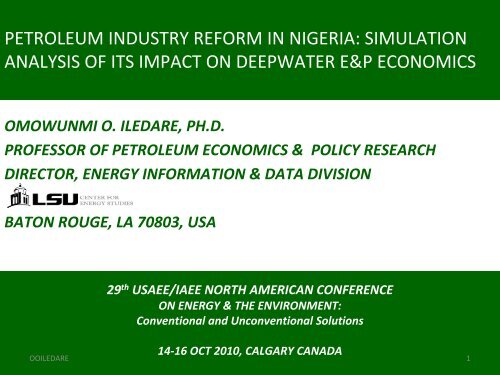

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ...

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ...

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>PETROLEUM</strong> <strong><strong>IN</strong>DUSTRY</strong> <strong>REFORM</strong> <strong>IN</strong> <strong>NIGERIA</strong>: <strong>SIMULATION</strong><br />

ANALYSIS OF ITS IMPACT ON DEEPWATER E&P ECONOMICS<br />

OMOWUNMI O. ILEDARE, PH.D.<br />

PROFESSOR OF <strong>PETROLEUM</strong> ECONOMICS & POLICY RESEARCH<br />

DIRECTOR, ENERGY <strong>IN</strong>FORMATION & DATA DIVISION<br />

BATON ROUGE, LA 70803, USA<br />

29 th USAEE/IAEE NORTH AMERICAN CONFERENCE<br />

ON ENERGY & THE ENVIRONMENT:<br />

Conventional and Unconventional Solutions<br />

14‐16 OCT 2010, CALGARY CANADA<br />

OOILEDARE 1

Presentation Outline<br />

• Nigeria’s petroleum economy overview<br />

• Nigeria petroleum industry reform objectives<br />

• Fiscal & non fiscal reform legislative instruments<br />

• Diagnosis of fiscal legislative instruments<br />

• Impact deepwater project economics<br />

• Concluding remarks and questions<br />

OOILEDARE 2<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Petroleum Industry in Nigeria<br />

• Nigeria ranks among the top 10 nations in proved oil and<br />

natural gas reserves worldwide.<br />

• The largest oil producer in Africa; 7 th in OPEC; but fifth largest<br />

economy in OPEC.<br />

• As of January 1, 2010, the estimated crude oil and natural gas<br />

reserves are 37.2 billion barrels and 185.4 trillion cubic feet<br />

(TCF).<br />

– The target to expand its proven oil reserves to 40.0 billion barrels and<br />

increase its production capacity to 4 million barrels per day by 2010 is<br />

impracticable with less than three months to go.<br />

OOILEDARE 3<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Reform Legislation in Nigeria<br />

‣Describes the legislative, tax, contractual and fiscal<br />

elements under which petroleum operations are conducted<br />

in a petroleum province, region on nation.<br />

‣Defines the relationship between federal government of<br />

Nigeria and the oil and gas companies (IOC, NOC, & DOC).<br />

‣Explains how costs are to be recovered and profits are to<br />

be shared between firms, the host governments, and the<br />

host communities<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

4

Broad Objectives of the Reform<br />

• Provides petroleum industry operational strategies and guidelines.<br />

• Proffers solutions to petroleum fiscal problems and community<br />

issues affecting oil and gas operations in the upstream, midstream,<br />

and downstream sectors of the Nigerian petroleum economy.<br />

• Aligns the oil and gas industry in Nigeria with international best<br />

practices in order to facilitate good governance and transparency in<br />

the industry.<br />

• Assigns separate functional responsibilities to institutional<br />

structures in order to manage the commercial and operational<br />

aspects of the oil and gas sector as well as the policy‐making and<br />

regulatory aspects effectively.<br />

OOILEDARE 5<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Broad Objectives of the Ongoing Reform<br />

• Revamps the petroleum revenue system in terms of revenue<br />

collection, revenue enhancement, and wealth creation and<br />

restructures the taxation system for the oil and gas industry in<br />

Nigeria.<br />

• Repositions the national oil company to a level comparable to<br />

the status of other prominent national oil corporations (NOCs)<br />

• Defines a new joint venture structure to address the funding<br />

problems of industry projects with a new indsutry structure<br />

termed incorporated joint ventures (IJV).<br />

OOILEDARE 6<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Fiscal System Instruments<br />

Nigeria Sliding Royalty Scales<br />

Royalty B4 Reform Legislation<br />

Water Depth 0‐100 100‐200 201‐500 501‐800 801‐1000m >1000m<br />

Onshore: 20%<br />

Swamp/<br />

Shallow water<br />

18.5%<br />

Shelf PSC 16.67%<br />

Deep Offshore PSC 12% 8% 4% 0<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

7<br />

7

Fiscal Instruments for Deepwater PSC:<br />

Nigeria Taxation Examples<br />

Pre‐Reform for 1000m Water Depth<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

8<br />

8

Proposed Fiscal Instruments for<br />

Nigeria Taxation Examples<br />

All Deepwater PSC in Nigeria<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

