Reserve Bank of Australia Annual Report 2011

Reserve Bank of Australia Annual Report 2011

Reserve Bank of Australia Annual Report 2011

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Accounting Valuation<br />

For financial statement purposes, the financial positions <strong>of</strong> the superannuation schemes are valued in<br />

accordance with AASB 119. Under AASB 119, accrued benefits are determined by discounting future benefits<br />

payable to current fund members at the yield on government bonds <strong>of</strong> similar maturity on the reporting date.<br />

The approach under AASB 119, in contrast with the results <strong>of</strong> the actuaries’ triennial valuations noted above,<br />

does not take into account that the assets held by the superannuation schemes to fund future benefits have<br />

generally earned a higher rate <strong>of</strong> return on average than government bonds.<br />

The principal actuarial assumptions for the AASB 119 valuation used in the case <strong>of</strong> the OSF were a discount<br />

rate <strong>of</strong> 5.38 per cent (5.27 per cent in 2009/10), future salary increases <strong>of</strong> 3.5 per cent (3.5 per cent in 2009/10),<br />

future pension increases <strong>of</strong> 3.5 per cent (3.5 per cent in 2009/10) and an assumed return on plan assets <strong>of</strong><br />

8.5 per cent (8.5 per cent in 2009/10). The actual return on plan assets <strong>of</strong> the OSF for 2010/11 was 8.1 per cent<br />

(10.6 per cent in 2009/10). The assumptions used for the UK Pension Scheme were a discount rate <strong>of</strong> 5.4 per<br />

cent (5.3 per cent in 2009/10), future salary increases <strong>of</strong> 5.65 per cent (5.25 per cent in 2009/10), future pension<br />

increases <strong>of</strong> 3.65 per cent (3.25 per cent in 2009/10) and an assumed return on plan assets <strong>of</strong> 4.1 per cent<br />

(4.4 per cent in 2009/10). The actual return on plan assets <strong>of</strong> the UK Pension Scheme for 2010/11 was 10.0 per<br />

cent (6.1 per cent in 2009/10). The expected overall rates <strong>of</strong> return are based on the actuaries’ models <strong>of</strong> returns<br />

for major asset classes and reflect the historic rates <strong>of</strong> return and volatility for each class and correlations across<br />

asset classes.<br />

Details <strong>of</strong> the funds are as shown on the following pages. In the case <strong>of</strong> the OSF, these details relate only to the<br />

defined benefit component <strong>of</strong> the fund; defined contribution accumulation balances, on which the <strong>Bank</strong> has<br />

no actuarial risk, are excluded. This has no effect on the measurement <strong>of</strong> the surpluses in the OSF. At 30 June<br />

<strong>2011</strong> accumulation balances in the OSF totalled $165.4 million ($150.5 million as at 30 June 2010).<br />

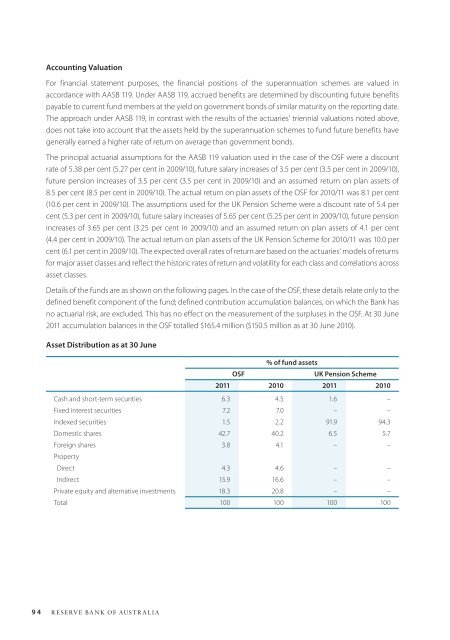

Asset Distribution as at 30 June<br />

% <strong>of</strong> fund assets<br />

OSF<br />

UK Pension Scheme<br />

<strong>2011</strong> 2010 <strong>2011</strong> 2010<br />

Cash and short-term securities 6.3 4.5 1.6 –<br />

Fixed interest securities 7.2 7.0 – –<br />

Indexed securities 1.5 2.2 91.9 94.3<br />

Domestic shares 42.7 40.2 6.5 5.7<br />

Foreign shares 3.8 4.1 – –<br />

Property<br />

Direct 4.3 4.6 – –<br />

Indirect 15.9 16.6 – –<br />

Private equity and alternative investments 18.3 20.8 – –<br />

Total 100 100 100 100<br />

94 <strong>Reserve</strong> bank <strong>of</strong> <strong>Australia</strong>

![KNOW YOUR NEW GIBRALTAR BANKNOTES - [Home] bThe/b](https://img.yumpu.com/50890985/1/184x260/know-your-new-gibraltar-banknotes-home-bthe-b.jpg?quality=85)

![PAPUA NEW GUINEA - [Home] - Polymer Bank Notes of the World](https://img.yumpu.com/49758743/1/190x143/papua-new-guinea-home-polymer-bank-notes-of-the-world.jpg?quality=85)