Executive Investigations

Executive Investigations

Executive Investigations

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

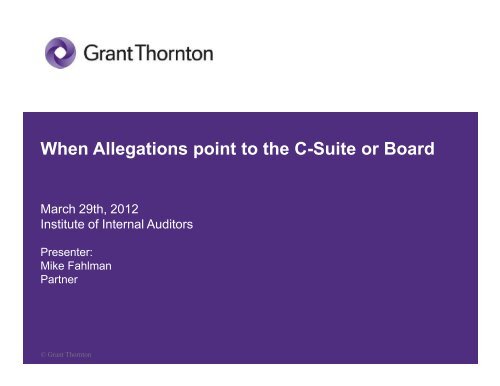

When Allegations point to the C-Suite or Board<br />

March 29th, 2012<br />

Institute of Internal Auditors<br />

Presenter:<br />

Mike Fahlman<br />

Partner<br />

© Grant Thornton

Michael A. Fahlman, CPA/CFF, CIRA<br />

Mike is a Partner in the Forensic and Valuation Services group of Grant Thornton<br />

LLP. He has focused his career on assisting clients, including legal counsel,<br />

boards of directors and executive management, with complex commercial litigation,<br />

dispute resolution, investigations, and distressed businesses. He has served in the<br />

testifying expert and consulting expert roles in litigation, arbitration and mediation,<br />

and as an independent third party in alternative dispute resolutions.<br />

Grant Thornton LLP<br />

Michael.Fahlman@us.gt.com<br />

(213) 596-6739<br />

© Grant Thornton 2

Agenda<br />

• Fraud Background, Trends & <strong>Executive</strong>s<br />

• Investigation Response & Reporting<br />

• Remediation & Restatements<br />

© Grant Thornton 3

Fraud Background, Trends & <strong>Executive</strong>s<br />

What is fraud? (Black's Law definition)<br />

• Wrongful or criminal deception intended to result<br />

in financial or personal gain.<br />

• A person or thing intended to deceive others,<br />

typically by unjustifiably claiming or being credited<br />

with accomplishments or qualities<br />

© Grant Thornton 4

Fraud Background, Trends & <strong>Executive</strong>s<br />

What is occupational fraud? (ACFE's definition)<br />

• The use of one’s occupation for personal<br />

enrichment through the deliberate misuse or<br />

misapplication of the employing organization’s<br />

resources or assets.<br />

© Grant Thornton 5

Fraud Background, Trends & <strong>Executive</strong>s<br />

Fraud Triangle<br />

Fraud<br />

Triangle<br />

Rationalization<br />

© Grant Thornton 6

Fraud Background, Trends & <strong>Executive</strong>s<br />

Why do people commit corporate fraud?<br />

© Grant Thornton 7<br />

* 2007 Oversight Systems Report on Corporate Fraud

Fraud Background, Trends & <strong>Executive</strong>s<br />

Position of Perpetrator in the United States — 968 Cases<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 8

Fraud Background, Trends & <strong>Executive</strong>s<br />

Position of Perpetrator — Median Loss Based on Gender<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 9

Fraud Background, Trends & <strong>Executive</strong>s<br />

Age of Perpetrator – Median Loss<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 10

Fraud Background, Trends & <strong>Executive</strong>s<br />

Tenure of Perpetrator – Median Loss<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 11

Fraud Background, Trends & <strong>Executive</strong>s<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 12

Fraud Background, Trends & <strong>Executive</strong>s<br />

Perpetrator's Criminal Background<br />

Perpetrator's Employment Background<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 13

