Vol 66, No. 7 - International Technology and Engineering Educators ...

Vol 66, No. 7 - International Technology and Engineering Educators ...

Vol 66, No. 7 - International Technology and Engineering Educators ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

estimates <strong>and</strong> decisions about tool purchases, workstation<br />

design, <strong>and</strong> production flow.<br />

D ay 3—Estimating Costs U sing A pplied A lgebra<br />

An overview of the final day’s activities included a review<br />

of manufacturing engineering roles <strong>and</strong> an examination<br />

of how algebra skills are used to inform cost-related<br />

decisions in manufacturing engineering. The review<br />

consisted of questions that guided group discussion,<br />

including:<br />

1. What are the primary goals of a manufacturing engineer?<br />

How do the responsibilities <strong>and</strong> skills of a methods<br />

engineer, planning specialist, <strong>and</strong> time analyst differ?<br />

2. What strategies do engineers use to ensure the<br />

consistent <strong>and</strong> efficient manufacture of products?<br />

Discuss tooling (fixtures <strong>and</strong> templates) <strong>and</strong> a methods<br />

instruction sheet.<br />

3. What algebra concepts <strong>and</strong> procedures do time analysts<br />

employ? Discuss symbolic representation, variables,<br />

<strong>and</strong> equations.<br />

After ample time for discussion, students were reminded<br />

that a primary goal of a manufacturing company is to sell<br />

their manufactured products to make a profit. Typically,<br />

the finance department of a company oversees the balance<br />

of costs (e.g., materials, energy, labor, <strong>and</strong> equipment),<br />

market price, <strong>and</strong> profits. However, estimating, reducing,<br />

<strong>and</strong> controlling the costs of manufacturing a product lie<br />

within the purview of manufacturing engineers. So, in<br />

addition to the technical aspects of processing materials,<br />

engineers must possess the skill to apply many mathematical<br />

processes (e.g., capacity or break-even analysis) to inform<br />

cost decisions. For instance, the decisions engineers make<br />

about which equipment will be purchased for a workstation<br />

directly impact the cost of the labor required to perform the<br />

operation. Carefully planning, estimating, <strong>and</strong> controlling<br />

manufacturing costs requires engineers to employ a variety<br />

of algebra concepts <strong>and</strong> skills, including using symbolic<br />

expressions to represent costs, organizing costs into<br />

matrices, <strong>and</strong> solving equations to estimate costs.<br />

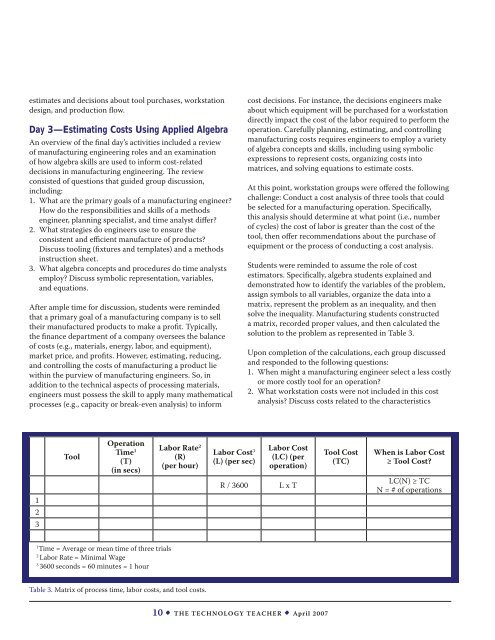

At this point, workstation groups were offered the following<br />

challenge: Conduct a cost analysis of three tools that could<br />

be selected for a manufacturing operation. Specifically,<br />

this analysis should determine at what point (i.e., number<br />

of cycles) the cost of labor is greater than the cost of the<br />

tool, then offer recommendations about the purchase of<br />

equipment or the process of conducting a cost analysis.<br />

Students were reminded to assume the role of cost<br />

estimators. Specifically, algebra students explained <strong>and</strong><br />

demonstrated how to identify the variables of the problem,<br />

assign symbols to all variables, organize the data into a<br />

matrix, represent the problem as an inequality, <strong>and</strong> then<br />

solve the inequality. Manufacturing students constructed<br />

a matrix, recorded proper values, <strong>and</strong> then calculated the<br />

solution to the problem as represented in Table 3.<br />

Upon completion of the calculations, each group discussed<br />

<strong>and</strong> responded to the following questions:<br />

1. When might a manufacturing engineer select a less costly<br />

or more costly tool for an operation?<br />

2. What workstation costs were not included in this cost<br />

analysis? Discuss costs related to the characteristics<br />

Tool<br />

Operation<br />

Time 1<br />

(T)<br />

(in secs)<br />

Labor Rate 2<br />

(R)<br />

(per hour)<br />

Labor Cost 3<br />

(L) (per sec)<br />

Labor Cost<br />

(LC) (per<br />

operation)<br />

Tool Cost<br />

(TC)<br />

When is Labor Cost<br />

≥ Tool Cost?<br />

1<br />

2<br />

3<br />

R / 3600<br />

L x T<br />

LC(N) ≥ TC<br />

N = # of operations<br />

1<br />

Time = Average or mean time of three trials<br />

2<br />

Labor Rate = Minimal Wage<br />

3<br />

3600 seconds = 60 minutes = 1 hour<br />

Table 3. Matrix of process time, labor costs, <strong>and</strong> tool costs.<br />

10 • The <strong>Technology</strong> Teacher • April 2007