Commercial Loan Guaranty Agreements - Strafford

Commercial Loan Guaranty Agreements - Strafford

Commercial Loan Guaranty Agreements - Strafford

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

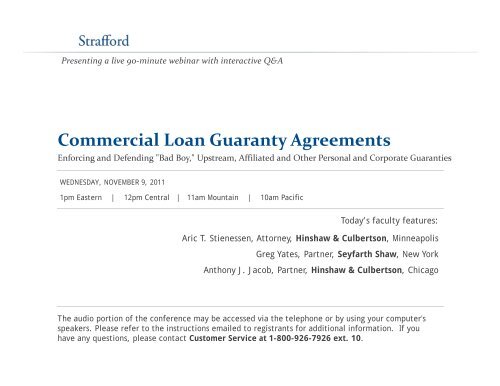

Presenting a live 90‐minute webinar with interactive Q&A<br />

<strong>Commercial</strong> <strong>Loan</strong> <strong>Guaranty</strong> <strong>Agreements</strong><br />

Enforcing and Defending "Bad Boy," Upstream, Affiliated and Other Personal and Corporate Guaranties<br />

WEDNESDAY, NOVEMBER 9, 2011<br />

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific<br />

Td Today’s faculty features:<br />

Aric T. Stienessen, Attorney, Hinshaw & Culbertson, Minneapolis<br />

Greg Yates, Partner, Seyfarth Shaw, New York<br />

Anthony J. Jacob, Partner, Hinshaw & Culbertson, Chicago<br />

The audio portion of the conference may be accessed via the telephone or by using your computer's<br />

speakers. Please refer to the instructions emailed to registrants for additional information. If you<br />

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials<br />

If you have not printed the conference materials for this program, please<br />

complete the following steps:<br />

• Click on the + sign next to “Conference Materials” in the middle of the left-<br />

hand column on your screen.<br />

• Click on the tab labeled “Handouts” that appears, and there you will see a<br />

PDF of the slides for today's program.<br />

• Double click on the PDF and a separate page will open.<br />

• Print the slides by clicking on the printer icon.

Continuing Education Credits<br />

FOR LIVE EVENT ONLY<br />

For CLE purposes, please let us know how many people are listening at your<br />

location by completing each of the following steps:<br />

• Close the notification box<br />

• In the chat box, type (1) your company name and (2) the number of<br />

attendees at your location<br />

• Click the SEND button beside the box

Tips for Optimal Quality<br />

Sound Quality<br />

If you are listening via your computer speakers, please note that the quality of<br />

your sound will vary depending on the speed and quality of your internet<br />

connection.<br />

If the sound quality is not satisfactory and you are listening via your computer<br />

speakers, you may listen via the phone: dial 1-866-871-8924 and enter your PIN -<br />

when prompted. Otherwise, please send us a chat or e-mail<br />

sound@straffordpub.com immediately so we can address the problem.<br />

If you dialed in and have any difficulties during the call, press *0 for assistance.<br />

Viewing Quality<br />

To maximize your screen, press the F11 key on your keyboard. To exit full screen,<br />

press the F11 key again.