Fraud Background, Trends & <strong>Executive</strong>s<br />

Schemes Committed by Perpetrators in <strong>Executive</strong>/<br />

Upper Management Positions – 224 Cases<br />

ACFE 2010 Report to the Nations on Occupational Fraud and Abuse<br />

© Grant Thornton 14

Fraud Background, Trends & <strong>Executive</strong>s<br />

FCPA & Dodd-Frank<br />

• Recent reemergence of the Foreign Corrupt Practices Act<br />

– SEC reports receiving an average of one FCPA allegation per day<br />

• Dodd-Frank Whistleblower Program effective August 2011<br />

– Incentivizes reporting of fraud to SEC<br />

• Two acts are linked<br />

– Whistleblower allegations under the Dodd-Frank Act will relate to<br />

FCPA violations<br />

• Internal Audit's Role<br />

© Grant Thornton 15

Fraud Background, Trends & <strong>Executive</strong>s<br />

Dodd-Frank Whistleblower Program<br />

• Background<br />

– July 21, 2010: Dodd-Frank Act signed<br />

– May 25, 2011: Final Whistleblower Program approved<br />

– August 12, 2011: Whistleblower Program became effective<br />

• Rule<br />

– An award is given to a whistleblower who voluntarily provides<br />

the SEC with "original information that leads to the successful<br />

enforcement by the SEC of a federal court or administrative action<br />

in which the SEC obtains monetary sanctions totaling more than<br />

$1 million."<br />

© Grant Thornton 16

"Whistleblower Improvement Act"<br />

• Recently introduced House Bill to modify Whistleblower Program<br />

• Would require whistleblowers to report violations to employer first<br />

– Allows for the following exceptions:<br />

o When wrongdoing is conducted by:<br />

• compliance officers<br />

• highest level of management<br />

o When company does not have a robust internal reporting<br />

mechanism<br />

• Changes payout range from 10-30% to 0-30%<br />

© Grant Thornton 17

Agenda<br />

• Fraud Background, Trends & <strong>Executive</strong>s<br />

• Investigation Response & Reporting<br />

• Remediation & Restatements<br />

© Grant Thornton 18

Investigation Response & Reporting<br />

A whistle is blown regarding the C-Suite or<br />

Board…now what?<br />

© Grant Thornton 19

Investigation Response & Reporting<br />

Acommon process, unique facts and circumstances:<br />

1. Assess the situation<br />

2. Consider internal vs. external investigation<br />

3. Assemble the team<br />

4. Evidence & analysis<br />

5. Reporting<br />

© Grant Thornton 20

Investigation Response & Reporting<br />

Step 1 - Assess the situation<br />

• React immediately upon discovering allegation<br />

• Evaluate nature of allegation – who, what, when, where, why, how<br />

– Source of allegation<br />

– Parties involved – how high up the organization & how pervasive<br />

– Location of incident<br />

– Implications for ongoing operations<br />

• Evaluate stakeholders & reporting<br />

– Management<br />

– Board of Directors / Audit Committee / Special Committee<br />

– External auditors<br />

– Regulators & enforcement bodies<br />

– Shareholders<br />

– Employees / third parties / customers / vendors<br />

© Grant Thornton 21

Investigation Response & Reporting<br />

Step 2 -Internal vs. External<br />

• Internal<br />

– Advantages<br />

o Your organization – know the players<br />

o Access to information<br />

o Less cost<br />

o Less disruptive to normal operations<br />

– Disadvantages<br />

o Independence in fact and appearance<br />

o Senior Management override<br />

o May lack experience/expertise<br />

© Grant Thornton 22

Investigation Response & Reporting<br />

Step 2 -Internal vs. External (con't)<br />

• External<br />

– Advantages<br />

o Expertise, experience, resources<br />

o Credibility (Board, Regulators & External auditors)<br />

o Independent<br />

o Attorney privilege<br />

– Disadvantages<br />

o More costly<br />

o Disrupts normal business operations<br />

© Grant Thornton 23

Investigation Response & Reporting<br />

Step 3 - Assemble The Team<br />

• Multi-disciplinary<br />

– General Counsel vs. Outside Counsel vs. Independent Counsel<br />

– Forensic Accountants<br />

– Computer Data / Electronic Discovery Specialists<br />

– Subject Experts<br />

• Team should have experience in:<br />

– Conducting investigations<br />

– Evidence gathering and preservation<br />

– Reviewing large amounts of data<br />

– Conducting interviews<br />

– Dealing with various stakeholders & reporting/presentations<br />

© Grant Thornton 24

Investigation Response & Reporting<br />

Step 4 -Evidence & Analysis<br />

• Electronic evidence preservation & computer forensics<br />

• Hard copy evidence preservation<br />

• Interviews [Initial round(s)]<br />

• Accounting data [system, network, user share, desktop]<br />

• Source documents<br />

• Pressures, incentives and scenario development<br />

• External environment & information/research<br />

• Interviews [Follow-up round(s)]<br />

• Corroboration<br />

© Grant Thornton 25

Investigation Response & Reporting<br />

Step 5 -Reporting<br />

• Stakeholders<br />

• Regulators<br />

• Plaintiffs & law suits<br />

• Report vs. Presentation vs. Verbal<br />

• Attorney work product & distribution<br />

• External auditors and the "shadow investigation"<br />

• Remediation<br />

© Grant Thornton 26

Agenda<br />

• Fraud Background, Trends & <strong>Executive</strong>s<br />

• Investigation Response & Reporting<br />

• Remediation & Restatements<br />

© Grant Thornton 27

Remediation & Restatements<br />

Common remediation points<br />

• Policies and procedures<br />

• Internal controls<br />

• Personnel actions & leadership changes<br />

• Documentation & retention<br />

• Training<br />

• Fraud "tools" & "programs"<br />

• Internal compliance/audit<br />

© Grant Thornton 28

Remediation & Restatements<br />

Remediation considerations<br />

• Non-disclosed remediation<br />

• Timing of remediation<br />

• External auditor involvement<br />

• Management buy-in<br />

• Who performs the remediation<br />

• Resources to get it done<br />

• Oversight and subsequent period follow-up<br />

© Grant Thornton 29

Remediation & Restatements<br />

Restatement considerations<br />

• Public vs. Private company<br />

• Stakeholders beyond shareholders, including bank and<br />

related covenants<br />

• Who prepares the restatement<br />

• Starting point for restatement<br />

• # of years of presentation<br />

© Grant Thornton 30

Remediation & Restatements<br />

Restatement considerations<br />

• Time table and pending deadlines<br />

– SEC Filings<br />

– Bank covenants<br />

– Capital raises<br />

– Product release<br />

• Legal privileges re: investigators' work papers<br />

• Representation & certification – departed employees<br />

• Potential lawsuits and other legal liabilities, and related<br />

disclosures / accruals<br />

© Grant Thornton 31

Closing and Questions<br />

Mike Fahlman<br />

Partner<br />

Forensic and Valuation Services<br />

515 South Flower Street<br />

7 th Floor<br />

Los Angeles, CA 90071<br />

Michael.Fahlman@us.gt.com<br />

(213) 596-6739<br />

Grant Thornton: www.grantthornton.com<br />

© Grant Thornton 32