lake Charles in the USA or divert to other<br />

markets, as part of its flexible portfolio<br />

approach. The first LNG cargo was lifted<br />

in September 2005.<br />

The Egyptian LNG facilities, located at Idku,<br />

comprise the two LNG production trains<br />

and include the common facilities such<br />

as storage tanks, loading jetty and utilities.<br />

There is sufficient space at the Idku site for<br />

a further four LNG trains. The commercial<br />

structure of Egyptian LNG has been designed<br />

to allow future expansion without the need<br />

to involve all existing partners, and it is<br />

possible that third parties could supply gas<br />

to future Egyptian LNG trains.<br />

WDDM: integrated upstream and downstream<br />

TRAIN 1<br />

Start date 2005<br />

TRAIN 2<br />

Start date 2005<br />

Gas<br />

www.bg-group.com<br />

<strong>BG</strong> <strong>Group</strong> 50%<br />

Gas<br />

Egyptian LNG Company owns both the<br />

Egyptian LNG site and common facilities.<br />

Its sister company, Egyptian Operating<br />

Company for Natural Gas Liquefaction<br />

Projects (Opco) (<strong>BG</strong> <strong>Group</strong> 35.5%), undertakes<br />

the operation of all trains. El Beheira Natural<br />

Gas Liquefaction Company (Train 1 Co.)<br />

(<strong>BG</strong> <strong>Group</strong> 35.5%) owns Train 1 and the Idku<br />

Natural Gas Liquefaction Company (Train 2<br />

Co.) (<strong>BG</strong> <strong>Group</strong> 38%) owns Train 2.<br />

GAS SUPPLY LIQUEFACTION OUTPUT LNG PURCHASE<br />

565 mmscfd – WDDM<br />

565 mmscfd – WDDM<br />

<strong>BG</strong> <strong>Group</strong> 50%<br />

Train 1 – 3.6 mtpa<br />

Tolling plant<br />

<strong>BG</strong> <strong>Group</strong> 35.5%<br />

PETRONAS 35.5%<br />

EGPC 12%<br />

EGAS 12%<br />

GDF SUEZ 5%<br />

Train 2 – 3.6 mtpa<br />

Tolling plant<br />

<strong>BG</strong> <strong>Group</strong> 38%<br />

PETRONAS 38%<br />

EGPC 12%<br />

EGAS 12%<br />

GDF SUEZ 100%<br />

UPSTREAM LIQUEFACTION OUTPUT DOWNSTREAM<br />

LNG<br />

LNG<br />

<strong>BG</strong> <strong>Group</strong> 100%

Tunisia<br />

<strong>BG</strong> <strong>Group</strong> is the largest producer of gas in Tunisia. The<br />

Miskar field, through the Hannibal gas treatment plant,<br />

currently provides around 40% of Tunisian domestic gas<br />

demand. The recently completed Hasdrubal development<br />

will take <strong>BG</strong> <strong>Group</strong>'s share of local demand to over 50%.<br />

Areas of operation<br />

Key to operations<br />

Gas<br />

Oil<br />

Gas pipeline<br />

Oil pipeline<br />

New information<br />

• Hasdrubal field onstream<br />

Key dates<br />

A L G E R I A<br />

Proposed<br />

pipeline<br />

<strong>BG</strong> <strong>Group</strong>operated<br />

block<br />

0 200km<br />

Hannibal<br />

1989 Tenneco assets acquired<br />

1996 Miskar field first production<br />

2006 Hasdrubal development<br />

plan approved<br />

TUNISIA<br />

Hasdrubal Plant<br />

LPG Facility<br />

TUNIS<br />

BIZERTE<br />

LA SKHIRA<br />

GABES<br />

SFAX<br />

SOUSSE<br />

GULF OF GABES<br />

MEDITERRANEAN SEA<br />

Amilcar<br />

Miskar<br />

Hasdrubal<br />

Tunisia: <strong>BG</strong> <strong>Group</strong> 3 year production<br />

Total production mmboe (net)<br />

16<br />

12<br />

8<br />

4<br />

0<br />

Oil & liquids<br />

Gas<br />

12.4<br />

2006<br />

11.9<br />

2007<br />

11.0<br />

2008<br />

AMILCAR PERMIT<br />

<strong>BG</strong> <strong>Group</strong> is operator and joint permit holder<br />

