AP3 - Principles for Responsible Investment

AP3 - Principles for Responsible Investment

AP3 - Principles for Responsible Investment

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

An investor initiative in partnership with UNEP Finance Initiative and the UN Global Compact<br />

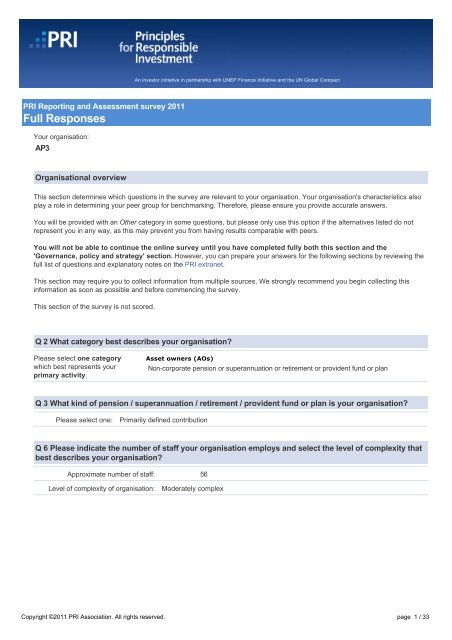

PRI Reporting and Assessment survey 2011<br />

Full Responses<br />

Your organisation:<br />

<strong>AP3</strong><br />

Organisational overview<br />

This section determines which questions in the survey are relevant to your organisation. Your organisation's characteristics also<br />

play a role in determining your peer group <strong>for</strong> benchmarking. There<strong>for</strong>e, please ensure you provide accurate answers.<br />

You will be provided with an Other category in some questions, but please only use this option if the alternatives listed do not<br />

represent you in any way, as this may prevent you from having results comparable with peers.<br />

You will not be able to continue the online survey until you have completed fully both this section and the<br />

'Governance, policy and strategy' section. However, you can prepare your answers <strong>for</strong> the following sections by reviewing the<br />

full list of questions and explanatory notes on the PRI extranet.<br />

This section may require you to collect in<strong>for</strong>mation from multiple sources. We strongly recommend you begin collecting this<br />

in<strong>for</strong>mation as soon as possible and be<strong>for</strong>e commencing the survey.<br />

This section of the survey is not scored.<br />

Q 2 What category best describes your organisation?<br />

Please select one category<br />

which best represents your<br />

primary activity.<br />

Asset owners (AOs)<br />

Noncorporate pension or superannuation or retirement or provident fund or plan<br />

Q 3 What kind of pension / superannuation / retirement / provident fund or plan is your organisation?<br />

Please select one:<br />

Primarily defined contribution<br />

Q 6 Please indicate the number of staff your organisation employs and select the level of complexity that<br />

best describes your organisation?<br />

Approximate number of staff: 56<br />

Level of complexity of organisation:<br />

Moderately complex<br />

Copyright ©2011 PRI Association. All rights reserved. page 1 / 33

Q 7 What were your organisation's total assets under management as of 31 December 2010, including the<br />

assets of all your consolidated subsidiaries?<br />

billions millions thousands units<br />

Total AUM: 220 829 000 000<br />

Currency:<br />

Swedish Krona (SEK)<br />

Date of assets under management figure<br />

year month day<br />

Date: 2010 December 31<br />

The amount you indicated above is roughly equal to the amount calculated below in United States Dollars. Please<br />

confirm that this figure is approximately correct be<strong>for</strong>e proceeding. Exchange rates are from the International<br />

Monetary Fund.<br />

Source: IMF Exchange Rate archive, December 2010<br />

billions millions thousands units<br />

Total AUM in USD: 32 462 775 686<br />

Copyright ©2011 PRI Association. All rights reserved. page 2 / 33

Q 8 Please provide an approximation of your average asset mix <strong>for</strong> 2010 or your most recent count, in %.<br />

(For asset classes you hold in insignificant amounts you may choose not to list them and will not be asked<br />

related questions. +/ 5% is sufficient; the sum of all the fields must be 100 %)<br />

Asset class<br />

Internal<br />

active<br />

Internal<br />

passive<br />

External<br />

active<br />

External<br />

passive<br />

Listed equity (developed markets) 1 % 19 % 1 % 22 %<br />

Listed equity (emerging markets) 0 % 3 % 3 % 3 %<br />

Fixed income sovereign and<br />

other noncorporate issuers<br />

0 % 34 % % %<br />

Fixed income corporate issuers % % 0 % %<br />

Private equity % % 5 % 0 %<br />

Listed real estate or property 0 % % % 0 %<br />

Nonlisted real estate or property 4 % % % 2 %<br />

Hedge funds % % % %<br />

Commodities 0 % 0 % 0 % 0 %<br />

Infrastructure % % % %<br />

Cash 0 % 0 % 0 % 0 %<br />

Other please specify:<br />

Fixed income internal mgmt <br />

we have not divided our<br />

portfolio into corporate,<br />

soveriegn and noncorp,<br />

there<strong>for</strong>e I have put the whole<br />

internal fixed income portfolio<br />

into the box "Soveriegn and<br />

noncorp" , although it also<br />

includes corporate bonds.<br />

Real estate includes<br />

timberland.<br />

The box OTHEr contains<br />

New strategies<br />

3 % 0 % 0 % 0 %<br />

Please contact the PRI Secretariat at assessment@unpri.org be<strong>for</strong>e indicating that more than 10% of your assets fall into the<br />

'Other' category. A response of 'Other' may render the benchmarking results less useful <strong>for</strong> you and your peers.<br />

If you manage balanced or multiasset class products with listed equity, fixed income and potentially other asset classes, the<br />

relative assets in these funds need to be separated out into the different asset classes.<br />

Total (must add up to 100%): 100 %<br />

Q 9 Please provide the following in<strong>for</strong>mation based on your asset classes holdings:<br />

(rough estimates of /+ 5% are fine; when negligible, please leave as zero)<br />

B. What percentage of your assets invested in publicly listed<br />

companies are invested in companies where your<br />

organisation or external investment managers have<br />

significant control? Significant control implies that active<br />

ownership can influence change more so than proxy voting<br />

and engagement alone.<br />

1 %<br />

Copyright ©2011 PRI Association. All rights reserved. page 3 / 33

Q 10 What percentage of your externally managed assets are managed by PRI signatories?<br />

(+/ 5% is sufficient)<br />

Percentage: 27 %<br />

Copyright ©2011 PRI Association. All rights reserved. page 4 / 33

Governance, policy and strategy<br />

This section is focused on the governance, policies and strategies guiding your organisation's approach to responsible investment<br />

(RI). 'Policy' in this section may refer to one overall RI policy or multiple policies that address various elements of RI or ESG<br />

issues. Some questions in this section are scored, while other questions are not scored but do determine the applicability of<br />

subsequent questions.<br />

Please make sure you provide accurate answers. You will not be able to enter this section unless you have completed the<br />

"Organisational overview" section. You will not be able to continue the survey until you have finalised this section.<br />

However, if you wish to begin preparing your answers <strong>for</strong> the following sections, you may do so by reviewing the full list of<br />

questions and explanatory notes in the manual provided on the PRI extranet. This section will be scored separately from the six<br />

<strong>Principles</strong>.<br />

Q 11 Please provide a description of how your governance, policies and strategies address RI and ESG<br />

issues.<br />

Note that this text in addition to being part of the full survey will also be part of the Executive Summary<br />

of the survey. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong><br />

each of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

The Third Swedish National Pension Fund (<strong>AP3</strong>) aims to generate maximum returns on fund capital at a low level of risk, and<br />

we use our influence as an investor to help us achieve that goal. The legislation that regulates our operations requires us to<br />

disregard economic and business policy considerations in our investment decisions. We are, however, required to take<br />

environmental and social considerations in our investment activities, without compromising the goal of securing high returns.<br />