9<br />

9

Proposed Fiscal Instruments<br />

Sliding Royalty Scales by Volume in the PIB<br />

Sliding Scale Royalty by Volume<br />

OIL<br />

Natural Gas<br />

Area/Royalty<br />

5% 12.5% 25% 5% 12.5%<br />

Onshore 0‐2M b/d 2‐5Mb/d >5Mb/d 0‐100MMcf/d >100 MMcf/d<br />

Shallow Water 0‐5M b/d 5‐20Mb/d >20Mb/d 0‐200 MMcf/d >200 MMcf/d<br />

Deep Water 0‐50M b/d 50‐100Mb/d >100Mb/d 0‐500MMcf/d >500 MMcf/d<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

10 12

Proposed Example Fiscal of Instruments<br />

Nigeria<br />

Sliding Royalty Scales by Value in the PIB<br />

Sliding Royalty Scales by Value<br />

Sliding Scale Royalty by Value<br />

Oil Price<br />

Per Bbl<br />

Royalty<br />

%<br />

Gas Price<br />

per MMBtu<br />

Royalty<br />

%<br />

$0 ‐ $70 0 $0 ‐ $2 0<br />

$70 ‐ $100 0.4 per $ $2 ‐ $7 0.20/10cents<br />

$100 ‐ $140 12 + 0.2 /$ $7 ‐ $13 10 + 0.15/10cents<br />

$140 ‐ $190 20 + 0.1/$ $13 ‐ $19 19 + 0.10/10cents<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

11<br />

11

Modeling Reform Legislation Impact<br />

on Deepwater Economics—DCF Approach<br />

Where:<br />

‣NCF t = After‐tax net cash flow in year t,<br />

‣GRR t = Gross revenue in year t,<br />

‣ROY t = Total royalty paid in year t,<br />

‣CPX t = Total capital expenditures in year t,<br />

‣OPX t = Total operating expenditures in year t,<br />

‣BNS t = Bonus paid in year t,<br />

‣PO/G t = Government profit oil in year t,<br />

‣TAX t = Total taxes paid in year t,<br />

‣OTH t = Other costs or taxes paid in year t.<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

12

Modeling Deepwater Economics<br />

—DCF Modeling Output Indicators<br />

HGT:<br />

PV =<br />

=<br />

k<br />

∑<br />

t = 1<br />

(1<br />

NCF<br />

+ D<br />

)<br />

t<br />

t<br />

− 1<br />

IRR (f, F) = { D | PV ( f ,F) = 0}<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

13

Production Sharing Contract Model<br />

Stochastic Variable Assumptions<br />

Instruments<br />

Real Oil Price,<br />

2010$/Bbl<br />

OPEX, 2010$/Bbl<br />

Actual OPEX<br />

Abroad, %<br />

Actual CAPEX<br />

Abroad, %<br />

Capacity,<br />

Bbl/Day<br />

Inflation,%<br />

Distribution<br />

Assumptions<br />

Triangular<br />

(Min, Mode, Max)<br />

Triangular<br />

(Min, Mode, Max)<br />

Triangular<br />

(Min, Mode, Max)<br />

Triangular<br />

(Min, Mode, Max)<br />

Lognormal<br />

(Mode, Mean, Std)<br />

Triangular<br />

(Min, Mode, Max)<br />

Distribution<br />

Parameters<br />

60.00 75.00 90.00<br />

5.00 6.00 7.50<br />

0 50 100<br />

0 80 100<br />

40,000 50,000 500<br />

1.0 2.0 3.0<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

14

Production Sharing Contract Model<br />

Decision Variable Base Assumptions<br />

Decision Instruments<br />

Cost Recovery Limit,<br />

%<br />

Distribution<br />

Parameters<br />

Profit Oil Split/G,% 20<br />

80<br />

Eligible Foreign<br />

CAPEX, %<br />

Eligible Foreign<br />

OPEX, %<br />

Hydrocarbon Tax<br />

CITA<br />

Allowance Cap, $/Bbl<br />

80<br />

80<br />

30<br />

30<br />

Min (7, 0.3*P)<br />

P=real oil price<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

15

Standalone Deepwater Project :<br />

100 MMB Deterministic Model Results<br />

Metric Systems Measures (Nominal$)<br />

Host Govt.<br />

BIT $MM<br />

Contractor Host Govt. AIT<br />

BIT $MM $ MM<br />

Contractor<br />

AIT $MM<br />

Net Present Value @12.5% $ 751.46 $ 777.36 $ 1,065.83 $ 293.40<br />

Internal Rate of Return 40.0% 27.5%<br />

Growth Rate of Return 16.3% 14.3%<br />

Undiscounted Take Statistics 45.1% 54.9% 72.4% 27.6%<br />

Discounted Take Statistics 49.2% 50.8% 78.4% 21.6%<br />

Metric Systems Measures (Real 2010$)<br />

Host Govt.<br />

BIT $MM<br />

Contractor Host Govt. AIT<br />

BIT $MM $ MM<br />

Contractor<br />

AIT $MM<br />

Net Present Value @12.5% $ 573.94 $ 597.06 $ 815.93 $ 220.95<br />

Internal Rate of Return 37.6% 25.7%<br />

Growth Rate of Return 16.1% 14.1%<br />

Undiscounted Take Statistics 44.4% 55.6% 71.7% 28.3%<br />

Discounted Take Statistics 49.0% 51.0% 78.7% 21.3%<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

