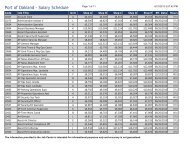

Agenda Reports - Port of Oakland

Agenda Reports - Port of Oakland

Agenda Reports - Port of Oakland

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Blair30<br />

OMAR BENJAMIN<br />

Executive Director<br />

DAVID L. ALEXANDER<br />

<strong>Port</strong> Attorney<br />

ARNEL ATIENZA<br />

<strong>Port</strong> Auditor<br />

JOHN T. BETTERTON<br />

Secretary <strong>of</strong> the Board<br />

ROLL CALL<br />

PORT OF OAKLAND<br />

BOARD OF PORT COMMISSIONERS<br />

530 Water Street <strong>Oakland</strong>, California 94607<br />

Telephone: (510) 627-1100<br />

Facsimile: (510) 451-5914<br />

TDD/TTY – Dial 711<br />

E-Mail: board@portoakland.com<br />

Website: www.port<strong>of</strong>oakland.com<br />

AGENDA<br />

Regular Meeting <strong>of</strong> the Board <strong>of</strong> <strong>Port</strong> Commissioners<br />

Thursday February 2, 2012 – 1:00 p.m.<br />

Board Room – 2 nd Floor<br />

PAMELA CALLOWAY<br />

President<br />

GILDA GONZALES<br />

First Vice-President<br />

JAMES W. HEAD<br />

Second Vice-President<br />

MARGARET GORDON<br />

Commissioner<br />

1 st Vice President Gonzales, 2 nd Vice-President Head, Commissioner Gordon,<br />

Commissioner Uno, Commissioner Yee and President Calloway<br />

1. CLOSED SESSION (will be taken out <strong>of</strong> order - at the end <strong>of</strong> the meeting)<br />

2. MAJOR PROJECTS<br />

VICTOR UNO<br />

Commissioner<br />

ALAN S. YEE<br />

Commissioner<br />

This segment <strong>of</strong> the meeting is reserved for action and discussions regarding the status<br />

<strong>of</strong> Major Projects and issues <strong>of</strong> special importance.<br />

3. BUDGET & FINANCE<br />

This segment <strong>of</strong> the meeting is reserved for action or discussion regarding the status <strong>of</strong><br />

Budget and Finance issues.<br />

4. STRATEGY & POLICY<br />

This segment <strong>of</strong> the meeting is reserved for action or discussion on Strategy and Policy<br />

Issues<br />

4.1 Overview <strong>of</strong> Maritime Division (Maritime)<br />

5. CONSENT ITEMS<br />

Action by the Board under “Consent Items” means that all matters listed below have<br />

been summarized and will be adopted by one motion and appropriate vote. Consent<br />

Items may be removed for further discussion by the Board at the request <strong>of</strong> any member<br />

<strong>of</strong> the Board.<br />

AGENDA<br />

1 <strong>of</strong> 52

6. REMAINING ACTION ITEMS<br />

Remaining Action Items are items not previously addressed in this <strong>Agenda</strong> that may<br />

require staff presentation and/or discussion and information prior to action by the Board.<br />

7. UPDATES/ANNOUNCEMENTS<br />

The President and/ or Executive Director will report on noteworthy events occurring since<br />

the last Board Meeting.<br />

8. SCHEDULING<br />

OPEN FORUM<br />

This segment <strong>of</strong> the meeting is reserved for scheduling items for future <strong>Agenda</strong>s and/or<br />

scheduling Special Meetings<br />

The Board will receive public comment on non-agenda items during this time. Please fill<br />

out a speaker card and present it to the Secretary <strong>of</strong> the Board.<br />

1. CLOSED SESSION (approximately 2:30)<br />

1.1 CONFERENCE WITH REAL PROPERTY NEGOTIATOR - As provided under California<br />

Government Code Section 54956.8:<br />

Property: Former <strong>Oakland</strong> Army Base and Adjacent Properties<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong>, Prologis and California Capital Group<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 20-26 Outer Harbor Terminal Facilities<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and <strong>Port</strong>s America Outer Harbor Terminals<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 30-33<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and TransPacific Container Service (TraPac)<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 33-37<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and Evergreen Marine Corporation (Taiwan)<br />

Ltd<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 55-56<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and Total Terminals, Inc, LLC (TTI)<br />

2<br />

AGENDA<br />

2 <strong>of</strong> 52

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths: 57-59<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and SSA Terminals, LLC (SSAT)<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 60-63<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and Eagle Marine Services (APL Terminal)<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Berths 67-68<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and SSA Terminals, LLC (SSAT) (Howard<br />