Our mandate gives us a unique opportunity to exercise influence as an independent institutional shareholder on Sweden's<br />

equity market. As part of the national pension system, we are independent of other investors and business interests.<br />

The Board of Directors review the corporate governance policy on an annual basis. The policy is published on the Fund´s web<br />

site. The Board has delegated the exercise of the corporate governance policy to the Funds CEO who in turn has appointed a<br />

governance team. The Fund regularly reports on how it exercise it responsible governance role to the Board. Moreover, the Fund<br />

publish an ESGreport one a year as well.<br />

We believe that active governance makes a positive contribution over time to our primary goal of obtaining high investment<br />

returns. We prioritise active governance in companies where we have relatively large equity holdings, which at present relates<br />

mainly to Swedish stocks and Swedish real estate. We also prioritise taking an active role in the debate on corporate<br />

governance guidelines in the Swedish equity market.<br />

Most of our <strong>for</strong>eign equity portfolio is managed by external managers. However, we have <strong>for</strong> the past years expanded our direct<br />

voting in the global equity portfolio as part of our extended commitment to corporate governance.<br />

Our main governance tools are:<br />

o Active participation in nomination committees<br />

o Dialogue with company boards and managements<br />

o Exercising voting rights at AGMs including vote on ESG resolutions, file/cofile resolutions<br />

o Speaking at AGMs<br />

o Active involvement in developing the system of selfregulation through<br />

participation in organisations such as the Institutional<br />

o Owners Association <strong>for</strong> Regulatory Issues in the Stock Market and the<br />

Swedish Corporate Governance Board<br />

o Building relations and working closely with Swedish and international<br />

investors<br />

o Focus on environmental and ethical issues <strong>AP3</strong>'s policy is to<br />

encourage companies in which we invest to take responsibility <strong>for</strong> the<br />

environmental and social impact of their business activities.<br />

Environment and social responsibility<br />

<strong>AP3</strong> believes there is a connection between corporate ethics and the capacity to deliver longterm shareholder value. Our core<br />

values are founded on international conventions signed by the Swedish government and and its support <strong>for</strong> initiatives such as<br />

the United Nations Global Compact and the OECD Guidelines <strong>for</strong> Multinational Enterprises. Sweden is a signatory to many<br />

international conventions, covering areas such as human and labour rights, corruption and inhumane weapons. Our ethical and<br />

environmental policy is based on the core values of the Swedish state, <strong>for</strong> which democracy and equality are paramount.<br />

Active governance is <strong>AP3</strong>'s primary tool <strong>for</strong> environmentally and ethically responsible investment. In rare cases, we may<br />

exclude companies from the portfolio if they fail to meet the standards required under our corporate governance policy.<br />

Copyright ©2011 PRI Association. All rights reserved. page 5 / 33

<strong>AP3</strong> has a twostep system <strong>for</strong> incorporating environmental and ethical considerations in our investment activities.<br />

1. Ethical screening to establish if any of the companies in the portfolio are acting in contravention of international conventions.<br />

2. Ethical risk analysis to establish the environmental and social risks to which portfolio companies are exposed and how the<br />

companies manage these risks.<br />

This process is designed a) to ensure that <strong>AP3</strong> has no investments in companies that contravene international conventions, and<br />

b) to guarantee that the Fund is aware of the environmental and social risks pertaining to companies in which we are a major<br />

shareholder. <strong>AP3</strong> will initiate discussions with a company if a deficiency comes to light.<br />

<strong>AP3</strong>'s ethical risk analysis focuses on companies in which we hold relatively large shareholdings. These are primarily<br />

businesses based in Sweden.<br />

Joint Ethical Council of the AP funds<br />

AP1, AP2, <strong>AP3</strong> and AP4 have a joint Ethical Council that handles issues of environmental and ethical compliance at <strong>for</strong>eign<br />

companies in which they hold shares. <strong>AP3</strong>'s screening of its listed equity portfolio takes place largely through the Ethical<br />

Council.<br />

The Ethical Council seeks to persuade companies to refrain from infringing conventions and to introduce groupwide preventive<br />

measures to prevent future breaches.<br />

The Ethical Council also seeks to influence companies by voting at AGMs, file shareholder resolutions and working with other<br />

investors that share a similar approach. The council also supports industry and investor initiatives aimed at improving<br />

transparency and protecting shareholders' interests.<br />

Q 12 Do you have a policy or a set of policies that make specific reference to responsible investment, and<br />

if so, do they cover environmental, social, and governance issues?<br />

Please select "Yes" or "No":<br />

If "Yes", which issue(s) does it cover?<br />

Yes<br />

Environmental<br />

Social<br />

Governance<br />

Q 13 For the following asset classes, to what extent has your policy or approach to responsible investment<br />

been incorporated into internal management processes (e.g. business planning, strategic planning, or<br />

similar)?<br />

Extent that your approach has been<br />

incorporated into internal<br />

management processes<br />

Asset class<br />

Listed equity (developed markets)<br />

Listed equity (emerging markets)<br />

Fixed income sovereign and other noncorporate<br />

issuers<br />

Private equity<br />

Nonlisted real estate or property<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Moderate<br />

Moderate<br />

Not at all<br />

Moderate<br />

Moderate<br />

Copyright ©2011 PRI Association. All rights reserved. page 6 / 33

Q 14 Within your organisation:<br />

What roles are present?<br />

Who has a clear responsibility related to responsible investment implementation? and<br />

Are there incentives and/or training on RI/ESG issues?<br />

Roles present in<br />

your organisation<br />

Responsibilities<br />

on RI/ESG<br />

Please check all that apply<br />

Incentives<br />

Training<br />

Please choose among<br />

"Yes, <strong>for</strong> all", "Yes, <strong>for</strong> some" or "No"<br />

Board of trustees or board of<br />

directors and their<br />

committees<br />

Yes Yes N/A No<br />

Chief Executive Officer or<br />

Chief <strong>Investment</strong> Officer or<br />

equivalent<br />

Yes<br />

Yes<br />

No<br />

Yes, <strong>for</strong> all<br />

Other senior management<br />

Yes<br />

Portfolio managers Yes Yes<br />

Analysts Yes Yes<br />

Researchers<br />

RI or ESG specialist Yes Yes<br />

Other please specify:<br />

No<br />

No<br />

No<br />

Yes, <strong>for</strong> some<br />

Yes, <strong>for</strong> some<br />

Yes, <strong>for</strong> all<br />

Q 15 Select any of the following RI, ESG and/or SRI approaches that you or your external investment<br />

managers currently apply in the investment decision making process.<br />

Please note that this question helps determine which questions you will be asked in subsequent sections,<br />

so please carefully review the definition of each possible answer.<br />

Please select all those that are relevant<br />

(columns are visible based on your answer<br />

to Q8 on asset classes breakdown)<br />

Internally managed<br />

Externally managed<br />

Exclusion based on ethical criteria<br />

Screening as a way to avoid the potential<br />

negative publicity surrounding the<br />

companies/sectors in question as it may<br />

adversely reflect on you or your manager's<br />

brand/license to operate<br />

Screening based on a belief that exclusion<br />

or inclusion of certain investments from<br />

your investment universe can have a<br />

material effect on portfolio per<strong>for</strong>mance<br />

ESG analysis within individual investment<br />

decisions, possibly including these factors<br />

into valuation and investment per<strong>for</strong>mance<br />

models<br />

Themed investing<br />

None of the above (this reply excludes any<br />

of the above)<br />

Copyright ©2011 PRI Association. All rights reserved. page 7 / 33

Q 16 Please indicate which of the following thematic investment strategies your organisation employs?<br />