with Entreprise Tunisienne d'Activités<br />

Pétrolières (ETAP), the Tunisian state-owned<br />

company, of the 1 016 square kilometre<br />

Amilcar exploration permit, offshore Sfax<br />

in the Gulf of Gabès. In 2006, <strong>BG</strong> <strong>Group</strong><br />

was granted a new extension to this permit,<br />

which now expires in December 2009. An<br />

application for a further extension of up<br />

to two years is underway. Granted from this<br />

permit are the Miskar concession (<strong>BG</strong> <strong>Group</strong><br />

100%) and the Hasdrubal concession<br />

(<strong>BG</strong> <strong>Group</strong> 50%, ETAP 50%).<br />

MISKAR GAS FIELD<br />

<strong>BG</strong> <strong>Group</strong> net production in 2008 from its<br />

Miskar field was 11.0 mmboe. Gas from the<br />

field is processed at the <strong>BG</strong> <strong>Group</strong>-operated<br />

Hannibal plant, 21 kilometres south of<br />

Sfax, and sold into the Tunisian gas system.<br />

<strong>BG</strong> <strong>Group</strong> has a gas sales contract with the<br />

Tunisian state electricity and gas company,<br />

Société Tunisienne de l’Electricité et du Gaz<br />

(STEG), which gives <strong>BG</strong> <strong>Group</strong> the right to<br />

supply up to 230 mmscfd from Miskar on a<br />

long-term basis. Offshore compression was<br />

commissioned in 2005 to maintain the<br />

production plateau of the field.<br />

<strong>BG</strong> <strong>Group</strong> has drilled five wells as part of<br />

the Miskar infill drilling campaign between<br />

2007 and 2009. These wells further extend<br />

the field production plateau.<br />

An upgrade of the Hannibal production<br />

facilities to process varying compositions<br />

of gas is complete. Other works include<br />

Hannibal plant and Miskar platform upgrades,<br />

resulting in an additional facilities capacity<br />

of 5%. Hydrogen sulphide will be processed into<br />

sulphuric acid, a more environmentally friendly<br />

solution. A 60 kilometre condensate pipeline<br />

was commissioned in 2007 to transport Miskar<br />

condensate from Hannibal to La Skhira port.<br />

HASDRUBAL DEVELOPMENT<br />

First gas production from Hasdrubal<br />

is expected in September 2009. Gross<br />

production from this joint project (<strong>BG</strong> <strong>Group</strong><br />

50%, ETAP 50%) is expected to average<br />

approximately 32 000 boed. Gas will be<br />

sold to STEG at rates of up to approximately<br />

100 mmscfd gross, whilst liquids and LPG<br />

amounting to a further 16 000 boed gross<br />

will be exported or sold in the local market.<br />

Production will be delivered from six wells<br />

on an offshore platform through dedicated<br />

offtake facilities. An onshore gas processing<br />

facility and LPG production facility have been<br />

established adjacent to the Hannibal plant<br />

and an LPG storage terminal has been<br />

constructed in Gabès to receive and export<br />

butane and propane.<br />

<strong>BG</strong> <strong>Group</strong> Data Book 2009<br />

15<br />

AFRICA, MIDDLE EAST AND ASIA

16 Africa, Middle East and Asia<br />

India<br />

<strong>BG</strong> <strong>Group</strong> is a key player within the gas industry in India,<br />

with a significant presence in both the E&P and T&D<br />

segments. <strong>BG</strong> <strong>Group</strong> has increased its exposure in India’s<br />