<strong>Commercial</strong> <strong>Loan</strong><br />

<strong>Guaranty</strong> <strong>Agreements</strong><br />

Enforcing and Defending “Bad Boy,”<br />

Upstream, Affiliated and Other Personal and<br />

Corporate Guaranties<br />

November 9, 2011<br />

Aric T. Stienessen<br />

Anthony J. Jacob<br />

Greg Yates<br />

astienessen@hinshawlaw.com<br />

612-334-2504<br />

ajacob@hinshawlaw.com<br />

312-704-3105<br />

gyates@seyfarth.com<br />

212-218-3336

Presenters<br />

Aric T. Stienessen, Partner<br />

Hinshaw & Culbertson LLP, Minneapolis<br />

He represents lenders, investment banks and borrowers in commercial<br />

finance transactions. He also represents businesses and real property<br />

developers in sales and purchase transactions involving commercial<br />

real property, and handles transactions involving mergers,<br />

acquisitions, divestitures and corporate organization and governance.<br />

6<br />

6

Presenters<br />

Anthony J. Jacob, Partner<br />

Hinshaw & Culbertson, Chicago<br />

Mr. Jacob is engaged g in general corporate practice, including various<br />

aspects of private merger, acquisition, divestiture and employee<br />

benefit matters. In addition, Mr. Jacob’s practice includes secured and<br />

unsecured lending transactions, asset securitization and structured<br />

finance, ESOP loans, initial debt and equity offerings, primary and<br />

secondary debt offerings, corporate reorganizations and restructuring,<br />

joint ventures and syndicated commercial financing transactions. His<br />

clients include domestic and foreign corporations, limited it liability<br />

companies and partnerships, and banks and other lending institutions.<br />

7<br />

7

Presenters<br />

Greg Yates, Partner<br />

Seyfarth Shaw, New York<br />

A member of the Bankruptcy, Workouts & Reorganization Department,<br />

he is a trusted advisor to financial institutions as well as to noninstitutional<br />

lenders and investors. Mr. Yates’ national practice is<br />

concentrated in the area of debtor/creditor relations, including<br />

workouts, restructurings, and bankruptcy. A key focus of his practice is<br />

advising clients on creative solutions to distressed commercial real<br />

estate transactions and, if necessary, litigation relating to those<br />

transactions. ti In 2011, Mr. Yates was selected by the Turnaround<br />

Management Association as a recipient of its Transaction of the Year -<br />

Large Turnaround Award.<br />

8<br />

8

Outline<br />

I<br />

II.<br />

III. Bankruptcy Issues<br />

IV. Questions and Answers<br />

I. Overview of General Types of Guaranties<br />

General Legal Issues to Enforce and Defend Guaranties<br />

9<br />

9

I. Overview of General Types of Guaranties<br />

• The <strong>Guaranty</strong> Agreement<br />

• A guaranty is an agreement made by a third party, whether a<br />

person, trust or a business entity, to pay and/or perform the<br />

obligations of a debtor for the satisfaction of a debt owed to a<br />

creditor upon the occurrence of an event, typically a default by<br />

the debtor under the original loan agreement.<br />

• A guaranty, like any contract, requires mutual assent, adequate<br />

consideration, definiteness and a meeting of the minds. Under<br />

most states’ Statute of Frauds, a guaranty must be in writing,<br />

signed by the guarantor(s) and delivered d to the creditor.<br />

1010

I. Overview of General Types of Guaranties<br />

• In the context of a loan transaction, a guaranty serves as a form<br />

of collateral to support the debt obligation between the debtor and<br />

the creditor.<br />

• But, the guaranty and the loan agreement evidence separate<br />

obligations, and their independence is not affected by the fact that<br />

both agreements are written on the same paper or instrument or<br />

are contemporaneously executed.<br />

• The guaranty cannot exist without a primary debt obligation. Thus,<br />

if the primary debt obligation has been fully satisfied, is void or is<br />

illegal, a guaranty of the debt obligation is also unenforceable.<br />

1111

I. Overview of General Types of Guaranties<br />

• Consideration<br />

• A guaranty is a contract and, as such, it must be supported by<br />

consideration. A guaranty without consideration is merely an<br />

unenforceable gratuitous promise. While some guaranties are founded<br />

on separate consideration than the original credit transaction, the<br />

guarantor need not receive a direct benefit for consideration to exist.<br />

The consideration usually consists of a benefit to the debtor or a<br />

detriment to the creditor.<br />

1212

I. Overview of General Types of Guaranties<br />

• Courts have deemed consideration to be sufficient in the following<br />

cases:<br />

• <strong>Guaranty</strong> is made contemporaneously with loan agreement. See, In re Kraft,<br />

LLC, 429 B.R. 637, 659 (Bankr.N.D.Ind. 2010); Jackson v. Luellen Farms, Inc.,<br />