Terminal)<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

Property: Joint Intermodal Terminals<br />

Negotiating Parties: <strong>Port</strong> <strong>of</strong> <strong>Oakland</strong> and Burlington Northern Santa Fe<br />

Agency Negotiator: Director <strong>of</strong> Maritime, James Kwon<br />

Under Negotiation: Price and Terms <strong>of</strong> Payment<br />

1.2 THREAT TO PUBLIC SERVICES OR FACILITIES<br />

Consultation with: <strong>Port</strong> Security Officer<br />

CLOSED SESSION REPORT<br />

The <strong>Port</strong> Attorney or Board Secretary will report on any final actions taken in Closed<br />

Session.<br />

ADJOURNMENT<br />

The next Regular Meeting <strong>of</strong> the Board will be held on February 16, 2012 at 1:00 p.m. in<br />

the Board Room.<br />

3<br />

AGENDA<br />

3 <strong>of</strong> 52

PUBLIC PARTICIPATION<br />

Disability Related Modifications<br />

Any person who requires a disability-related modification or accommodation, including auxiliary aids or<br />

services, in order to participate in the meeting, may submit a written request, electronic request, or telephone<br />

request [via the California Relay Service (telephone) for the hearing impaired at (800) 735-2922], to the<br />

Secretary <strong>of</strong> the Board no later than five working days prior to the scheduled meeting date.<br />

John Betterton, Secretary <strong>of</strong> the Board<br />

530 Water Street, <strong>Oakland</strong>, CA 94607<br />

jbetterton@portoakland.com<br />

(510) 627-1696<br />

Language & Interpretive Services<br />

As a grantee <strong>of</strong> federal aid grant funds from the US Department <strong>of</strong> Transportation, the <strong>Port</strong> is responsible for<br />

ensuring equal access to its programs, services, and benefits. To request bilingual interpreters or materials in<br />

alternate formats, please contact the Assistant Secretary <strong>of</strong> the Board no later than five working days prior to<br />

the scheduled meeting date.<br />

Daria Edgerly, Assistant Secretary <strong>of</strong> the Board<br />

530 Water Street, <strong>Oakland</strong>, CA 94607<br />

dedgerly@portoakland.com<br />

(510) 627-1337<br />

Scented Products<br />

Please refrain from wearing scented products to this meeting so attendees who experience chemical sensitivities<br />

may attend.<br />

To Speak on an <strong>Agenda</strong> Item<br />

You may speak on any item appearing on the <strong>Agenda</strong>. Please fill out a Speaker’s Card and give it to the Board<br />

Secretary before the start <strong>of</strong> the meeting or immediately after conclusion <strong>of</strong> Closed Session. Cards received<br />

after the start <strong>of</strong> the meeting will be treated as a single request to speak in Open Forum. All speakers will be<br />

allotted a minimum <strong>of</strong> one minute.<br />

<strong>Agenda</strong> & Related Materials<br />

Should you have questions or concerns regarding this <strong>Agenda</strong>, or wish to review any <strong>of</strong> the <strong>Agenda</strong> Related<br />

Materials, please contact the Board Secretary, John Betterton, at (510) 627-1696, or visit our web page at<br />

www.port<strong>of</strong>oakland.com<br />

To receive <strong>Port</strong> <strong>Agenda</strong>s and <strong>Agenda</strong> Related Materials by email, please email your request to<br />