growing natural gas sector by developing its upstream<br />

position through licensing rounds and acquisitions.<br />

Areas of operation<br />

Key to operations<br />

Gas<br />

<strong>BG</strong> <strong>Group</strong>operated<br />

Oil<br />

block<br />

Gas pipeline <strong>BG</strong> <strong>Group</strong><br />

non-operated<br />

block<br />

INDIA 1<br />

KAKINADA<br />

INDIA<br />

KG-DWN-98/4<br />

KG-OSN-2004/1<br />

Key dates<br />

0 100km<br />

www.bg-group.com<br />

Mukta<br />

ARABIAN SEA<br />

BHUBANESHWAR<br />

PURI<br />

MN-DWN-2002/02<br />

ANKLESHWAR<br />

GGCL transmission pipeline<br />

Tapti<br />

GULF OF CAMBAY<br />

INDIA 2<br />

1995 Mahanagar Gas Ltd (MGL) formed<br />

1997 Majority stake in GGCL acquired<br />

2002 Enron Oil and Gas India Limited<br />

acquired and thereby a 30%<br />

participating interest in the<br />

Panna/Mukta and Tapti<br />

(PMT) fields<br />

AHMEDABAD<br />

HAZIRA<br />

Panna<br />

VADODARA<br />

1<br />

SURAT<br />

BHARUCH<br />

Gujarat Gas<br />

Tapti gas pipeline<br />

INDIA<br />

HVJ pipeline<br />

MUMBAI<br />

Mahanagar Gas<br />

INDIA<br />

2<br />

2007 PSC for Block KG-OSN-2004/1<br />

signed<br />

2008 New agreements signed with<br />

GAIL to take PMT gas production<br />

Farm-ins to Blocks KG-DWN-98/4<br />

and MN-DWN-2002/02 off the<br />

Indian east coast signed<br />

India: <strong>BG</strong> <strong>Group</strong> 3 year production<br />

Total production mmboe (net)<br />

20<br />

15<br />

10<br />

5<br />

0<br />

Oil & liquids<br />

Gas<br />

10.3<br />

2006<br />

13.7<br />

2007<br />

UPSTREAM<br />

<strong>BG</strong> <strong>Group</strong> has held a 30% interest in the<br />

mid and south Tapti gas fields and the<br />

Panna/Mukta oil and gas fields since 2002.<br />

In 2008, the combined fields produced<br />

around 15.5 mmboe (net to <strong>BG</strong> <strong>Group</strong>).<br />

Gross production from PMT fields has<br />

doubled in the past five years since <strong>BG</strong> <strong>Group</strong><br />

took over the management of technical<br />

operations. <strong>BG</strong> <strong>Group</strong>’s aim is to optimise<br />

recovery from the PMT fields through<br />

ongoing field development as well as<br />

new projects.<br />

The Panna infill programme (26 wells) was<br />

successfully completed in 2006 and has<br />

increased recovery by around 50 mmbbl<br />

and 200 bcf gas. As a part of the first<br />

phase of the approved Expanded Plan<br />

of Development (EPOD) for Panna, two<br />

wellhead platforms have been installed<br />

and development wells are being drilled.<br />

First production from EPOD was achieved<br />

in 2007. The EPOD for Panna also involved<br />

the drilling of 21 wells, which completed<br />

in third quarter 2008.<br />

15.5<br />

2008<br />

Panna K started production in August 2009<br />

and the south-west Panna installation is<br />

scheduled to be completed by end first<br />

quarter 2010. Future developments will focus<br />

on development of Panna L and the next<br />

phase of the Mukta reservoir (Mukta B).<br />

The fourth wellhead platform on the south<br />

Tapti field became functional in 2006, helping<br />

to maintain a 250 mmscfd production rate.<br />

In 2007, the next phase of development of the<br />

mid Tapti gas field was completed and first<br />