Thomson Reuters European Crude and Products Swap ...

Thomson Reuters European Crude and Products Swap ...

Thomson Reuters European Crude and Products Swap ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

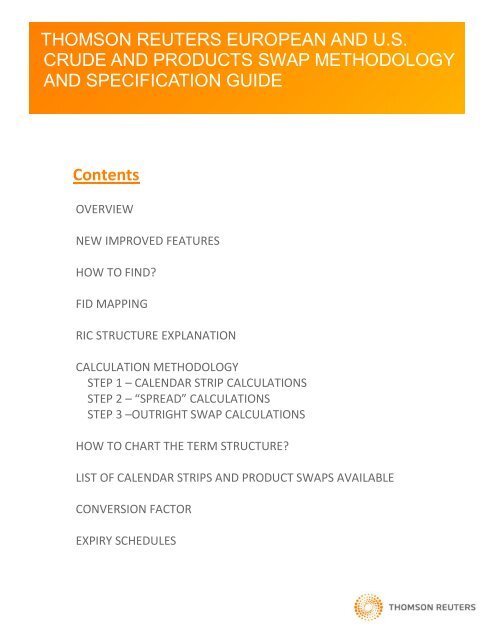

THOMSON REUTERS EUROPEAN AND U.S.<br />

CRUDE AND PRODUCTS SWAP METHODOLOGY<br />

AND SPECIFICATION GUIDE<br />

Contents<br />

OVERVIEW<br />

NEW IMPROVED FEATURES<br />

HOW TO FIND?<br />

FID MAPPING<br />

RIC STRUCTURE EXPLANATION<br />

CALCULATION METHODOLOGY<br />

STEP 1 – CALENDAR STRIP CALCULATIONS<br />

STEP 2 – “SPREAD” CALCULATIONS<br />

STEP 3 –OUTRIGHT SWAP CALCULATIONS<br />

HOW TO CHART THE TERM STRUCTURE?<br />

LIST OF CALENDAR STRIPS AND PRODUCT SWAPS AVAILABLE<br />

CONVERSION FACTOR<br />

EXPIRY SCHEDULES

Overview<br />

<strong>Thomson</strong> <strong>Reuters</strong> provides extended forward curve assessments for the <strong>European</strong> <strong>and</strong> US <strong>Crude</strong><br />

<strong>and</strong> Oil <strong>Products</strong>. As a further enhancement, <strong>Thomson</strong> <strong>Reuters</strong> is introducing a change in the<br />

source for the Calendar Strip calculations <strong>and</strong> is also introducing Balance of Month (BOM),<br />

Balance of Quarter (BOQ) <strong>and</strong> Balance of Year (BOY) RICs for all the Calendar Strips <strong>and</strong> <strong>Swap</strong>s.<br />

The Calendar Strips which were being calculated using the respective Future Contracts will be<br />

calculated using the respective Future Fair Value Curves going forward.<br />

The Fair Value curves that <strong>Thomson</strong> <strong>Reuters</strong> launched recently are independently sourced <strong>and</strong><br />

rigorously crafted, in real time. The Fair Value algorithm uses a combination of real-time bid,<br />

ask, intermonth <strong>and</strong>/or interproduct spread <strong>and</strong> other data to arrive at a theoretical price level<br />

for each individual traded contract. These are published in real time throughout the day as the<br />

markets change, so there is access to accurate forward-curve data for decision making. The Fair<br />

Value curves can be accessed from the page .<br />

The Calendar Strip assessments include ICE Brent <strong>Crude</strong> Oil, Gasoil, Heating Oil, RBOB Gasoline,<br />

WTI crude oil <strong>and</strong> NYMEX Light Sweet <strong>Crude</strong> Oil, Heating Oil, RBOB Gasoline.<br />

The calendar strip assessments are provided for as many months as the respective future<br />

contracts, 10 Quarters <strong>and</strong> 3 Years forward.<br />

The <strong>Products</strong> <strong>Swap</strong> assessments include Propane, Naphtha, Mogas, Unleaded Gasoline, Gasoil<br />

0.1%, Gasoil 10ppm, Jet Fuel, Diesel, Heating Oil, High Sulphur Fuel Oil <strong>and</strong> Low Sulphur Fuel Oil.<br />

The Product <strong>Swap</strong> assessments are provided for 24 Months, 10 Quarters <strong>and</strong> 3 Years forward.<br />

BFO CFD <strong>and</strong> Dated <strong>Swap</strong> assessments are also provided for 6 Weeks, 24 Months, 10 Quarters<br />