jbetterton@portoakland.com<br />

4<br />

AGENDA<br />

4 <strong>of</strong> 52

MAJOR PROJECTS<br />

MAJOR PROJECTS Tab 2<br />

This segment <strong>of</strong> the meeting is reserved for action and<br />

discussions regarding the status <strong>of</strong> Major Projects and<br />

issues <strong>of</strong> special importance.<br />

5 <strong>of</strong> 52

BUDGET & FINANCE<br />

BUDGET & FINANCE Tab 3<br />

This segment <strong>of</strong> the meeting is reserved for action or<br />

discussion regarding the status <strong>of</strong> Budget and Finance<br />

issues.<br />

6 <strong>of</strong> 52

STRATEGY & POLICY<br />

STRATEGY & POLICY Tab 4<br />

This segment <strong>of</strong> the meeting is reserved for action or<br />

discussion on Strategy and Policy Issues.<br />

7 <strong>of</strong> 52

Maritime Division<br />

STRATEGY & POLICY Tab 4.1<br />

1<br />

8 <strong>of</strong> 52

Today’s Presentation<br />

Division Overview<br />

Structure <strong>of</strong> Organization and Tenants<br />

Revenue and Expenses<br />

Business Overview<br />

Industry and <strong>Port</strong> Performance<br />

Market Dynamics<br />

Customer and Commodity Pr<strong>of</strong>ile<br />

Strategic Initiatives<br />

STRATEGY & POLICY Tab 4.1<br />

2<br />

9 <strong>of</strong> 52

Maritime Division Organization Chart<br />

Total FTE Count = 68<br />

December 2011<br />

Manager, Finance and<br />

Administration<br />

Jean Banker<br />

Executive Assistant<br />

Brenda James<br />

Manager, Marketing<br />

and Business<br />

Development<br />

Lawrence Dunnigan<br />

Maritime Director<br />

James Kwon<br />

Chief Wharfinger<br />

Chris Peterson<br />

STRATEGY & POLICY Tab 4.1<br />

Manager, Harbor<br />

Facilities<br />

Bill Morrison<br />

Staff <strong>of</strong> 5 FTE’s Staff <strong>of</strong> 3 FTE’s<br />

Staff <strong>of</strong> 4 wharfinger<br />

FTE's and 2 security<br />

FTE's<br />

Staff <strong>of</strong> 48 FTE’s<br />

3<br />

10 <strong>of</strong> 52

Maritime Revenue And Expenses<br />

FY 03 – FY14<br />

(in 000's)<br />

$156,000<br />

$143,000<br />

$130,000<br />

$117,000<br />

$104,000<br />

$91,000<br />

$78,000<br />

$65,000<br />

$52,000<br />

$39,000<br />

$26,000<br />

$13,000<br />

$0<br />

Source: <strong>Port</strong> data<br />

FY '03 FY '04 FY '05 FY '06 FY '07 FY '08 FY '09 FY '10 FY '11 FY '12<br />

Bdgt<br />

STRATEGY & POLICY Tab 4.1<br />

FY '13<br />

Proj.<br />

FY '14<br />

Proj.<br />

Revenue<br />

Expense<br />

4<br />

11 <strong>of</strong> 52

Berth 20-26 <strong>Port</strong>s America Terminal<br />

Berth 30-32 TraPac Terminal<br />

Berth 35-38 Ben E. Nutter Terminal<br />

Berth 55-56 Hanjin Terminal<br />

Berth 57-59 <strong>Oakland</strong> Int’l Container Terminal<br />

Berth 60-63 APL Terminal<br />

Berth 67-68 Charles P. Howard Terminal<br />

2018<br />

2024<br />

2013<br />

2016 2017<br />

STRATEGY & POLICY Tab 4.1<br />

12 <strong>of</strong> 52

U.S. Container Volume – at major U.S. container ports<br />

Note: East Coast and Gulf Coast 2011 figures are projected based on January 2011 through November 2011 volume<br />

Source: American Association <strong>of</strong> <strong>Port</strong> Authorities (AAPA)<br />

STRATEGY & POLICY Tab 4.1<br />

6<br />

13 <strong>of</strong> 52

<strong>Oakland</strong> Performance on the West Coast<br />

2005 2006 2007 2008 2009 2010 2011<br />

Source: American Association <strong>of</strong> <strong>Port</strong> Authorities (AAPA)<br />