Cleantech<br />

Please select all that apply<br />

Microfinance<br />

Sustainable <strong>for</strong>estry<br />

Global health<br />

Water<br />

Other (1) please specify:<br />

Green buildings/sustainable real<br />

estate<br />

Other (2) please specify:<br />

Green bonds<br />

Other (3) please specify:<br />

Other (4) please specify:<br />

Other (5) please specify:<br />

Q 17 Please select any of the following active ownership activities that you, your external service<br />

providers or your external investment managers have undertaken in 2010 on behalf of your organisation?<br />

Please note that this question helps determine which questions you will be asked in subsequent sections,<br />

so please carefully review the definition of each possible answer.<br />

(Proxy) voting related to listed equity investments in<br />

the following asset classes: Listed equity<br />

(developed markets), listed equity (emerging<br />

markets), or listed real estate/property (including<br />

the votes on listed securities held in hedge funds).<br />

File and/or cofile shareholder resolutions on listed<br />

companies.<br />

Engagement on ESG issues with listed equity or<br />

fixed income issuers in the following asset classes:<br />

listed equity (developed markets), listed equity<br />

(emerging markets), listed real estate/property,<br />

listed securities held in hedge funds, or fixed<br />

income corporate issuers.<br />

Ownership and engagement activities focused on<br />

ESG issues related to investments in the following<br />

asset classes: Listed equities which permit a<br />

significant control, sovereign and other noncorporate<br />

fixed income, private equity, non listed<br />

real estate/property, hedge funds, infrastructure, or<br />

other.<br />

None of the above (this reply excludes any of the<br />

above).<br />

You may select any approach you or your<br />

external managers, service providers or<br />

partner entities adopt on your behalf<br />

Copyright ©2011 PRI Association. All rights reserved. page 8 / 33

Q 18 Please add any overall comments and clarifications related to governance, policy and strategy here.<br />

Please see our web site http://www.ap3.se/sites/english/<strong>AP3</strong>_as_owner/Pages/Corporategovernacereports.aspx where our<br />

corporate governance policy, yearly AGM reports and approach to ethical and environmental consideration is practised.<br />

See also www.ethicalcouncil.com where the strategy and work, companies and initiatives we are engaged in are disclosed,<br />

including annual reports, of the AP fund's joint Ethical council is presented.<br />

Copyright ©2011 PRI Association. All rights reserved. page 9 / 33

Principle 1 We will incorporate ESG issues into investment analysis and decisionmaking processes.<br />

This section focuses on the integration of ESG considerations into the investment process. The questions are split into three<br />

sections. Only questions relevant to your organisation will be displayed, based on your responses to Q 8 (your investment<br />

management structure and asset class breakdown).<br />

The three sections are:<br />

I. Internally and actively managed investments;<br />

II.<br />

III.<br />

Externally and actively managed investments; and<br />

Passively (both internally and externally) managed investments.<br />

Some questions in this section are scored. Any question that is scored, but is not relevant to your organisation, based on your<br />

investment management structure and asset class breakdown or other responses, will not affect your overall score <strong>for</strong> Principle 1.<br />

You do not need to complete Principle 1 questions be<strong>for</strong>e completing questions <strong>for</strong> other <strong>Principles</strong>. While completing this section<br />

you are free to navigate to any of the other sections of the survey without losing answers already completed.<br />

Definitions<br />

Please note that this section of the survey focuses on investment decisionmaking processes and how ESG issues are integrated<br />

in these processes. It does not address the integration of ESG issues in other parts of your organisation and/or activities, such as<br />

the running of offices (e.g. how you manage your own organisation's waste) or your organisation's collaboration with other<br />

investors on ESG issues.<br />

ESG Integration, as addressed in this section of the survey, relates to the consideration of ESG issues alongside<br />

traditional financial measures, based on the belief that ESG issues can affect the per<strong>for</strong>mance (risk and/or return) of<br />

investment portfolios (to varying degrees across companies, sectors, regions, and asset classes and through time).<br />

Integration is considered to be:<br />

screening based on the belief that exclusion or inclusion of certain investments in the investable universe can effect materially<br />

on the portfolio's financial per<strong>for</strong>mance; and/or<br />

ESG analysis within individual investment decisions based on the belief that such analysis can effect materially on the<br />

investment's financial per<strong>for</strong>mance.<br />

Please note the view that ESG issues can influence investment returns based either on:<br />

1. The premise that per<strong>for</strong>mance on these issues will eventually be reflected in financial and operational outcomes and that<br />

externalised costs in the future will be priced and have an impact on revenue growth, margins, etc.; or,<br />

2. The premise that the way in which the market rates or prices the stock will be affected even in the absence of an impact on<br />

financial or operational per<strong>for</strong>mance.<br />

Exclusion of stocks or sectors from portfolios or downweighting them based on the possibility that an association with the stocks<br />

may adversely affect the owners profile or brand amongst stakeholders is not regarded as integration. Also, exclusion based on<br />

ethical considerations of sectors is not considered ESG integration. However, screening based on norms that are believed to be<br />

material in the investment process are included in the above definition of integration.<br />

Copyright ©2011 PRI Association. All rights reserved. page 10 / 33

Q 19 Please provide a description of your organisation's approach to this Principle. For example, how do<br />

your organisation's investment analysis and decisionmaking processes incorporate ESG issues?<br />

If your assets are managed both internally and externally, please describe how you address this in both<br />

portions of your assets. In addition, please describe any activities you may be doing to integrate ESG<br />

issues into the management of those investments that passively track indices (if you use this approach).<br />

Note that this text in addition to being part of the full survey will also be part of the Executive Summary<br />

of the survey. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong><br />

each of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

We believe that well governed companies per<strong>for</strong>m better in the long term and are there<strong>for</strong>e a better long term investment. As a<br />

long term investor we consider ESG to be important issues in order to create long term values in companies.<br />

We screen our internal and external equity portfolio to identify convention breaches. We engage in dialogues with companies<br />

that are breaching international conventions. We support investor initiatives aimed at increasing transparency, adopting best<br />

practices, protect shareholder rights and influence policy makers.We conduct proactive dialogues with companies on ESG<br />

issues. We use our voting rights. We have part of the portfolio invested in environmental investments such av clean tech, green<br />

bonds, sustainable <strong>for</strong>est, green buildings, wind mills.<br />

We are working on integrating ESG on a broader basis in our portfolio and it is an ongoing work. Having a large amount of<br />

passive investments and alpha separation (short investment horizon) makes integration of ESG challenging. We there<strong>for</strong>e use<br />

voting, reactive dialogues and support of investor initatives as a way to integrate ESG in that part of the portfolio. We also<br />

ecourage our external managers to sign or adopt PRI principles in order to integrate ESG.<br />

Q 20 What percentage, by asset class, of your organisation's assets under active management internally<br />

integrate the consideration of RI/ESG issues in investment decision making processes such as<br />

researching ESG in<strong>for</strong>mation and/or constructing/managing portfolios and to what extent?<br />

Please note that the percentages requested here are different from the data in Q8.<br />

Asset class<br />

What percentage of<br />

assets under active<br />

management<br />

internally (see<br />

example in notes)<br />

(+/ 5 per cent is<br />

sufficient)<br />

Research<br />

(gathering and<br />

analysing)<br />

Portfolio<br />

construction and<br />

management<br />

If percentage is greater than zero,<br />

please select: "Large", "Moderate",<br />

"Small" or "Not at all"<br />

Listed equity (developed markets)<br />

100 %<br />

Moderate<br />

Moderate<br />

Nonlisted real estate or property<br />

100 %<br />

Small<br />

Moderate<br />

Q 21 For the assets under active management internally that integrate the consideration of RI/ESG issues,<br />

to what extent do you have a process <strong>for</strong> monitoring the capability of investment analysts, portfolio<br />

managers and other relevant investment professionals on how they integrate the consideration of RI/ESG<br />

issues into investment analysis and decisionmaking processes?<br />

Applies only to investments that include integration of RI/ESG issues as indicated in Q20.<br />