<strong>and</strong> 3 Years forward.<br />

The Calendar Strips are calculated as the weighted average of the respective future fair value<br />

contracts.<br />

The Product Outright <strong>Swap</strong>s are always calculated by applying the corresponding crack spreads<br />

<strong>and</strong> differential swap spreads to the respective calendar strips. The new methodology aims at<br />

providing the outright values through the “spreads” rather than just the direct outright value.<br />

In order to do so the “spreads” are assessed during the day from the price discovery process by<br />

the editorial also including data from different sources <strong>and</strong> brokers, thus providing the latest<br />

“spreads” for each of the products. These “spreads” when applied to the calendar strips provide<br />

a real time live outright swap data in line with the trades on the future contracts. So each of the<br />

products has “spreads” <strong>and</strong> outright swaps both assessed real time.<br />

The Light Distillates- Propane, Naphtha, Mogas <strong>and</strong> Unleaded Gasoline are calculated by<br />

applying the crack spreads to the calendar strips.<br />

The Mid Distillates- Gasoil 0.1%, Gasoil 10ppm, Jet Fuel, Diesel, Heating Oil are calculated by<br />

applying the differential swap spreads to the calendar strips.<br />

The Heavy products -High Sulphur Fuel Oil <strong>and</strong> Low Sulphur Fuel Oil are calculated by applying<br />

the crack spreads to the calendar strips.

The close value for the calendar strips are calculated from the settle/close value of the future<br />

fair value contracts. The close for the calendar strips <strong>and</strong> corresponding swaps is updated at<br />

00:30 GMT for EU <strong>and</strong> 23:30 GMT for US.<br />

The close is snapped to the historical database at 00:45 GMT for EU <strong>and</strong> 23:45 GMT for US.<br />

The net change between the previous day’s close <strong>and</strong> current day’s latest price is available on<br />

FID 11 (NETCHNG_1).<br />

New Improved Features<br />

Extended Forward Curves.<br />

The calendar strip assessments provided for as many months as the respective future<br />

fair value contracts, 10 Quarters <strong>and</strong> 3 Years forward.<br />

Rolling <strong>and</strong> Continuous form of RICs with calendar rolling pattern.<br />

Real time updates refreshed as <strong>and</strong> when there is an update on either the future fair<br />

value contracts or the differential swaps <strong>and</strong> crack spreads.<br />

Improved calculation methodology using the “spreads”.<br />

Use of interpolation <strong>and</strong> extrapolation techniques taking into account the seasonality<br />

<strong>and</strong> convenience yield where relevant for assessing the forward curves.<br />

Individual pages providing composite view specific to products <strong>and</strong> markets.<br />

All <strong>Crude</strong> <strong>Swap</strong>s expressed in USD/BBL. All Product <strong>Swap</strong>s expressed in USD/TONNE.<br />

For some of the future contracts which are quoted in USD/U GAL, the corresponding<br />

calendar strips assessments are provided in both USD/U GAL <strong>and</strong> USD/TONNE.<br />

Introduction of BOM, BOQ <strong>and</strong> BOY RICs for Calendar Strips <strong>and</strong> <strong>Swap</strong>s.<br />

Use of Future Fair Value Curves as source for calculating Calendar Strips.<br />

How to find?<br />

in Kobra quote object will display the overview menu for the EU, US <strong>and</strong> AS<br />

calendar strips <strong>and</strong> swaps categorized by regions into crude swaps; products swaps - in the<br />

order of light distillates, mid distillates, heavy products <strong>and</strong> individual composite views.

FID Mapping<br />

PRIMACT_1 (FID 393) - The latest update value<br />

PRIMACT_2 (FID 394) – The second latest update value<br />

PRIMACT_3 (FID 395) – The third latest update value<br />

VALUE_DT1 (FID 875) – The date of the latest update in FID 393<br />

VALUE_DT2 (FID 876) – The date of the second latest update in FID 394<br />

VALUE_DT3 (FID 877) – The date of the third latest update in FID 395<br />

VALUE_TS1 (FID 1010) – The time of the latest update in FID 393<br />

VALUE_TS2 (FID 1011) - The time of update in FID 394<br />

VALUE_TS3 (FID 1012) – The time of update in FID 395<br />

HST_CLOSE (FID 21) – The close value of the previous day<br />

HSTCLSDATE (FID 79) – The date of the previous day’s close value<br />

DATE _RANGE (FID 859) – The contract month, quarter or year<br />

CURRENCY (FID 15) – The currency in which the swaps are expressed<br />

LOTSZNITS (FID 54) – The units in which the swaps are expressed

RIC Structure Explanation<br />

Calendar Strips<br />

Rolling RICs <strong>and</strong> Chains<br />

The rolling RICs for calendar strips use the code of the respective future contracts followed by<br />