STRATEGY & POLICY Tab 4.1<br />

14 <strong>of</strong> 52

2011 Container Volumes<br />

SEA/TAC<br />

3.5m TEU<br />

OAK<br />

2.3m TEU<br />

LA/LB<br />

14m TEU<br />

* Figures are projected based on January 2011 through November 2011 volume<br />

Source: <strong>Port</strong> authority websites<br />

HOU<br />

1.9m TEU*<br />

STRATEGY & POLICY Tab 4.1<br />

SAV<br />

2.9m TEU*<br />

CHS<br />

1.4m TEU*<br />

NY/NJ<br />

5.5m TEU*<br />

NOR<br />

1.9m TEU*<br />

8<br />

15 <strong>of</strong> 52

Approx. USWC Intermodal Volume<br />

SEA/TAC<br />

65% IPI*<br />

2.3m TEU<br />

LA/LB<br />

45% IPI*<br />

6.3m TEU<br />

* Estimated<br />

OAK<br />

20% IPI<br />

500k TEU<br />

STRATEGY & POLICY Tab 4.1<br />

9<br />

16 <strong>of</strong> 52

Megaregion Population<br />

8.4 million<br />

14 million 2025 CAGR<br />

16.4m 1.06%<br />

24.3 million<br />

5.7 million<br />

5.5 million<br />

Source: America 2050 / Regional Plan Association<br />

19.7 million<br />

55.5 million<br />

STRATEGY & POLICY Tab 4.1<br />

10<br />

17 <strong>of</strong> 52

Expected Rail Growth through 2035<br />

Source: IHS Global Insight<br />

STRATEGY & POLICY Tab 4.1<br />

18 <strong>of</strong> 52

MARITIME PROMOTIONAL VIDEO<br />

Link: http://youtu.be/y7skbc4HKs0<br />

STRATEGY & POLICY Tab 4.1<br />

19 <strong>of</strong> 52

<strong>Oakland</strong>’s Trading Partners<br />

Source: <strong>Port</strong> data<br />

STRATEGY & POLICY Tab 4.1<br />

20 <strong>of</strong> 52

<strong>Oakland</strong> Imports<br />

USWC Import Market Share<br />

2011 <strong>Port</strong> Cargo Throughput Loaded TEU<br />

Source: <strong>Port</strong> data<br />

STRATEGY & POLICY Tab 4.1<br />

<strong>Oakland</strong><br />

Seattle<br />

Tacoma<br />

Los Angeles<br />

Long Beach<br />

21 <strong>of</strong> 52

Major Imports by Value, 2010<br />

Total value <strong>of</strong> all imports—$21.3 Billion<br />

Commodity $ Millions<br />

1 Machinery 4,505<br />

2 Electrical Equipment 2,312<br />

3 Furniture and Bedding 1,158<br />

4 Beverages 1,098<br />

5 Knit Apparel 965<br />

6 Woven Apparel 873<br />

7 Vehicles 791<br />

8 Toys and Sports Equipment 671<br />

9 Plastic 595<br />

10 C<strong>of</strong>fee 506<br />

Source: Bureau <strong>of</strong> Census, U.S. Department <strong>of</strong> Commerce<br />

STRATEGY & POLICY Tab 4.1<br />

22 <strong>of</strong> 52

High Volume Importers through <strong>Oakland</strong><br />

1 Canon USA/HP (Electronics)<br />

2 Target (General Dept. Store Merchandise)<br />

3 Cost Plus (Home Furnishings)<br />

4 Gap Inc. (Apparel)<br />

5 JC Penney (General Dept. Store Merchandise)<br />

6 Crate & Barrel (Home Furnishings)<br />

7 Dynacraft (Bicycles)<br />

8 Walgreens (General Dept. Store Merchandise)<br />

9 Diablo Valley Packaging (Wine bottles)<br />

10 Southern Wine & Spirits (Beverages)<br />

Source: PIERS<br />

STRATEGY & POLICY Tab 4.1<br />

23 <strong>of</strong> 52

<strong>Oakland</strong> Exports<br />

USWC Export Market Share<br />

2011 <strong>Port</strong> Cargo Throughput Loaded TEU<br />

Source: <strong>Port</strong> data<br />

STRATEGY & POLICY Tab 4.1<br />

<strong>Oakland</strong><br />

Seattle<br />

Tacoma<br />

Los Angeles<br />

Long Beach<br />

24 <strong>of</strong> 52

Major Exports by Value, 2010<br />

Total value <strong>of</strong> all exports—$14.8 Billion<br />

Commodity $ Millions<br />

1 Edible Fruit and Nuts 1,802<br />

2 Meat 1,064<br />

3 Machinery 652<br />

4 Beverages 546<br />

5 Inorganic Chemicals/Rare Earth 521<br />

6 Vehicles 472<br />

7 Cereals 420<br />

8 Electrical Machinery 408<br />

9 Optical/Medical Instruments 363<br />

10 Misc Chemical Products 275<br />

Source: Bureau <strong>of</strong> Census, U.S. Department <strong>of</strong> Commerce<br />

