EVI-Emerging Asia - EDHEC-Risk

EVI-Emerging Asia - EDHEC-Risk

EVI-Emerging Asia - EDHEC-Risk

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

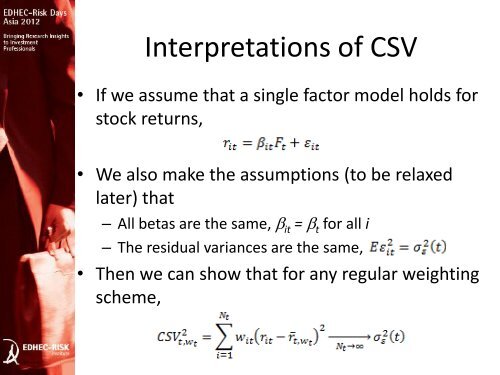

Interpretations of CSV<br />

• If we assume that a single factor model holds for<br />

stock returns,<br />

• We also make the assumptions (to be relaxed<br />

later) that<br />

– All betas are the same, it = t for all i<br />

– The residual variances are the same,<br />

• Then we can show that for any regular weighting<br />

scheme,