‘CAL’ then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by the<br />

corresponding one letter code <strong>and</strong> the last digit of the year.<br />

Example: ICE Brent <strong>Crude</strong> LCO Calendar Strip<br />

LCO + CAL + M + K + 0 -----> LCOCALMK0 ------ > May 2010 Month contract<br />

LCO + CAL + Q + U +0 ----- > LCOCALQU0 --------> 3 Quarter 2010 contract<br />

LCO + CAL + Y + Z + 1 ------ > LCOCALYZ1 ---------> 2011 Year contract<br />

The composite chain for the calendar strip rolling RICs follows the same structure with the<br />

future contract code followed by ‘CAL’ <strong>and</strong> then a ‘:’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Individual chains for the months, quarters <strong>and</strong> years are also available, where they follow the<br />

same structure as the composite chain followed by ‘M:’ for month, ‘Q:’ for quarter, ‘Y:’ for year.<br />

Example: <br />

<br />

<br />

Continuous RICs <strong>and</strong> Chains<br />

The continuous RICs for calendar strips use the code of the respective future contracts followed<br />

by ‘CAL’ then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by ‘c’ <strong>and</strong> 1, 2,..<br />

Example: ICE Brent <strong>Crude</strong> LCO Calendar Strip<br />

LCO + CAL + M + c + 1 -----> LCOCALMc1 ------ > the first Month contract continuation<br />

LCO + CAL + Q + c +1 ----- > LCOCALQc1 --------> the first Quarter contract continuation<br />

LCO + CAL + Y + c + 1 ------ > LCOCALYc1---------> the first Year contract continuation<br />

The composite chain for the calendar strip continuous RICs follows the same structure with the<br />

future contract code followed by ‘CAL’ <strong>and</strong> then a ‘c’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Crack Spreads from Calendar Strips<br />

Rolling RICs <strong>and</strong> Chains<br />

The rolling RICs for crack spread from calendar strips use the code of the respective future<br />

contracts followed by ‘C’ then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them<br />

followed by the corresponding one letter code <strong>and</strong> the last digit of the year.<br />

Example: ICE Gasoil LGO Crack Spread<br />

LGO + C+ M + K + 0 -----> LGOCMK0 ------ > May 2010 Month contract<br />

LGO + C + Q + U +0 ----- > LGOCQU0 --------> 3 Quarter 2010 contract<br />

LGO + C + Y + Z + 1 ------ > LGOCYZ1 ---------> 2011 Year contract

The composite chain for the crack spread rolling RICs follow the same structure with the future<br />

contract code followed by ‘C’ <strong>and</strong> then a ‘:’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Individual chains for the months, quarters <strong>and</strong> years are also available, where they follow the<br />

same structure as the composite chain followed by ‘M:’ for month, ‘Q:’ for quarter, ‘Y:’ for year.<br />

Example: <br />

<br />

<br />

Continuous RICs <strong>and</strong> Chains<br />

The continuous RICs for crack spread of calendar strips use the code of the respective future<br />

contracts followed by ‘C’ then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed<br />

by ‘c’ <strong>and</strong> 1, 2,..<br />

Example: ICE Gasoil LGO Crack Spread<br />

LGO + C + M + c + 1 -----> LGOCMc1 ------ > the first Month contract continuation<br />

LGO + C + Q + c +1 ----- > LGOCQc1 --------> the first Quarter contract continuation<br />

LGO + C+ Y + c + 1 ------ > LGOCYc1---------> the first Year contract continuation<br />

The composite chain for the crack spread continuous RICs follows the same structure with the<br />

future contract code followed by ‘C’ <strong>and</strong> then a ‘c’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Product Outright <strong>Swap</strong>s<br />

Rolling RICs <strong>and</strong> Chains<br />

The first three characters in the rolling RICs for product swaps denote the product; followed by<br />

‘C’ for CIF or ‘F’ for FOB; the next three characters for region; then ‘M’ for Month, ‘Q’ for<br />

Quarter, ‘Y’ for Year; each of them followed by the corresponding one letter code <strong>and</strong> the last<br />

digit of the year.<br />

Example: Naphtha CIF Cargo NWE Outright <strong>Swap</strong><br />

NAP + C + NWE + M + K + 0 -----> NAPCNWEMK0 ------ > May 2010 Month contract<br />