STRATEGY & POLICY Tab 4.1<br />

25 <strong>of</strong> 52

High Volume Exporters through <strong>Oakland</strong><br />

1 American Chung Nam (Wastepaper)<br />

2 Globerunners (Ag products)<br />

3 E & J Gallo<br />

4 C G Roxane (Bottled water)<br />

5 Tyson Fresh Meats<br />

6 Olympic Industries (Lumber)<br />

7 ADM Rice<br />

8 Seaboard Foods (Frozen meat)<br />

9 JC Horizon (Wastepaper)<br />

10 EP Minerals (Diatomaceous earth)<br />

Source: PIERS<br />

STRATEGY & POLICY Tab 4.1<br />

26 <strong>of</strong> 52

Top Ocean Carriers Serving <strong>Oakland</strong><br />

Total 2011 volume<br />

TEU<br />

(thousands) Carrier<br />

Source: <strong>Port</strong> data<br />

% Growth over<br />

same period 2010<br />

180 APL -3%<br />

172 Evergreen -4%<br />

139 MSC 18%<br />

135 Hanjin 10%<br />

129 Yang Ming 16%<br />

101 Hapag-Lloyd 1%<br />

100 Maersk -24%<br />

95 Horizon 15%<br />

91 Matson 5%<br />

79 Mitsui 10%<br />

STRATEGY & POLICY Tab 4.1<br />

27 <strong>of</strong> 52

Major changes in carrier alliances and services<br />

Asia/Europe trade lane…<br />

9/12/2011<br />

Maersk Line (1) announces<br />

daily guaranteed service<br />

between Asia and<br />

Europe<br />

15.9% <strong>of</strong> global fleet<br />

12/1/2011<br />

MSC (2) and CMA CGM (3)<br />

announce operating<br />

partnership<br />

21.6% <strong>of</strong> global fleet<br />

(N) global ranking in terms <strong>of</strong> fleet size<br />

Note: All subsidiaries are consolidated.<br />

Source: AXS-Alphaliner, www.alphaliner.com/top100/index.php<br />

STRATEGY & POLICY Tab 4.1<br />

12/20/2011<br />

New World and Grand Alliances<br />

announce partnership<br />

APL (7) Hapag Lloyd (5)<br />

MOL (10) OOCL (11)<br />

Hyundai (18) NYK (12)<br />

12/27/2011<br />

17.3% <strong>of</strong> global fleet CKYH Alliance and Evergreen (6)<br />

announce partnership<br />

COSCO (4) K Line (16)<br />

Yang Ming (15) Hanjin (9)<br />

15.4% <strong>of</strong> global fleet<br />

21<br />

28 <strong>of</strong> 52

Strategic Initiatives<br />

• Export Promotion Program<br />

• Incentive for new intermodal rail cargo<br />

• Facilities<br />

• Rail improvements<br />

• Transloading<br />

• Shore power<br />

STRATEGY & POLICY Tab 4.1<br />

22<br />

29 <strong>of</strong> 52

Export Promotion Program<br />

Connecting U.S. Exporters to the Global Marketplace….<br />

• Commission study to target export opportunities<br />

• Engage with key trade associations and government agencies<br />

and programs to align export promotion strategies<br />

• Educational events and seminars<br />

• Regional focus events<br />

• Strategic Counsel<br />

STRATEGY & POLICY Tab 4.1<br />

23<br />

30 <strong>of</strong> 52

Uncertainty and Opportunity<br />

STRATEGY & POLICY Tab 4.1<br />

February 2, 2012<br />

Walter Kemmsies, Anne Landstrom<br />

M<strong>of</strong>fatt & Nichol<br />

31 <strong>of</strong> 52

Main Points<br />

• Global rebalancing has begun but the recovery hasn’t<br />

• Excesses such as US and Asian trade imbalances are beginning to<br />

reverse<br />

• US is no longer able to prosper without competitive exports<br />

• US share <strong>of</strong> GDP has declined from 50% in 1980 to 22% in 2011<br />

• Comparative advantage in agriculture, energy and high-end capital<br />

goods<br />

• <strong>Oakland</strong> is an export gateway to fast growing economies<br />

• Growth will depend on proper planning and execution<br />

STRATEGY & POLICY Tab 4.1<br />

32 <strong>of</strong> 52

Why The US Economy Has Been Struggling<br />

Millions <strong>of</strong> People<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

1991<br />

1992<br />

Manufacturing Employment and Goods Trade Deficit<br />

1993<br />

1994<br />

1995<br />

1996<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

• Outsourced jobs were not replaced by export-oriented industries<br />

• Income-constrained households resorted to borrowing to buy homes, cars and<br />

goods<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

Recession Manufacturing Employment Goods Trade balance (ex-Oil)<br />

STRATEGY & POLICY Tab 4.1<br />

2011<br />

$0<br />

-$10<br />

-$20<br />

-$30<br />

-$40<br />

-$50<br />

-$60<br />

Billiosn <strong>of</strong> Dollars<br />

33 <strong>of</strong> 52

16%<br />

14%<br />

12%<br />

10%<br />

8%<br />

6%<br />

4%<br />

2%<br />

0%<br />

-2%<br />

-4%<br />

-6%<br />

Emerging Markets Have “Driven” The Global Recovery<br />

2000<br />

Developed Economies Are Struggling… … Emerging Markets Are Leading<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

