CAPITAL STRUCTURE AND THE COST OF CAPITAL External ...

CAPITAL STRUCTURE AND THE COST OF CAPITAL External ...

CAPITAL STRUCTURE AND THE COST OF CAPITAL External ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>CAPITAL</strong> <strong>STRUCTURE</strong> <strong>AND</strong> <strong>THE</strong> <strong>COST</strong> <strong>OF</strong> <strong>CAPITAL</strong><br />

Direct all comments, remarks, questions to:<br />

Calin Valsan<br />

Williams School of Business<br />

Bishop's University<br />

cvalsan-at-ubishops-dot-ca<br />

<strong>External</strong> financing involves raising capital to finance the assets of the firm. The most important decision to make is whether<br />

to raise debt or equity. This decision impacts the relative proportions of debt and equity. In usual finance vernacular this is<br />

referred to as capital structure. To tackle this problem we need to set out the relevant criteria on which to base our choice.<br />

The traditional decision criterion has been the long-term wealth of shareholders, which is contingent on the fair market<br />

value of the firm. Choosing between external equity and debt is thus a question of maximizing the present value of firm's<br />

cash flows.<br />

The present value of firm's cash flow depends in turn on the absolute magnitude of annual cash flows and on their volatility.<br />

Riskiness is the ultimate factor in deciding the cost of procuring the capital needed to produce those cash flows.<br />

The riskier the cash flow, the more expensive the cost of obtaining outside financing. It stands to reason that in order to<br />

maximize the market value of the firm, the best possible capital structure has to maximize expected cash flows and<br />

minimize the cost of procuring external financing. This cost is simply called the cost of capital, and has at least two<br />

components: the cost of equity and the cost of debt (for companies that issue preferred shares, one has to account for the<br />

cost of preferred shares as well).<br />

One has to be careful not to confuse the cost of capital with the cost of issuing capital. The cost of capital is simply a fair<br />

financial compensation owed to the providers of capital and is proportional to the riskiness of their respective financial<br />

claims. The cost of issuing capital is made of all direct and indirect expenses incurred by the firm in order to bring the bonds<br />

and shares in the hands of claimholders: creditors and shareholders. The cost of issuing capital is also referred to as flotation<br />

cost and is at its very heart an intermediation cost: commission, fees, spreads, money left on the table, etc. These costs are<br />

paid to underwriters, regulators, lawyers, accountants, etc.<br />

The cost of external equity is larger than the cost of debt because equity is riskier than debt. The riskiness of both claims,<br />

however, is contingent on the overall riskiness of the firm. The overall riskiness of the firm is an aggregate of business risk<br />

and financial risk. Business risk is an unavoidable risk faced by any enterprise in the course of conducting its operations. Its<br />

magnitude is given by the specificity of firm's assets. An airline has a different business risk than that of a grocery store. A<br />

pharmaceutical company has a different business risk than that of a bank. Besides the nature of assets, other factors, such as<br />

regulation, exchange rates, morality etc., play an important role in shaping the environment, and hence the risk to which the<br />

firm is exposed. In addition to business risk, firms face an additional type of risk - financial risk- given by the manner in<br />

which they finance their operations. The more debt, the higher the financial risk. Debt adds more risk, because interests<br />

payments represent a contractual, firm commitment to pay predetermined amounts at predetermined time periods. Failure to<br />

fulfill these contractual commitments results in financial distress and failure.<br />

It is therefore customary to treat capital structure as a case of debt financing. We start by assuming an all-equity firm and we<br />

ask what happens to its market value if we substitute some of its equity with debt. Or, we start with a leveraged firm and we<br />

ask what happens to its market value if we substitute its outstanding debt with equity. In order to answer these pseudopractical<br />

questions, we need to understand, as already explained, two things: how cash flow change, and how the cost of<br />

capital change. While determining the change in cash flow appears predictable to a certain extent, estimating the cost of<br />

capital is a daunting task. Of the two main types of capital, the cost of debt is easier to estimate. We simply observe the<br />

interest a firm pays on its loans or the coupon it pays on its bonds. Banks and creditors usually do a fair job at estimating<br />

the riskiness of corporate borrowing. Of course, they all can be wrong at times, but in general the cash flow generated by<br />

debt is reasonably predictable because it is made of fixed payments at fixed intervals. Firms have no choice but to pay their<br />

financial obligations as they come due. The hard part is to estimate the probability the firm will default; firms with solid<br />

solvency ratios borrow at low rates, firms with acceptable solvency ratios borrow at higher rates, and firms on the verge of<br />

financial distress usually do not have access to debt financing. In general, the higher the level of financial leverage, the<br />

higher the marginal interest rate at which the firm can acquire new debt. This follows from the fact that more debt means<br />

more financial risk.<br />

The cost of equity is a whole different story. The most accurate thing we can say about the cost of equity (the required rate<br />

1

of return on equity) is that it must be larger than the marginal (i.e., highest) interest rate at which the firm is able to borrow.<br />

By how much? One is at a loss to quantify this premium for lack of a reliable return generating model, that is, a functional<br />

model measuring how return varies with risk. The most notable attempt to produce a return generating model is the Capital<br />

Asset Pricing Model (CAPM). At the beginning, the CAPM was hailed as a breakthrough in modern finance. As it stands<br />

now, the model has been adopted as the default approach to estimating required return by scores of academics and<br />

practitioners alike, in spite of its many apparent flaws. The CAPM is a very elegant and seducing mathematical model, yet<br />

its validity is more a question of metaphysics than of reality. As a practical tool for estimating required returns, the CAPM is<br />

quite unhelpful.<br />

A possible contender for calculating the cost of equity is the dividend growth model. The dividend growth model relies on<br />

estimating the stream of future dividend payments., and comparing it to the current market price of the stock. As a practical<br />

tool, it too, has many debilitating flaws. For one, it provides no mechanism for accounting for risk. In addition, it forces us<br />

to assume the stock is already correctly priced, which in many instances is a no starter. Since capital structure is an exercise<br />

in valuation, this assumption defeats the purpose of the entire process of searching for a fair market value.<br />

The only one left standing is the initial heuristic approach of adding a risk premium to the highest observed interest rate paid<br />

by the firm in order to come up with a rudimentary estimation for the cost of equity. It is indeed a very crude approach,<br />

relying on guesswork and subjective approximation, but at least it does not have the pretense of being accurate and<br />

scientific. In spite of its disheveled appearance, this ad-hoc method is in fact less arbitrary than the more mathematically<br />

sophisticated methods, which are metaphysically enticing, yet seriously lacking in practical relevance.<br />

When we allow the cost of equity to follow the cost of debt, we end up with a complex relationship between financial<br />

leverage and market value. When markets are optimistic and tolerate high risk - either because of misperception or<br />

overconfidence - the relationship between leverage and total market value is approximately flat, edging up slightly as the<br />

total debt ratio approaches 100%. When markets are paranoid and hardly tolerate any credit risk, the relation become<br />

humpback-shaped, increasing for very low levels of debt, and then dropping vertiginously as total debt ratio approaches<br />

100%.<br />

Implicit in this valuation approach is an average cost of capital that can be used to estimate the fair total market value of the<br />

firm by discounting its total cash flows. The calculation of this average cost, however, is contingent on estimating the fair<br />

market weights of equity and debt in the fair total market value of the firm.<br />

The complex valuation profile described earlier owes to the fact that - contrary to what the neo-classical theory contends 1 -<br />

there is no true separation between the investment and the financing decision of the firm. The behavior of, and the options<br />

available to the financial manager are partially contingent on his financing choices. The neo-classical theory sees the world<br />

as a giant clockwork, with well defined and delineated parts and functions, in which various outcomes are observed to flow<br />

linearly from cause A to effect B, while the rest is of the world is graciously suspended in limbo.<br />

The holistic interpretation offered here as a counterweight to the neo-classical model, views the various variables populating<br />

the system as deeply interconnected and banding together in complex, simultaneous interactions, subject to measurement<br />

indeterminacy. Any attempt at measuring a variable in isolation is either doomed or seriously distorted. The price to pay for<br />

this more realistic stance is significant: while one can provide a credible, although approximate description of what might be<br />

going on, one is at a loss to generate normative judgments. One has to rely more on the business savvy, the instinct and the<br />

acumen of the entrepreneur than on the sophistication of mathematical models. This contention has far reaching<br />

implications as far as market regulation goes: if we cannot formulate operational models of financing choices, in which<br />

causal relationships are well specified, then we cannot formulate regulation that is fair and effective. The most effective type<br />

of regulation is probably limited to the one attempting to establish and reinforce trust among market participants and<br />

decision makers.<br />

1 Fisher, Irving (1930) The Theory of Interest: As determined by impatience to spend income and opportunity to invest it. 1954 reprint, New York: Kelley<br />

and Millman.<br />

2

Debt financing : The case of Toy Inc.<br />

We start by trying to estimate the impact of debt financing on the cash flows of the firm. The following simplified example<br />

should give us a good idea of what is going on. Consider the case of Toy Inc., partially financed with debt. Let us assume<br />

that there are two possible outcomes next year: sales can go up by 20%, or sales can go down by 20%. Each scenario has an<br />

equal chance of occurring. Furthermore, let us assume that costs grow (decreases) only half as fast as sales. The pro-forma<br />

income statement shows what happens in each case. When sales slump, Toy Inc. incurs a loss. EBIT and net income turn<br />

negative. Fortunately, the firm still has enough liquidity to pay its obligations and to dampen the drop. For now, the<br />

company is able to survive with minor bruises; its assets, however, will drop, reflecting the loss. If sales increase, the<br />

bulging profits will be associated with an increase in total assets.<br />

Toy Inc.: Pro-forma income statement<br />

Today Next year: sales up 20%, costs up 10% Next year: sales down 20%, costs down 10%<br />