NAP + C + NWE + Q + U +0 ----- > NAPCNWEQU0 -------> 3 Quarter 2010 contract<br />

NAP + C + NWE + Y + Z + 1 ------ >NAPCNWEYZ1 ---------> 2011 Year contract<br />

The composite chain for the product outright swap rolling RICs follows the same structure with<br />

first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB; the next three<br />

characters for region; then a ‘:’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Individual chains for the months, quarters <strong>and</strong> years are also available, where they follow the<br />

same structure as the composite chain followed by ‘M:’ for month, ‘Q:’ for quarter, ‘Y:’ for year.<br />

Example: <br />

<br />

Continuous RICs <strong>and</strong> Chains<br />

The first three characters in the continuous RICs for product swaps denote the product;<br />

followed by ‘C’ for CIF or ‘F’ for FOB; the next three characters for region; then ‘M’ for Month,<br />

‘Q’ for Quarter, ‘Y’ for Year; each of them followed by ‘c’ <strong>and</strong> 1, 2,..<br />

Example: Naphtha CIF Cargo NWE Outright <strong>Swap</strong><br />

NAP + C + NWE + M + c + 1 -----> NAPCNWEMc1 ------ > the first Month contract continuation<br />

NAP + C + NWE + Q + c + 1 ----- > NAPCNWEQc1 --------> the first Quarter contract continuation<br />

NAP + C + NWE + Y + c+ 1 ------ >NAPCNWEYc1 ---------> the first Year contract continuation<br />

The composite chain for the product outright swap continuous RICs follows the same structure<br />

with first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB; the next<br />

three characters for region; then a ‘c’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Product Crack Spreads<br />

Rolling RICs <strong>and</strong> Chains<br />

The first three characters in the rolling RICs for product crack spread denote the product;<br />

followed by ‘C’ for CIF or ‘F’ for FOB; the next three characters for region; ‘C’ for Crack; then ‘M’<br />

for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by the corresponding one letter<br />

code <strong>and</strong> the last digit of the year.<br />

Example: Naphtha CIF Cargo NWE Crack Spread<br />

NAP + C + NWE + C + M + K + 0 -----> NAPCNWECMK0 ------ > May 2010 Month contract<br />

NAP + C + NWE + C + Q + U +0 ----- > NAPCNWECQU0 --------> 3 Quarter 2010 contract<br />

NAP + C + NWE + C + Y + Z + 1 ------ >NAPCNWECYZ1 ---------> 2011 Year contract<br />

The composite chain for the product crack spread rolling RICs follows the same structure with<br />

first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB; the next three<br />

characters for region; ‘C’ for Crack; then a ‘:’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Individual chains for the months, quarters <strong>and</strong> years are also available, where they follow the<br />

same structure as the composite chain followed by ‘M:’ for month, ‘Q:’ for quarter, ‘Y:’ for year.<br />

Example: <br />

<br />

<br />

Continuous RICs <strong>and</strong> Chains<br />

The first three characters in the continuous RICs for product crack spread denote the product;<br />

followed by ‘C’ for CIF or ‘F’ for FOB; the next three characters for region; ‘C’ for Crack; then ‘M’<br />

for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by ‘c’ <strong>and</strong> 1, 2,..<br />

Example: Naphtha CIF Cargo NWE Crack Spread<br />

NAP + C + NWE + C+M + c+ 1 -----> NAPCNWECMc1------ > the first Month contract continuation<br />

NAP + C + NWE + C+ Q + c+ 1 ----> NAPCNWECQc1--------> the first Quarter contract continuation<br />

NAP + C + NWE + C+ Y + c+ 1 ------ >NAPCNWECYc1 ---------> the first Year contract continuation

The composite chain for the product crack spread continuous RICs follows the same structure<br />

with first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB; the next<br />

three characters for region; ‘C’ for Crack; then a ‘c’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Product Differential <strong>Swap</strong> Spreads<br />

Rolling RICs <strong>and</strong> Chains<br />

The first three characters in the rolling RICs for product differential swap spread denote the<br />

product; followed by ‘C’ for CIF or ‘F’ for FOB; the next three characters for region; ‘D’ for<br />

Differential; then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by the<br />

corresponding one letter code <strong>and</strong> the last digit of the year.<br />

Example: Jet Fuel CIF Cargo NWE Differential <strong>Swap</strong><br />

JET + C + NWE + D + M + K + 0 -----> JETCNWEDMK0 ------ > May 2010 Month contract<br />