877 N.E.2d 848 (Ind. Ct. App. 2007).<br />

• <strong>Guaranty</strong> is made as part of the loan transaction, even if the two documents are<br />

not executed on the same date. See, Michelin Management Co., Inc. v.<br />

Mayaud, 307 A.D.2d 280, 762 N.Y.S.2d 108 (2d Dep't 2003).<br />

• Amendment to the loan agreement, note or other loan document that is<br />

acknowledged and approved by the guarantor. See, First Commerce Bank v.<br />

Palmer, 226 S.W.3d 396 (Tex. 2007); Caves v. Columbus Bank & Trust Co.,<br />

589 S.E.2d 670, 676 (Ga.App. 2003); Brown v. Lawrenceville Properties, LLC,<br />

710 S.E.2d 682, 685 (Ga.App. 2011).<br />

1313

I. Overview of General Types of Guaranties<br />

• Resolution and/or settlement of claims against debtor; the creditor's<br />

compromise of a claim against the debtor. See, Cincinnati Ins. Co. v.<br />

American Hardware Mfrs. Ass'n, 898 N.E.2d 216, 230 (Ill.App. 1st Dist.<br />

2008); Tag to Print 3Tower Investors, LLC v. 111 East Chestnut<br />

Consultants, Inc., 864 N.E.2d 927, 937 (Ill.App. 1st Dist. 2007).<br />

• Continuance and/or expansion of debtor’s business with creditor or other<br />

vendors or service providers; the creditor's agreement to continue doing<br />

business with the primary debtor. See, Material Partnerships, Inc. v.<br />

Ventura, 102 S.W.3d 252 (Tex. App. 14th Dist. 2003).<br />

• Creditor’s agreement to conduct business with guarantor or to provide<br />

guarantor with a benefit outside of the guaranty agreement; a bank's<br />

retention of the guarantor's friend in his position as president of the bank.<br />