Sales $5,000.00 $6,000.00 $4,000.00<br />

(Costs) $3,500.00 $3,850.00 $3,150.00<br />

(Depreciation) $1,000.00 $1,000.00 $1,000.00<br />

EBIT $500.00 $1,150.00 -$150.00<br />

(Interest) $80.75 $80.75 $80.75<br />

EBT $419.25 $1,069.25 -$230.75<br />

(Tax) $142.55 $363.55 $0.00<br />

Net income $276.71 $705.71 -$230.75<br />

Addition to RE $179.86 $458.71 -$230.75<br />

Dividend $96.85 $247.00 $0.00<br />

Toy Inc.: Pro-forma balance sheet<br />

Today<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Today<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Cash $100.00 $1,468.71 $869.25 Accounts payable $300.00 $300.00 $300.00<br />

Inventory $500.00 $550.00 $500.00 Notes payable $400.00 $400.00 $400.00<br />

A/R $400.00 $440.00 $400.00 Total current liabilities $700.00 $700.00 $700.00<br />

Current assets $1,000.00 $2,458.71 $1,769.25<br />

Long-term debt $1,500.00 $1,500.00 $1,500.00<br />

Gross fixed assets $3,000.00 $3,000.00 $3,000.00 Other long-term $0.00 $0.00 $0.00<br />

Depreciation $1,000.00 $2,000.00 $2,000.00 Outstanding shares $1,120.14 $1,120.14 $1,120.14<br />

Net fixed assets $2,000.00 $1,000.00 $1,000.00 Retained earnings $179.86 $638.57 -$50.89<br />

Other assets $500.00 $500.00 $500.00 Owner's equity $1,300.00 $1,758.71 $1,069.25<br />

Total assets $3,500.00 $3,958.71 $3,269.25 Total liabilities and equity $3,500.00 $3,958.71 $3,269.25<br />

3

Financial ratios reflect the fortunes of the company. When sales are up, all solvency and profitability ratios are up as well.<br />

Earnings per share, dividend per share, and book value of equity are all up. It is not possible to estimate the dividend yield,<br />

simply because we don't know how the stock price will change if earnings increase. It will probably go up as well, but by<br />

how much, it is anyone's guess.<br />

When sales are down, solvency and profitability ratios are down as well. In fact, profitability ratios turn negative, due to the<br />

loss. It is likely that the stock price will decrease too, but since Toy Inc. will pay no dividend, we can obviously ascertain a<br />

zero dividend yield.<br />

Toy Inc.: Selected ratios<br />

Today Next year: sales up 20%, costs up 10% Next year: sales down 20%, costs down 10%<br />

TAT 1.43 3.51 1.22<br />

FAT 2.50 2.73 4.00<br />

D/E 1.69 1.25 2.06<br />

Total debt ratio 0.63 0.56 0.67<br />

LT debt ratio 0.43 0.38 0.46<br />

TIE 6.19 14.24 -1.86<br />

Cash coverage 18.58 26.63 10.53<br />

Profit margin 5.53% 11.76% -5.77%<br />

ROA 7.91% 17.83% -7.06%<br />

ROE 21.29% 40.13% -21.58%<br />

Dividend per share $0.97 $2.47 $0.00<br />

EPS $2.77 $7.06 -$2.31<br />

Book value per share $13.00 $17.59 $10.69<br />

Dividend yield 3.87% ? 0.00%<br />

Cash flows follow the fortunes of earnings as well. When earnings are up, we see a significant increase in total cash flows,<br />

due to a larger dividend payment. When earnings are down, cash flows retreat to the bare minimum represented by interest<br />

payments.<br />

Toy Inc.: Cash flows to claimholders<br />

Today Next year: sales up 20%, costs up 10% Next year: sales down 20%, costs down 10%<br />

CF to creditors $80.75 $80.75 $80.75<br />

CF to shareholders $96.85 $247.00 $0.00<br />

CF from assets $177.60 $327.75 $80.75<br />

4

Debt financing and Toy Inc. in a parallel universe<br />

Let us now imagine a parallel universe in which everything is the same as in ours, except that we have magically substituted<br />

all the debt of Toy Inc. with equity. In this parallel universe, Toy Inc. is entirely equity financed, and we will henceforth call<br />

it all-equity Toy Inc. The pro-forma financial statements of all-equity Toy Inc. are very similar to those of Toy Inc. As in the<br />

previous case, a drop in sales results in a loss and entails a decrease in total assets.<br />

All-equity Toy Inc.: Pro-forma income statement<br />

Today Next year: sales up 20%, costs up 10% Next year: sales down 20%, costs down 10%<br />

Sales $5,000.00 $6,000.00 $4,000.00<br />

(Costs) $3,500.00 $3,850.00 $3,150.00<br />

(Depreciation) $1,000.00 $1,000.00 $1,000.00<br />

EBIT $500.00 $1,150.00 -$150.00<br />

(Interest) $0.00 $0.00 $0.00<br />

EBT $500.00 $1,150.00 -$150.00<br />

(Tax) $170.00 $391.00 $0.00<br />

Net income $330.00 $759.00 -$150.00<br />

Addition to RE $214.50 $493.35 -$150.00<br />

Dividend $115.50 $265.65 $0.00<br />

All-equity Toy Inc.: Pro-forma balance sheet<br />

Today<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Today<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Cash $100.00 $1,503.35 $950.00 A/P $0.00 $0.00 $0.00<br />

Inventory $500.00 $550.00 $500.00 N/P $0.00 $0.00 $0.00<br />

A/R $400.00 $440.00 $400.00 Current liabilities $0.00 $0.00 $0.00<br />

Current assets $1,000.00 $2,493.35 $1,850.00<br />

Long-term debt $0.00 $0.00 $0.00<br />

Gross fixed assets $3,000.00 $3,000.00 $3,000.00 Other long-term $0.00 $0.00 $0.00<br />

Depreciation $1,000.00 $2,000.00 $2,000.00 Outstanding shares $3,285.50 $3,285.50 $3,285.50<br />

Net fixed assets $2,000.00 $1,000.00 $1,000.00 Retained earnings $214.50 $707.85 $64.50<br />

Other assets $500.00 $500.00 $500.00 Owner's equity $3,500.00 $3,993.35 $3,350.00<br />

Total assets $3,500.00 $3,993.35 $3,350.00 Total L&E $3,500.00 $3,993.35 $3,350.00<br />

5

Financial ratios follow the trajectory of sales and earnings. When sales are up, all ratios are improving and cash flow grows<br />

larger. When sales are down, all ratios get weaker and cash flow drops to zero, as there is no money left for dividend<br />

payment. Unlike Toy Inc., the cash flow of all-equity Toy Inc. is only made of dividend payments. When earnings are<br />

growing, so does the cash flow. When incurring a loss, all-equity Toy's Inc.'s cash flow dries up.<br />

All-equity Toy Inc.: Selected ratios<br />

Today Next year: sales up 20%, costs up 10%<br />

Next year: sales down 20%, costs<br />

down 10%<br />

TAT 1.43 1.50 1.19<br />

FAT 2.50 6.00 4.00<br />

D/E 0.00 0.00 0.00<br />

Total debt ratio 0.00 0.00 0.00<br />

LT debt ratio 0.00 0.00 0.00<br />

TIE 0.00 0.00 0.00<br />

Cash coverage 0.00 0.00 0.00<br />

Profit margin 6.60% 12.65% -3.75%<br />

ROA 9.43% 19.01% -4.48%<br />

ROE 9.43% 19.01% -4.48%<br />

Dividend per share $1.16 $2.66 $0.00<br />

EPS $3.30 $7.59 -$1.50<br />

Book value per share $35.00 $39.93 $33.50<br />

Dividend yield ? ? 0%<br />

All-equity Toy Inc.: Cash flows to claimholders<br />

Today Next year: sales up 20%, costs up 10% Next year: sales down 20%, costs down 10%<br />

CF to creditors $0.00 $0.00 $0.00<br />

CF to shareholders $115.50 $265.65 $0.00<br />

CF from assets $115.50 $265.65 $0.00<br />

6

Debt financing in parallel universes: Toy Inc. and all-equity Toy Inc. side by side<br />

A cursory inspection of Toy Inc. and all-equity Toy Inc. shows very similar tendencies in financial ratios and cash flows. To<br />

get a more revealing picture we need to analyze them side by side. We start with their current standing and we see that most<br />

differences are rather subtle (except for the differences due to the lack of leverage, that is). All-equity Toy Inc. has a slightly<br />

higher profit margin and return on assets (no interest payments to reduce earnings), yet it boasts a lower return on equity.<br />