World<br />

Canada<br />

US<br />

Japan<br />

Eurozone<br />

• Emerging markets have helped the global economy recover<br />

16%<br />

14%<br />

12%<br />

10%<br />

8%<br />

6%<br />

4%<br />

2%<br />

0%<br />

-2%<br />

-4%<br />

-6%<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

STRATEGY & POLICY Tab 4.1<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

China<br />

India<br />

Brazil<br />

World<br />

34 <strong>of</strong> 52

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

Growth Has Not Been Driven By Consumers<br />

%<br />

1990<br />

1992<br />

1994<br />

Investment Spending Share <strong>of</strong> GDP<br />

1996<br />

1998<br />

2000<br />

2002<br />

2004<br />

2006<br />

2008<br />

2010<br />

2012<br />

2014<br />

2016<br />

STRATEGY & POLICY Tab 4.1<br />

China<br />

India<br />

Mexico<br />

Saudi Arabia<br />

World<br />

Japan<br />

Brazil<br />

United States<br />

Germany<br />

35 <strong>of</strong> 52

World Economy StrainsTo Recover Without The US<br />

7%<br />

6%<br />

5%<br />

4%<br />

3%<br />

2%<br />

1%<br />

0%<br />

-1%<br />

-2%<br />

-3%<br />

1981<br />

US Consumer Spending and Global Real GDP Growth<br />

1983<br />

1985<br />

• The US accounts for 22% <strong>of</strong> World GDP<br />

1987<br />

1989<br />

1991<br />

1993<br />

1995<br />

US Consumer<br />

World GDP<br />

• US consumers account for 70% <strong>of</strong> US GDP, or 15% <strong>of</strong> World GDP<br />

1997<br />

1999<br />

2001<br />

2003<br />

2005<br />

2007<br />

2009<br />

STRATEGY & POLICY Tab 4.1<br />

2011<br />

2013<br />

2015<br />

36 <strong>of</strong> 52

150%<br />

140%<br />

130%<br />

120%<br />

110%<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

-10%<br />

US Consumers Are Deleveraging<br />

Consumer Debt-To-Income Ratio and Debt Growth Rate<br />

1953<br />

1956<br />

1959<br />

1962<br />

1965<br />

1968<br />

1971<br />

1974<br />

1977<br />

1980<br />

1983<br />

1986<br />

1989<br />

1992<br />

1995<br />

1998<br />

2001<br />

2004<br />

Recession Growth <strong>of</strong> Debt Debt-to-Income<br />

STRATEGY & POLICY Tab 4.1<br />

2007<br />

2010<br />

2013<br />

2016<br />

• It will take some time for the debt-to-income ratio to become sustainable<br />

37 <strong>of</strong> 52

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

1970<br />

1972<br />

18 Mos<br />

1974<br />

1976<br />

15 Mos<br />

1978<br />

Employment Recovery Trends<br />

Non-farm Employment Since 1970<br />

1980<br />

26 Mos<br />

10 Mos<br />

1982<br />

1984<br />

1986<br />

1988<br />

1990<br />

30 Mos<br />

46 Mos<br />

95 Mos?<br />

• Since 1980 recovery in employment to pre-recession levels has lengthened<br />

1992<br />

1994<br />

1996<br />

1998<br />

2000<br />

2002<br />

Recession Employment (millions)<br />

2004<br />

2006<br />

STRATEGY & POLICY Tab 4.1<br />

2008<br />

2010<br />

2012<br />

2014<br />

2016<br />

38 <strong>of</strong> 52

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

The World’s Population Is Aging<br />

Proportion <strong>of</strong> Population Above 55 Years <strong>of</strong> Age<br />

1990 2000 2010 2020 2030 2040 2050<br />

• These trends underlie major global and US trends<br />

STRATEGY & POLICY Tab 4.1<br />

Japan<br />

Europe<br />

China<br />

Canada<br />

US<br />

Brazil<br />

Mexico<br />

India<br />

39 <strong>of</strong> 52

$20<br />

$0<br />

-$20<br />

-$40<br />

-$60<br />

-$80<br />

1992<br />

Billions<br />

1993<br />

1994<br />

1995<br />

1996<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

Unsustainable Trade Deficit<br />

US Trade Balance Components: 1992 -2010<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

Goods Balance Services Balance Oil Balance<br />

2008<br />

2009<br />

STRATEGY & POLICY Tab 4.1<br />

2010<br />

2011<br />

2012<br />

45% <strong>of</strong> the<br />

trade<br />

deficit is<br />

due to<br />

petroleum<br />

imports<br />

• Including oil, the goods deficit is 4.8x the services surplus, 2.8x excluding oil<br />

• Increased import dependency is unavoidable – the US needs to export more<br />

40 <strong>of</strong> 52

US Export Candidates<br />

• Bulk commodities and specialized capital goods (project cargo) fit the<br />

pr<strong>of</strong>ile <strong>of</strong> US comparative advantages<br />

• Relative to faster growing Emerging Markets, the US has<br />

• A lower cost <strong>of</strong> capital, but a higher cost <strong>of</strong> labor<br />

• Relative abundance <strong>of</strong> scare resources such as water<br />

• More advanced biotechnology<br />

• More reliable quality control and surveillance <strong>of</strong> compliance<br />

