EVI-Emerging Asia - EDHEC-Risk

EVI-Emerging Asia - EDHEC-Risk

EVI-Emerging Asia - EDHEC-Risk

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

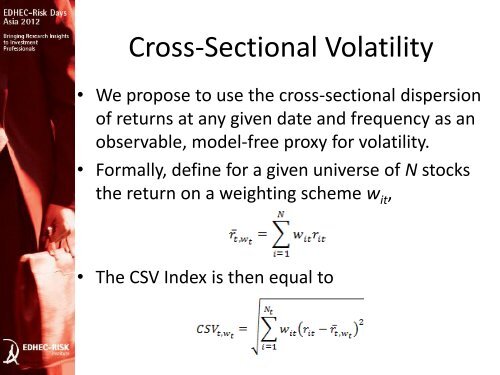

Cross-Sectional Volatility<br />

• We propose to use the cross-sectional dispersion<br />

of returns at any given date and frequency as an<br />

observable, model-free proxy for volatility.<br />

• Formally, define for a given universe of N stocks<br />

the return on a weighting scheme w it ,<br />

• The CSV Index is then equal to