Linear Time Series Models for Stationary data - Feweb

Linear Time Series Models for Stationary data - Feweb

Linear Time Series Models for Stationary data - Feweb

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

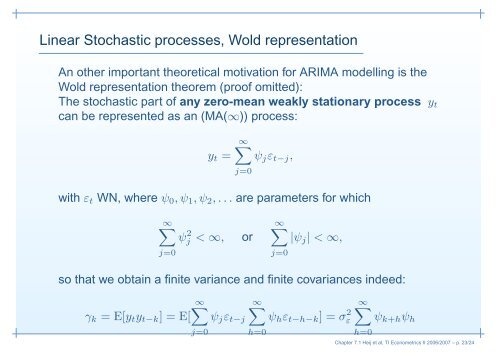

<strong>Linear</strong> Stochastic processes, Wold representation<br />

An other important theoretical motivation <strong>for</strong> ARIMA modelling is the<br />

Wold representation theorem (proof omitted):<br />

The stochastic part of any zero-mean weakly stationary process yt<br />

can be represented as an (MA(∞)) process:<br />

yt =<br />

∞<br />

j=0<br />

ψjεt−j,<br />

with εt WN, where ψ0, ψ1, ψ2, . . . are parameters <strong>for</strong> which<br />

∞<br />

j=0<br />

ψ 2 j < ∞, or<br />

∞<br />

|ψj| < ∞,<br />

so that we obtain a finite variance and finite covariances indeed:<br />

γk = E[ytyt−k] = E[<br />

∞<br />

j=0<br />

ψjεt−j<br />

∞<br />

h=0<br />

j=0<br />

ψhεt−h−k] = σ 2 ε<br />

∞<br />

h=0<br />

ψk+hψh<br />

Chapter 7.1 Heij et al, TI Econometrics II 2006/2007 – p. 23/24