Agricultural Value Chains in the Mexicali Valley of Mexico: Main ...

Agricultural Value Chains in the Mexicali Valley of Mexico: Main ...

Agricultural Value Chains in the Mexicali Valley of Mexico: Main ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

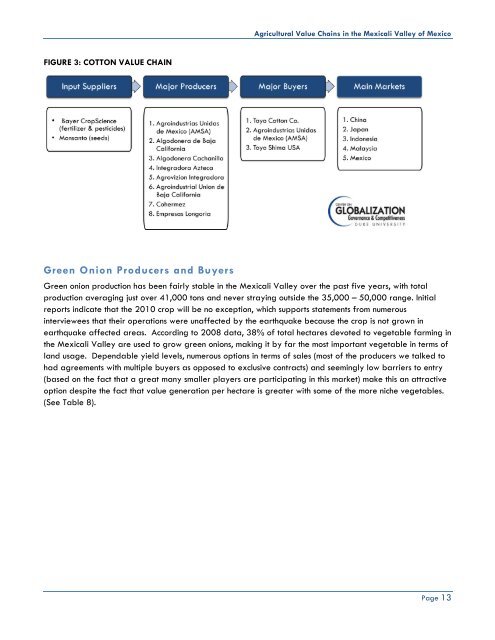

FIGURE 3: COTTON VALUE CHAIN<br />

Green Onion Producers and Buyers<br />

<strong>Agricultural</strong> <strong>Value</strong> <strong>Cha<strong>in</strong>s</strong> <strong>in</strong> <strong>the</strong> <strong>Mexicali</strong> <strong>Valley</strong> <strong>of</strong> <strong>Mexico</strong><br />

Green onion production has been fairly stable <strong>in</strong> <strong>the</strong> <strong>Mexicali</strong> <strong>Valley</strong> over <strong>the</strong> past five years, with total<br />

production averag<strong>in</strong>g just over 41,000 tons and never stray<strong>in</strong>g outside <strong>the</strong> 35,000 – 50,000 range. Initial<br />

reports <strong>in</strong>dicate that <strong>the</strong> 2010 crop will be no exception, which supports statements from numerous<br />

<strong>in</strong>terviewees that <strong>the</strong>ir operations were unaffected by <strong>the</strong> earthquake because <strong>the</strong> crop is not grown <strong>in</strong><br />

earthquake affected areas. Accord<strong>in</strong>g to 2008 data, 38% <strong>of</strong> total hectares devoted to vegetable farm<strong>in</strong>g <strong>in</strong><br />

<strong>the</strong> <strong>Mexicali</strong> <strong>Valley</strong> are used to grow green onions, mak<strong>in</strong>g it by far <strong>the</strong> most important vegetable <strong>in</strong> terms <strong>of</strong><br />

land usage. Dependable yield levels, numerous options <strong>in</strong> terms <strong>of</strong> sales (most <strong>of</strong> <strong>the</strong> producers we talked to<br />

had agreements with multiple buyers as opposed to exclusive contracts) and seem<strong>in</strong>gly low barriers to entry<br />

(based on <strong>the</strong> fact that a great many smaller players are participat<strong>in</strong>g <strong>in</strong> this market) make this an attractive<br />

option despite <strong>the</strong> fact that value generation per hectare is greater with some <strong>of</strong> <strong>the</strong> more niche vegetables.<br />

(See Table 8).<br />

Page 13