Monitoring<br />

Asset class<br />

Listed equity (developed markets)<br />

Nonlisted real estate or property<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Moderate<br />

Moderate<br />

Copyright ©2011 PRI Association. All rights reserved. page 11 / 33

Q 22 What percentage, by asset class, of your organisation's assets under active management externally<br />

did you specify contractually or via other agreement that the consideration of RI/ESG issues be<br />

integrated into the investment decisionmaking processes of your external investment managers?<br />

For these assets, what is the extent of integration you agreed upon and to what extent do you monitor<br />

such integration?<br />

Please note that the percentages requested here are different from the data in Q8.<br />

Asset class<br />

Assets under active<br />

management<br />

externally<br />

(see example in notes)<br />

(+/ 5 per cent is<br />

sufficient)<br />

Agreed RI/ESG<br />

integration<br />

Please select:<br />

"Large",<br />

"Moderate" or "Small"<br />

Monitor<br />

Please select:<br />

"Large", "Moderate",<br />

"Small" or "Not at all"<br />

Listed equity (developed markets)<br />

100 %<br />

Moderate<br />

Moderate<br />

Listed equity (emerging markets)<br />

100 %<br />

Moderate<br />

Moderate<br />

Private equity 50 % Moderate Moderate<br />

Q 23 When searching <strong>for</strong> and selecting external investment managers <strong>for</strong> your current portfolio, to what<br />

extent did your organisation consider the capabilities of external investment managers to consider<br />

RI/ESG issues?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select:<br />

Moderate<br />

Q 24 Has your organisation directly, or via a mandate with an external manager, requested that any<br />

passive index tracking investments be managed relative to indexes that are constructed using relevant<br />

ESG issues?<br />

Please select: "Yes" or "No"<br />

Please select:<br />

No<br />

Please add any other comments regarding how you are, or are not, addressing ESG issues in your passively managed<br />

investments.<br />

We have looking into the possibility to using ESG indices but have not made a decison to use these indices yet. However, we<br />

believe that we through supporting different investor initatives, voing and screening can "add value " to passive investments.<br />

Q 25 Please add any overall comments and clarifications related to Principle 1 here. Please also describe<br />

any significant activities relating to Principle 1 not already captured by your answers above.<br />

This is the principle that provides most challenges, especially since large part of the portfolio is externally managed and/or<br />

passively managed.<br />

Our business model with alpha/beta separation provides another challenge. Alpha has been separated and investment horizon<br />

of these absolute return startegies is very short which means ESG is difficult to include to make sense.<br />

It is also a challenge to integrate ESG in all asset classes.<br />

Copyright ©2011 PRI Association. All rights reserved. page 12 / 33

Principle 2 We will be active owners and incorporate ESG issues into our ownership policies and<br />

practices.<br />

This section is focused on active ownership and is divided into three parts. You will see only those questions relevant to your<br />

organisation.<br />

The first part addresses voting related to listed investments. The second part addresses nonvoting engagement activities<br />

undertaken by your organisation or on your behalf by third parties with listed equity and corporate fixed income issuers. For the<br />

purpose of this survey, the term 'engagement' refers to nonvoting contact with companies to discuss concerns regarding ESG<br />

issues. The third part addresses ownership and engagement practices <strong>for</strong> other asset classes such as sovereign and other noncorporate<br />

fixed income issuers, private equity, nonlisted real estate/property, hedge funds, and infrastructure. This third section<br />

also covers any listed equities where investors have significant control (as defined in Q9, explanatory note [B]).<br />

The third section is necessary to account <strong>for</strong> the differing levels of influence that investors may acquire when investing in other<br />

asset classes versus those of listed equities.<br />

The contents and parts <strong>for</strong> this section of the survey are there<strong>for</strong>e:<br />

1. Voting and engagement activities related to listed equity investments undertaken by:<br />

A. internal staff;<br />

B. external parties (e.g., service providers and external managers).<br />

2. Engagement activities related to corporate fixed income issuers;<br />

3. Ownership and engagement activities <strong>for</strong> sovereign and other noncorporate fixed income, private equity, nonlisted real<br />

estate and property, hedge funds, and infrastructure, as well as listed equities when they represent significant control.<br />

While completing this section you are free to move to any of the other sections of the survey without losing work already done.<br />

Please note that <strong>for</strong> this survey, proxy voting activities entail any casting of votes at AGMs and the filing or cofiling of resolutions.<br />

Engagement activities refer to all interactions with investee companies that are not related to voting activities. Engagement<br />

activities should seek to achieve relevant in<strong>for</strong>mation and promote better ESG per<strong>for</strong>mance by companies. Such activities involve<br />

usually written communications, phone calls and meetings with management. For indirect investors in certain asset classes,<br />

such as private equity, infrastructure, and nonlisted real estate, active ownership may not be possible with the underlying asset.<br />

Active ownership in this case should be viewed as engaging with third party managers to consider and interact on ESG issues<br />

with underlying holdings. Working with governments to modify laws, rules and regulations in favour of ESG issues should not be<br />

counted as engagement in this part of the survey and it will be addressed separately in Principle 4 and 5.<br />

Copyright ©2011 PRI Association. All rights reserved. page 13 / 33

Q 26 Please provide a description of your organisation's approach to this Principle. For example, how is<br />

your organisation an active owner and how does it incorporate ESG issues in its ownership policies and<br />

practices?<br />

Describe both your voting activities and any other engagement activities you undertake across the<br />

different asset classes you hold.<br />

Note that this text in addition to being part of the full survey will also be part of the Executive Summary<br />

of the survey. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong><br />

each of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

We engage on different levels.<br />

1) We engage with domestic companies regarding ESGissues. We engage in dialogues with domestic companies of board<br />

issues, governance issues and we take part in a number of nomination committes. We engage in domestic companies to<br />

ensure they have risk assesments and procedures regarding E&Sissue in place.<br />

2) We vote in a part of our Swedish and <strong>for</strong>eign equity portfolio. We cofile/file resolutions on ESG issues or vote on existing<br />

ESG resolutions.<br />

3) We engage as responsible owners with <strong>for</strong>eign companies together with AP1AP4 through the Ethical council. We engage in<br />

dialogues with companies that are accused of breaching international conventions.<br />

4) We engage, mainly throgh the Ethical Council, in proactive initaitives in <strong>for</strong>eign companies to promote increased<br />

transparency, incrased climate risk awareness and adoptation of best practice (<strong>for</strong> example Global Compact).<br />

The Ethical Council applies a systematic process <strong>for</strong> identifying where active management will reap the greatest benefit. The<br />

process helps us to ensure a good spread of issues, geographical locations and assets, so that not all of the work<br />

is derived from the same industry or relate to the same issues. The working method of the Ethical Council is based on a<br />

monitoring of the portfolios of the four AP Funds <strong>for</strong> violations of international conventions. The goal of the Ethical Council is to<br />

conduct an active dialogue with companies that breach conventions, with a view to driving them to take action. The examination<br />

is carried out with the help of an external consultant who, on a daily basis, seeks out and gathers in relevant in<strong>for</strong>mation from a<br />

large number of sources, including various UN sources, the media and reports from a range of voluntary and stakeholder<br />

organisations.<br />

The shareholdings of the AP Funds are matched against this database and in cases of reported incidents involving violations of<br />

international conventions, these companies are investigated further. The task of the consultant is to verify the<br />

sources and make contact with the company <strong>for</strong> their comments on the reported violations. Of the companies with verified<br />

violations, a number are chosen by the Ethical Council and become the subject of a dialogue. A dialogue may last <strong>for</strong> several<br />

years, but as long as it continues to move <strong>for</strong>ward and the Ethical Council believes in the possibility of influencing the company<br />

in a positive direction, the Council is willing to devote time and resources to the dialogue.<br />

