2002-03 - Grasim

2002-03 - Grasim

2002-03 - Grasim

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

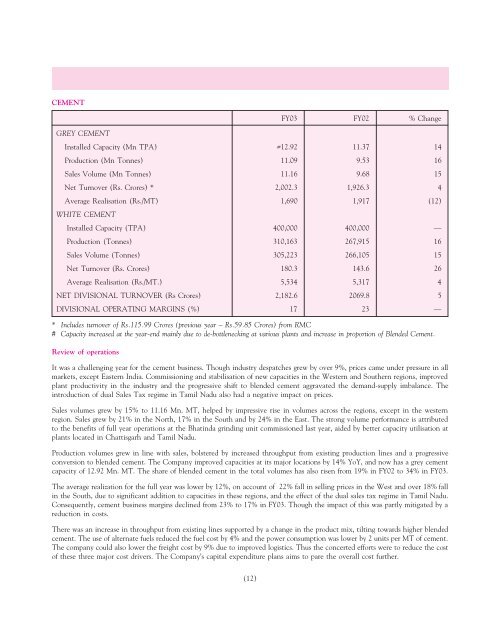

CEMENT<br />

FY<strong>03</strong> FY02 % Change<br />

GREY CEMENT<br />

Installed Capacity (Mn TPA) #12.92 11.37 14<br />

Production (Mn Tonnes) 11.09 9.53 16<br />

Sales Volume (Mn Tonnes) 11.16 9.68 15<br />

Net Turnover (Rs. Crores) * 2,002.3 1,926.3 4<br />

Average Realisation (Rs./MT) 1,690 1,917 (12)<br />

WHITE CEMENT<br />

Installed Capacity (TPA) 400,000 400,000 —<br />

Production (Tonnes) 310,163 267,915 16<br />

Sales Volume (Tonnes) 305,223 266,105 15<br />

Net Turnover (Rs. Crores) 180.3 143.6 26<br />

Average Realisation (Rs./MT.) 5,534 5,317 4<br />

NET DIVISIONAL TURNOVER (Rs Crores) 2,182.6 2069.8 5<br />

DIVISIONAL OPERATING MARGINS (%) 17 23 —<br />

* Includes turnover of Rs.115.99 Crores (previous year – Rs.59.85 Crores) from RMC<br />

# Capacity increased at the year-end mainly due to de-bottlenecking at various plants and increase in proportion of Blended Cement.<br />

Review of operations<br />

It was a challenging year for the cement business. Though industry despatches grew by over 9%, prices came under pressure in all<br />

markets, except Eastern India. Commissioning and stabilisation of new capacities in the Western and Southern regions, improved<br />

plant productivity in the industry and the progressive shift to blended cement aggravated the demand-supply imbalance. The<br />

introduction of dual Sales Tax regime in Tamil Nadu also had a negative impact on prices.<br />

Sales volumes grew by 15% to 11.16 Mn. MT, helped by impressive rise in volumes across the regions, except in the western<br />

region. Sales grew by 21% in the North, 17% in the South and by 24% in the East. The strong volume performance is attributed<br />

to the benefits of full year operations at the Bhatinda grinding unit commissioned last year, aided by better capacity utilisation at<br />

plants located in Chattisgarh and Tamil Nadu.<br />

Production volumes grew in line with sales, bolstered by increased throughput from existing production lines and a progressive<br />

conversion to blended cement. The Company improved capacities at its major locations by 14% YoY, and now has a grey cement<br />

capacity of 12.92 Mn. MT. The share of blended cement in the total volumes has also risen from 19% in FY02 to 34% in FY<strong>03</strong>.<br />

The average realization for the full year was lower by 12%, on account of 22% fall in selling prices in the West and over 18% fall<br />

in the South, due to significant addition to capacities in these regions, and the effect of the dual sales tax regime in Tamil Nadu.<br />

Consequently, cement business margins declined from 23% to 17% in FY<strong>03</strong>. Though the impact of this was partly mitigated by a<br />

reduction in costs.<br />

There was an increase in throughput from existing lines supported by a change in the product mix, tilting towards higher blended<br />

cement. The use of alternate fuels reduced the fuel cost by 4% and the power consumption was lower by 2 units per MT of cement.<br />

The company could also lower the freight cost by 9% due to improved logistics. Thus the concerted efforts were to reduce the cost<br />

of these three major cost drivers. The Company’s capital expenditure plans aims to pare the overall cost further.<br />

(12)