STRATEGY & POLICY Tab 4.1<br />

• Strong Emerging Market demand for bulk is expected to continue as these<br />

economies continue to grow and migrate from rural areas to industrializing<br />

urban areas<br />

• Grains and oilseeds<br />

• Meat<br />

• Bi<strong>of</strong>uels – wood pellets<br />

• Gas and Coal<br />

• Strong bulk demand also means strong demand for capital equipment –<br />

energy, construction, agricultural<br />

• US has to develop infrastructure to compete in the global market place<br />

41 <strong>of</strong> 52

Soy Yield trends In Large Producer Economies<br />

35,000<br />

30,000<br />

25,000<br />

20,000<br />

15,000<br />

10,000<br />

5,000<br />

0<br />

Soy Hectogram Yields Per Hectare<br />

1982<br />

1983<br />

1984<br />

1985<br />

1986<br />

1987<br />

1988<br />

1989<br />

1990<br />

1991<br />

1992<br />

1993<br />

1994<br />

1995<br />

1996<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

• US has the highest rate <strong>of</strong> agricultural productivity in the world<br />

USA<br />

Brazil<br />

Argentina<br />

Canada<br />

World<br />

China<br />

Indonesia<br />

• Nations with fastest growing consumption have lowest productivity<br />

STRATEGY & POLICY Tab 4.1<br />

India<br />

42 <strong>of</strong> 52

<strong>Oakland</strong>’s Share <strong>of</strong> Food Product Exports<br />

(Including Meats, Fresh & Frozen)<br />

• <strong>Oakland</strong> share <strong>of</strong><br />

Nevada, Utah, Colorado<br />

and Idaho meat product<br />

exports is significant<br />

• Good opportunities exist<br />

for increased market<br />

share in key meat<br />

producing states <strong>of</strong><br />

Nebraska, Iowa and<br />

Kansas<br />

• Export flows are<br />

consistent with rail and<br />

road transportation<br />

coverage<br />

STRATEGY & POLICY Tab 4.1<br />

43 <strong>of</strong> 52

Food Manufacturing Production Areas by County<br />

• California’s central<br />

valley is key<br />

producer <strong>of</strong> high<br />

value, specialty crops<br />

which are ideal for<br />

export<br />

• Part <strong>of</strong> the process<br />

we are going through<br />

involves identifying<br />

<strong>Oakland</strong>’s immediate<br />

hinterland as well as<br />

their opportunity<br />

areas<br />

STRATEGY & POLICY Tab 4.1<br />

44 <strong>of</strong> 52

STRATEGY & POLICY Tab 4.1<br />

<strong>Oakland</strong>’s Share <strong>of</strong> Certain Food and Beverage Export<br />

Commodities is Very High (Tree Nuts, Wine)- Opportunities<br />

to Increase in Other Commodities (Citrus, Soybeans)<br />

CALIFORNIA COLORADO IDAHO NEVADA UTAH WYOMING At <strong>Oakland</strong> Tonnage<br />