On behalf of the Ethical Council and other clients, the consultant maintains a<br />

dialogue with the companies with which the Ethical Council has chosen not to enter into direct dialogue, but where suspected<br />

or confirmed violations have been reported. When the Ethical Council removes companies from its dialogue list as a result of the<br />

objective of the dialogue being achieved or the company being excluded, the Council then opens a direct dialogue with new<br />

companies. The Ethical Council receives ongoing in<strong>for</strong>mation on new incidents and monitors the progress of all company<br />

dialogues and incidents.<br />

Although a large number of sources are monitored, there is naturally always a risk<br />

that something might be missed. If the Ethical Council receives in<strong>for</strong>mation about a<br />

violation by some other means, this is integrated into the same systematic process as the other in<strong>for</strong>mation.<br />

5) <strong>AP3</strong> collaborates on its own or through the Ethical Council with other investors on ESG related issues, either by supporting<br />

industry initiatives, dialogue with companies or intitaives to support shareholder rights.<br />

Q 27 Do you have a (proxy) voting policy, and, if so, does it address environmental, social and governance<br />

(ESG) issues?<br />

Do you have a voting policy?<br />

If Yes, please select all that apply:<br />

Yes<br />

Environmental<br />

Social<br />

Governance<br />

Copyright ©2011 PRI Association. All rights reserved. page 14 / 33

Q 28 For listed equities, please indicate the ratio of (proxy) votes cast, either directly or via third parties<br />

(such as an external service providers or external investment manager), against those you could have<br />

cast in 2010 <strong>for</strong> at least one of the following measures:<br />

by ballots item or resolution;<br />

by meetings (e.g. AGMs, EGMs, special);<br />

by listed assets under management.<br />

Please answer <strong>for</strong> at least one of these measures,<br />

if available please provide others as well<br />

Ballot items Meetings Listed assets<br />

We do not track our<br />

listed equity voting<br />

activities<br />

Actually cast vs. all you<br />

could have cast<br />

% 15 % %<br />

Q 29 For listed equities, who makes voting decisions on behalf of your (or your client's) organisation?<br />

Please rank the importance of the different groups listed below based on the proportion of decisions<br />

made by that group.<br />

Please note that subsequent questions will be asked specifically on the group that you list as most<br />

important and if specified of the second and third most important. Only the activities of the most<br />

important will be scored.<br />

Most important:<br />

Second most important:<br />

Third most important:<br />

Please select from:<br />

"Internal investment manager or other internal staff"<br />

"Internal voting or governance group"<br />

"External investment manager"<br />

"External proxy voting service"<br />

"External service provider" or<br />

"Other third party voting support entity"<br />

Internal voting or governance group<br />

External proxy voting service<br />

External service provider<br />

Q 30 For those listed equity votes you cast:<br />

a. to what extent is in<strong>for</strong>mation related to voting items gathered and analysed be<strong>for</strong>e voting decisions<br />

are made; and<br />

b. do you monitor whether voting is done in accordance with your voting instructions?<br />

a. In<strong>for</strong>mation gathered and analysed b. Monitor voting<br />

Please select<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Large<br />

Please select<br />

"Yes, <strong>for</strong> all", "Yes, <strong>for</strong> some" or<br />

"No, we make no ef<strong>for</strong>t to ensure"<br />

Yes, <strong>for</strong> all<br />

Copyright ©2011 PRI Association. All rights reserved. page 15 / 33

Q 31 Do you proactively in<strong>for</strong>m your listed equity companies of your rationale when you abstain or vote<br />

against management recommendations?<br />

Please select one:<br />

Yes, <strong>for</strong> some<br />

If "Yes", please indicate how this disclosure is communicated to companies.<br />

If answering "No", please explain why.<br />

We in<strong>for</strong>m or rationale if we vote against the Boards proposal either by sending a letter or by talking to the Board of Directors.<br />

We disclose our rational to the public on how we casted our votes in domestic companies by publishing a corporate governance<br />

report once a year.<br />

Swedish reports http://wwwap3admin/<strong>AP3</strong>somagare/Sidor/Ägarrapporter.aspx<br />

English (Summary) reports:<br />

http://wwwap3admin/sites/english/<strong>AP3</strong>_as_owner/Pages/Corporategovernacereports.aspx<br />

Q 33 For listed equity votes that your external manager or service provider casts on your behalf, to what<br />

extent did you monitor that voting decisions were analysed and made in accordance with your (proxy)<br />

voting policy?<br />

Please select<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select one:<br />

Large<br />

Q 34 How does your listed equity securities lending programme address voting?<br />

Please select one:<br />

Other, please specify:<br />

We recall all Swedish shares <strong>for</strong> voting, we recall some <strong>for</strong>eign shares.<br />

Q 35 To what extent do you and/or your agents review shareholder resolutions put <strong>for</strong>ward by other<br />

shareholders to determine whether or not to support the resolution?<br />

Please select<br />

"Large", "Moderate", "Small", "Not at all" or<br />

"We do not vote on shareholder resolutions"<br />

Voting managed internally<br />

Voting managed externally<br />

Large<br />

Large<br />

Copyright ©2011 PRI Association. All rights reserved. page 16 / 33

Q 36 How many shareholder resolutions related to ESG issues did you file or cofile during 2010 and, of<br />

these, what percentage were:<br />

voted on by shareholders?<br />

withdrawn due to changes at and/or negotiations with the company?<br />

withdrawn with no changes at the company in 2010?<br />

As Lead filer<br />

As Cofiler<br />

Number of ESG shareholder resolutions filed 0 1<br />

Of these:<br />

Of these led<br />

shareholder<br />

resolutions<br />

Of these cofiled<br />

shareholder<br />

resolutions<br />

Voted on %<br />

100 %<br />

Withdrawn due to changes at and/or negotiations<br />

with the company<br />

% 0 %<br />

Withdrawn <strong>for</strong> other reasons, please specify: % 0 %<br />

Total percentage (must be 100%) 0 %<br />

100 %<br />

Please explain why you filed or cofiled any shareholder resolutions related to RI/ESG issues during 2010.<br />

Cofiling resolutions is sometimes an efficient tool to put pressure on a compaany when the dialogue with the company doesn't<br />

move in the desired direction. Equally important as filing /cofiling is to vote on other resolutions and there<strong>for</strong>e it is useful to have<br />

the PRI Clearinghouse in<strong>for</strong>m about upcomming resolutions. (Such as the CERES initiative which we have supported)<br />

Q 37 Do you have a written engagement policy or other documents that direct engagement with listed<br />

equity and fixed income issuers; if so, do these policies address environmental, social and governance<br />

(ESG) issues?<br />

Engagement policy or<br />

other documents<br />

Do they address E, S or G<br />

Asset class Please select "Yes" or "No" Please select all that apply<br />

Listed equities Yes Environmental<br />

Social<br />

Governance<br />

Copyright ©2011 PRI Association. All rights reserved. page 17 / 33

Q 38 Who engages with listed equity or fixed income issuers on behalf of your (or your client's)<br />

organisation? Please rank the importance of the different groups listed below based on the engagements<br />

undertaken by that group.<br />

Please note that subsequent questions will be asked specifically on the groups that you list here. Only the<br />

activities of the most important will be scored (except <strong>for</strong> question 39 where all will be scored).<br />