See, Performance Elec., Inc. v. CIB Bank, 864 N.E.2d 779, 784 (Ill.App. 1<br />

Dist. 2007).<br />

1414

I. Overview of General Types of Guaranties<br />

• Joint and Several Liability<br />

• Typically, with multiple guarantors of the same debt obligation,<br />

the creditor can proceed against less than all of the coguarantors<br />

for recovery of the entire guaranteed obligations.<br />

See Wachovia Bank, Nat. Ass'n v. Horizon Wholesale Foods,<br />

LLC, 2009 WL 3526662 (S.D.Ala. 2009); Finagin v. Arkansa<br />

Dev. Fin. Auth., 139 S.W.3d 797, 803 (Ark. 2003); Century<br />

Business Credit Corp. v. Gargiulo Foods, L.L.C., 2003 WL<br />

21998959 (S.D.N.Y.,2003).<br />

1515

I. Overview of General Types of Guaranties<br />

• Death of Guarantor<br />

• Unless expressly provided in the guaranty, a guarantor's death does<br />

not terminate a guaranty. See, In re Steagall's Estate, 444 N.E.2d 838<br />

(4th Dist. 1983); In re Klink's Estate, 35 N.E.2d 684 (1st Dist. 1941).<br />

The death of the guarantor of a continuing guaranty may limit the<br />

guarantor’s liability as it relates to future transactions but does not<br />

affect the credit transaction that was originally guaranteed. However,<br />

the estate of the deceased continues to guaranty a credit transaction<br />

by providing for renewals, as the consideration for the additional<br />

obligation that was extended before the guarantor's death.<br />

1616

I. Overview of General Types of Guaranties<br />

• Types of Guaranties<br />

• Absolute<br />

• An absolute guaranty provides that the guarantor promises to pay<br />

or perform the obligations of the debtor upon the occurrence of a<br />

default event (typically debtor’s default). If a guaranty does not<br />

contain words of limitation or conditions, it is typically construed as<br />

an absolute guaranty.<br />

• Conditional<br />

• A conditional guaranty requires the happening of some contingent<br />

event (other than the default of the debtor) or the performance of<br />

some act on the part of the creditor before the guarantor will be<br />

liable.<br />

1717

I. Overview of General Types of Guaranties<br />

• Payment<br />

• A payment guaranty obligates the guarantor to pay the debt at maturity<br />

(which may arise due to an event of default). Upon the occurrence of a<br />

debtor's default, the guarantor’s obligation becomes fixed and the<br />

creditor does not need to make a demand on the debtor.<br />

• Collection<br />

• A guaranty of collection is a guarantor’s promise that if the creditor<br />

cannot collect the claim with due diligence, usually after suit (and<br />

exhaustion of remedies) against the debtor, the guarantor will pay the<br />

creditor.<br />

• Performance<br />

• A performance guaranty obligates the guarantor to perform some<br />

obligation on behalf of the debtor for the benefit of the creditor.<br />

1818

I. Overview of General Types of Guaranties<br />

• Continuing<br />

• A guaranty is continuing when it is not limited to a single transaction<br />

but contemplates a future course of dealing which may encompass a<br />

series of transactions, may be for an indefinite period and/or may be<br />

intended to secure payment or performance of an overall debt of the<br />

debtor. As such, a continuing guaranty may include subsequent<br />

indebtedness without new consideration.<br />

• Restricted<br />

• A guaranty is a restricted guaranty when it is limited to a single or<br />

limited number of transactions, to a certain part of the debt obligation<br />

and/or to a certain period of time.<br />

1919

I. Overview of General Types of Guaranties<br />

• Downstream<br />

• A downstream guaranty is a guaranty by a parent corporation for the<br />

obligations of its subsidiary. In this scenario, a lender will look to the<br />

parent corporation to back up the debt of a subsidiary corporation due<br />

to the parent corporation’s superior assets and financial condition.<br />

• Upstream<br />

• An upstream guaranty is a guaranty by a subsidiary corporation for the<br />

obligations of its parent corporation. Typically, a creditor will require an<br />

upstream guaranty when debtor’s, i.e. the parent corporation’s, only<br />

assets are the stock of a subsidiary, and the subsidiary owns assets<br />

used as collateral to secure the credit obligations.<br />

• Cross-stream<br />

• A cross-stream guaranty is a guaranty among affiliated corporations,<br />

whose stock are both owned by the same parent.<br />

2020

I. Overview of General Types of Guaranties<br />

• “Bad Boy” <strong>Guaranty</strong><br />

• Many non-recourse guaranties will include provisions that carve-out<br />

instances where the guarantor may be personally liable upon the<br />

occurrence of certain enumerated bad acts. This type of guaranty is<br />

referred to as a “bad boy” guaranty. The types of bad acts commonly<br />

include matters such as fraud, misappropriation, waste, and other acts<br />

that show some bad act on the part of the guarantor. Since the<br />

guarantor’s personal liability arises only upon the occurrence of a bad<br />

act, the guaranty’s liability is sometimes referred to as a springing<br />

liability.<br />

2121

II. Enforcement and Defense of Guaranties<br />

• Capacity<br />

• Delaware Corporations – General Power<br />

• “(a) In addition to the powers enumerated in § 122 of this title, every<br />

corporation, its officers, directors and stockholders shall possess<br />

and may exercise all the powers and privileges granted by this<br />

chapter or by any other law or by its certificate of incorporation,<br />

together with any powers incidental thereto, so far as such powers<br />

and privileges are necessary or convenient to the conduct,<br />

promotion or attainment of the business or purposes set forth in its<br />

certificate of incorporation.<br />

• (b) Every corporation shall be governed by the provisions i and be<br />

subject to the restrictions and liabilities contained in this chapter.”<br />

8 Del.C. § 121<br />

2222

II. Enforcement and Defense of Guaranties<br />

• Capacity<br />

• Delaware Limited Liability Companies – General and Specific <strong>Guaranty</strong> Power<br />

• “(b) A limited liability company shall possess and may exercise all the<br />

powers and privileges granted by this chapter or by any other law or by its<br />

limited it liability company agreement, together th with any powers incidental id thereto, including such powers and privileges as are necessary or<br />

convenient to the conduct, promotion or attainment of the business,<br />

purposes or activities of the limited liability company.<br />

• (c) Notwithstanding any provision of this chapter to the contrary, without<br />

limiting the general powers enumerated in subsection (b) of this section, a<br />

limited liability company shall, subject to such standards and restrictions, if<br />

any, as are set forth in its limited liability company agreement, have the<br />

power and authority to make contracts of guaranty and suretyship and enter<br />

into interest rate, basis, currency, hedge or other swap agreements or cap,<br />

