Framework-based IFRS teaching workshop at the BAFA Conference

Framework-based IFRS teaching workshop at the BAFA Conference

Framework-based IFRS teaching workshop at the BAFA Conference

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org<br />

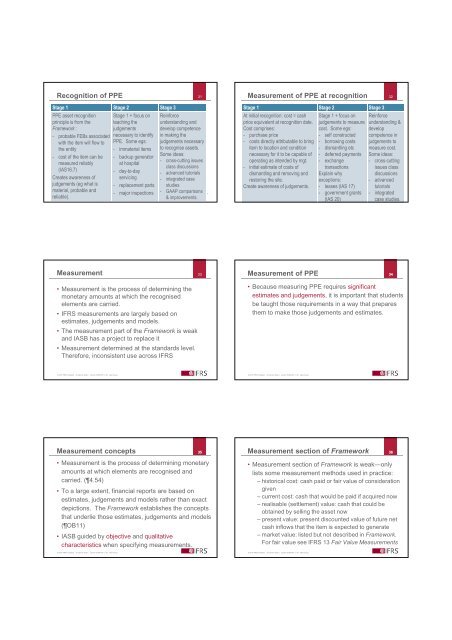

Recognition of PPE<br />

Stage 1 Stage 2 Stage 3<br />

PPE asset recognition<br />

principle is from <strong>the</strong><br />

<strong>Framework</strong> :<br />

Stage 1 + focus on<br />

<strong>teaching</strong> <strong>the</strong><br />

judgements<br />

- probable FEBs associ<strong>at</strong>ed necessary to identify<br />

with <strong>the</strong> item will flow to PPE. Some egs:<br />

<strong>the</strong> entity<br />

- imm<strong>at</strong>erial items<br />

- cost of <strong>the</strong> item can be<br />

measured reliably<br />

- backup gener<strong>at</strong>or<br />

<strong>at</strong> hospital<br />

(IAS16.7)<br />

- day-to-day<br />

Cre<strong>at</strong>es awareness of servicing<br />

judgements (eg wh<strong>at</strong> is - replacement parts<br />

m<strong>at</strong>erial, probable and<br />

reliable).<br />

- major inspections<br />

31<br />

Reinforce<br />

understanding and<br />

develop competence<br />

in making <strong>the</strong><br />

judgements necessary<br />

to recognise assets.<br />

Some ideas:<br />

- cross-cutting issues<br />

class discussions<br />

- advanced tutorials<br />

- integr<strong>at</strong>ed case<br />

studies<br />

- GAAP comparisons<br />

& improvements.<br />

Measurement of PPE <strong>at</strong> recognition<br />

Stage 1 Stage 2 Stage 3<br />

At initial recognition: cost = cash<br />

price equivalent <strong>at</strong> recognition d<strong>at</strong>e.<br />

Cost comprises:<br />

- purchase price<br />

- costs directly <strong>at</strong>tributable to bring<br />

item to loc<strong>at</strong>ion and condition<br />

necessary for it to be capable of<br />

oper<strong>at</strong>ing as intended by mgt.<br />

- initial estim<strong>at</strong>e of costs of<br />

dismantling and removing and<br />

restoring <strong>the</strong> site.<br />

Cre<strong>at</strong>e awareness of judgements.<br />

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org<br />

Stage 1 + focus on<br />

judgements to measure<br />

cost. Some egs:<br />

- self constructed<br />

- borrowing costs<br />

- dismantling etc<br />

- deferred payments<br />

- exchange<br />

transactions<br />

Explain why<br />

exceptions:<br />

- leases (IAS 17)<br />

- government grants<br />

(IAS 20)<br />

32<br />

Reinforce<br />

understanding &<br />

develop<br />

competence in<br />

judgements to<br />

measure cost.<br />

Some ideas:<br />

- cross-cutting<br />

issues class<br />

discussions<br />

- advanced<br />

tutorials<br />

- integr<strong>at</strong>ed<br />

case studies.<br />

Measurement<br />

• Measurement is <strong>the</strong> process of determining <strong>the</strong><br />

monetary amounts <strong>at</strong> which <strong>the</strong> recognised<br />

elements are carried.<br />

• <strong>IFRS</strong> measurements are largely <strong>based</strong> on<br />

estim<strong>at</strong>es, judgements and models.<br />

• The measurement part of <strong>the</strong> <strong>Framework</strong> is weak<br />

and IASB has a project to replace it<br />

• Measurement determined <strong>at</strong> <strong>the</strong> standards level.<br />

Therefore, inconsistent use across <strong>IFRS</strong><br />

33<br />

Measurement of PPE 34<br />

• Because measuring PPE requires significant<br />

estim<strong>at</strong>es and judgements, it is important th<strong>at</strong> students<br />

be taught those requirements in a way th<strong>at</strong> prepares<br />

<strong>the</strong>m to make those judgements and estim<strong>at</strong>es.<br />

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org<br />

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org<br />

Measurement concepts 35<br />

• Measurement is <strong>the</strong> process of determining monetary<br />

amounts <strong>at</strong> which elements are recognised and<br />

carried. (4.54)<br />

• To a large extent, financial reports are <strong>based</strong> on<br />

estim<strong>at</strong>es, judgements and models r<strong>at</strong>her than exact<br />

depictions. The <strong>Framework</strong> establishes <strong>the</strong> concepts<br />

th<strong>at</strong> underlie those estim<strong>at</strong>es, judgements and models<br />

(OB11)<br />

• IASB guided by objective and qualit<strong>at</strong>ive<br />

characteristics when specifying measurements.<br />

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org<br />

Measurement section of <strong>Framework</strong> 36<br />

• Measurement section of <strong>Framework</strong> is weak―only<br />

lists some measurement methods used in practice:<br />

– historical cost: cash paid or fair value of consider<strong>at</strong>ion<br />

given<br />

– current cost: cash th<strong>at</strong> would be paid if acquired now<br />

– realisable (settlement) value: cash th<strong>at</strong> could be<br />

obtained by selling <strong>the</strong> asset now<br />

– present value: present discounted value of future net<br />

cash inflows th<strong>at</strong> <strong>the</strong> item is expected to gener<strong>at</strong>e<br />

– market value: listed but not described in <strong>Framework</strong>.<br />

For fair value see <strong>IFRS</strong> 13 Fair Value Measurements<br />

© 2010 <strong>IFRS</strong> Found<strong>at</strong>ion. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org