Cash flow to shareholders is higher for all-equity Toy Inc., yet, total cash flow is higher for Toy Inc. This is so because total<br />

cash flow of all-equity Toy Inc. is made only of dividend payments, while that of Toy Inc. is made of dividend payments<br />

and interest payments.<br />

Parallel universes: Toy Inc. and all-equity Toy Inc.<br />

All equity Toy Inc.<br />

Toy Inc.<br />

Sales $5,000 $5,000<br />

Net income $330 $276.71<br />

Dividend $115.50 $96.85<br />

Total assets $3,500 $3,500<br />

TAT 1.43 1.43<br />

FAT 2.50 2.50<br />

D/E 0.00 1.69<br />

Total debt ratio 0.00 0.63<br />

LT debt ratio 0.00 0.43<br />

TIE 0.00 6.19<br />

Cash coverage 0.00 18.58<br />

Profit margin 6.60% 5.53%<br />

ROA 9.43% 7.91%<br />

ROE 9.43% 21.29%<br />

Dividend per share $1.16 $0.97<br />

EPS $3.30 $2.77<br />

Book value per share $35.00 $13.00<br />

Dividend yield ? 3.87%<br />

CF to creditors $0.00 $80.75<br />

CF to shareholders $115.50 $96.85<br />

CF from assets $115.50 $177.60<br />

7

The differences between the two parallel universes appear more manifest when analyzed dynamically. The main points can<br />

be summarized as follows:<br />

• Average profit margin is lower, but profit margin volatility is higher for Toy Inc.<br />

• Average ROA is lower, but ROA volatility is higher for Toy Inc.<br />

• Average ROE is higher and ROE volatility is higher for Toy Inc.<br />

• Total cash flows are larger for Toy Inc. (the lower volatility here is somewhat misleading, as we have considered<br />

Toy Inc. is able to make interests payments regardless of the growth outcome)<br />

Parallel universes: Toy Inc. and all-equity Toy Inc. under two growth scenarios<br />

All equity Toy Inc.<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

All equity Toy Inc.<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Average<br />

Standard<br />

deviation<br />

Toy Inc.<br />

Next year:<br />

sales up 20%,<br />

costs up 10%<br />

Toy Inc.<br />

Next year:<br />

sales down 20%,<br />

costs down 10%<br />

Average<br />

Standard<br />

deviation<br />

Sales $6,000.00 $4,000.00 $5,000.00 $1,414.21 $6,000.00 $4,000.00 $5,000.00 $1,414.21<br />

Net income $759.00 -$150.00 $304.50 $642.76 $705.71 -$230.75 $237.48 $662.18<br />

Dividend $265.65 $0.00 $132.83 $187.84 $247.00 $0.00 $123.50 $174.66<br />

Total assets $3,993.35 $3,350.00 $3,671.68 $454.92 $3,958.71 $3,269.25 $3,613.98 $487.52<br />

TAT 1.50 1.19 1.35 0.22 3.51 1.22 2.37 1.62<br />

FAT 6.00 4.00 5 1.41 2.73 4.00 3.37 0.9<br />

D/E 0.00 0.00 0 0 1.25 2.06 1.66 0.57<br />

Total debt ratio 0.00 0.00 0 0 0.56 0.67 0.62 0.08<br />

LT debt ratio 0.00 0.00 0 0 0.38 0.46 0.42 0.06<br />

TIE 0.00 0.00 0 0 14.24 -1.86 6.19 11.38<br />

Cash coverage 0.00 0.00 0 0 26.63 10.53 18.58 11.38<br />

Profit margin 12.65% -3.75% 4.45% 11.60% 11.76% -5.77% 3.00% 12.40%<br />

ROA 19.01% -4.48% 7.27% 16.61% 17.83% -7.06% 5.39% 17.60%<br />

ROE 19.01% -4.48% 7.27% 16.61% 40.13% -21.58% 9.28% 43.64%<br />

Dividend per share $2.66 $0.00 $1.33 $1.88 $2.47 $0.00 $1.24 $1.75<br />

EPS $7.59 -$1.50 $3.05 $6.43 $7.06 -$2.31 $2.38 $6.63<br />

Book value per share $39.93 $33.50 $36.72 $4.55 $17.59 $10.69 $14.14 $4.88<br />

Dividend yield ? 0% n/a n/a ? 0.00% n/a n/a<br />

CF to creditors $0.00 $0.00 $0.00 $0.00 $80.75 $80.75 $80.75 $0.00<br />

CF to shareholders $265.65 $0.00 $132.83 $187.84 $247.00 $0.00 $123.50 $174.66<br />

CF from assets $265.65 $0.00 $132.83 $187.84 $327.75 $80.75 $204.25 $174.66<br />

So far we have considered only a relatively mild downturn in sales and earnings. Both Toy Inc. and all-equity Toy Inc.<br />

appear to survive it relatively unscathed. It is time we considered a more dramatic scenario that will reveal some of the more<br />

dramatic consequences of borrowing.<br />

8

Parallel universes: A severe downturn<br />

Let us imagine a severe drop in sales and how it affects Toy Inc. and all-equity Toy Inc. Consider an 80% decrease in sales<br />

that results in a massive loss of over $2,500. The loss is so dramatic that assets plummet from $3,500 to $1,100.<br />

Pro-forma income statement of Toy Inc. under a severe market downturn scenario<br />

Today<br />

Next year<br />

Sales $5,000.00 $1,000.00<br />

(Costs) $3,500.00 $2,450.00<br />

(Depreciation) $1,000.00 $1,000.00<br />

EBIT $500.00 -$2,450.00<br />

(Interest) $80.75 $80.75<br />

EBT $419.25 -$2,530.75<br />

(Tax) $142.55 $0.00<br />

Net income $276.71 -$2,530.75<br />

Addition to RE $179.86 -$2,530.75<br />

Dividend $96.85 $0.00<br />

Pro-forma balance sheet of Toy Inc. under a severe market downturn scenario<br />

Today Next year Today Next year<br />

Cash $100.00 $0.00 A/P $300.00 $430.75<br />

Inventory $500.00 $100.00 N/P $400.00 $400.00<br />

A/R $400.00 $0.00 Current liabilities $700.00 $830.75<br />

Current assets $1,000.00 $100.00<br />

Long-term debt $1,500.00 $1,500.00<br />

Gross fixed assets $3,000.00 $3,000.00 Other long-term $0.00 $0.00<br />

Depreciation $1,000.00 $2,000.00 Outstanding shares $1,120.14 $1,120.14<br />

Net fixed assets $2,000.00 $1,000.00 Retained earnings $179.86 -$2,350.89<br />

Other assets $500.00 $0.00 Owner's equity $1,300.00 -$1,230.75<br />

Total assets $3,500.00 $1,100.00 Total L&E $3,500.00 $1,100.00<br />

We estimate a cash coverage ratio of -18 for next year. The company can try to increase its accounts payable, use up all<br />

strategic cash reserves to pay its employees, write-off accounts receivables, but in the end, Toy Inc still does not have<br />

enough money left to cover its interest obligation - at this point in time bankruptcy is most likely declared. Notice how,<br />

under the burden of the loss, even owner's equity becomes negative. This equity deficit is a bad omen: although book value<br />

of equity reflects only historical costs, it signals the firm might not be viable anymore. It is quite possible that the market<br />

value of assets could be less than that of debt obligations, case in which liquidation would result in a partial loss to creditors<br />

and a total loss to shareholders.<br />

9

Consider now what happens to all-equity Toy Inc. Even though the loss is still staggering it does not necessarily spell the<br />

demise of the company, at least not yet. The company will again try to use accounts payable, tap into its strategic cash<br />

reserves, write-off account receivables, etc., but fortunately, here there is no need to worry about paying interest.<br />

For the time being the company has wiggled its way out of a tight spot. It has another chance to pick themselves up and try<br />

again in one year's time. It could also raise new equity to replenish cash and prepare for the eventuality that the years ahead<br />

would again be bad. Of course, the company cannot operate like this indefinitely (unless you're a third generation<br />

entrepreneur sitting on top of a family fortune waiting to be squandered), but for the particular period under analysis, allequity<br />

Toy Inc. need not go bankrupt like Toy Inc.<br />

Pro-forma income statement of all-equity Toy Inc. under a severe market downturn scenario<br />

Today<br />

Next year<br />

Sales $5,000.00 $1,000.00<br />

(Costs) $3,500.00 $2,450.00<br />

(Depreciation) $1,000.00 $1,000.00<br />

EBIT $500.00 -$2,450.00<br />

(Interest) $0.00 $0.00<br />

EBT $500.00 -$2,450.00<br />

(Tax) $170.00 $0.00<br />

Net income $330.00 -$2,450.00<br />

Addition to RE $214.50 -$2,450.00<br />

Dividend $115.50 $0.00<br />

Pro-forma balance sheet of all-equity Toy Inc. under a severe market downturn scenario<br />

Today Next year Today Next year<br />

Cash $100.00 $0.00 A/P $300.00 $50.00<br />

Inventory $500.00 $100.00 N/P $400.00 $0.00<br />

A/R $400.00 $0.00 Current liabilities $700.00 $50.00<br />

Current assets $1,000.00 $100.00<br />

Long-term debt $1,500.00 $0.00<br />

Gross fixed<br />

assets<br />

$3,000.00 $3,000.00 Other long-term $0.00 $0.00<br />

Depreciation $1,000.00 $2,000.00 Outstanding shares $1,120.14 $3,285.50<br />

Net fixed assets $2,000.00 $1,000.00 Retained earnings $179.86 -$2,235.50<br />

Other assets $500.00 $0.00 Owner's equity $1,300.00 $1,050.00<br />

Total assets $3,500.00 $1,100.00 Total L&E $3,500.00 $1,100.00<br />

10

The Holy Grail of finance and the cash cow<br />

Our analysis has established so far that Toy Inc. appears to reward its shareholders with higher returns than all-equity Toy<br />