floor, put, call, option, exchange or collar agreements, derivative<br />

agreements, or other agreements similar to any of the foregoing.”<br />

6 Del.C. § 18-106<br />

2323

II. Enforcement and Defense of Guaranties<br />

• Capacity<br />

• Delaware Corporations – Specific <strong>Guaranty</strong> Power<br />

• “Every corporation created under this chapter shall have power to:<br />

a. (13) Make contracts, including contracts of guaranty and suretyship, incur liabilities,<br />

borrow money at such rates of interest t as the corporation may determine, issue its<br />

notes, bonds and other obligations, and secure any of its obligations by mortgage,<br />

pledge or other encumbrance of all or any of its property, franchises and income,<br />

and make contracts of guaranty and suretyship which are necessary or convenient<br />

to the conduct, promotion or attainment of the business of (a) a corporation all of<br />

the outstanding t stock of which h is owned, directly or indirectly, by the contracting<br />

ti<br />

corporation, or (b) a corporation which owns, directly or indirectly, all of the<br />

outstanding stock of the contracting corporation, or (c) a corporation all of the<br />

outstanding stock of which is owned, directly or indirectly, by a corporation which<br />

owns, directly or indirectly, all of the outstanding stock of the contracting<br />

corporation, which contracts of guaranty and suretyship shall be deemed to be<br />

necessary or convenient to the conduct, promotion or attainment of the business of<br />

the contracting corporation, and make other contracts of guaranty and suretyship<br />

which are necessary or convenient to the conduct, promotion or attainment of the<br />

business of the contracting corporation;”<br />

8 Del.C. § 122<br />

2424

II. Enforcement and Defense of Guaranties<br />

• Statute of Frauds<br />

• Mistake<br />

• Misrepresentation<br />

• Parol Evidence<br />

• Interpretation<br />

2525

II. Enforcement and Defense of Guaranties<br />

• Impossibility, Impracticability, and Frustration of<br />

Purpose<br />

• Accord and Satisfaction<br />

• Novation<br />

• Statute of Limitations<br />

• Lack of Notice of Adverse Effects<br />

2626

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral – UCC 3-605<br />

• “(a) If a person entitled to enforce an instrument releases the obligation of a principal<br />

obligor in whole or in part, and another party to the instrument is a secondary obligor with<br />

respect to the obligation of that principal obligor, the following rules apply:<br />

• (1) Any obligations of the principal obligor to the secondary obligor with respect to any<br />

previous payment by the secondary obligor are not affected. Unless the terms of the<br />

release preserve the secondary obligor's recourse, the principal obligor is discharged,<br />

to the extent of the release, from any other duties to the secondary obligor under this<br />

article.<br />

• (2) Unless the terms of the release provide that the person entitled to enforce the<br />

instrument retains the right to enforce the instrument against the secondary obligor, the<br />

secondary obligor is discharged to the same extent as the principal obligor from any<br />

unperformed portion of its obligation on the instrument. If the instrument is a check and<br />

the obligation of the secondary obligor is based on an indorsement of the check, the<br />

secondary obligor is discharged without regard to the language or circumstances of the<br />

discharge or other release.<br />

• (3) If the secondary obligor is not discharged under paragraph (2), the secondary<br />

obligor is discharged to the extent of the value of the consideration for the release, and<br />

to the extent that the release would otherwise cause the secondary obligor a loss.<br />

2727

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral – UCC 3-605<br />

• (b) If a person entitled to enforce an instrument grants a principal obligor an extension of<br />

the time at which one or more payments are due on the instrument and another party to the<br />

instrument is a secondary obligor with respect to the obligation of that principal obligor, the<br />

following rules apply: ppy<br />

• (1) Any obligations of the principal obligor to the secondary obligor with respect to any<br />

previous payment by the secondary obligor are not affected. Unless the terms of the<br />

extension preserve the secondary obligor's recourse, the extension correspondingly<br />

extends the time for performance of any other duties owed to the secondary obligor by<br />

the principal i obligor under this article.<br />

• (2) The secondary obligor is discharged to the extent that the extension would<br />

otherwise cause the secondary obligor a loss.<br />

• (3) To the extent that the secondary obligor is not discharged under paragraph (2), the<br />

secondary obligor may perform its obligations to a person entitled to enforce the<br />

