STANLIB's Risk Profile Funds

STANLIB's Risk Profile Funds

STANLIB's Risk Profile Funds

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

STANLIB’s <strong>Risk</strong><br />

<strong>Profile</strong> <strong>Funds</strong><br />

the art and science of investing

STANLIB’s <strong>Risk</strong> <strong>Profile</strong>d <strong>Funds</strong> provide a managed<br />

solution for conservative to aggressive investors.<br />

How to maximize your wealth<br />

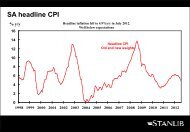

In the investment world, the quote “eat well, sleep well” refers to the trade off made between risk and return. The more risk one is able to stomach, the<br />

higher the potential return and thus the possibility of eating well. However, with risk there often exists great uncertainty and volatility, thus the possibility<br />

of sleepless nights. We all know the roller coaster ride of volatile equity returns too well! Look at the differences (volatility) in return from one year to<br />

another as per the graph below. Also note that most crashes were followed by two or three strong years.<br />

SA All Share Index return (%) 1960 to 2010<br />

1996<br />

1995<br />

1988 2010<br />

1984 2007 2004<br />

2002 2000 1983 2003 2001<br />

1998 1997 1974 1994 1991<br />

1976 1992 1973 1967 1982 2009 2005 1999<br />

1975 1990 1971 1966 1978 2006 1989 1993<br />

2008 1969 1987 1965 1964 1977 1985 1986 1979<br />

1970 1960 1981 1961 1963 1962 1980 1968 1972<br />

-30 to -20 -20 to -10 -10 to 0 0 to 10 10 to 20 20 to 30 30 to 40 40 to 50 Over 50<br />

Source: STANLIB<br />

Conversely, one can invest conservatively which means sleeping well, but the return will probably be lower which translates into not eating as well. If you<br />

have been saving for the last 10 years into the money market, you would in fact not have saved anything, once you have paid your taxes, and you have<br />

taken inflation into account.<br />

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 10 yr Avg.<br />

Cash Return 10.6 11.5 12.8 8.2 7.5 7.9 10.1 12.4 8.9 6.9 9.7<br />

After tax return (Assume rate of 40%) 6.4 6.9 7.7 4.9 4.5 4.7 6 7.4 5.3 4.1 6.2<br />

Inflation (CPI) 6.6 9.3 6.8 4.3 3.9 4.6 6.5 11.5 7.2 4.3 6.5<br />

Real Return -0.2 -2.4 0.9 0.6 0.6 0.1 -0.5 -4.1 -1.9 -0.2 -0.7<br />

Source: STANLIB<br />

So, how do you balance “eat well and sleep well”?<br />

The key decision you should make is how much risk you need to take and are comfortable taking. Consider the following:<br />

• Your appetite or attitude to risk – All things being equal, most people prefer lower risk to higher risk and most are risk averse.<br />

• Your need for risk - Your need for risk is assessed by examining the extent of any gap between the lifestyle you wish to lead and your expected financial<br />

resources available to meet that lifestyle.The required investment risk of the portfolio, most consistent with achievement of your lifestyle objectives,<br />

may not match the portfolio indicated by your risk profile score. If your need for risk suggests a more risky portfolio this raises an uncomfortable<br />

dilemma – do you “eat well or sleep well?” Neither, more risk (with uncertain outcomes) nor a lower expected lifestyle is particularly attractive.<br />

Without adequate discussion around these decisions, when growth assets are performing well the tendency is for most people to opt for higher risk than<br />

their risk profile indicates they would be comfortable with, rather than pare back lifestyle expectations. However, when the inevitable downturns occur<br />

these people often lose discipline and abandon sound financial strategies. Their short term desire for comfort and apparent safety jeopardizes their long<br />

term lifestyle aspirations.<br />

Asset allocation – the art of balancing <strong>Risk</strong> and Return<br />

What does asset allocation mean? It is an investment strategy that aims to balance risk and reward by apportioning your portfolio’s assets according to your:<br />

• Investment goals<br />

• <strong>Risk</strong> tolerance<br />

• Investment horizon<br />

The choice of an appropriate asset allocation is the most important decision you have to make. It is a choice about the investment risk you are prepared to<br />

take. It is the decision as to how to apportion your investments between:<br />

• Defensive assets i.e. cash and fixed interest; and<br />

• Growth assets i.e. shares and listed property

By investing in a diversified portfolio, (including cash, bonds, listed property and equities) the positive performance of some asset classes can help offset<br />

the negative performance of others. This approach reduces the volatility within a portfolio and guarantees that although you won’t be the top performer,<br />

you definitely won’t be the worse. As evident below, it is very difficult to pick the best performing asset class in a year.<br />