Inc. , but these returns are also more volatile. At the same time, Toy Inc. also produces larger total cash flows. We examined<br />

other financial ratios and found to display similar trends. One thing that was left hanging was the issue of dividend yield.<br />

Here, we are asking an apparently innocuous question: In a parallel universe, what is the dividend yield of all-equity Toy<br />

Inc. ? What would be the price of its stock? To answer this question we need to know the valuation of all-equity Toy Inc.:<br />

Dividend yield = Current dividend/Current stock price<br />

Based on what we found until now, we have good reasons to believe that the market value of all-equity Toy Inc. would be<br />

different than that of Toy Inc. Consider this:<br />

P = PV(cash flows)<br />

P = CF1/(1+ r) + CF2/(1+r) 2 + CF3/(1+r) 3 + .......etc<br />

As already acknowledged, cash flow is not the same in the two parallel universes. Cash flow to shareholders is larger for the<br />

all-equity Toy Inc. However, total cash flow is larger for the leveraged Toy Inc.<br />

Total cash flow of all-equity Toy Inc. = Cash flow to shareholders<br />

Total cash flow of levered Toy Inc. = Cash flow to shareholders + Cash flow to creditors<br />

Return on equity volatility is not the same, as calculated earlier. It is smaller for all-equity Toy Inc. and larger for Toy Inc.<br />

The same can be said about total cash flow. The volatility of total cash flow of Toy Inc. is larger, when we take into account<br />

the possibility of Toy Inc. going bankrupt:<br />

Variance (ROE) all-equity Toy Inc. < Variance (ROE) levered Toy Inc.<br />

Variance (Total CF) all-equity Toy Inc. < Variance (Total CF) levered Toy Inc. (when bankruptcy is possible)<br />

Unquestionably, Toy Inc is the riskier company. It has an added layer of risk. An extra risk dimension. The overall riskiness<br />

of the firm is the sum of business risk and financial risk. Business risk is an unavoidable risk faced by any enterprise in the<br />

course of conducting its operations. Its magnitude is given by the specific nature of its assets. An airline has a different<br />

business risk than that of a grocery store. A pharmaceutical company has a different business risk than that of a bank. A steel<br />

mill has a different business risk than a hedge fund. Besides the nature of assets, other factors, such as regulation, exchange<br />

rates, inflation, wages, transportation costs, climate, and even morality play an important role in shaping the environment,<br />

and hence the risk to which the firm is exposed. In addition to business risk, firms face an additional form of risk- financial<br />

risk- contingent on the manner in which assets are financed. The more debt, the higher the financial risk. Debt adds more<br />

risk, because interests payments represent a contractual, firm commitment to pay predetermined amounts at predetermined<br />

time periods. Failure to fulfill these contractual commitments results in financial distress and failure. We have already<br />

concluded that total cash flow has become larger for Toy Inc, yet also more volatile: if in any given year sales crash<br />

unexpectedly, Toy Inc might not be able to make interest payments and would have to file for bankruptcy protection. To<br />

summarize, financial risk has two important dimensions:<br />

(i) Extra volatility in equity returns and cash flows<br />

(ii) The real possibility that the firm could go bankrupt if unable to pay its financial obligations<br />

It follows that the risk faced by the two companies in parallel universes is:<br />

Total risk of all-equity Toy Inc = Business risk<br />

Total risk of levered Toy Inc. = Business risk + Financial risk<br />

The logical conclusion of this discussion is that the equity of Toy Inc. needs a higher discount rate to compensate for the<br />

additional financial risk. The hard question, however, is this: how much more return would the market require in order to<br />

compensate for financial risk? To answer, we have to know how return varies with risk. This is the holy grail of modern<br />

finance, a question that every investor is grappling with.<br />

11

Enter the cash cow. A cash cow is a mature company, without great growth prospects, generating a predictable and steady<br />

stream of dividends year in and year out. Let us imagine Toy Inc. as a the proverbial cash cow. This current year, Toy Inc.<br />

paid $96.85 to its shareholders and $80.75 to its creditors. If we assume no changes in sales, next year's cash flow will be<br />

the same. Toy Inc.'s going discount rate on equity is implicitly given by the current market price. At the present time, the<br />

stock of Toy Inc is selling for $25/share.<br />

$25 = $0.97/r<br />

r = $0.97/$25 = 3.8%<br />

Is this number a fair discount rate? That is, if we buy the stock, are we fairly rewarded in making a return in the<br />

neighborhood of 4% (plus whatever expected growth rate in earnings), without being unrealistically optimistic about the<br />

future? Is the current dividend stream likely to prevail in the future? Is the volatility of this dividend payment reflected in<br />

the current market price? Should we embrace 4% as such, just because it prevails in the market? What if the market is<br />

replete with irrational exuberance or blinded by fear? Should we follow it unconditionally or attempt to pass our own<br />

judgment?<br />

Suppose tomorrow the price drops to $18. What would it mean? Several possible things:<br />

It could be that the going rate has been revised upward to 5.4% amid fears of higher volatility in the future:<br />

$18 = $0.97/0.054 (approximately)<br />

Or, it could be that risk is expected to remain the same, but the expected amount of cash to be paid in the future to<br />

shareholders is down to $0.68 per share:<br />

$18 = $0.68/0.038<br />

Or, it could be that both risk expectations and cash flows expectations have changed at the same time, such that:<br />

or<br />

or<br />

$18 = $1.5/0.083<br />

$18 = $1.6/0.088<br />

$18 = $1.9/0.105<br />

or........an infinity of other possibilities<br />

In fact we would never know for sure how the valuation of the market has changed exactly. It could be driven by fear and<br />

panic, by wisdom, by ignorance, by savvy, by greed, or by all of the above. The truth is, crowds are fickle and whimsical.<br />

Investors are possessed by strong emotions and many a times exhibit herding behavior. Following the ups and down of the<br />

market is maddening and stressful; even if we trust the market is always right, we are bound to be taken by surprise, to<br />

always lag one step behind. Ideally, we want our own formula to tell us whether the current stock price is fair. But how can<br />

we catch a glimpse of it? This is the big question. Every discipline grapples with its own deep questions. Philosophers ask<br />

why is there something instead of nothing; physicists try to find a formula that would explain gravity, electromagnetism and<br />

elementary forces in a unified way; mathematicians compare infinities and count prime numbers; engineers want to build an<br />

engine that would run on light, wind, water, or whatever is dirt cheap but not dirty; doctors want to cure cancer and other<br />

serious illnesses; financial economists, however, want a formula to tell them how much to pay for an asset that will<br />

generate an uncertain payoff in the future. We want to know how much to pay for something that is not yet in existence, but<br />

might come into existence in the future in a variety of ways. It sounds as though we want a crystal ball. Where should we<br />

start?<br />

12

The concept of cost of capital<br />

The cost of capital is the required rate of return that makes investors willing to provide capital. The economic significance<br />

of the cost of capital is straightforward: it is used to discount expected cash flows in order to determine the fair market value<br />

of the firm. The cost of capital has two components: the cost of equity and the cost of debt (for companies that issue<br />

preferred shares, one has to account for the cost of preferred shares as well). As already mentioned at the beginning of this<br />

section, one has to be careful not to confuse the cost of capital with the cost of issuing capital. The cost of capital is simply<br />

a fair financial compensation owed to the providers of capital and is proportional to the riskiness of their respective financial<br />

claims. The cost of issuing capital is made of all direct and indirect expenses incurred by the firm in order to bring the bonds<br />

and shares in the hands of claimholders: creditors and shareholders. The cost of issuing capital is also referred to as flotation<br />

cost and is at its very heart an intermediation cost: commission, fees, spreads, money left on the table, etc. These costs are<br />

paid to underwriters, regulators, lawyers, accountants, etc.<br />

Of the two types enumerated above, the cost of debt is easier to estimate. We simply observe the interest a firm pays on its<br />

loans or the coupon it pays on its bonds. Banks and creditors usually do a fair job at estimating the riskiness of corporate<br />

borrowing. Of course, they all can be wrong at times, but in general the cash flow generated by debt is reasonably<br />

predictable because it is made of fixed payments at fixed intervals. Firms have no choice but to pay their financial<br />

obligations as they come due. The hard part is to estimate the probability that the firm will default. Some financial<br />

institutions use sophisticated methodologies to determine the level of creditworthiness of the borrower. Everyone is familiar<br />

with the bond rating done by Moody's, Standard & Poor, and Fitch:<br />

Summary of credit rating: Moody's, Standard&Poor, and Fitch<br />

Moody's rating Standard&Poor rating Fitch's rating<br />

Aaa AAA AAA Prime<br />

Aa1 AA+ AA+ High grade<br />

Aa2 AA AA High grade<br />

Aa3 AA- AA- High grade<br />

A1 A+ A+ Upper medium grade<br />

A2 A A Upper medium grade<br />

A3 A- A- Upper medium grade<br />

Baa1 BBB+ BBB+ Lower medium grade<br />

Baa2 BBB BBB Lower medium grade<br />

Baa3 BBB- BBB- Lower medium grade<br />

Ba1 BB+ BB+ Non Investment grade speculative<br />

Ba2 BB BB Non Investment grade speculative<br />

Ba3 BB- BB- Non Investment grade speculative<br />

B1 B+ B+ Highly Speculative<br />

B2 B B Highly Speculative<br />

B3 B- B- Highly Speculative<br />

Caa1 CCC+ CCC Substantial risks<br />

Caa2 CCC Extremely speculative<br />

Caa3 CCC- In default with little prospect for recovery<br />

Ca CC In default with little prospect for recovery<br />

/ D DDD In default<br />

/ DD In default<br />

/ D In default<br />

Source:Bonds online at http://www.bondsonline.com/asp/research/bondratings.asp and Wikipedia at http://en.wikipedia.org/wiki/Bond_credit_rating<br />