JET + C + NWE + D + Q + U +0 ----- > JETCNWEDQU0 --------> 3 Quarter 2010 contract<br />

JET + C + NWE + D + Y + Z + 1 ------ >JETCNWEDYZ1 ---------> 2011 Year contract<br />

The composite chain for the product differential swap spread rolling RICs follows the same<br />

structure with first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB;<br />

the next three characters for region; ‘D’ for Differential; then a ‘:’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example: <br />

Individual chains for the months, quarters <strong>and</strong> years are also available, where they follow the<br />

same structure as the composite chain followed by ‘M:’ for month, ‘Q:’ for quarter, ‘Y:’ for year.<br />

Example: <br />

<br />

<br />

Continuous RICs <strong>and</strong> Chains<br />

The first three characters in the continuous RICs for product differential swap spread denote the<br />

product; followed by ‘C’ for CIF or ‘F’ for FOB; the next three characters for region; ‘D’ for<br />

Differential; then ‘M’ for Month, ‘Q’ for Quarter, ‘Y’ for Year; each of them followed by ‘c’ <strong>and</strong> 1,<br />

2,..<br />

Example: Jet Fuel CIF Cargo NWE Differential <strong>Swap</strong><br />

JET + C + NWE + D+M + c+ 1 -----> JETCNWEDMc1------ > the first Month contract continuation<br />

JET + C + NWE + D+ Q + c+ 1 -----> JETCNWEDQc1--------> the first Quarter contract continuation<br />

JET + C + NWE + D+ Y + c+ 1 ------ >JETCNWEDYc1 ---------> the first Year contract continuation<br />

The composite chain for the product differential swap spread continuous RICs follows the same<br />

structure with first three characters denoting the product; followed by ‘C’ for CIF or ‘F’ for FOB;<br />

the next three characters for region; ‘D’ for Differential; then a ‘c’ <strong>and</strong> all this preceded by a ‘0#’<br />

Example:

RIC Structure Explanation for BOM, BOQ <strong>and</strong> BOY RICs<br />

Rolling RICs<br />

The rolling RICs for BOM, BOQ <strong>and</strong> BOY calendar strips <strong>and</strong> swaps use the same code as the<br />

existing calendar strips <strong>and</strong> swaps but with an additional ‘B’ for ‘Balance’ in the RIC name.<br />

Example: ICE Brent <strong>Crude</strong> LCO Calendar Strip BOM, BOQ <strong>and</strong> BOY RICs<br />

LCO + CAL + B + M + G + 3 -----> LCOCALBMG3 ------ > Feb 2013 Balance of Month contract<br />

LCO + CAL + B + Q + H + 3 ----- > LCOCALBQH3 --------> 2013 Balance of Quarter contract<br />

LCO + CAL + B + Y + Z + 3 ------ > LCOCALBYZ3 ---------> 2013 Balance of Year contract<br />

The BOM, BOQ <strong>and</strong> BOY RICs can be accessed from the respective existing composite chains.<br />

Example: , , can be accessed from the chain<br />

<br />

Continuous RICs<br />

The continuous RICs for BOM, BOQ <strong>and</strong> BOY calendar strips <strong>and</strong> swaps use the same code as the<br />

existing calendar strips <strong>and</strong> swaps but with a ‘c0’ (<strong>and</strong> without ‘B’) in the RIC name. So the BOM,<br />

BOQ <strong>and</strong> BOY continuous RICs will be denoted by ‘c0’ <strong>and</strong> the first, second <strong>and</strong> consecutive<br />

forwards by c1, c2 etc., respectively.<br />

Example: ICE Brent <strong>Crude</strong> LCO Calendar Strip BOM, BOQ <strong>and</strong> BOY RICs<br />

LCO + CAL + M + c + 0 -----> LCOCALMc0 ------ > Balance of Month contract continuation<br />

LCO + CAL + Q + c +0 ----- > LCOCALQc0 --------> Balance of Quarter contract continuation<br />

LCO + CAL + Y + c + 0 ------ > LCOCALYc0---------> Balance of Year contract continuation<br />

The BOM, BOQ <strong>and</strong> BOY RICs can be accessed from the respective existing composite chains.<br />

Example: , , can be accessed from the chain<br />

Calculation Methodology<br />

Step 1 – Calendar Strip Calculations<br />

i) BOM Calendar Strip Calculation<br />

The BOM calendar strips are calculated as the weighted average of the future fair value<br />

contracts (weight: based on working days)<br />

Illustration:<br />

ICE Brent <strong>Crude</strong> LCO Calendar Strip BOM calculation for the month of FEB 2013 <br />

