Capital Series Update - ComSec

Capital Series Update - ComSec

Capital Series Update - ComSec

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

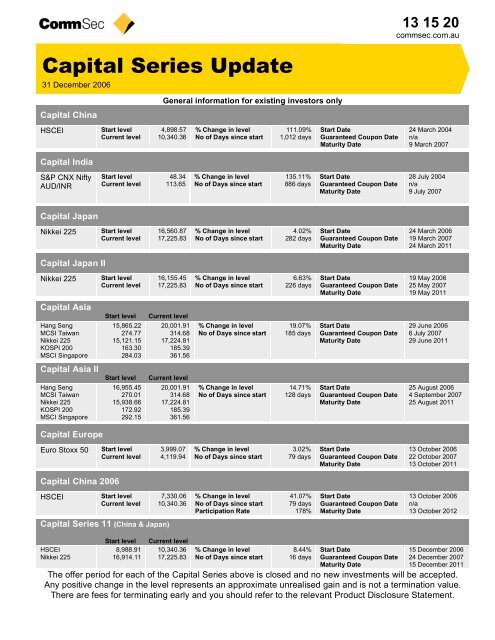

13 15 20<br />

commsec.com.au<br />

<strong>Capital</strong> <strong>Series</strong> <strong>Update</strong><br />

31 December 2006<br />

<strong>Capital</strong> China<br />

HSCEI<br />

<strong>Capital</strong> India<br />

Start level<br />

Current level<br />

General information for existing investors only<br />

4,898.57<br />

10,340.36<br />

% Change in level<br />

No of Days since start<br />

111.09%<br />

1,012 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

24 March 2004<br />

n/a<br />

9 March 2007<br />

S&P CNX Nifty<br />

AUD/INR<br />

Start level<br />

Current level<br />

48.34<br />

113.65<br />

% Change in level<br />

No of Days since start<br />

135.11%<br />

886 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

28 July 2004<br />

n/a<br />

9 July 2007<br />

<strong>Capital</strong> Japan<br />

Nikkei 225<br />

Start level<br />

Current level<br />

16,560.87<br />

17,225.83<br />

% Change in level<br />

No of Days since start<br />

4.02%<br />

282 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

24 March 2006<br />

19 March 2007<br />

24 March 2011<br />

<strong>Capital</strong> Japan II<br />

Nikkei 225<br />

Start level<br />

Current level<br />

16,155.45<br />

17,225.83<br />

% Change in level<br />

No of Days since start<br />

6.63%<br />

226 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

19 May 2006<br />

25 May 2007<br />

19 May 2011<br />

<strong>Capital</strong> Asia<br />

Hang Seng<br />

MCSI Taiwan<br />

Nikkei 225<br />

KOSPI 200<br />

MSCI Singapore<br />

Start level<br />

15,865.22<br />

274.77<br />

15,121.15<br />

163.30<br />

284.03<br />

Current level<br />

20,001.91<br />

314.68<br />

17,224.81<br />

185.39<br />

361.56<br />

% Change in level<br />

No of Days since start<br />

19.07%<br />

185 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

29 June 2006<br />

6 July 2007<br />

29 June 2011<br />

<strong>Capital</strong> Asia II<br />

Hang Seng<br />

MCSI Taiwan<br />

Nikkei 225<br />

KOSPI 200<br />

MSCI Singapore<br />

Start level<br />

16,955.45<br />

270.01<br />

15,938.66<br />

172.92<br />

292.15<br />

Current level<br />

20,001.91<br />

314.68<br />

17,224.81<br />

185.39<br />

361.56<br />

% Change in level<br />

No of Days since start<br />

14.71%<br />

128 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

25 August 2006<br />

4 September 2007<br />

25 August 2011<br />

<strong>Capital</strong> Europe<br />

Euro Stoxx 50<br />

Start level<br />

Current level<br />

3,999.07<br />

4,119.94<br />

% Change in level<br />

No of Days since start<br />

3.02%<br />

79 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

13 October 2006<br />

22 October 2007<br />

13 October 2011<br />

<strong>Capital</strong> China 2006<br />

HSCEI<br />

Start level<br />

Current level<br />

7,330.06<br />

10,340.36<br />

% Change in level<br />

No of Days since start<br />

Participation Rate<br />

41.07%<br />

79 days<br />

178%<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

13 October 2006<br />

n/a<br />

13 October 2012<br />

<strong>Capital</strong> <strong>Series</strong> 11 (China & Japan)<br />

HSCEI<br />

Nikkei 225<br />

Start level<br />

8,988.91<br />

16,914.11<br />

Current level<br />

10,340.36<br />

17,225.83<br />

% Change in level<br />

No of Days since start<br />

8.44%<br />

16 days<br />

Start Date<br />

Guaranteed Coupon Date<br />

Maturity Date<br />

15 December 2006<br />

24 December 2007<br />

15 December 2011<br />

The offer period for each of the <strong>Capital</strong> <strong>Series</strong> above is closed and no new investments will be accepted.<br />

Any positive change in the level represents an approximate unrealised gain and is not a termination value.<br />

There are fees for terminating early and you should refer to the relevant Product Disclosure Statement.