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010<br />

SA Equity<br />

32.6<br />

Property<br />

20.4<br />

Property<br />

38.7<br />

Property<br />

39.8<br />

SA Equity<br />

47.3<br />

SA Equity<br />

41.2<br />

Property<br />

22.9<br />

Bonds<br />

17<br />

SA Equity<br />

32.1<br />

Property<br />

26.8<br />

Global Equity<br />

30.2<br />

Bonds<br />

16<br />

Balanced<br />

Portfolio<br />

18.4<br />

Balanced<br />

Portfolio<br />

23.1<br />

Property<br />

38.6<br />

Global Equity<br />

31.1<br />

SA Equity<br />

19.2<br />

Cash<br />

11.7<br />

Balanced<br />

Portfolio<br />

21.7<br />

SA Equity<br />

19<br />

Balanced<br />

Portfolio<br />

24.9<br />

Inflation<br />

12.4<br />

Bonds<br />

18.1<br />

SA Equity<br />

25.4<br />

Balanced<br />

Portfolio<br />

35.1<br />

Balanced<br />

Portfolio<br />

28.1<br />

Balanced<br />

Portfolio<br />

15.6<br />

Inflation<br />

9.5<br />

Property<br />

17.4<br />

Balanced<br />

Portfolio<br />

17.8<br />

Bonds<br />

17.8<br />

Cash<br />

11.6<br />

SA Equity<br />

16.1<br />

Bonds<br />

15.3<br />

Global Equity<br />

21.1<br />

Property<br />

15.7<br />

Cash<br />

9.4<br />

Property<br />

-10.1<br />

Cash<br />

9.1<br />

Bonds<br />

15<br />

Cash<br />

10.2<br />

Balanced<br />

Portfolio<br />

1.4<br />

Cash<br />

12.3<br />

Cash<br />

8<br />

Bonds<br />

10.8<br />

Cash<br />

7.4<br />

Inflation<br />

9<br />

Balanced<br />

Portfolio<br />

-10.4<br />

Inflation<br />

6.2<br />

Cash<br />

6.9<br />

Property<br />

7.7<br />

SA Equity<br />

-8.3<br />

Global Equity<br />

1.8<br />

Inflation<br />

3.4<br />

Cash<br />

7.1<br />

Inflation<br />

5.8<br />

Bonds<br />

4.2<br />

Global Equity<br />

-21.7<br />

Global Equity<br />

1.14<br />

Inflation<br />

3.5<br />

Inflation<br />

4.6<br />

Global Equity<br />

-43.5<br />

Inflation<br />

0.33<br />

Global Equity<br />

-4.8<br />

Inflation<br />

3.6<br />

Bonds<br />

5.5<br />

Global Equity<br />

3.8<br />

SA Equity<br />

-23.2<br />

Bonds<br />

-1<br />

Global Equity<br />

-1.58<br />

* Balanced Portfolio: 60% Equities, 20% Bonds, 10% Listed Property and Cash<br />

Source: INET and Morningstar<br />

The STANLIB <strong>Risk</strong> <strong>Profile</strong> funds are aligned with these sound investment principles and<br />

offer you a one stop solution.<br />

Fund description<br />

STANLIB’s <strong>Risk</strong> <strong>Profile</strong>d Fund of <strong>Funds</strong> range provide a managed solution for conservative to aggressive investors. The asset allocation is actively managed<br />

within specific strategic asset class bands for each fund. The process in which funds are managed reflects STANLIB’s best investment view based on our<br />

tactical asset allocation calls. These are recommended in the STANLIB Fund Focus document.<br />

