expenses which can be directly attributed to the project. (4) The capital expenditure providedto NSAI by the Partnership, which appear reasonable, is based, inter alia, on thedevelopment plan in the Tamar project and on NSAI's experience in similar projects. Thecapital expenditure taken into account is the capital expenditure required to develop andcomplete wells, develop new wells and for production equipment. As required by thePartnership, these costs remain fixed until actually expended; 74 (5) The abandonment coststaken into account are costs provided to NSAI by the Partnership according to itsassessments of the cost of abandoning wells, platforms and production facilities. Thesecosts do not take into account the salvage value of the Tamar lease and facilities in theTamar field. As required by the Partnership, abandonment costs remain fixed until actuallyexpended. (6) The tax calculations take into account corporate tax rates provided to NSAI bythe Partnership, which are the expected tax rates for each of the years included in thediscounted cash flows. (7) Actual production capacity for each of the reserve categoriesdescribed above could be lower or higher than the production capacity used to estimate thediscounted cash flows. In addition, NSAI did not prepare a sensitivity analysis for theproduction capacity of the wells. A sensitivity analysis could lead to a conclusion that thereserves are not feasible for production.It is noted that the discounted cash flow does not take into account revenue and/or expensesrelating to the offshore project for liquefaction of gas for export as set out in section 7.26.8below.שגיאה! It is further noted that the discounted cash flow includes royalties as set out in sectionabove, and petroleum profits tax applicable to the Partnership in מקור ההפניה לא נמצא.accordance with the Taxation of Petroleum Profits Law ("the Law"). It is emphasized thatcalculation of the levy was based on the definitions, formulas and mechanisms set out in thelaw as understood and interpreted by the Partnership, however, since the law is new and thecalculation formulas and mechanisms set out in the law are complex, it is not certain whetherthis interpretation of the calculation method for the levy will be the same as that adopted bythe tax authorities and/or the same as the interpretations of the law by the court, insofar as aruling is required on these issues. To date, these issues have not been brought before thecourts in Israel. The levy was calculated according to the transitional provisions in the law fora project that started commercial production before the Law came into effect, based on thefollowing assumptions: The developer will report in US dollars according to section 13(B) ofthe law, the rate of inflation in the United States in the coming years will be 2%, all of thedeveloper's payments (production costs and investments) will be recognized by the taxauthorities for calculation of the levy and calculation of the developers revenues will take intoaccount actual selling prices of the gas.Following is the estimated discounted cash flows at December 31, <strong>2011</strong>, in thousands ofUSD (after the levy and income tax) attributable to the Partnership's share in the reserves inthe Tamar field for each of the reserve categories set out above (the cash flow is based onassumptions, which are described above). It is noted that there is a significant change in thediscounted cash flow compared to that published in the shelf prospectus of July 22, <strong>2011</strong>(which was the same as of March 31, <strong>2011</strong>), for the following reasons: (1) change in theforecasted quantities of sales in each of the project years, due to signing gas supplycontracts and estimates for the scope of market demand; (2) change in estimated sellingprices, in view of prices in gas supply agreements signed recently; (3) the scope of thePartnership’s actual investments in the project as from June <strong>2011</strong> until the end of <strong>2011</strong>; (4)the effect of the passage of time on the discounted cash flow; (5) change in estimatedongoing investments and capital investments in view of the updated estimates; (6)elimination of the tax reduction that was expected in the past, which also resulted in achange in the expected maximum levy in accordance with the Petroleum Profits Tax Law.74The capital investments taken into account when preparing the discounted cash flow exceed the development costsapproved by the Partnership for development of the Tamar lease, and it also includes estimated costs of futureinvestments after production starts for use of part of the development facilities of the Yam Tethys project andexpansion of output at the receiving terminal in Ashdod. These investments have not yet been approved by theproject partners.A-59