Most important:<br />

Second most important:<br />

Third most important:<br />

Fourth most important:<br />

Please select from:<br />

"Internal staff"<br />

"External engagement service provider(s)"<br />

"External investment manager(s) "<br />

"Other external entity"<br />

Internal staff<br />

External engagement service provider(s)<br />

External investment manager(s)<br />

Other external entity (specify below)<br />

If "Other external entity" is selected, please list it here.<br />

Othr external entity CDP , who engages with large number of companies worldwide and that we support<br />

Q 39 In total, how many listed equity and fixed income issuers did your organisation engage with or were<br />

engaged with on your organisation's behalf on ESG issues in 2010, by level of engagement?<br />

Please do not double count. Engagements that are listed in one column should not<br />

be repeated in another. Choose to list them where the highest level of ef<strong>for</strong>t is<br />

being applied. Consider both individual and collaborative engagements carried out<br />

during the year.<br />

Internal staff<br />

External<br />

enagement<br />

service<br />

provider(s)<br />

External<br />

investment<br />

manager(s)<br />

Other<br />

external entity<br />

Extensive engagement 65 48 0<br />

Moderate engagement 171 123 0<br />

Basic engagement 106 24 4974<br />

We do not track these<br />

engagement activities<br />

Q 40 Approximately what proportion of the engagements with listed equity or fixed income issuers<br />

undertaken by your organisation or on your organisation's behalf addressed environmental, social or<br />

governance (ESG) issues?<br />

(+/ 5% rounding is sufficient)<br />

Internal staff<br />

External<br />

enagement<br />

service<br />

provider(s)<br />

External<br />

investment<br />

manager(s)<br />

Other<br />

external entity<br />

Environmental 33 % 21 % %<br />

100 %<br />

Social 33 % 74 % % 0 %<br />

Governance 33 % 5 % % 0 %<br />

We do not track these<br />

engagement activities<br />

Copyright ©2011 PRI Association. All rights reserved. page 18 / 33

Q 41 To what extent do you assess and monitor the ESG engagement competency and capabilities of the<br />

following groups?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Internal staff<br />

External engagement service provider(s)<br />

External investment manager(s)<br />

Other external entity<br />

Moderate<br />

Large<br />

Moderate<br />

Small<br />

Q 42 Given your (or your client's) engagement policy and/or approach to engagement, to what extent do<br />

you or do the third parties acting on your behalf, have a process <strong>for</strong> identifying and prioritising ESG<br />

related engagement opportunities?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Internal staff<br />

External engagement service provider(s)<br />

External investment manager(s)<br />

Other external entity<br />

Large<br />

Large<br />

Small<br />

Large<br />

Q 43 To what extent do you or your third party engagement providers or investment managers set ESG<br />

engagement objectives and evaluate engagement successes?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Internal staff<br />

External engagement service provider(s)<br />

External investment manager(s)<br />

Other external entity<br />

Moderate<br />

Large<br />

Not at all<br />

Large<br />

Q 44 To what extent do you or your external investment manager integrate the in<strong>for</strong>mation gained from<br />

ESG engagements into the investment decisionmaking process?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Internal staff<br />

External investment manager(s)<br />

Moderate<br />

Small<br />

Q 45 When searching <strong>for</strong> and selecting investment managers <strong>for</strong> your current portfolio, did you consider<br />

the capabilities of external investment managers to engage with companies on ESG issues on your<br />

behalf?<br />

Please select one:<br />

Yes, <strong>for</strong> more than half of our external investment managers<br />

Copyright ©2011 PRI Association. All rights reserved. page 19 / 33

Q 46 What percentage of engagements with listed equity and fixed income issuers that ended in 2010 were<br />

deemed successful?<br />

Internal staff<br />

External<br />

enagement<br />

service<br />

provider(s)<br />

External<br />

investment<br />

manager(s)<br />

Other<br />

external entity<br />

Engagement success 26 % 3 % % %<br />

What measures does your organisation or its external service provider(s) and or external manager use to assess the<br />

impact and success of engagement with listed equity and fixed income issuers, and how did you per<strong>for</strong>m in 2010<br />

based on those measures?<br />

On this question we have only measured succes on the cases were we had extensive engagement.<br />

Succesesful enagement is measured by preset goals.<br />

Our external engagement service provider has <strong>for</strong> each engagement case a set of revision criteria that a company needs<br />

to fulfil be<strong>for</strong>e the case will be revised. During 2010, two companies fulfilled the revision criteria which is outlined below.<br />

1. The violation has ceased;<br />

2. The company has adopted a responsible course of action;<br />

3.The company has taken a proactive and precautionary approach to improve routines and prevent future violations;<br />

4. The company's action is verifiable.<br />

Internal engagement Success is measusered in different ways. Engagement is usually a long term approach taht lasts <strong>for</strong><br />

several years. When we think an engagement is succesful it cn there<strong>for</strong>e be be success regarding partial goals although overall<br />

goals haven´t been achieved yet but the company through partial goals is stepping in a positive direction.<br />

We have not measured success reagrding Other external entity. However, the fact that CDP (other external entity) gets got<br />

response rate to their questionnaires is a proof of success. Moreover an increased number of compnaies have improved<br />

reporting and per<strong>for</strong>mance during the years which is another success <strong>for</strong> CDP.<br />

Q 47 Do you have an active ownership policy and/or strategy that addresses environmental, social and<br />

governance (ESG) issues <strong>for</strong> each of the following asset classes?<br />

Asset class<br />

Listed equity with significant control<br />

Policy and/or strategies address<br />

Environmental<br />

Social<br />

Governance<br />

Fixed income sovereign and other noncorporate<br />

issuers<br />

Private equity<br />

Nonlisted real estate and property<br />

Environmental<br />

Social<br />

Governance<br />

Environmental<br />

Social<br />

Governance<br />

Copyright ©2011 PRI Association. All rights reserved. page 20 / 33

Q 48 Per asset class, which role is most important in bringing <strong>for</strong>th active ownership activities on your<br />

behalf and, to what extent are ESG issues addressed by this role in these ownership activities?<br />

Asset class<br />

Listed equity with<br />

significant control<br />

Fixed income <br />

sovereign and other<br />

noncorporate issuers<br />

Select the most important:<br />

"Internal staff", "External engagement service<br />

provider(s)", "External investment manager(s)",<br />

"Other external entity" or "Nobody"<br />

Internal staff<br />

Nobody<br />

Please select the extent of<br />

active ownership activities:<br />

"Large", "Moderate" or "Small"<br />

<strong>for</strong> each of the categories selected<br />

Moderate<br />

Private equity Internal staff Moderate<br />

Nonlisted real<br />

estate/property<br />

Internal staff<br />

Moderate<br />

Q 49 To what extent do you assess and monitor ESG active ownership competency and capabilities<br />

undertaken by the groups listed below in the following asset classes: Listed equities with significant<br />

control, fixed income, sovereign and other noncorporate issuers, private equity, nonlisted real<br />

estate/property, hedge funds and infrastructure?<br />

Please select:<br />

"Large", "Moderate", "Small", "Not at all" or "Not applicable<br />

Internal staff<br />

External engagement service provider(s)<br />

External investment manager(s)<br />

Other external entity<br />

Moderate<br />

Large<br />

Moderate<br />

Not applicable<br />

Q 50 Please describe your organisation's , your external service providers or your external investment<br />

manager's approach to addressing ESG issues in active ownership in the following asset classes. Please<br />

include a description of the processes used to ensure ESG issues are addressed, any metrics used to<br />

gauge success, the sources of your expertise and specific examples.<br />

Asset class<br />

Listed equity with<br />

significant control<br />

Fixed income sovereign<br />

and other noncorporate<br />

issuers<br />

Private equity<br />

Nonlisted real estate and<br />

property<br />

Please add your remarks<br />

We engage in dialogue with the companies. We participate in nomination committees in domestic<br />

companies whenever we are asked. We vote in part of our equity portfolio. We engage in active<br />

dialogues with companies on ESG issues.<br />

ESG issues are currently not addressed<br />

We invest in private equity companies/funds and not directly in the companies. We have during<br />