Strategic Asset Allocation Bands<br />

STANLIB Conservative<br />

Fund of <strong>Funds</strong><br />

STANLIB Moderately<br />

Conservative Fund of <strong>Funds</strong><br />

STANLIB Moderate<br />

Fund of <strong>Funds</strong><br />

STANLIB Moderately<br />

Aggressive Fund of <strong>Funds</strong><br />

STANLIB Aggressive<br />

Fund of <strong>Funds</strong><br />

Cash 40%-60% 20%-40% 15%-25% 5%-15% 0%-10%<br />

Bonds 20%-30% 20%-30% 20%-30% 10%-20% 0%-10%<br />

Property 0%-20% 0%-20% 0%-20% 0%-20% 0%-20%<br />

Equities 5%-20% 30%-40% 45%-55% 60%-75% 75%-95%<br />

How does a <strong>Risk</strong> <strong>Profile</strong> Fund actually work?<br />

Client’s Money<br />

Your investment is allocated into the various asset classes and underlying investment portfolios, according to your<br />

risk profile, and the tactical asset allocation.<br />

All the diversification is done for you, both asset classes as well as equity funds.<br />

Into one of the five <strong>Risk</strong><br />

<strong>Profile</strong> <strong>Funds</strong><br />

Cash 50%<br />

Bonds 20%<br />

Institutional Money Market Fund<br />

Bond Fund<br />

Conservative Fund<br />

Equity 10%<br />

ALSI 40<br />

Value Fund<br />

Growth Fund<br />

Financial Fund*<br />

Resourses Fund<br />

Small Cap Fund<br />

Property 20%<br />

Institutional Property Fund**<br />

* STANLIB Financials Fund has won the Morningstar Award 2010 for Equity - Financial Services<br />

** The STANLIB Property Income Fund was named as the top performer at this year’s prestigious Raging Bull Awards 2010

More about the Fund Manager<br />

Paul Hansen<br />

After completing articles at Alex Aiken and Carter, Paul joined UAL Merchant Bank in1979. He then worked in the US,<br />

mainly with Shearson Lehman Bros and returning to SA in 1992, joined Old Mutual and then RMB Asset Management.<br />

He joined SCMB Asset Management in 1995, and has been with STANLIB since the merger in 2002.<br />

Paul has won 9 Raging Bull awards during his time at SCMB and STANLIB.<br />

Fund Performance<br />

For the latest performance numbers for STANLIB’S <strong>Risk</strong> <strong>Profile</strong> <strong>Funds</strong>, refer to the fund fact sheets on the STANLIB website, or the STANLIB Weekly Focus.<br />

What are the advantages of investing in the STANLIB <strong>Risk</strong> <strong>Profile</strong> <strong>Funds</strong>?<br />

• A tailor-made solution according to your individual risk profile<br />

• Access to a well diversified fund across all four asset classes<br />

• Tactical Asset Allocation done once a quarter on your behalf, after rigorous debate from all the STANLIB investment specialists<br />

• The equity portion of the funds are well diversified across sectors and fund managers<br />

• The costs associated with the fund is low, you are getting all the benefits of a multi-manager fund, for a single manager fund charge<br />

• You do not incur CGT on any switches done within the fund<br />

• Low entry level into the world of investments – minimum investment of only R500 per month required<br />

In closing - what should a smart investor do?<br />

• Align your investment choices with your time horizon and investment objective<br />

• Do not attempt to pick “winners” i.e. shares, properties and fund managers<br />

• Do not attempt to time markets<br />

• Diversify broadly to reduce volatility i.e. have many holdings across all selected asset classes, rather than concentrations within any asset class; and<br />

• Choose an appropriate asset allocation and stick with it. Rebalance as required<br />

• Invest on a regular basis, this allows you to take advantage of what is known as “cost averaging”<br />

• Invest with a reputable company<br />

Disclaimer<br />

Collective Investment Schemes in Securities (CIS) are generally medium to long term investments. An investment in the participations of a collective investment scheme in securities is not the same as a deposit with<br />

a banking institution. The value of participatory interests may go down as well as up and past performance is not necessarily a guide to the future. CIS are traded at ruling prices and can engage in borrowing and scrip<br />

lending. A schedule of fees and charges and maximum commissions is available on request from the company/scheme. Commission and incentives may be paid and if so, would be included in the overall costs. A fund<br />

of funds is a portfolio that invests in portfolios of collective investment schemes, which levy their own charges, which could result in a higher fee structure for these portfolios.<br />

Forward pricing is used. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down.<br />

The manager is a member of the Association for Savings & Investment of South Africa (ASISA)<br />

Trustees: ABSA Bank Ltd. 6th Floor ABSA Towers North (6E1), 180 Commissioner Street, Johannesburg, 2001. Tel 011 350 4000<br />

Compliance number: 3783LN