Investors and banks care about credit rating because it is a good indicator of how much to require for lending money. Firms<br />

with solid solvency ratios borrow at low rates, firms with acceptable solvency ratios borrow at higher rates, and firms on the<br />

13

verge of financial distress usually do not have access to debt financing. In general, the higher the level of financial leverage,<br />

the higher the marginal interest rate at which the firm can acquire new debt. This follows from the fact that more debt means<br />

more financial risk.<br />

The cost of equity is simply the required return on equity; that is, a return representing a fair compensation for the risk<br />

undertaken by shareholders. The most accurate thing we can say about the cost of equity is that it must be larger than the<br />

marginal (i.e., highest) interest rate at which the firm is able to borrow. By how much? One is at a loss to quantify the<br />

difference for lack of a reliable return generating model, that is, a functional model measuring how return varies with risk.<br />

Based on our discussion of business and financial risk, we contend that the cost of equity must be an increasing function of<br />

leverage, although we are not able to specify its functional form in too much detail:<br />

r = y(financial risk) + x(financial risk)<br />

where:<br />

r = cost of equity<br />

y = the cost of debt, a function of financial risk<br />

x = equity premium, also a function of financial risk<br />

This method is heuristic, because it is partially based on speculative judgments; it is, without a question a subjective<br />

approach.<br />

Academics and practitioners, however, don't like this elusive guesswork. They want hard numbers to justify their decisions -<br />

some equations to confer them the respectability of physics or engineering. There have been serious attempts to quantify<br />

this relationship in a more rigorous manner. Most corporate finance textbooks use a formula proposed by Merton Miller an<br />

Franco Modigliani 2 (the economist, not the painter):<br />

where:<br />

r = r(all-equity) + [r(all-equity) - y]*(D/E)*(1-Tc)<br />

r = the cost of equity; r(all-equity) is the cost of equity for a similar all-equity firm<br />

y = the cost of debt<br />

D = market value of debt, a function of rational expectations<br />

E = market value of equity, a function of rational expectations<br />

Tc = tax rate on corporate profits<br />

In this formula, the cost of equity is a nice, smooth, linear function of financial leverage, as measured by the debt-to-equity<br />

ratio. The trouble is, the relationship is indeterminate. First, we cannot tell what is the fair cost of equity for the all-equity<br />

firm; the cost of debt varies with leverage as well; and leverage is expressed in terms of market values -not those we can<br />

directly observe in the market at a given point in time- rather those contingent on rational expectations, that is, contingent<br />

on knowing the cost of equity. In other words, the cost of equity for the levered firm, the cost of equity for the all-equity<br />

firm, and the fair market value of equity are jointly determined. We just cannot hold them constant for the convenience of<br />

estimating them one at a time. We have one equation and at least three unknown variables that move together. We need<br />

alternative approaches.<br />

2 Modigliani, F. and Miller, M. H., (1963) "Corporate Income Taxes and the Cost of Capital: A Correction," American Economic Review, 53(3), 433–43.<br />

14

The Nine Lives of the Capital Asset Pricing Model (CAPM)<br />

The CAPM is at the heart of modern finance theory. It is a model of the return generating process, meaning that it aims to<br />

quantify how the required return of each security traded in the market is commensurate to its relative risk. The CAPM is<br />

both intuitive and simple to understand. It has a stunning mathematical elegance and a hard to equal beauty as far as<br />

economic theory goes. It appears to be the ideal candidate to estimating the cost of equity. CAPM relies on concepts like<br />

diversification, absolute risk, relative risk, efficient portfolios, and market portfolio.<br />

Diversification is the most intuitive concept of all. It simply states that by combining risky assets in the same portfolio, we<br />

might be able to reduce the total return volatility of the portfolio. Return volatility, as measured by variance (or standard<br />

deviation) is a measure of absolute risk. Diversification works when returns accross various securities are not perfectly<br />

correlated among them. Take the example of two assets, A and B, with return volatilities measured by σ(A) and σ(B). If the<br />

correlation between the two is less than 1, then the combined portfolio will have an absolute risk lower than the weighted<br />

average of the two individual risks:<br />

At the same time:<br />

σ(A and B) < σ(A) + σ(B)<br />

Eret(A + B) = Eret(A) + Eret(B)<br />

where:<br />

Eret (A+B)<br />

Eret(A)<br />

Eret(B)<br />

= expected return on the combined portfolio<br />

= expected return on asset A<br />

= expected return on asset B<br />

In other words, when we construct a portfolio of risky securities, the resulting return is simply the weighted average of the<br />

two returns, while the resulting risk is less than the weighted average of the two individual risks. The more securities we add<br />

to our portfolio the lower the resulting volatility of the portfolio. There are limits, however, to how much we can diversify<br />

away risk. As long as various securities exhibit a certain measure of correlation, no matter how hard we try, we reach a level<br />

beyond which volatility cannot be reduced any further. The level of portfolio volatility that cannot be diversified away is<br />

called systematic 3 , non-diversifiable, or market risk.<br />

It stands to reasons that, among all possible portfolios that we can construct with all the available securities, some will<br />

exhibit the largest level of return for a given level of standard deviation of return, or the lowest level of standard deviation<br />

of return for a given level of return. These portfolios are called efficient portfolios, and common sense dictates that a<br />

rational investor would only hold these efficient portfolios. Why hold just any portfolio, when for a particular level of risk<br />

there is an efficient portfolio with a higher return? In other words, efficient portfolios are desirable because they optimize<br />

the trade-off between risk and return.<br />

But which efficient portfolios to hold? That depends on each individual investor's risk aversion: more risk averse individuals<br />

will hold efficient portfolios with lower risk and lower return, while less risk averse individuals will hold efficient portfolios<br />

with higher risk and higher return.<br />

When there exists a (quasi) risk-free asset (such as a government-issued bond), it can be mathematically shown that,<br />

regardless of the level of risk aversion, rational investors will hold only one portfolio: this special portfolio contains all<br />

imaginable assets in the known universe, and is called the Market Portfolio. However, in order to accommodate each<br />

individual's risk preferences, the theory shows that the Market Portfolio can be combined with the risk-free asset in various<br />

proportions to generate various levels of risk and return. More prudent individuals will invest a fraction of their wealth in<br />

the risk-free asset (that is, buy government T-bills), and the remaining portion in the Market Portfolio. More adventurous<br />

investors would borrow money in order to increase their investment in the Market Portfolio. In any case, in a system of<br />

coordinates with standard deviation of return on the X-axis, and expected return on the Y-axis, all resulting possible<br />

combinations between the risk-free asset and the Market Portfolio will lie on a perfectly straight line known as the Capital<br />

Market Line.<br />

3 Not to be confused with systemic risk, which refers to the risk faced by financial institutions when the failure of one entity triggers a domino effect that<br />

threatens to bring down the entire system.<br />

15

Relative risk and β<br />

Since return volatility can be reduced, or rather partially neutralized through diversification, it stands to reason that the<br />

standard deviation of return is not the most relevant way to measure risk.<br />

Instead of focusing on the standard deviation of return, we should measure the extent to which adding a given asset to a<br />

well-diversified portfolio, such as the Market Portfolio, contributes to the overall return volatility of the portfolio. The<br />

relative contribution of an asset to the overall return volatility of the Market Portfolio is measured by the fabled β, the<br />

quintessential measure of relative risk. Mathematically, β is nothing else but the covariance between the return of the<br />

Market Portfolio and that of the asset, divided by the variance of the Market Portfolio:<br />

β = covariance(M, asset)/variance(M)<br />

where M denotes the Market Portfolio.<br />

By definition, β(M) = 1. This simply follows from the above equality.<br />

When an asset has a beta larger than one, it follows that adding that asset to the Market Portfolio will increase the overall<br />

volatility of return of the Market Portfolio. A beta less than one means that adding that asset to the Market Portfolio will<br />

decrease the overall volatility of return of the Market Portfolio. A beta equal to one will leave the overall volatility of return<br />

of the Market Portfolio unchanged.<br />

Having established that relative risk is the relevant measure of risk, we now turn to analyzing return. We notice that risky<br />

securities require a return above and beyond the return on the risk-free asset. Obviously, the risk-free rate is a compensation<br />

for inflation and time preference 4 , but not for risk. While trivial, this observation has profound implications. It follows that<br />

the difference between the required return on the Market Portfolio and the return on the risk-free asset shows the extra<br />

return required only and only by market risk alone. This difference is called market risk premium:<br />

Market risk premium = Rret(M) – Rret(risk-free asset)<br />

Obviously, the risk premium of any given asset will vary according to risk. To be more precise, according to relative risk.<br />