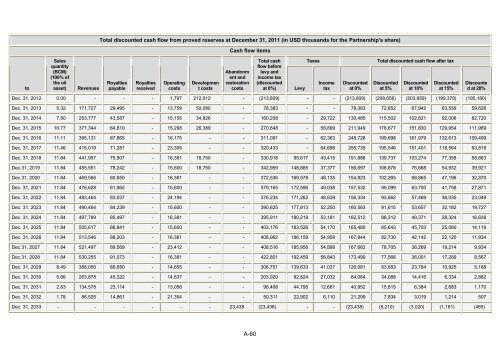

Total discounted cash flow from proved reserves at December 31, <strong>2011</strong> (in USD thousands for the Partnership's share)Cash flow itemstoSalesquantity(BCM)(100% ofthe oilasset)RevenuesRoyaltiespayableRoyaltiesreceivedOperatingcostsDevelopment costsAbandonment andrestorationcostsTotal cashflow beforelevy andincome tax(discountedat 0%)LevyTaxesIncometaxDiscountedat 0%Total discounted cash flow after taxDiscountedat 5%Discountedat 10%Discountedat 15%Discounted at 20%Dec. 31, 2012 0.00 - - - 1,797 212,012 - (213,809) - - (213,809) (208,656) (203,859) (199,378) (195,180)Dec. 31, 2013 5.32 171,727 6,,0,6 - 13,759 50,090 - 11,313 - - 11,313 16,166 21,,06 23,66, 6,,261Dec. 31, 2014 7.50 253,777 03,611 - 15,155 34,826 - 021,611 - 6,,166 031,016 006,616 016,160 ,6,112 16,161Dec. 31, 2015 10.77 377,344 20,101 - 15,298 26,389 - 611,101 - 61,1,, 600,,0, 011,211 060,131 06,,,60 000,,2,Dec. 31, 2016 11.11 395,131 21,126 - 16,175 - - 300,1,0 - 26,323 601,161 0,,,2,1 020,,1, 036,203 01,,0,,Dec. 31, 2017 11.46 415,019 10,610 - 23,305 - - 361,033 - 20,2,1 666,136 0,6,602 060,010 001,620 ,3,10,Dec. 31, 2018 11.84 441,957 16,,11 - 16,381 18,750 - 331,,01 ,6,201 03,006 0,0,112 03,,131 013,610 11,361 61,223Dec.31, 2019 11.84 455,551 11,606 - 15,600 18,750 - 306,,6, 001,116 31,311 062,2,1 011,211 12,221 60,,36 3,,,60Dec.31, 2020 11.84 469,566 11,261 - 16,381 - - 316,632 02,,611 01,036 060,163 016,626 21,126 01,0,2 36,111Dec. 31, 2021 11.84 476,628 10,126 - 15,600 - - 31,,026 016,6,2 0,,131 061,636 ,,,1,, 23,111 00,161 61,110Dec. 31, 2022 11.84 483,464 13,131 - 24,194 - - 312,630 010,626 01,231 062,330 ,3,226 61,02, 32,136 63,10,Dec. 31, 2023 11.84 490,464 10,63, - 15,600 - - 3,1,266 011,103 66,661 021,623 ,0,206 63,261 36,016 0,,161Dec. 31, 2024 11.84 497,789 16,0,1 - 16,381 - - 3,6,,00 011,60, 63,010 026,606 11,306 0,,310 61,360 02,23,Dec. 31, 2025 11.84 505,617 12,100 - 15,600 - - 013,012 013,662 60,011 026,011 16,203 06,113 66,111 00,00,Dec. 31, 2026 11.84 513,546 11,613 - 16,381 - - 011,,26 012,06, 60,,61 021,100 16,131 06,006 66,061 00,,30Dec.31, 2027 11.84 521,497 1,,62, - 23,412 - - 011,602 016,,62 60,1,1 021,226 11,116 31,62, 0,,600 ,,,30Dec.31, 2028 11.84 530,255 ,0,113 - 16,381 - - 066,110 0,6,06, 62,103 013,0,, 11,622 32,110 01,61, 1,621Dec. 31, 2029 8.49 388,056 22,261 - 14,655 - - 312,160 03,,233 00,131 062,110 63,213 63,110 01,,66 6,011Dec. 31, 2030 5.66 263,878 06,366 - 14,637 - - 613,,61 ,6,160 61,136 10,120 30,111 00,002 2,330 6,116Dec. 31, 2031 2.83 134,578 63,000 - 13,056 - - ,1,011 00,1,6 06,220 01,,66 06,106 2,310 6,213 0,011Dec. 31, 2032 1.78 86,526 00,120 - 21,354 - - 61,300 66,,16 2,001 60,6,, 1,130 3,10, 0,600 611Dec. 31, 2033 - - - - - - 23,438 (23,438) - - (23,438) (8,210) (3,020) (1,161) (465)A-60