Export Food and Beverages 38% 39% 7% 64% 80% 39% 1,249,483<br />

WINES 96% 98% 97% 11% 100% 0% 532,463<br />

BERRIES (EXCEPT STRAWBERRIES) 67% 46% 6% 100% 95% 0% 1,138<br />

CITRUS FRUITS (EXCEPT ORANGES) 29% 43% 5% 71% 51% 0% 12,230<br />

CORN 12% 49% 46% 0% 41% 0% 13,687<br />

COTTON 11% 12% 6% 9% 41% 0% 62,263<br />

DRY PEAS AND BEANS 27% 19% 0% 16% 49% 0% 12,075<br />

GRAPES 33% 64% 24% 87% 91% 0% 21,344<br />

HAY, ALFALFA HAY, AND CLOVER 6% 28% 15% 100% 85% 0% 57,623<br />

NURSERY PRODUCTS AND TREES 68% 44% 1% 79% 65% 0% 1,631<br />

OILSEEDS (EXCEPT SOYBEAN) 50% 40% 2% 70% 83% 0% 9,003<br />

ORANGES 50% 82% 45% 100% 96% 0% 91,276<br />

OTHER GRAINS 35% 88% 47% 0% 93% 0% 1,392<br />

OTHER MISCELLANEOUS AGRICULTURAL PROCUCTS 20% 6% 0% 26% 86% 12% 8,131<br />

OTHER NONCITRUS FRUITS 66% 74% 4% 64% 92% 1% 70,378<br />

OTHER VEGETABLES (EXCEPT POTATOES) AND<br />

MELONS 68% 78% 5% 84% 93% 0% 77,818<br />

SOYBEANS 20% 33% 7% 66% 53% 0% 103,355<br />

STRAWBERRIES 100% 99% 86% 100% 99% 0% 1,707<br />

TREE NUTS 87% 88% 23% 76% 97% 77% 701,555<br />

45 <strong>of</strong> 52

STRATEGY & POLICY Tab 4.1<br />

There are more Opportunities to Increase <strong>Oakland</strong><br />

Imports and More Leakage to Southern California<br />

At <strong>Oakland</strong><br />

Tonnage<br />

WINES CALIFORNIA COLORADO IDAHO NEVADA UTAH WYOMING 208,100<br />

OTHER COMPUTER EQUIPMENT 13% 23% 3% 39% 49% 0% 13,741<br />

OTHER ELECTRONIC COMPONENTS 10% 17% 2% 31% 40% 0% 11,727<br />

OTHER MEASURING AND CONTROLLING DEVICES 27% 46% 72% 37% 75% 0% 10,556<br />

SEMICONDUCTORS AND RELATED DEVICES 39% 62% 28% 71% 79% 0% 14,647<br />

DRIED AND DEHYDRATED FOODS 50% 90% 0% 82% 100% 6% 83,459<br />

FROZEN FRUITS, JUICES AND VEGETABLES 24% 2% 14% 4% 31% 34% 29,482<br />

FRUITS AND VEGETABLES PRESERVED 19% 2% 11% 4% 21% 65% 118,635<br />

MEAT PRODUCTS (EXCEPT POULTRY) 19% 5% 27% 15% 43% 0% 52,049<br />

MILLED RICE AND BY-PRODUCTS 30% 50% 0% 5% 77% 0% 59,326<br />

OTHER HOUSEHOLD TEXTILE PRODUCTS 17% 47% 12% 51% 62% 20% 147,431<br />

MOTOR VEHICLE PARTS, NESOI 4% 14% 6% 16% 15% 4% 109,432<br />

MOTORCYCLES, BICYCLES, AND PARTS 39% 66% 42% 52% 67% 0% 72,954<br />

46 <strong>of</strong> 52

Main Points<br />

• Global rebalancing has begun but the recovery hasn’t<br />

• Excesses such as US and Asian trade imbalances are beginning to<br />

reverse<br />

• US is no longer able to prosper without competitive exports<br />

• US share <strong>of</strong> GDP has declined from 50% in 1980 to 22% in 2011<br />

• Comparative advantage in agriculture, energy and high-end capital<br />

goods<br />

• <strong>Oakland</strong> is an export gateway to fast growing economies<br />

• Growth will depend on proper planning and execution<br />

STRATEGY & POLICY Tab 4.1<br />

47 <strong>of</strong> 52

STRATEGY & POLICY Tab 4.1<br />

Summary<br />

• <strong>Oakland</strong> has significant opportunities to increase exports<br />

provided there are enough imports to provide empty<br />

equipment<br />

• Exports from the Midwest are a key target area and planned<br />

infrastructure development adjacent to the port on the<br />

<strong>Oakland</strong> Army Base could play a big part in attracting some <strong>of</strong><br />

these commodities<br />

• As we go through the next steps <strong>of</strong> the project, additional<br />

opportunities will surface and that will help in moving towards<br />

the next phase <strong>of</strong> building the strategic plan<br />

48 <strong>of</strong> 52

CONSENT ITEMS<br />

CONSENT ITEMS Tab 5<br />

Action by the Board under “Consent Items” means that all<br />

matters listed below have been summarized, and are<br />

considered to be perfunctory in nature, and will be adopted<br />

by one motion and appropriate vote. Consent Items may be<br />

removed for further discussion by the Board at the request <strong>of</strong><br />

any member <strong>of</strong> the Board.<br />

49 <strong>of</strong> 52

REMAINING ACTION ITEMS<br />

REMAINING ACTION ITEMS Tab 6<br />

Remaining Action Items are items not previously addressed<br />

in this <strong>Agenda</strong> that may require staff presentation and/or<br />

discussion and information prior to action by the Board.<br />

50 <strong>of</strong> 52

UPDATES & ANNOUNCEMENTS Tab 7<br />

UPDATES & ANNOUNCEMENTS<br />

The President and / or Executive Director will report on<br />

noteworthy events occurring since the last Board Meeting.<br />

51 <strong>of</strong> 52

SCHEDULING<br />

SCHEDULING Tab 8<br />

This segment <strong>of</strong> the meeting is reserved for scheduling<br />

items for future <strong>Agenda</strong>s and/or scheduling Special<br />

Meetings.<br />

52 <strong>of</strong> 52