The Market Portfolio is now the main reference point. It is the yardstick for measuring return and risk. All the pieces of the<br />

puzzle are about to fall into place.<br />

The main contention of the CAPM is that the risk premium per unit of relative risk must be the same across all assets in the<br />

market:<br />

[Rret(A) – Rret(Risk-free asset)]/ β(A) = [Rret(B) – Rret(Risk-free asset)]/ β(B) = .......etc.<br />

Since the Market Portfolio is an asset as well, it follows that:<br />

[Rret(A) – Rret(Risk-free asset)]/ β(A) = [Rret(M) – Rret(Risk-free asset)]/ β(M)<br />

By definition, β(M) = 1. It follows that:<br />

or<br />

[Rret(A) – Rret(Risk-free asset)]/ β(A) = [Rret(M) – Rret(Risk-free asset)]<br />

Rret(A) = Rret(Risk-free asset) + β(A)*[Rret(M) – Rret(Risk-free asset)]<br />

This conclusion is highly intuitive, almost trivial, if you think about it. While in the grocery store the price of a steak is<br />

proportional to its weight times the price per pound, in the financial market the required return of an asset is proportional to<br />

4 Time preference denotes the willingness to postpone or sacrifice current consumption in exchange for future consumption. It can also be viewed as the<br />

degree of consumption impatience. Investors with high time preference will require high rates of return to compensate them for postponing current<br />

consumption, even when there is no risk.<br />

16

its relative risk times the return premium per unit of relative risk. Another nontrivial contention is that the market rewards<br />

only systematic risk, not absolute risk. Required return is proportional to beta, not to the standard deviation of return. The<br />

connoisseur can only wonder at the exquisite elegance, audacity and sheer scope of the mathematical apparatus deployed<br />

here to make this simple point 5 .<br />

Albert Einstein once quipped that “ elegance is for tailors.” The beauty and elegance of the CAPM, however, is only<br />

equaled by its absolute lack of practicality. The CAPM first emerged as a positive (i.e. descriptive) theory of the return<br />

generating process, but was surreptitiously perverted into a normative theory of estimating required return and measuring<br />

performance. If there is anything for which the CAPM is ill-equipped, it has to be its inability for providing guidance in<br />

estimating required rates of return. Without dwelling too much on its many metaphysical flaws, let us draw the attention to<br />

some very simple, yet practical shortcomings.<br />

Suppose you wish to estimate the cost of capital for Toy Inc. The cost of capital is the rate of returned required by Toy Inc.<br />

shareholders. The first step is to estimate the beta of the stock. Next, estimate the market risk premium, and the risk-free<br />

rate. Once all these variables have been accounted for, use the formula:<br />

Rret(Toy Inc.) = Rret(Risk-free asset) + β(Toy Inc.)*[Rret(M) – Rret(Risk-free asset)]<br />

Easier said than done. Once we start to carry on these steps we soon realize how insurmountable the practical details of our<br />

endeavor turn out to be. The beta of Toy Inc. should reflect the rational expectations of investors regarding the relative risk<br />

of Toy Inc. going forward. Investors' expectations are virtually unobservable quantities. Alas, we are able to observe only<br />

realizations. Meanwhile, under the influence of new information constantly flowing into the market, investors have moved<br />

on to new expectations. The only way out is to assume that current expectation are predicted by past expectations, and<br />

estimate beta by regressing Toy Inc.'s past returns against Market Portfolio past returns. This statement turns out to be very<br />

controversial. If life is filled with uncertainty, and things happen at random, then expectations about future events should<br />

change randomly. Even when investors are not rational and are under the influence of past events, it would still hold true<br />

that current expectations need not be the same as past realizations. Even if we take the ultimate leap of faith and equate past<br />

realization with current expectations, we arrive at a very troubling conclusion: if the future is predicted by the past, why<br />

bother to entertain this arcane and contrived exercise, when we could simply extrapolate past returns into the future. In fact,<br />

technical analysts shun CAPM and other type of fundamental analysis altogether, and stick with extrapolating charts and<br />

trends, without too much success either; but that is a whole different story.<br />

For now let us ignore all these (otherwise legitimate) concerns, and let us plod ahead with our estimation of the required<br />

return. In order to estimate the beta of Toy Inc. we have no choice but to regress the historical return of Toy Inc. against that<br />

of the Market Portfolio:<br />

Hret(Toy Inc.) = a + b*Hret(M) + e<br />

where:<br />

Hret(Toy Inc.) = historical returns on Toy Inc.<br />

Hret(M) = historical return on the Market Portfolio<br />

a, b, = regression coefficients<br />

e<br />

= error term, following a normal distribution with mean zero and standard deviation equal to one<br />

But what is the Market Portfolio? The theory behind the CAPM states that the Market Portfolio is made up of ALL assets<br />

that could be traded world-wide. This includes stocks, bonds, real estate, collectibles, art, gold, racing cars, bottle-aged<br />

wine, and many others. To our knowledge, there is no market index (yet) that includes everything. Can we settle for an<br />

index that approximates the market portfolio? The answer of CAPM is a resounding NO. An index similar to the Market<br />

Portfolio is no substitute for the real thing. Close enough is not good enough. Once we make the substitution, we abandon<br />

the CAPM, and start operating according to a different model, not yet formalized or explained. Call it Joe's Asset Pricing<br />

Model, or Buster's Asset Pricing Model, or the Ad-Hoc Pricing Model, or the Makeshift Asset Pricing Model, but it is<br />

definitely NOT the Capital Asset Pricing Model. In practice, however we have little choice because there is only a limited<br />

range of indexes available. Hence, we pick one that we feel is representative and we pretend not to notice we are straying<br />

away more and more from the gospel of the theory. Now that we have trampled over yet another legitimate objection let us<br />

5 As the reader has probably realized by now, the above discussion is an oversimplification of the mathematically-rich derivation of the CAPM; many<br />

steps have been skipped and replaced with a sleigh of hand.<br />

17

settle for the S&P 500 as a proxy of the Market Portfolio.<br />

Let us consider the following data:<br />

Monthly returns S&P 500 and Toy Inc. (2000-2009). Source: S&P data provided by Standard & Poor Index Services, Toy Inc. is fictitious.<br />

Month S&P 500 close Change S&P 500 monthly return Toy Inc. monthly return Risk-free rate Market risk premium<br />