- Page 4:

All English versions / translation

- Page 7 and 8:

2.5 Map of the Limited Partnership'

- Page 9 and 10:

351/Hannah, 352/David and 353/Eran

- Page 11 and 12: Law), which sets out provisions for

- Page 13 and 14: (D)(E)(F)(G)(H)(I)(J)(K)(L)(M)Exami

- Page 15 and 16: The Natural Gas Sector Law and its

- Page 17 and 18: Description of the Partnership's oi

- Page 19 and 20: The main terms of the leases in the

- Page 21 and 22: Noa leasePeriodSummary of the opera

- Page 23 and 24: 7.3.7 Calculation of the effective

- Page 25 and 26: the oil asset (before other payment

- Page 27 and 28: DescriptionBudget actually invested

- Page 29 and 30: have not been brought before the co

- Page 31 and 32: Salesquantity(BCM)(100% of theoil a

- Page 33 and 34: Salesquantity(BCM)(100% of theoil a

- Page 35 and 36: (4) Production dataThe following ta

- Page 37 and 38: on the project level and the Partne

- Page 39 and 40: Sensitivity analysis for the main p

- Page 42 and 43: (3) Basic parameters used to calcul

- Page 44 and 45: 7.4 Tamar project7.4.1 GeneralTamar

- Page 46 and 47: 7.4.2 Main terms of the I/12 Tamar

- Page 48 and 49: (C)If the Commissioner postpones or

- Page 50 and 51: (F)(G)(H)(I)(J)(K)(1) The leasehold

- Page 52 and 53: 7.4.5 Actual work plan and intended

- Page 54 and 55: PeriodDalit leaseSummary of the ope

- Page 56 and 57: Dalit leaseParticipation rate %Perc

- Page 58 and 59: DescriptionEffective share attribut

- Page 60 and 61: 7.4.9 Royalties and payments paid d

- Page 64 and 65: Total discounted cash flow from pro

- Page 66 and 67: Total discounted cash flow from pro

- Page 68 and 69: Total discounted cash flow from pos

- Page 70 and 71: Sensitivity/categoryTotalPresentval

- Page 72 and 73: Contingent resources in the Dalit l

- Page 74 and 75: ParameterPorosity (decimal)Lowestim

- Page 76 and 77: 7.5 Ratio Yam licenses7.5.1 General

- Page 78 and 79: The following are the planned activ

- Page 80 and 81: PeriodEran licenseDescription of th

- Page 82 and 83: PeriodAmit licenseSummary of the op

- Page 84 and 85: Hannah licensePeriodSummary of the

- Page 86 and 87: PeriodEran licenseSummary of the op

- Page 88 and 89: 7.5.7 Calculation of the effective

- Page 90 and 91: (B)(C)(D)(E)B. A statistical progra

- Page 92 and 93: 7.5.10 Prospective resources in the

- Page 94 and 95: ParameterLower-Oligocene(%)Mid-Cret

- Page 96 and 97: (D)(E)(F)(G)(4) The contingent reso

- Page 98 and 99: 7.5.12 Prospective resources in the

- Page 100 and 101: PeriodDescription of the updated wo

- Page 102 and 103: Description%Summary of the calculat

- Page 104 and 105: 7.6.8 Royalties and payments paid d

- Page 106 and 107: 7.7.3 Binding work plan according t

- Page 108 and 109: 7.7.5 Disclosure of the effective p

- Page 110 and 111: 7.7.8 Royalties and payments paid d

- Page 112 and 113:

General information about the Partn

- Page 114 and 115:

PeriodDescription of the updated wo

- Page 116 and 117:

Description %Summary of the calcula

- Page 118 and 119:

7.8.10 Royalties and payments paid

- Page 120 and 121:

(B)(C)The report was based on the r

- Page 122 and 123:

7.9 Petroleum licenses that were re

- Page 124 and 125:

7.10 Products and servicesDuring th

- Page 126 and 127:

7.11.3 Agreements to sell natural g

- Page 128 and 129:

At the signing date of the letter o

- Page 130 and 131:

(G)addition, Yam Tethys partners ha

- Page 132 and 133:

(B)(13) Breach and damages: Accordi

- Page 134 and 135:

(D)Agreement to sell natural gas to

- Page 136 and 137:

(4) The gas price stipulated in the

- Page 138 and 139:

energy market is characterized by h

- Page 140 and 141:

7.20 Financing7.20.1 General(A)(B)(

- Page 142 and 143:

The dollar-denominated loan bears a

- Page 144 and 145:

tests 157 ; compliance with the res

- Page 146 and 147:

(E)financing agreement; purchase of

- Page 148 and 149:

(C)Tamar financing agreementFinanci

- Page 150 and 151:

As set out above, under licenses an

- Page 152 and 153:

(C) Petroleum Regulations (Principl

- Page 154 and 155:

The gas facilities that the license

- Page 156 and 157:

(2) Without derogating from the gen

- Page 158 and 159:

B. The operator of an offshore righ

- Page 160 and 161:

subsection (4) below exist (conditi

- Page 162 and 163:

Furthermore, the draft regulations

- Page 164 and 165:

(D)(E)(F)(G)(H)(I)(J)months after c

- Page 166 and 167:

(N)(O)(9) If a revised assessment i

- Page 168 and 169:

# Assumption Details and explanatio

- Page 170 and 171:

7.24 AntitrustOn October 12, 2000,

- Page 172 and 173:

(C)For expenses associated with dev

- Page 174 and 175:

(F)(G)(H)committee of the joint ven

- Page 176 and 177:

(L)(M)(N)(O)accumulated according t

- Page 178 and 179:

(D)(E)Subject to the terms of the o

- Page 180 and 181:

(I)(J)committee meetings, and will

- Page 182 and 183:

obtaining Cypriot government approv

- Page 184 and 185:

(5) It is noted that under Regulati

- Page 186 and 187:

Contingent agreements for the sale

- Page 188 and 189:

had not yet been received, although

- Page 190 and 191:

Liquefaction (LNG) The Partnership

- Page 192 and 193:

7.30 Risk factorsOil and gas explor

- Page 194 and 195:

in deviations in the budget (expect

- Page 196 and 197:

process for transferring the rights

- Page 198 and 199:

GlossaryAppraisal well: a drilling

- Page 201 and 202:

Avner Oil Exploration Limited Partn

- Page 203 and 204:

The effects of the increase in sale

- Page 205 and 206:

USD 6.5 million, as noted above. In

- Page 207 and 208:

investment in development of the Ta

- Page 209 and 210:

marine areas on the Cyprus continen

- Page 211 and 212:

Part II: Market Risks - Exposure an

- Page 213 and 214:

As collateral for the Partnership's

- Page 215 and 216:

3. Independent directorsThe Compani

- Page 217 and 218:

5. External auditors' feesThe amoun

- Page 219 and 220:

4) Accepting a financial liability

- Page 221 and 222:

Project cash flow (in USD millions)

- Page 224 and 225:

AVNER OIL EXPLORATION (LIMITED PART

- Page 226 and 227:

Auditors' Report to the Partners of

- Page 228 and 229:

Avner Oil Explorations - Limited Pa

- Page 230 and 231:

Avner Oil Explorations - Limited Pa

- Page 232 and 233:

Avner Oil Explorations - Limited Pa

- Page 234 and 235:

AVNER OIL EXPLORATION (LIMITED PART

- Page 236 and 237:

AVNER OIL EXPLORATION (LIMITED PART

- Page 238 and 239:

AVNER OIL EXPLORATION (LIMITED PART

- Page 240 and 241:

AVNER OIL EXPLORATION (LIMITED PART

- Page 242 and 243:

AVNER OIL EXPLORATION (LIMITED PART

- Page 244 and 245:

AVNER OIL EXPLORATION (LIMITED PART

- Page 246:

AVNER OIL EXPLORATION (LIMITED PART

- Page 249 and 250:

Untimely Meditationshad only you, t

- Page 252 and 253:

AVNER OIL EXPLORATION (LIMITED PART

- Page 254 and 255:

AVNER OIL EXPLORATION (LIMITED PART

- Page 256 and 257:

AVNER OIL EXPLORATION (LIMITED PART

- Page 258 and 259:

AVNER OIL EXPLORATION (LIMITED PART

- Page 260 and 261:

AVNER OIL EXPLORATION (LIMITED PART

- Page 262 and 263:

AVNER OIL EXPLORATION (LIMITED PART

- Page 264 and 265:

AVNER OIL EXPLORATION (LIMITED PART

- Page 266 and 267:

AVNER OIL EXPLORATION (LIMITED PART

- Page 268 and 269:

AVNER OIL EXPLORATION (LIMITED PART

- Page 270 and 271:

AVNER OIL EXPLORATION (LIMITED PART

- Page 272 and 273:

AVNER OIL EXPLORATION (LIMITED PART

- Page 274 and 275:

AVNER OIL EXPLORATION (LIMITED PART

- Page 276 and 277:

AVNER OIL EXPLORATION (LIMITED PART

- Page 278 and 279:

AVNER OIL EXPLORATION (LIMITED PART

- Page 280 and 281:

AVNER OIL EXPLORATION (LIMITED PART

- Page 282 and 283:

AVNER OIL EXPLORATION (LIMITED PART

- Page 284 and 285:

AVNER OIL EXPLORATION (LIMITED PART

- Page 286 and 287:

AVNER OIL EXPLORATION (LIMITED PART

- Page 288 and 289:

AVNER OIL EXPLORATION (LIMITED PART

- Page 290 and 291:

AVNER OIL EXPLORATION (LIMITED PART

- Page 292 and 293:

AVNER OIL EXPLORATION (LIMITED PART

- Page 294 and 295:

AVNER OIL EXPLORATION (LIMITED PART

- Page 296 and 297:

AVNER OIL EXPLORATION (LIMITED PART

- Page 298 and 299:

AVNER OIL EXPLORATION (LIMITED PART

- Page 300 and 301:

AVNER OIL EXPLORATION (LIMITED PART

- Page 302 and 303:

AVNER OIL EXPLORATION (LIMITED PART

- Page 304 and 305:

AVNER OIL EXPLORATION (LIMITED PART

- Page 306:

AVNER OIL EXPLORATION (LIMITED PART

- Page 309 and 310:

Regulation 10A: Summary of the Part

- Page 311 and 312:

Regulation 12:Regulation 13:Regulat

- Page 313 and 314:

C. Interested parties in the Partne

- Page 315 and 316:

Regulation 24:will not be able to d

- Page 317 and 318:

Regulation 24B: Holders of the Part

- Page 319 and 320:

10. Occupation in the past five yea

- Page 321 and 322:

9. Education: LLB, Tel Aviv Univers

- Page 323 and 324:

Ronen Edward (ID 024652745)1. Date

- Page 325:

executive liability insurance, base

- Page 328 and 329:

Avner Oil Exploration - Limited Par

- Page 330:

Declaration of the CFO based on Reg