16

Incremental Deepwater Project:<br />

100 MMB Deterministic Model Results<br />

Metric Systems Measures (Nominal$)<br />

Host Govt.<br />

BIT $MM<br />

Contractor Host Govt. AIT<br />

BIT $MM $ MM<br />

Contractor<br />

AIT $MM<br />

Net Present Value @12.5% $ 722.95 $ 805.87 $ 1,014.13 $ 345.09<br />

Internal Rate of Return 44.9% 38.7%<br />

Growth Rate of Return 16.4% 14.5%<br />

Undiscounted Take Statistics 44.8% 55.2% 72.2% 27.8%<br />

Discounted Take Statistics 47.3% 52.7% 74.6% 25.4%<br />

Metric Systems Measures (Real 2010$)<br />

Host Govt.<br />

BIT $MM<br />

Contractor Host Govt. AIT<br />

BIT $MM $ MM<br />

Contractor<br />

AIT $MM<br />

Net Present Value @12.5% $ 547.20 $ 623.80 $ 768.10 $ 268.79<br />

Internal Rate of Return 42.5% 36.7%<br />

Growth Rate of Return 16.2% 14.4%<br />

Undiscounted Take Statistics 44.0% 56.0% 71.4% 28.6%<br />

Discounted Take Statistics 46.7% 53.3% 74.1% 25.9%<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

17

Sensitivity of Nominal IRR vs. HGT<br />

to Stochastic Variables‐‐Standalone<br />

OOILEDARE 18<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Sensitivity of Nominal IRR vs. HGT<br />

to Decision Variables‐‐Standalone<br />

OOILEDARE 19<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Sensitivity of Nominal IRR vs. HGT<br />

to Stochastic Variables‐‐Standalone<br />

OOILEDARE 20<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Sensitivity of Nominal IRR vs. HGT<br />

to Decision Variables‐‐Standalone<br />

OOILEDARE 21<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Deepwater 100 MMB PSC Project:<br />

Simulation Model Output Standalone<br />

Economics System Output<br />

Measures<br />

Mean Minimum Most Likely Maximum<br />

NPV @12.5%, $Million 290.80 135.05 299.29 419.83<br />

IRR, Percent 27.3 19.8 27.6 32.0<br />

HGT, Percent 78.6 75.9 78.6 83.4<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

22

Internal Rate of Return:<br />

Fifty Percent Certainty—Standalone<br />

OOILEDARE 23<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Government Take Statistic<br />

Fifty Percent Certainty Range—Standalone<br />

OOILEDARE 24<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada

Conclusions<br />

• Ongoing petroleum industry reform legislation in Nigeria has fiscal<br />

instruments and terms that enhance government access to gross revenue<br />

and still makes E&P operations profitable in Nigeria.<br />

• There is a fifty percent likelihood that the legislation will give 78‐79 percent<br />

of total profit from a 100 MMB deepwater oil project to the host<br />

government.<br />

• Justification for this high government take is being tied to high hydrocarbon<br />

prospectivity in Nigeria, but undue fiscal burdens may also disenfranchise<br />

investors as evident in the sensitivity of IRR to selected decision variables.<br />

• If contractors spend low proportion of its expenditures abroad, project<br />

profitability, ceteris paribus, tend to increase<br />

• Allowing all CAPEX to be expensed in NHT and CITA calculations increases<br />

project profitability as expected.<br />

• Deep water profitability is higher for existing operators in deepwater than<br />

new comers because CITA and NHT are allowed to be consolidated rather<br />

than being ringfenced.<br />

OOILEDARE<br />

USAEE 2010, Calgary, Canada<br />

25

<strong>PETROLEUM</strong> <strong><strong>IN</strong>DUSTRY</strong> <strong>REFORM</strong> <strong>IN</strong> <strong>NIGERIA</strong>: A <strong>SIMULATION</strong><br />

ANALYSIS OF ITS IMPACT ON DEEPWATER E&P ECONOMICS<br />

OMOWUNMI O. ILEDARE, PH.D.<br />

PROFESSOR OF <strong>PETROLEUM</strong> ECONOMICS & POLICY RESEARCH<br />

DIRECTOR, ENERGY <strong>IN</strong>FORMATION & DATA DIVISION<br />

BATON ROUGE, LA 70803, USA<br />

29 th USAEE/IAEE NORTH AMERICAN CONFERENCE<br />

ON ENERGY & THE ENVIRONMENT:<br />

Conventional and Unconventional Solutions<br />

14‐16 OCT 2010, CALGARY CANADA<br />

OOILEDARE 26