Capital calculation methods

Capital calculation methods

Capital calculation methods

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

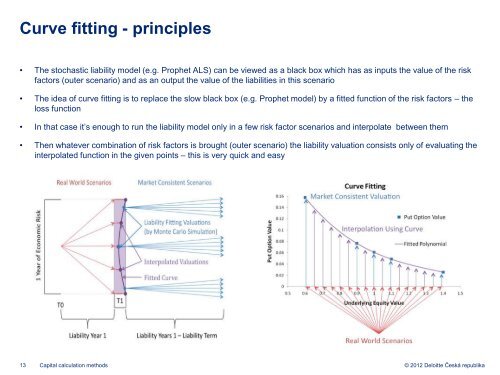

Curve fitting - principles<br />

• The stochastic liability model (e.g. Prophet ALS) can be viewed as a black box which has as inputs the value of the risk<br />

factors (outer scenario) and as an output the value of the liabilities in this scenario<br />

• The idea of curve fitting is to replace the slow black box (e.g. Prophet model) by a fitted function of the risk factors – the<br />

loss function<br />

• In that case it’s enough to run the liability model only in a few risk factor scenarios and interpolate between them<br />

• Then whatever combination of risk factors is brought (outer scenario) the liability valuation consists only of evaluating the<br />

interpolated function in the given points – this is very quick and easy<br />

13 <strong>Capital</strong> <strong>calculation</strong> <strong>methods</strong><br />

© 2012 Deloitte Česká republika