Economic Overview<br />

China<br />

After rising to record highs in early 2007, China’s share markets have lost ground; the Hang Seng China Enterprises<br />

Index (HSCEI) is down 7.5 per cent from 10,766 to 9,944 points. Concerns that a government imposed land tax will<br />

erode earnings of property companies resulted in the sector slumping. However, it is expected that the HSCEI will<br />

likely continue to trend higher in coming months, as corporate balance sheets remain healthy. The performance of the<br />

sharemarket is being underpinned by robust investment and consistent growth in domestic spending. While the<br />

Chinese authorities are attempting to moderate the pace of economic development with monetary policy and fiscal<br />

reforms, there are no signs of a sharp slowdown. Chinese authorities are trying to reduce the economy’s dependence<br />

on exports. With the end of the transitional arrangements for China to join the World Trade Organisation, the<br />

government intends to further open the economy to imports and foreign investment. The government also intends to<br />

reduce exchange rate distortions, but this is likely to happen at a moderate pace.<br />

Japan<br />

The Nikkei has been climbing steadily in recent months and has just surpassed the six-year high of 17,353 points that<br />

was reached in April 2006. After seven months of positive growth in consumer prices, it seems that Japan has shaken<br />

off the deflation era. Since the end to Japan’s quantitative easing policy early in 2006, the Bank of Japan has<br />

increased interest rates only once by a quarter of a per cent to 0.25 per cent. However, economic growth remains<br />

subdued, rising by only 0.8 per cent in annual terms in the September quarter. And speculation of higher interest rates<br />

appears to have had a negative impact on consumers, with retail sales falling by 0.1 per cent in the year to November.<br />

But research by the Bank of Japan indicated that retail spending would prove to be stronger-than-expected over the<br />

end-of-year holiday period. Industrial production rose by 4.8 per cent in the year to November, and while it slowed<br />

markedly from the October figure, it is still well above the 5-year average of around 2.5 per cent.<br />

Europe<br />

The Euro Stoxx 50 index is just below the record highs reached in mid-January. The Euro-zone economy and share<br />

market should be supported by the accommodative interest rate environment. The Euro-zone economy grew at a 2.7<br />

per cent annual pace during the September quarter, just below the 2.8 per cent result for the previous quarter – the<br />

strongest growth in over five years. Inflation for the Euro-zone in November was 1.9 per cent – close to the European<br />

Central Bank’s (ECB) comfort level of 2.0 per cent. The ECB raised interest rates to 3.5 per cent in December - the<br />

third rate hike during 2006. The ECB continually asserts that it will hike rates again if inflationary pressures persist.<br />

However, at its January meeting rates were kept on hold and the tone of the accompanying statement was softened.<br />

Retail sales have been reasonably stable over the second half of 2006. Annual spending growth is 1.3 per cent, the<br />

same rate as 5-year average growth. Unemployment trended lower over the course of 2006 and this should be<br />

supportive of further growth in spending.<br />

India<br />

The Indian economy has experienced rapid industrialisation in recent years, and has grown at an annual rate of 9.2<br />

per cent in the September quarter. The current growth rate is well above the five-year average annual growth rate of<br />

7.2 per cent. The IMF expects growth to be 8.3 per cent over 2006, then moderating to 7.3 per cent in 2007.<br />

Inflationary pressures are the main focus of the Reserve Bank of India (RBI). Interest rates have been lifted three<br />

times in 2006 and look set to rise further in order to cool domestic investment and spending. The RBI is cautiously<br />

optimistic on the outlook for business conditions going into 2007. The RBI business expectations index slowed during<br />

the September quarter but was still firmer than in previous years. The RBI noted that employment is strong, capacity<br />

utilisation is high and that demand should continue to improve as order books were being filled quickly.<br />

You do not need to take any action on this update.<br />

This <strong>Capital</strong> <strong>Series</strong> <strong>Update</strong> is issued by Commonwealth Bank of Australia ABN 48 123 123 124, AFSL 234945 for general information of existing<br />

investors only. Past performance is not a reliable indicator of future performance. The Commonwealth Bank believes the information herein is<br />

correct but makes no warranty as to the accuracy, reliability of completeness of that information. Except to the extent that any liability under any law<br />

cannot be excluded, no liability for any loss or damage which may be suffered by any person, directly or indirectly, through relying upon any<br />

information or statement in this <strong>Capital</strong> <strong>Series</strong> <strong>Update</strong> is accepted by the Commonwealth Bank or any member of the Commonwealth Bank Group,<br />

or their directors, employees or agents, whether that loss or damage is caused by any fault or negligence on the part of their part or otherwise. This<br />

report does not take into account the investment objectives, financial situation or particular needs of any particular individual. These matters should<br />

be considered, with or without professional advice, when deciding if an investment is appropriate.