The below formula is used:<br />

(D1 * LCOFVH3 + D2 * LCOFVJ3) / (D1 + D2)<br />

Where:<br />

is the future fair value contract for the month of March 2013<br />

is the future fair value contract for the month of April 2013<br />

D1 is the number of days from the day the calendar strip is calculated till the expiry date of the<br />

first future fair value contract; excluding the expiry date, Saturday, Sunday <strong>and</strong> holiday.<br />

D2 is the number of days from the expiry date till the end of the month, including the expiry<br />

date <strong>and</strong> excluding Saturday, Sunday <strong>and</strong> holiday.<br />

expires 13th Feb 2013<br />

expires 14th Mar 2013<br />

D1 is the number of working days from 1st Feb 2013 to 13th Feb 2013 (exclusive of 13th Feb)<br />

D2 is the number of working days from 13th Feb 2013 to 28th Feb 2013 (inclusive of 13th Feb)<br />

When the first leg of the calendar strip BOM i.e., expires on 13th Feb 2013, the<br />

calendar strip BOM value from 14th Feb to 28th Feb 2013 will be equal to the second leg i.e.,<br />

.<br />

Note: For Nymex contracts, the D1 will include the expiry date <strong>and</strong> is excluded from D2.<br />

ii) Forward Months Calendar Strip Calculation<br />

The calendar strips for forward months are calculated as the weighted average of the future fair<br />

value contracts (weight: based on working days)<br />

Illustration:<br />

ICE Brent <strong>Crude</strong> LCO Calendar Strip calculation for the month of MAR <br />

The below formula is used:<br />

(D1 * LCOFVJ3 + D2 * LCOFVK3) / (D1 + D2)

Where:<br />

is the future fair value contract for the month of April 2013<br />

is the future fair value contract for the month of May 2013<br />

D1 is the number of days from the day the calendar strip is calculated till the expiry date of the<br />

first future fair value contract; excluding the expiry date, Saturday, Sunday <strong>and</strong> holiday.<br />

D2 is the number of days from the expiry date till the end of the month, including the expiry<br />

date <strong>and</strong> excluding Saturday, Sunday <strong>and</strong> holiday.<br />

Note: For Nymex contracts, the D1 will include the expiry date <strong>and</strong> is excluded from D2.<br />

The calendar strips for quarters are calculated as the average of the month calendar strips<br />

applying in that quarter.<br />

The calendar strips for years are calculated as the average of the month/quarter calendar strips<br />

applying in that year.<br />

Step 2 – “Spread” Calculations<br />

The “spreads” – crack <strong>and</strong> differential for the products are assessed from the price discovery<br />

process during the day.<br />

The process involves assessing data from different sources, brokers, traders <strong>and</strong> editorial.<br />

The aim is to determine the “spreads” for each of the products.<br />

During the course, if an outright value is available for any of the products from any of the<br />

sources, then the “spread” implied by that outright value at that point of time is derived.<br />

If the implied “spread” cannot be derived from an outright value, then it is not considered.<br />

The implied “spread” is then applied to the calendar strips to obtain the outright swaps.<br />

Step 3 –Outright <strong>Swap</strong> Calculations<br />

The “spreads” obtained from step 2 for each of the products is applied to the respective<br />

calendar strips to calculate the outright swap for each of those products.<br />

Illustration:<br />

Naphtha CIF Cargo NWE Outright <strong>Swap</strong> Calculation for the month of MAY <br />

1. Identify the reference calendar strip.<br />

As Naphtha is a light distillate, the reference calendar strip is the Brent crude <br />

2. Identify the crack spread. Here there can be two possibilities.<br />

a) The crack spread is available.<br />

In this case the crack spread is available on the RIC <br />

b) The crack spread is not available.

3. Calculate the outright swap. Here again there can be two possibilities.<br />

a) The crack spread is available.<br />

Apply the crack spread on the RIC to the calendar strip on the RIC<br />

. Both the calendar strip <strong>and</strong> crack spread are expressed in USD/BBL. The<br />

conversion factor has to be applied to obtain the outright swap in USD/TONNE.<br />

b) The crack spread is not available.<br />

In this case the interpolation <strong>and</strong> extrapolation techniques are employed.<br />

Interpolation – If the data has to be calculated for maturity period(s) in between two<br />

periods having data then interpolation is used.<br />

Extrapolation – If the data has to be calculated for maturity period(s) before periods<br />

having data (rare case) or further than periods having data then extrapolation is used.