02/2009 735.09 -90.79 -10.99% -22.00% 0.03% -11.03%<br />

01/2009 825.88 -77.37 -8.57% 2.50% 0.03% -8.60%<br />

12/2008 903.25 7.01 0.78% 1.80% 0.03% 0.75%<br />

11/2008 896.24 -72.51 -7.49% 2.70% 0.03% -7.51%<br />

10/2008 968.75 -197.61 -16.94% 6.40% 0.03% -16.97%<br />

09/2008 1166.36 -116.47 -9.08% 2.20% 0.03% -9.11%<br />

08/2008 1282.83 15.45 1.22% -1.20% 0.03% 1.19%<br />

07/2008 1267.38 -12.62 -0.99% 5.70% 0.04% -1.02%<br />

06/2008 1280.00 -120.38 -8.60% 7.90% 0.04% -8.63%<br />

05/2008 1400.38 14.79 1.07% -22.00% 0.04% 1.03%<br />

04/2008 1385.59 62.88 4.75% 25.00% 0.04% 4.72%<br />

03/2008 1322.70 -7.93 -0.60% 6.90% 0.05% -0.64%<br />

02/2008 1330.63 -47.92 -3.48% 4.90% 0.05% -3.52%<br />

01/2008 1378.55 -89.81 -6.12% 17.00% 0.05% -6.16%<br />

12/2007 1468.36 -12.79 -0.86% 3.00% 0.05% -0.91%<br />

11/2007 1481.14 -68.23 -4.40% 6.60% 0.05% -4.45%<br />

10/2007 1549.38 22.63 1.48% -2.55% 0.05% 1.43%<br />

09/2007 1526.75 52.76 3.58% -3.88% 0.09% 3.49%<br />

08/2007 1473.99 18.72 1.29% 12.70% 0.09% 1.20%<br />

07/2007 1455.27 -48.08 -3.20% 6.88% 0.09% -3.29%<br />

06/2007 1503.35 -27.27 -1.78% 8.90% 0.08% -1.87%<br />

05/2007 1530.62 48.25 3.26% -6.90% 0.08% 3.17%<br />

04/2007 1482.37 61.50 4.33% -1.10% 0.08% 4.24%<br />

03/2007 1420.86 14.05 1.00% -8.00% 0.25% 0.75%<br />

02/2007 1406.82 -31.42 -2.18% 4.70% 0.25% -2.43%<br />

01/2007 1438.24 19.94 1.41% -5.70% 0.25% 1.16%<br />

12/2006 1418.30 17.67 1.26% -7.90% 0.25% 1.01%<br />

11/2006 1400.63 22.69 1.65% -2.00% 0.17% 1.47%<br />

10/2006 1377.94 42.09 3.15% -1.00% 0.17% 2.98%<br />

09/2006 1335.85 32.03 2.46% -2.50% 0.17% 2.28%<br />

08/2006 1303.82 27.16 2.13% -6.00% 0.17% 1.95%<br />

07/2006 1276.66 6.46 0.51% -1.00% 0.17% 0.34%<br />

06/2006 1270.20 0.11 0.01% -1.00% 0.17% -0.16%<br />

05/2006 1270.09 -40.52 -3.09% 18.90% 0.20% -3.29%<br />

04/2006 1310.61 15.78 1.22% -0.20% 0.20% 1.02%<br />

03/2006 1294.83 14.17 1.11% -0.70% 0.20% 0.91%<br />

02/2006 1280.66 0.58 0.05% -2.00% 0.20% -0.15%<br />

01/2006 1280.08 31.79 2.55% -4.00% 0.20% 2.35%<br />

12/2005 1248.29 -1.19 -0.09% 1.00% 0.26% -0.36%<br />

18

11/2005 1249.48 42.47 3.52% -6.00% 0.26% 3.26%<br />

10/2005 1207.01 -21.80 -1.77% 3.50% 0.20% -1.97%<br />

09/2005 1228.81 8.48 0.69% -0.29% 0.20% 0.50%<br />

08/2005 1220.33 -13.85 -1.12% -2.07% 0.28% -1.40%<br />

07/2005 1234.18 42.85 3.60% 4.29% 0.15% 3.45%<br />

06/2005 1191.33 -0.17 -0.01% -1.36% 0.15% -0.16%<br />

05/2005 1191.50 34.65 3.00% 1.38% 0.15% 2.85%<br />

04/2005 1156.85 -23.74 -2.01% -1.44% 0.15% -2.16%<br />

03/2005 1180.59 -23.01 -1.91% -1.42% 0.29% -2.20%<br />

02/2005 1203.60 22.33 1.89% 1.56% 0.29% 1.60%<br />

01/2005 1181.27 -30.65 -2.53% -3.76% 0.29% -2.82%<br />

12/2004 1211.92 38.10 3.25% 3.16% 0.19% 3.06%<br />

11/2004 1173.82 43.62 3.86% 3.34% 0.19% 3.67%<br />

10/2004 1130.20 15.62 1.40% 1.18% 0.19% 1.21%<br />

09/2004 1114.58 10.34 0.94% 1.19% 0.19% 0.75%<br />

08/2004 1104.24 2.52 0.23% 1.68% 0.19% 0.04%<br />

07/2004 1101.72 -39.12 -3.43% -4.45% 0.21% -3.64%<br />

06/2004 1140.84 20.16 1.80% 3.21% 0.21% 1.58%<br />

05/2004 1120.68 13.38 1.21% 1.93% 0.17% 1.04%<br />

04/2004 1107.30 -18.91 -1.68% -2.01% 0.17% -1.85%<br />

03/2004 1126.21 -18.73 -1.64% -1.80% 0.17% -1.81%<br />

02/2004 1144.94 13.81 1.22% 1.90% 0.17% 1.05%<br />

01/2004 1131.13 19.21 1.73% 2.01% 0.17% 1.55%<br />

12/2003 1111.92 53.72 5.08% 4.26% 0.17% 4.90%<br />

11/2003 1058.20 7.49 0.71% 1.93% 0.17% 0.54%<br />

10/2003 1050.71 54.74 5.50% 5.32% 0.17% 5.32%<br />

09/2003 995.97 -12.04 -1.19% -0.36% 0.19% -1.38%<br />

08/2003 1008.01 17.70 1.79% 1.58% 0.19% 1.60%<br />

07/2003 990.31 15.81 1.62% 1.65% 0.19% 1.43%<br />

06/2003 974.50 10.91 1.13% 1.85% 0.17% 0.96%<br />

05/2003 963.59 46.67 5.09% 5.19% 0.17% 4.92%<br />

04/2003 916.92 68.74 8.10% 9.13% 0.17% 7.94%<br />

03/2003 848.18 7.03 0.84% -0.17% 0.17% 0.66%<br />

02/2003 841.15 -14.55 -1.70% -0.93% 0.17% -1.87%<br />

01/2003 855.70 -24.12 -2.74% -4.32% 0.17% -2.91%<br />

12/2002 879.82 -56.49 -6.03% -4.70% 0.17% -6.20%<br />

11/2002 936.31 50.55 5.71% 6.78% 0.25% 5.45%<br />

10/2002 885.76 70.48 8.64% 7.11% 0.25% 8.39%<br />

09/2002 815.28 -100.79 -11.00% -10.76% 0.20% -11.20%<br />

08/2002 916.07 4.45 0.49% 0.40% 0.20% 0.29%<br />

07/2002 911.62 -78.20 -7.90% -8.12% 0.20% -8.10%<br />

06/2002 989.82 -77.32 -7.25% -6.58% 0.13% -7.38%<br />

05/2002 1067.14 -9.78 -0.91% 0.57% 0.13% -1.04%<br />

04/2002 1076.92 -70.47 -6.14% -5.23% 0.12% -6.27%<br />

19

03/2002 1147.39 40.66 3.67% 2.48% 0.12% 3.56%<br />

02/2002 1106.73 -23.47 -2.08% -1.99% 0.12% -2.19%<br />

01/2002 1130.20 -17.88 -1.56% -0.85% 0.12% -1.67%<br />

12/2001 1148.08 8.63 0.76% 0.19% 0.12% 0.64%<br />

11/2001 1139.45 79.67 7.52% 7.36% 0.12% 7.40%<br />

10/2001 1059.78 18.84 1.81% 1.59% 0.14% 1.67%<br />

09/2001 1040.94 -92.64 -8.17% -7.42% 0.14% -8.31%<br />

08/2001 1133.58 -77.65 -6.41% -5.08% 0.14% -6.55%<br />

07/2001 1211.23 -13.15 -1.07% -2.27% 0.14% -1.21%<br />

06/2001 1224.38 -31.44 -2.50% -3.12% 0.29% -2.79%<br />

05/2001 1255.82 6.36 0.51% -0.62% 0.29% 0.22%<br />

04/2001 1249.46 89.13 7.68% 6.05% 0.37% 7.31%<br />

03/2001 1160.33 -79.61 -6.42% -5.56% 0.23% -6.65%<br />

02/2001 1239.94 -126.07 -9.23% -7.88% 0.23% -9.46%<br />

01/2001 1366.01 45.73 3.46% 3.27% 0.23% 3.23%<br />

12/2000 1320.28 5.33 0.41% -0.36% 0.38% 0.03%<br />

11/2000 1314.95 -114.45 -8.01% -7.59% 0.25% -8.26%<br />

10/2000 1429.40 -7.11 -0.49% 1.07% 0.25% -0.75%<br />

09/2000 1436.51 -81.17 -5.35% -6.74% 0.44% -5.79%<br />

08/2000 1517.68 86.85 6.07% 7.13% 0.31% 5.76%<br />

07/2000 1430.83 -23.77 -1.63% -0.95% 0.24% -1.87%<br />

06/2000 1454.60 34.00 2.39% 1.08% 0.24% 2.15%<br />

05/2000 1420.60 -31.83 -2.19% -1.45% 0.24% -2.43%<br />

04/2000 1452.43 -46.15 -3.08% -2.97% 0.38% -3.46%<br />

03/2000 1498.58 132.16 9.67% 8.47% 0.38% 9.30%<br />

02/2000 1366.42 -28.04 -2.01% -2.68% 0.24% -2.25%<br />

01/2000 1394.46 -74.79 -5.09% -6.72% 0.24%<br />

20

Why the period 2000-2009? There is no obvious answer to this question. In this particular case, we just found historical data<br />

with relative ease; we could have searched harder and go back to 1990, or to 1980, to 1970, or even earlier. We have<br />

absolutely no guidance as to how far back into the past we should go, because beta and the market risk premium are based<br />

on market expectations going forward, not looking back. CAPM is absolutely mum on historical estimation simply because<br />

one is not supposed to estimate beta in this way. The honest conclusion is that we have chosen this particular data arbitrarily.<br />

Another arbitrarily choice refers to the type of return. Here we show monthly returns. We could have used annual returns, or<br />

weekly returns, or daily returns. Again, convenience proved to be the trump card. Monthly returns were readily available,<br />

and we simply settled for them. Let us continue then.<br />

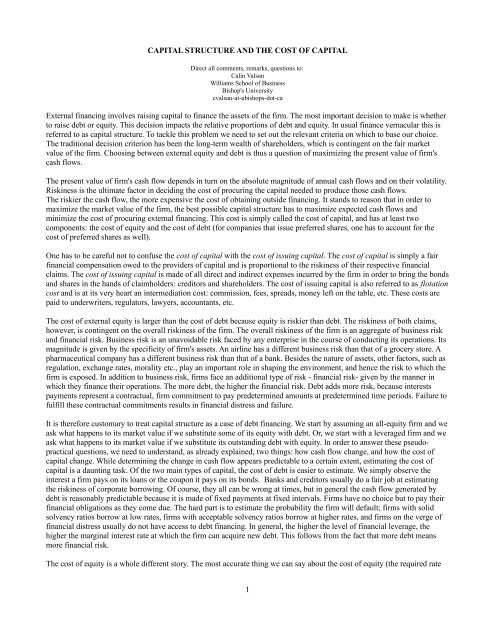

The relative risk of Toy Inc. is given by the strength of the correlation between the return on Toy Inc. and that of the S&P<br />

500 index. Mathematically, beta is represented by the coefficient of S&P 500 index in the following regression model:<br />

Hret(Toy Inc.) = a + b*Hret(S&P 500) + e<br />

Before we proceed with running the least-squares regression analysis, we plot the data along the XY-coordinates, with<br />

return on Toy Inc. on the Y-axis, and return on the S&P 500 on the X-axis:<br />

0.3<br />

Toy Inc. against the S&P 500: 2000-2009<br />

0.2<br />

Toy Inc. monthly return<br />

0.1<br />

0<br />

-0.1<br />

-0.2<br />

-0.3<br />

0.00% 2000.00% 4000.00% 6000.00% 8000.00% 10000.00% 12000.00%<br />

S&P 500 monthly return<br />

We use Excel or any other software with econometric functions and we obtain a result that should be similar to this one:<br />