2010 asked all our external private equity managers how they take ESG into account when they do<br />

due diligence and when they monitor/work with portfolio companies: We have engaged in dialogue<br />

with some of the managers to address this issue further.<br />

ESG issues are addressed in direct dialogue with the two domestic real estate companies where<br />

we are large shareholders. We sit on the board in these two large real estate companies.<br />

We invest in timberland funds and threre we have FSCcertification or similair certification as a<br />

requirement.<br />

Copyright ©2011 PRI Association. All rights reserved. page 21 / 33

Q 51 Please add any overall comments and clarifications related to Principle 2 here. Please also describe<br />

any significant activities relating to Principle 2 not already captured by your answers above.<br />

Our services provider GES <strong>Investment</strong> Services provides indepth analysis through the GES Global Ethical Standard(r) including<br />

engagement activities and risk analysis. The method is based on a systematic screening of international companies regarding<br />

their compliance with international conventions and guidelines on environment, human rights, labour rights and corruption.<br />

Currently, GES <strong>Investment</strong> Services covers approximately 5500 listed companies. The collection of in<strong>for</strong>mation on incidents and<br />

companies is managed through search tools covering media and news reporting as well as NGO websites and databases<br />

globally.<br />

The screening process results in an observation list of around 120 companies and an engage/exclude list of approximately 50<br />

companies associated to incidents or activities in breach of international norms. Each of the cases has an engagement<br />

strategy with a clear process goal connected to a set of revision criteria. There is also an identified strategy and action plan to<br />

reach the goal. The engagement strategy further involves cooperation between owners in company meetings, resolutions etc.<br />

Besides the abovementioned lists, there are also approximately 25 companies that are producers of cluster munitions, land<br />

mines and nuclear weapons.<br />

An example of an engagement success includes the dialogue with Wesfarmers. In this case a constructive dialogue has led to<br />

the company looking into alternative production technologies <strong>for</strong> enhancing phosphate rock that currently is imported from the<br />

occupied Western Sahara.<br />

Bridgestone is another example of a positive engagement development after a long standing constructive dialogue over several<br />

years regarding labour conditions at their rubber plantation in Liberia. Recently the company has reached a new agreement with<br />

the union to improve working conditions on the plantation which should decrease the presence of child labour. The<br />

improvements have been awarded by US Department of Labour with the 2011 Iqbal Masih Award.<br />

A third example is China Mengniu, a company which has improved product health and safety by changing from mostly buying<br />

milk from small farmers that use "middlemen" to buying most of their milk from large farms. This way, product quality increases<br />

because there is less human intervention, which makes contamination less likely. Product quality is now controlled twice: first<br />

at the dairy centre of 2000 employees and later via spot tests in the shops. China Mengniu has also obtained certifications from<br />

ISO9001, ISO14000, OHSAS18001 and food safety control system GMP and HACCP.<br />

Copyright ©2011 PRI Association. All rights reserved. page 22 / 33

Principle 3 We will seek appropriate disclosure on ESG issues by the entities in which we invest.<br />

Principle 3 is about ensuring that in<strong>for</strong>mation related to ESG issues is disclosed by companies and other entities in your<br />

organisation's investment universe. It is closely related to your activities on Principle 1 and Principle 2.<br />

This section lists questions regarding:<br />

Who seeks ESG disclosure in<strong>for</strong>mation <strong>for</strong> your organisation;<br />

The level of detail and content that is sought;<br />

The in<strong>for</strong>mation you may be seeking regarding norms, standards, codes of conduct or international initiatives related to RI/ESG.<br />

While completing this section you are free to move to other sections of the survey without losing work you have already done.<br />

Q 52 Please provide a description of your organisation's approach to this Principle. For example, how<br />

does your organisation seek appropriate disclosure on ESG issues by the entities in which it invests?<br />

Note that this text in addition to being part of the full survey will also be part of the survey's Executive<br />

Summary. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong> each<br />

of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

We seek appropriate disclosure on ESG issues by the entities we invest in through public published material. This means that<br />

sustainability reports, home pages, annual reports and press releases from the companies we invest in are important. When we<br />

feel that there is a lack of disclosure and transparency we will in many cases engage in a direct dialogue with the companies or<br />

join investor initaitives that aim to increase the disclosure.<br />

We actively promote an support reporting on ESGissues: For example we support several investor initiatives (like CDP, EITI,<br />

Global compactinitiatives, Sustainable Value creation project ( A Swedish project directed to the 100 largest companies) etc).<br />

We also promote reporting ESG by using GRI. We actively ask companies to report on ESG.<br />

Q 53 Who asked <strong>for</strong> and/or collected from your organisation's investee companies (or other investment<br />

entities) in<strong>for</strong>mation about their ESG policies, practices or per<strong>for</strong>mance in 2010?<br />

Internal staff<br />

Please select all that apply<br />

External investment manager(s)<br />

External engagement service provider(s)<br />

External research providers<br />

Brokers / dealers<br />

Other please specify:<br />

Some not all external managers use ESG in their analysis. We<br />

have a large passive portfolio.<br />

None of the above: Investee companies, or other investment entities, were<br />

not asked to provide in<strong>for</strong>mation about their ESG policies, practices or<br />

per<strong>for</strong>mance in 2010 (please specify below why not)<br />

If investee companies were not asked, please specify why.<br />

Copyright ©2011 PRI Association. All rights reserved. page 23 / 33

Q 54 To what extent did you or your external agent(s) seek appropriate disclosure on ESG issues by the<br />

investees and, where necessary, encourage investee companies to produce standardised and/or<br />

systematic reporting about their ESG policies, practices or per<strong>for</strong>mance in 2010?<br />

Asset class<br />

Listed equity (developed markets)<br />

Listed equity (emerging markets)<br />

Fixed income sovereign and other noncorporate<br />

issuers<br />

Private equity<br />

Nonlisted real estate or property<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Large<br />

Large<br />

Not at all<br />

Large<br />

Moderate<br />

Q 55 In which <strong>for</strong>mat or mechanism have you or your third party agents requested reporting on ESG<br />

policies, practices or per<strong>for</strong>mance?<br />

Reporting <strong>for</strong>mats<br />

Please select all that apply<br />

Integrated with regular financial reports<br />

Standalone corporate (social) responsibility or sustainability reports<br />

Global Reporting Initiative (GRI)<br />

Carbon Disclosure Project (CDP)<br />

Global Framework <strong>for</strong> Climate Risk Disclosure<br />

Communication on Progress (COP) by the United Nations Global<br />

Compact<br />

Countrylevel company <strong>for</strong>m of the Extractive Industries Transparency<br />

Initiative (EITI)<br />

Submission of a tailored survey<br />

Other reporting framework by an industry or association please specify:<br />

Report on human rights and labour right issues (ILO)<br />

None of the above<br />

Q 56 To what extent did you or your third party agents seek in<strong>for</strong>mation from companies regarding their<br />

practices related to norms, standards, codes of conduct or international initiatives/ declarations/<br />

conventions related to ESG issues in 2010?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select:<br />