instrument as if the time for payment had not been extended or, unless the terms of the<br />

extension provide that the person entitled to enforce the instrument retains the right to<br />

enforce the instrument against the secondary obligor as if the time for payment had not<br />

been extended, treat the time for performance of its obligations as having been<br />

extended correspondingly.<br />

2828

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral – UCC 3-<br />

605<br />

• (c) If a person entitled to enforce an instrument agrees, with or without<br />

consideration, to a modification of the obligation of a principal obligor other than<br />

a complete or partial release or an extension of the due date and another party<br />

to the instrument is a secondary obligor with respect to the obligation of that<br />

principal obligor, the following rules apply:<br />

• (1) Any obligations of the principal obligor to the secondary obligor with<br />

respect to any previous payment by the secondary obligor are not affected.<br />

The modification correspondingly modifies any other duties owed to the<br />

secondary obligor by the principal obligor under this article.<br />

• (2) The secondary obligor is discharged from any unperformed portion of its<br />

obligation to the extent that the modification would otherwise cause the<br />

secondary obligor a loss.<br />

• (3) To the extent that the secondary obligor is not discharged under<br />

paragraph (2), the secondary obligor may satisfy its obligation on the<br />

instrument as if the modification had not occurred, or treat its obligation on<br />

the instrument t as having been modified d correspondingly.<br />

2929

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral – UCC 3-<br />

605<br />

• (d) If the obligation of a principal obligor is secured by an interest in collateral,<br />

another party to the instrument is a secondary obligor with respect to that<br />

obligation, and a person entitled to enforce the instrument impairs the value of<br />

the interest in collateral, the obligation of the secondary obligor is discharged to<br />

the extent of the impairment. The value of an interest in collateral is impaired to<br />

the extent the value of the interest is reduced to an amount less than the<br />

amount of the recourse of the secondary obligor, or the reduction in value of the<br />

interest causes an increase in the amount by which the amount of the recourse<br />

exceeds the value of the interest. For purposes of this subsection, impairing the<br />

value of an interest in collateral includes failure to obtain or maintain perfection<br />

or recordation of the interest in collateral, release of collateral without<br />

substitution of collateral of equal value or equivalent reduction of the underlying<br />

obligation, failure to perform a duty to preserve the value of collateral owed,<br />

under Article 9 or other law, to a debtor or other person secondarily liable, and<br />

failure to comply with applicable law in disposing of or otherwise enforcing the<br />

interest in collateral.<br />

3030

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral – UCC 3-<br />

605<br />

• (e) A secondary obligor is not discharged under subsections (a)(3), (b), (c), or<br />

(d) unless the person entitled to enforce the instrument knows that the person is<br />

a secondary obligor or has notice under Section 3-419(c) that the instrument<br />

was signed for accommodation.<br />

• (f) A secondary obligor is not discharged under this section if the secondary<br />

obligor consents to the event or conduct that is the basis of the discharge, or<br />

the instrument or a separate agreement of the party provides for waiver of<br />

discharge under this section specifically or by general language indicating that<br />

parties waive defenses based on suretyship or impairment of collateral. Unless<br />

the circumstances indicate otherwise, consent by the principal obligor to an act<br />

that would lead to a discharge under this section constitutes consent to that act<br />

by the secondary obligor if the secondary obligor controls the principal obligor or<br />

deals with the person entitled to enforce the instrument on behalf of the<br />

principal obligor.<br />

3131

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral<br />

– UCC 3-605<br />

• (g) A release or extension preserves a secondary obligor's recourse if<br />

the terms of the release or extension provide that: t<br />

• (1) the person entitled to enforce the instrument retains the right to<br />

enforce the instrument against the secondary obligor; and<br />

• (2) the recourse of the secondary obligor continues as if the release<br />

or extension had not been granted.<br />

• (h) Except as otherwise provided in subsection (i), a secondary obligor<br />

asserting discharge under this section has the burden of persuasion<br />

both with respect to the occurrence of the acts alleged to harm the<br />

secondary obligor and loss or prejudice caused by those acts.<br />

3232

II. Enforcement and Defense of Guaranties<br />

• Material Change in Debt and Impairment of Collateral<br />

– UCC 3-605<br />

• (i) If the secondary obligor demonstrates prejudice caused by an impairment of<br />