If the crack spread for some month maturities is not available, then the data for those<br />

months are extrapolated (screenshot below)<br />

Extrapolated<br />

as no Crack<br />

Spreads

If the crack spread for some quarter maturities is not available, then the data for the<br />

months applying in that quarter is extrapolated <strong>and</strong> then the quarter is calculated from<br />

the months. (screenshot below – where the 2Q12 is calculated from the extrapolated<br />

month values)<br />

Extrapolated<br />

as no Crack<br />

Spreads

How To Chart The Term Structure?<br />

1. Insert in new frame (or pop-up) an empty chart object.<br />

2. Right click on the chart object <strong>and</strong> select ‘Insert Analysis’

3. From the list select ‘Term Structure’<br />

4. Under the tab ‘General’, in the box under ‘Instrument’ type in the chain for which the<br />

term structure is required.<br />

5. Under the ‘Parameters’ section, in the box for ‘Forward Contracts’ type in the number<br />

of months, quarters or years depending upon the instrument used.<br />

6. Click on ‘ADD’

7. The Term Structure will be displayed.<br />

8. The Term Structure for another instrument can be displayed in the same chart by<br />

repeating the above steps.

List of Calendar Strips <strong>and</strong> Product <strong>Swap</strong>s Available<br />

EU – <strong>Crude</strong> <strong>Swap</strong><br />

ICE Brent <strong>Crude</strong> Oil Calendar Strip <br />

ICE WTI <strong>Crude</strong> Oil Calendar Strip <br />

BFO CFD <br />

BFO DATED <strong>Swap</strong> <br />

EU – Product <strong>Swap</strong><br />

Propane CIF NWE Outright <strong>Swap</strong> <br />

Propane CIF NWE Crack Spread <br />

Naphtha CIF Cargo NWE Outright <strong>Swap</strong> <br />

Naphtha CIF Cargo NWE Crack Spread <br />

ICE RBOB Gasoline Calendar Strip (US Gallons) <br />

ICE RBOB Gasoline Calendar Strip (Tonnes) <br />

Mogas FOB Barge ARA Outright <strong>Swap</strong> <br />

Mogas FOB Barge ARA Crack Spread <br />

Mogas FOB MED Outright <strong>Swap</strong> <br />

Mogas FOB MED Crack Spread <br />

Mogas FOB NWE Outright <strong>Swap</strong> <br />

Mogas FOB NWE Crack Spread <br />

Jet Fuel CIF Cargo NWE Outright <strong>Swap</strong> <br />

Jet Fuel CIF Cargo NWE Differential <strong>Swap</strong> <br />

Jet Fuel FOB ARA Outright <strong>Swap</strong> <br />

Jet Fuel FOB ARA Differential <strong>Swap</strong> <br />

ICE Gasoil Calendar Strip <br />

ICE Gasoil Crack Spread <br />

GasOil 0.1% CIF Cargo NWE Outright <strong>Swap</strong> <br />

GasOil 0.1% CIF Cargo NWE Differential <strong>Swap</strong> <br />

GasOil 0.1% FOB NWE Outright <strong>Swap</strong> <br />

GasOil 0.1% FOB NWE Differential <strong>Swap</strong> <br />

GasOil 0.1% FOB MED Outright <strong>Swap</strong> <br />

GasOil 0.1% FOB MED Differential <strong>Swap</strong> <br />

GasOil 0.1% FOB ARA Outright <strong>Swap</strong> <br />

GasOil 0.1% FOB ARA Differential <strong>Swap</strong> <br />

GasOil 10ppm CIF Cargo NWE Outright <strong>Swap</strong> <br />

GasOil 10ppm CIF Cargo NWE Differential <strong>Swap</strong> <br />

GasOil 10ppm CIF MED Outright <strong>Swap</strong> <br />

GasOil 10ppm CIF MED Differential <strong>Swap</strong> <br />

GasOil 10ppm FOB Barge ARA Outright <strong>Swap</strong> <br />

GasOil 10ppm FOB Barge ARA Differential <strong>Swap</strong> <br />

ICE Heating Oil Calendar Strip (US Gallons) <br />

ICE Heating Oil Calendar Strip (Tonnes)