Large<br />

Copyright ©2011 PRI Association. All rights reserved. page 24 / 33

Q 57 Please add any overall comments and clarifications related to Principle 3 here. Please also describe<br />

any significant activities relating to Principle 3 that are not already captured by your answers above.<br />

<strong>AP3</strong> together with 14 other Swedish insitutional investors collaborated <strong>for</strong> the first time 2009/10 in a project regarding disclosure<br />

called "Sustainable Value Creation".<br />

The project used a questionnaire to find out how the 100 largest Swedish listed companies take responsibility <strong>for</strong> and work with<br />

sustainable business practices. The survey consisted of 26 questions distributed among four parts: accountability of the board,<br />

key policy documents, implementation and compliance, and communication and reporting. The response rate was very high, as<br />

84% of the companies answered the questionnaire.<br />

<strong>AP3</strong> has used the answers from the survey in dialogues with several of the participating companies during 2010. The survey and<br />

report can be downloaded fromhttp://www.ap3.se/sites/english/SiteCollectionDocuments/News/hallbart_vardeskapande_eng_%<br />

208feb.pdf<br />

In 2010 all participating companies were invited to a seminair hosted by <strong>AP3</strong> and the other 14 investors. the seminair also<br />

included a round table discussion to share experience with peer companies and investors.<br />

Copyright ©2011 PRI Association. All rights reserved. page 25 / 33

Principle 4 We will promote acceptance and implementation of the <strong>Principles</strong> within the investment<br />

industry.<br />

Principle 4 is about promoting the acceptance and implementation of the <strong>Principles</strong> <strong>for</strong> <strong>Responsible</strong> <strong>Investment</strong> (PRI) among your<br />

clients, service providers, partners, brokers/dealers and other investment industry players. In addition, it is about working with<br />

governments, regulators and international bodies to address and define approaches relating to ESG issues.<br />

While completing this section you are free to move to any of the other sections of the survey without losing work already done.<br />

Q 58 Please provide a description of your organisation's approach to this Principle. For example, how<br />

does your organisation promote the acceptance and implementation of the <strong>Principles</strong> within the<br />

investment industry?<br />

Please describe how you support the incorporation of ESG factors in the investment industry via<br />

mandates, incentives, Request <strong>for</strong> Proposals (RfPs), policy discussions etc. Please, indicate how your<br />

organisation does this in relation to clients and/or beneficiaries, peers or other entities.<br />

Note that this text in addition to being part of the full survey will also be part of the Executive Summary<br />

of the survey. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong><br />

each of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

We promoting and encourage other investors to adopt the PRI.<br />

We have over the years asked our external managers <strong>for</strong> reasons <strong>for</strong> not signing PRI and encouraged them to do so. During<br />

2010 we have had an extra focus on ourr private equity managers work with ESG and their view on PRI. Some of them have<br />

signed PRI after our talks and others might be interested. Moreover many of the managers have showed an interst and<br />

understanding of the importance of ESG integration in due diligence processes and portfolio managment work as well as<br />

reporting to investors, which I think is more on important than actually signing the PRI.<br />

PRI related questions have been part of RFPs during the past years. We encourage our peers to sign PRI. Two ways of<br />

encouraging peers and investors is through dialogue and by speaking on investor conferences.<br />

Copyright ©2011 PRI Association. All rights reserved. page 26 / 33

Q 59 Did you include RI/ESG considerations when working with service providers and/or external<br />

investment managers in 2010 (where applicable)?<br />

Specifically when:<br />

a. searching <strong>for</strong> service providers or external managers;<br />

b. agreeing on service requirements;<br />

c. structuring incentive schemes.<br />

Service providers or<br />

external managers<br />

Brokers / dealers<br />

a. Searches b. Agreements c. Incentives<br />

If you work with this type of service provider,<br />

please select "Yes, <strong>for</strong> all", "Yes, <strong>for</strong> some" or "No"<br />

No No No<br />

We do not work<br />

with this type of<br />

provider<br />

External engagement<br />

service provider<br />

Yes, <strong>for</strong> all<br />

Yes, <strong>for</strong> all<br />

No<br />

<strong>Investment</strong> consultant<br />

<strong>Investment</strong> research<br />

provider<br />

Proxy voting service<br />

provider<br />

Yes, <strong>for</strong> all<br />

Yes, <strong>for</strong> all<br />

No<br />

External investment<br />

manager<br />

Yes, <strong>for</strong> some Yes, <strong>for</strong> some No<br />

Other please specify:<br />

Q 60 To what extent did you encourage peer organisations and/or your institutional clients and/or other<br />

investment industry players to consider RI/ESG issues in 2010?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select:<br />

Large<br />

Q 61 Does your broker evaluation process (which determines how you allocate commissions to brokers)<br />

include an ESG component, and/or do you have a budget to pay <strong>for</strong> broker research on ESG issues?<br />

Please select:<br />

"Yes" or "No"<br />

Please select:<br />

No<br />

Q 62 To what extent do you identify ESG issues and suggest them to brokers or other investment<br />

research providers <strong>for</strong> research?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select:<br />

Not at all<br />

Copyright ©2011 PRI Association. All rights reserved. page 27 / 33

Q 63 To what extent did you engage in dialogue, lobbying or initiatives pertaining to government policy<br />

and/or industry regulations related to RI/ESG issues in 2010?<br />

Please select:<br />

"Large", "Moderate", "Small" or "Not at all"<br />

Please select:<br />

Moderate<br />

Q 64 Please add any overall comments and clarifications related to Principle 4 here. Please also describe<br />

any significant activities relating to Principle 4 not already captured by your answers above.<br />

We became members of the IIGCC in 2010. IIGCC plays an important role in working actively with policmakers.<br />

Copyright ©2011 PRI Association. All rights reserved. page 28 / 33

Principle 5 We will work together to enhance our effectiveness in implementing the <strong>Principles</strong>.<br />

Principle 5 is about collaborating with others in your implementation of responsible investment. The questions in this section are<br />

designed to capture the many ways in which signatories collaborate (<strong>for</strong> example by using the PRI Clearinghouse), and thus may<br />

overlap with areas discussed previously in the survey. However, the focus here is only those activities that involve working with<br />

others to implement the <strong>Principles</strong>.<br />

While completing this section you are free to move to any of the other sections of the survey without losing work already done.<br />

Q 65 Please provide a description of your organisation's approach to this Principle. For example, how<br />

does your organisation work with other parties to enhance its implementation of the <strong>Principles</strong>?<br />

Note that this text in addition to being part of the full survey will also be part of the Executive Summary<br />

of the survey. The Executive Summary is a separate document that will collate the text you provide <strong>for</strong><br />

each of the introductory sections of the survey (GPS and the six <strong>Principles</strong>).<br />

<strong>AP3</strong> believes that greater results can be achieved through collaboration with other owners. <strong>AP3</strong> there<strong>for</strong>e seek to cooperate<br />

with other shareholders when appropriate and in accordance with the Fund's corporate governance policy.<br />

<strong>AP3</strong> has together with three of the other AP funds (AP1, AP2 and AP4) <strong>for</strong>med an Ethical Council. The council coordinates the<br />

ES analysis of the environmental<br />

and ethical compliance in the <strong>for</strong>eign companies where the funds have holdings. The collaboration involves monitoring of the<br />

funds' investment portfolios<br />

with regard to violation of international conventions, analysis and dialogue with the portfolio companies. The Ethical Council<br />

gives international investors a<br />

powerful partner in Sweden with an active commitment to ethical and environmental aspects of corporate social responsibility.<br />

The Ethical Council is active in supporting investor initiatives aimed at encouraging<br />

companies to improve transparency, act more responsibly and address crucial ESG issues.<br />