KPMG PPT - Tax Executives Institute, Inc.

KPMG PPT - Tax Executives Institute, Inc.

KPMG PPT - Tax Executives Institute, Inc.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

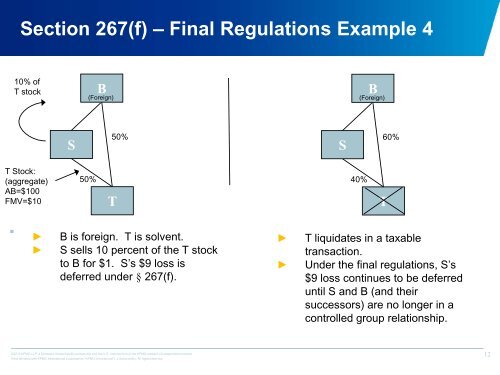

Section 267(f) – Final Regulations Example 4<br />

10% of<br />

T stock<br />

B<br />

(Foreign)<br />

B<br />

(Foreign)<br />

S<br />

50%<br />

S<br />

60%<br />

T Stock:<br />

(aggregate)<br />

AB=$100<br />

FMV=$10<br />

50%<br />

T<br />

40%<br />

T<br />

•<br />

►<br />

►<br />

B is foreign. T is solvent.<br />

S sells 10 percent of the T stock<br />

to B for $1. S’s $9 loss is<br />

deferred under § 267(f).<br />

►<br />

►<br />

T liquidates in a taxable<br />

transaction.<br />

Under the final regulations, S’s<br />

$9 loss continues to be deferred<br />

until S and B (and their<br />

successors) are no longer in a<br />

controlled group relationship.<br />

©2012 <strong>KPMG</strong> LLP, a Delaware limited liability partnership and the U.S. member firm of the <strong>KPMG</strong> network of independent member<br />

firms affiliated with <strong>KPMG</strong> International Cooperative (“<strong>KPMG</strong> International”), a Swiss entity. All rights reserved.<br />

12