Fuel Oil 3.5% CIF NWE Outright <strong>Swap</strong> <br />

Fuel Oil 3.5% CIF NWE Crack Spread <br />

Fuel Oil 3.5% CIF MED Outright <strong>Swap</strong> <br />

Fuel Oil 3.5% CIF MED Crack Spread <br />

Fuel Oil 3.5% FOB MED Outright <strong>Swap</strong> <br />

Fuel Oil 3.5% FOB MED Crack Spread <br />

Fuel Oil 3.5% FOB Barge ARA Outright <strong>Swap</strong> <br />

Fuel Oil 3.5% FOB Barge ARA Crack Spread <br />

Fuel Oil 1.0% FOB Cargo NWE Outright <strong>Swap</strong> <br />

Fuel Oil 1.0% FOB Cargo NWE Crack Spread <br />

Fuel Oil 1.0% FOB ARA Outright <strong>Swap</strong> <br />

Fuel Oil 1.0% FOB ARA Crack Spread <br />

Fuel Oil 1.0% FOB MED Outright <strong>Swap</strong> <br />

Fuel Oil 1.0% FOB MED Crack Spread <br />

ICE Sulphur Gas Calendar Strip <br />

EU – Natgas <strong>Swap</strong><br />

ICE Natgas NGLN Calendar Strip <br />

US – <strong>Crude</strong> <strong>Swap</strong><br />

Nymex WTI <strong>Crude</strong> Calendar Strip <br />

US – Product <strong>Swap</strong><br />

Nymex RBOB Gasoline Calendar Strip (US Gallons) <br />

Nymex RBOB Gasoline Calendar Strip (Tonnes) <br />

Nymex RBOB Gasoline Crack Spread <br />

Unleaded Gasoline FOB USG Crack Spread <br />

Unleaded Gasoline FOB USG Outright <strong>Swap</strong> <br />

Jet Fuel FOB USG Outright <strong>Swap</strong> <br />

Jet Fuel FOB USG Differential <strong>Swap</strong> <br />

ULSD FOB NYH Outright <strong>Swap</strong> <br />

ULSD FOB NYH Differential <strong>Swap</strong> <br />

ULSD FOB USG Outright <strong>Swap</strong> <br />

ULSD FOB USG Differential <strong>Swap</strong> <br />

Nymex Heating Oil Calendar Strip (US Gallons) <br />

Nymex Heating Oil Calendar Strip (Tonnes) <br />

Nymex Heating Oil Crack Spread <br />

Heating Oil FOB USG Outright <strong>Swap</strong> <br />

Heating Oil FOB USG Differential <strong>Swap</strong> <br />

Fuel Oil 3.5% FOB Barge USG Outright <strong>Swap</strong> <br />

Fuel Oil 3.5% FOB Barge USG Crack Spread <br />

Fuel Oil 1.0% FOB NYH Outright <strong>Swap</strong> <br />

Fuel Oil 1.0% FOB NYH Crack Spread <br />

US – Natgas <strong>Swap</strong><br />

Nymex Natgas NG Calendar Strip

Conversion Factor<br />

Expiry Schedules<br />

BBL/TONNE<br />

Brent <strong>Crude</strong> 7.4<br />

WTI <strong>Crude</strong> 7.33<br />

Propane 12.409<br />

Naphtha 8.9<br />

RBOB Gasoline 8.45<br />

Gasoline 8.405<br />

Jet Fuel 7.88<br />

Gas Oil 7.45<br />

Heating Oil 7.5<br />

Diesel 7.5<br />

High Sulphur Fuel Oil 6.317<br />

Low Sulphur Fuel Oil 6.368<br />

All the calendar strips <strong>and</strong> swaps which were previously following the expiry pattern of the<br />

respective future contracts will now follow calendar expiry pattern.<br />

Expiry pattern for Forward contracts<br />

All forward month contracts will expire on last day of the month preceeding the contract month.<br />

Ex: will expire last day of Feb i.e., 28th Feb 2013.<br />

All forward quarter contracts will expire on last day of the preceeding quarter.<br />

Ex: will expire last day of March i.e., 31st March 2013.<br />

All forward year contracts will expire on last day of the preceeding year.<br />

Ex: will expire last day of December i.e., 3st Dec 2013.<br />

Expiry pattern for ‘Balance Of’ contracts<br />

The BOM (Balance of Month) contract will expire last day of the contract month.<br />

Ex: will expire last day of Feb i.e., 28th Feb 2013.<br />

The BOQ (Balance of Quarter) contract will expire last day of the quarter.<br />

Ex: will expire last day of March i.e., 31st March 2013.<br />

The BOY (Balance of Year) contract will expire last day of the year.<br />

Ex: will expire last day of December i.e., 31st Dec 2013.<br />

Back to Contents