Silicon Solution Joint Venture, LLC - Energy Highway

Silicon Solution Joint Venture, LLC - Energy Highway

Silicon Solution Joint Venture, LLC - Energy Highway

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

US SOLAR – WHITE PAPER 24 May 2012<br />

There could be<br />

meaningful appetite to<br />

invest in solar projects if<br />

investments are<br />

structured to look like<br />

other asset classes<br />

The most telling statement about this analysis is the absence of a compelling pattern linking solar<br />

project investment to other asset classes. Investors across a broad spectrum of risk/return<br />

profiles, who are otherwise active in investments that could bear resemblance to solar projects,<br />

have largely not dipped a toe in the water, likely because the asset has not yet been 'configured'<br />

to match a familiar asset class. The findings suggest that there could be meaningful appetite if<br />

solar project investments are structured to look like other classes.<br />

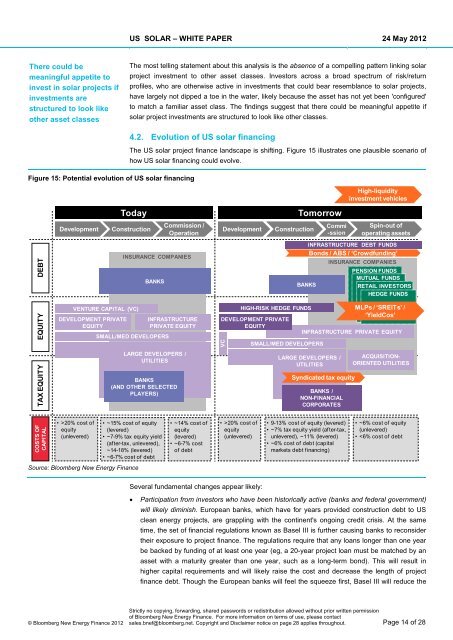

Figure 15: Potential evolution of US solar financing<br />

4.2. Evolution of US solar financing<br />

The US solar project finance landscape is shifting. Figure 15 illustrates one plausible scenario of<br />

how US solar financing could evolve.<br />

High-liquidity<br />

investment vehicles<br />

Today<br />

Tomorrow<br />

Development<br />

Construction<br />

Commission /<br />

Operation<br />

Development<br />

Construction<br />

Commi<br />

-ssion<br />

Spin-out of<br />

operating assets<br />

DEBT<br />

INSURANCE COMPANIES<br />

BANKS<br />

INFRASTRUCTURE DEBT FUNDS<br />

Bonds / ABS / ‘Crowdfunding’<br />

INSURANCE COMPANIES<br />

PENSION FUNDS<br />

MUTUAL FUNDS<br />

BANKS<br />

RETAIL INVESTORS<br />

HEDGE FUNDS<br />

EQUITY<br />

TAX EQUITY<br />

VENTURE CAPITAL (VC)<br />

DEVELOPMENT PRIVATE INFRASTRUCTURE<br />

EQUITY<br />

PRIVATE EQUITY<br />

SMALL/MED DEVELOPERS<br />

LARGE DEVELOPERS /<br />

UTILITIES<br />

BANKS<br />

(AND OTHER SELECTED<br />

PLAYERS)<br />

VC<br />

HIGH-RISK HEDGE FUNDS<br />

DEVELOPMENT PRIVATE<br />

EQUITY<br />

SMALL/MED DEVELOPERS<br />

LARGE DEVELOPERS /<br />

UTILITIES<br />

Syndicated tax equity<br />

BANKS /<br />

NON-FINANCIAL<br />

CORPORATES<br />

MLPs / ‘SREITs’ /<br />

‘YieldCos’<br />

INFRASTRUCTURE PRIVATE EQUITY<br />

ACQUISITION-<br />

ORIENTED UTILITIES<br />

COSTS OF<br />

CAPITAL<br />

• >20% cost of<br />

equity<br />

(unlevered)<br />

• ~15% cost of equity<br />

(levered)<br />

• ~7-9% tax equity yield<br />

(after-tax, unlevered),<br />

~14-18% (levered)<br />

• ~6-7% cost of debt<br />

• ~14% cost of<br />

equity<br />

(levered)<br />

• ~6-7% cost<br />

of debt<br />

• >20% cost of<br />

equity<br />

(unlevered)<br />

• 9-13% cost of equity (levered)<br />

• ~7% tax equity yield (after-tax,<br />

unlevered), ~11% (levered)<br />

• ~6% cost of debt (capital<br />

markets debt financing)<br />

• ~6% cost of equity<br />

(unlevered)<br />

•