21

Regression output: Toy Inc. as a dependent variable 2000-2009<br />

Regression Statistics<br />

Multiple R 0.33<br />

R Square 0.11<br />

Adjusted R Square 0.1<br />

Standard Error 0.06<br />

Observations 110<br />

ANOVA<br />

df SS MS F Significance F<br />

Regression 1 0.05 0.05 13.11 0<br />

Residual 108 0.4 0<br />

Total 109 0.45<br />

Coefficients<br />

Standard<br />

Error<br />

t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%<br />

Intercept 0.01 0.01 0.93 0.35 -0.01 0.02 -0.01 0.02<br />

S&P 0.47 0.13 3.62 0 0.21 0.72 0.21 0.72<br />

The regression output reveals some very interesting things: approximately 11% of the variance in the monthly returns of<br />

Toy Inc. is explained by the variance in the returns of the S&P 500 (R-square = 0.11). This influence is significant, that is.,<br />

the model has explanatory power (F = 13.11). It is significant, but small. It follows that the remaining 89% of the variance<br />

in the returns of Toy Inc. is explained by other factors than the S&P 500 index. One more reason to diversify your<br />

investments.<br />

The fitted regression model becomes:<br />

Ret(Toy Inc.) = 0.01 + 0.47*Ret(S&P 500)<br />

The estimated beta of Toy Inc. is equal to 0.47. The last step is to estimate the market risk premium and the risk-free rate.<br />

The risk-free rate can be approximated as being equal to the return on the one-month Treasuries. The estimation of the<br />

market risk premium is more problematic though. The average market risk premium (the difference between the return on<br />

the S&P 500 and the risk-free rate) for the period 2000-2009 is -0.7%. If we take this historical estimate to infer the<br />

expected market risk premium we end up with a paradox. Are investors really expecting a long-run negative return on the<br />

S&P 500? If so, why are they still holding on to their stocks? As I write these lines the S&P 500 and other major indices are<br />

all down significantly, having reached historical lows. A majority of investors still believe that next year's return will be<br />

negative; but they eventually hope that in two or three,or maybe four years things will turn around, and in the long-run, the<br />

expected return will average out to a positive number. No investor in his/her right mind would hold on to stocks that are<br />

expected to return -0.7% on average over the next century. This is plain common sense. The simple fact that there are still<br />

billions of dollars invested in S&P 500 stocks is a testimony to the expectations that – in spite of the current economic<br />

slump – markets will eventually turn around. The later this turnaround, the lower the index will go; however, as long as<br />

there is a glimmer of hope people will still hold stocks. But never mind all this; let us continue. We average the risk-free rate<br />

for the entire period and we find it equal to 0.17%. Now we can estimate the required rate of return for Toy Inc.<br />

Rret(Toy Inc.) = 0.17% + 0.46*(-0.7%) = -0.152%<br />

On an annualized base this equals -1.8%. We find that the cost of equity for Toy Inc. is a negative 1.8%/year. This result is<br />

evidently absurd!<br />

22

Let us try estimating beta using another period. Let us say 2005-2009, maybe recent trends are more relevant:<br />

30.00%<br />

T oy Inc. against the S&P 500: 2005-2009<br />

20.00%<br />

T oy Inc. monthly return<br />

10.00%<br />

0.00%<br />

-10.00%<br />

-20.00%<br />

-30.00%<br />

-20.00% -15.00% -10.00% -5.00% 0.00% 5.00% 10.00%<br />

S&P 500 monthly return<br />

Regression output: Toy Inc. as a dependent variable 2005-2009<br />

Regression Statistics<br />

Multiple R 0.12<br />

R Square 0.01<br />

Adjusted R Square -0.01<br />

Standard Error 0.08<br />

Observations 50<br />

ANOVA<br />

df SS MS F Significance F<br />

Regression 1 0 0 0.68 0.41<br />

Residual 48 0.32 0.01<br />

Total 49 0.32<br />

Coefficient<br />

s<br />

Standard<br />

Error<br />

t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%<br />

Intercept 0.01 0.01 0.62 0.54 -0.02 0.03 -0.02 0.03<br />

S&P -0.22 0.27 -0.83 0.41 -0.76 0.32 -0.76 0.32<br />

Notwithstanding the insignificant explanatory power of the model (F = 0.68), the regression line is now:<br />

23

Ret(Toy Inc.) = 0.01 -0.22*Ret(S&P 500)<br />

Beta is negative meaning that the return on Toy Inc. is negatively correlated to that on the S&P 500. Between 2005 and<br />

2009 Toy Inc. moved in the opposite direction of the S&P 500: when the index rose, the stock sank; when the index<br />

slumped, the stock rose. Obviously, this makes Toy Inc. a very good candidate for diversification. The market risk premium<br />

averages -1.03% for the period 2005-2009, and the risk-free rate averages 0.14%.<br />

Rret(Toy Inc.) = 0.14% -0.22*(-1.03%) = 0.37%<br />

On an annualized basis, the required return for Toy Inc. is equal to 4.49%. This figure appears more reasonable, but make no<br />

mistake, it is as arbitrary as the previous estimation. In fact there is absolutely no valid criteria to tell us why we should<br />

chose one historical period over another one. Were we to use the period 2007-2009, we would have ended up with a<br />

complete different result. Even if we stayed with the same period, but used daily returns instead of monthly returns, results<br />

would have changed. Every time we change our estimation method, results change. Period. So, CAPM is not very helpful or<br />

reliable.<br />

Perhaps, we should attempt another approach.<br />

24

The Dividend Growth Model<br />

The valuation of equity is usually done with the help of the dividend growth model. In real life, the stream of dividend is<br />

uneven and unpredictable, unlike the coupons paid by bonds. The smoothness and relative predictability of interest<br />

payments makes the valuation of bonds a walk in the park compared to the valuation of common equity. The formula for<br />

calculating the price of a bond is tight and sparse: the present value of a known annuity at known intervals of time, plus the<br />

present value of a known face value payment at a future known date. By contrast, the present value of common equity is<br />

given by an open ended model:<br />

P = dividend1/(1+r) + dividend2/(1+r) 2 + dividend3/(1+r) 3 + ...... + dividendN/(1+r) n + ......<br />

Obviously, this is not of much practical help, unless we could make it more tractable. The solution is to imagine that the<br />

future (quasi) infinite stream of dividend can be smoothened out over long periods, by averaging out wild swings. The result<br />

is a perpetuity with constant growth rate g. It can be shown that:<br />

P = dividend/(1+r) + dividend(1+g)/(1+r) 2 + dividend(1+g) 2 /(1+r) 3 + ...... + dividend(1+g) n-1 /(1+r) n + ......<br />

can be approximated by the formula:<br />

P = dividend/(r-g)<br />

So, if we know the required rate and the expected long-term growth rate in dividends, we can easily estimate the price of the<br />

stock. But how can we know r? We simply turn the formula around:<br />

r = dividend/P + g<br />

where:<br />

dividend/P<br />

g<br />

= dividend yield<br />

= long-term growth rate in dividend<br />

when we deal with a cash cow, that is, a mature firm, without major growth opportunities, paying more or less a level<br />

dividend stream, the formula becomes:<br />

r = dividend/P<br />

This approach for estimating the cost of equity is less troublesome in some ways than the CAPM; it too, however, requires a<br />

major leap of faith. In order to estimate the required rate of return, the value of the current stock price entered in the formula<br />

has to reflect the true riskiness of the dividend stream. To see why this is true, consider the following example:<br />

Toy Inc. and Super Toy Inc. expected annual dividend<br />

Dividend paid if<br />

recession<br />

Probability of<br />

recession<br />

Dividend paid if<br />

expansion<br />

Probability of<br />

expansion<br />

Expected annual<br />

dividend<br />

Toy Inc. $0.9 0.5 $1.04 0.5 $0.97<br />

Super Toy Inc. $0.0 0.5 $1.94 0.5 $0.97<br />

Both Toy Inc. and Super Toy Inc. are expected to pay an annual dividend equal on average to $0.97. If both companies are<br />

priced in the market at $25/share, how do we know which one is correctly priced, and which is not? According to the<br />

dividend growth model, both firms should have a cost of equity equal to (assuming zero growth in dividends):<br />

r(Toy Inc.) = $0.97/$25 = 3.9%<br />

r(Super Toy Inc.) = $0.97/$25 = 3.9%<br />

We know, however, that this is not possible since Super Toy Inc. is riskier than Toy Inc. Obviously, one of them is<br />

mispriced. But once we admit the market is fallible, we open the door to the possibility that the market is wrong with<br />

respect to both of them. Maybe the price of Toy Inc. is too low, and the price of Super Toy Inc. is too high. In reality it is<br />

25

very hard to tell companies like Toy Inc. and Super Toy Inc. apart. Investors see that they both behave like cash cows and<br />

pay comparable annual dividends, hence they infer they should be priced the same.<br />

The problem gets worse when we deal with growth companies. Not only should we question the fairness of market pricing,<br />

but we also have to (gu)estimate the growth rate in earnings/dividends. While we might have an inkling about "next year,"<br />