its recourse, and the circumstances of the case indicate that the amount of loss<br />

is not reasonably susceptible of calculation or requires proof of facts that are<br />

not ascertainable, it is presumed that the act impairing recourse caused a loss<br />

or impairment equal to the liability of the secondary obligor on the instrument. In<br />

that event, the burden of persuasion as to any lesser amount of the loss is on<br />

the person entitled to enforce the instrument.”<br />

Unif.<strong>Commercial</strong> Code § 3-605<br />

3333

II. Enforcement and Defense of Guaranties<br />

• Change in Creditor<br />

• Lack of Notice of Foreclosure Sale<br />

• Failure to Conduct <strong>Commercial</strong>ly Reasonable Foreclosure Sale<br />

• Release of Co-guarantors<br />

• Negligent <strong>Loan</strong> Administration<br />

• Failure to Pursue the Underlying Debtor<br />

• Defense on the Underlying Debt<br />

• Bankruptcy Issues (ex. automatic stay and fraudulent<br />

conveyances)<br />

3434

III.<br />

Bankruptcy Issues<br />

• Springing (“Bad Boy”) Guaranties Generally Enforced<br />

By Bankruptcy Court<br />

• (See In re Extended Stay Inc., 418 B.R. 49 (Bankr. S.D.N.Y. 2009)<br />

aff’d in part by In re Extended d Stay Inc., 435 B.R. 139 (S.D.N.Y. 2010))<br />

• Bankruptcy Courts Will Typically Abstain from Hearing Springing<br />

<strong>Guaranty</strong> Actions Removed From State Court<br />

• Guarantors Must Have Waived Any Indemnity or Contribution<br />

Claims Against the Debtor<br />

• Potential for State Court <strong>Guaranty</strong> Action to be Stayed Under §105<br />

of Bankruptcy if Guarantor is “Integral” to Debtor Case and Action<br />

Would Significantly Limit Guarantor’s Participation In Bankruptcy<br />

3535

III.<br />

Bankruptcy Issues<br />

• Potential ti Fraudulent Conveyance Exposure<br />

• Most Risk for Upstream and Cross-Stream Guaranties<br />

• Intercorporate Guaranties Can Be Unwound In Bankruptcy<br />

Under:<br />

• Bankruptcy Code §548 (Guaranties Made Up to Two Years<br />

Before Filing), or<br />

• Under Bankruptcy Code §544 and the Uniform Fraudulent<br />

Transfer Act (UFTA) or the Uniform Fraudulent<br />

Conveyances Act (UFCA) (Typically, y Guaranties Made From<br />

Four to Six Years Before Filing)<br />

3636

III.<br />

Bankruptcy Issues<br />

• Inquiry is Typically Constructive Fraud<br />

• Under Bankruptcy Code §544 and the UFTA, the Test is<br />

Whether the Guarantor (Debtor) received “Reasonably<br />

Equivalent Value”<br />

• Under the UFTA, the Test is Whether the Guarantor (Debtor)<br />

Received “Fair Consideration”<br />

• Drafting Considerations<br />

• Net Worth <strong>Guaranty</strong><br />

• Savings Clause<br />

3737

III.<br />

Bankruptcy Issues<br />

• Risk of Separate Classification of Deficiency Claims in Bankruptcy<br />

Plan<br />

(See In re Loop, 442 B.R. 714 (Bankr. D. Ariz. 2010)<br />

• Bankruptcy Code §544 Requires that Substantially Similar Claims May Not Be<br />

Put Into Separate Classes to Gerrymander an Affirmative Vote to Confirm a<br />

Plan Under Bankruptcy Code §1129(b)<br />

• Some Bankruptcy Courts are Now Holding that Guaranteed Deficiency Claims<br />

are Different Than Other Unsecured Claims and Are Permitted to Be Separately<br />

Classified<br />

• Separate Classification May Result in Unsecured Creditors Voting in Favor of a<br />

Plan and the Debtor Being Able to Confirm a Cramdown Plan of Reorganization<br />

3838