Linear Time Series Models for Stationary data - Feweb

Linear Time Series Models for Stationary data - Feweb

Linear Time Series Models for Stationary data - Feweb

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

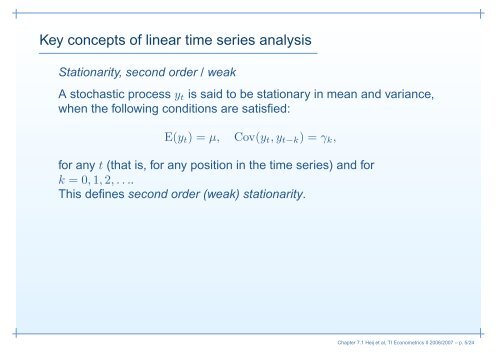

Key concepts of linear time series analysis<br />

Stationarity, second order / weak<br />

A stochastic process yt is said to be stationary in mean and variance,<br />

when the following conditions are satisfied:<br />

E(yt) = µ, Cov(yt, yt−k) = γk,<br />

<strong>for</strong> any t (that is, <strong>for</strong> any position in the time series) and <strong>for</strong><br />

k = 0, 1, 2, . . ..<br />

This defines second order (weak) stationarity.<br />

Chapter 7.1 Heij et al, TI Econometrics II 2006/2007 – p. 5/24