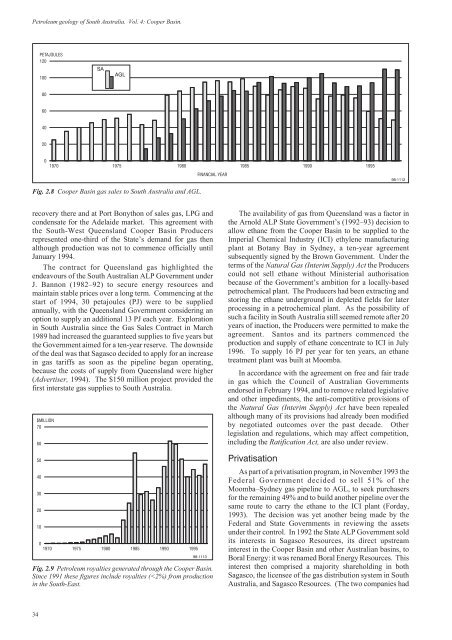

Petroleum geology <strong>of</strong> South Australia. Vol. 4: Cooper Basin.PETAJOULES120100SAAGL8060402001970 1975 1980 1985 1990 1995FINANCIAL YEAR98-1112Fig. 2.8 Cooper Basin gas sales to South Australia <strong>and</strong> AGL.recovery there <strong>and</strong> at Port Bonython <strong>of</strong> sales gas, LPG <strong>and</strong>condensate for the Adelaide market. This agreement withthe South-West Queensl<strong>and</strong> Cooper Basin Producersrepresented one-third <strong>of</strong> the State’s dem<strong>and</strong> for gas thenalthough production was not to commence <strong>of</strong>ficially untilJanuary 1994.The contract for Queensl<strong>and</strong> gas highlighted theendeavours <strong>of</strong> the South Australian ALP Government underJ. Bannon (1982–92) to secure energy resources <strong>and</strong>maintain stable prices over a long term. Commencing at thestart <strong>of</strong> 1994, 30 petajoules (PJ) were to be suppliedannually, with the Queensl<strong>and</strong> Government considering anoption to supply an additional 13 PJ each year. Explorationin South Australia since the Gas Sales Contract in March1989 had increased the guaranteed supplies to five years butthe Government aimed for a ten-year reserve. The downside<strong>of</strong> the deal was that Sagasco decided to apply for an increasein gas tariffs as soon as the pipeline began operating,because the costs <strong>of</strong> supply from Queensl<strong>and</strong> were higher(Advertiser, 1994). The $150 million project provided thefirst interstate gas supplies to South Australia.$MILLION7060504030201001970 1975 1980 1985 1990 199598-1113Fig. 2.9 Petroleum royalties generated through the Cooper Basin.Since 1991 these figures include royalties (

Petroleum geology <strong>of</strong> South Australia. Vol. 4: Cooper Basin.$MILLION10080604020Trenching in preparation for laying <strong>of</strong> South-West Queensl<strong>and</strong> gaspipeline to South Australia, 80 km northeast <strong>of</strong> Moomba, April1992. (Photo 40368)merged in April 1987.) The next sale was <strong>of</strong> PASA’spipeline interests to Tenneco (now Epic Energy) in mid1995. The PASA gas sales contracts with ETSA <strong>and</strong>Sagasco were transferred to a new Natural Gas Authority <strong>of</strong>South Australia. The contracts for additional gas suppliesbetween the Producers <strong>and</strong> ETSA <strong>and</strong> Sagasco were affectedin mid 1996: the Producers made separate contracts withthese organisations for gas supplies mainly beyond 2004.Further Cooper Basin gas discoveries are now necessary toallow new major contracts to be sought for bulk short-termor long-term supply. The recent corporatisation <strong>of</strong> ETSA(now ETSA Corporation <strong>and</strong> Optima Energy) was asignificant change to the local energy scene. This had littleimmediate impact on activity in the Cooper Basin althoughthere may be some impact in the longer term as the StateGovernment announced in February 1998 that ETSACorporation <strong>and</strong> Optima Energy were to be sold.Ongoing <strong>exploration</strong> <strong>and</strong> <strong>development</strong>Since 1959 more than 1200 <strong>exploration</strong> <strong>and</strong> <strong>development</strong>wells have been drilled by Santos <strong>and</strong> its joint venturepartners, with 146 oil <strong>and</strong> gas fields previously or currentlyon stream, <strong>and</strong> ~80 000 km <strong>of</strong> 2D <strong>and</strong> ~3 km 2 <strong>of</strong> 3D seismicdata have been recorded in the Cooper <strong>and</strong> EromangaBasins. Over the past 28 years <strong>exploration</strong> programs havebeen undertaken to add gas reserves to meet specificcontracts such as for the 1970–72 AGL agreement, 1979–81SAOG sole risk program, the Accelerated Gas Program <strong>of</strong>1983–85 <strong>and</strong> the 1990–92 program for PASA’s forwardcontract (Fig. 2.10). The latest program was announcedearly in 1996 <strong>and</strong> involves a three-year, $200 millionexpenditure by Santos to drill 125 <strong>exploration</strong> <strong>and</strong> appraisalwells. The aim was to take advantage <strong>of</strong> the impendingderegulated gas market by locking in new discoveries toshort-term gas contracts. In addition, with the imminentexpiry <strong>of</strong> PELs 5 <strong>and</strong> 6 an attempt was made to drill as manyoil <strong>and</strong> gas prospects as possible to maximise the area underPPLs by February 1999.This <strong>exploration</strong> program discovered two oil <strong>and</strong> sevengas fields in 1996 <strong>and</strong> one oil field in 1997 from a total <strong>of</strong> 48<strong>exploration</strong> wells. New gas fields which are relatively richin liquids are produced preferentially to take advantage <strong>of</strong>the increased sales value associated with the gas. To date01958 1964 1970 1976 1982 1988 199498-1114Fig. 2.10 Expenditure on <strong>petroleum</strong> <strong>exploration</strong> in the Cooper <strong>and</strong>Eromanga Basins.~129 x 10 9 m 3 (4.6 tcf) <strong>of</strong> gas <strong>and</strong> 4.6 x 10 6 kL (29.1 mmstb)<strong>of</strong> oil <strong>and</strong> condensate have been produced from the CooperBasin.Production has been obtained from all reservoir-bearingunits in the Cooper Basin. While earlier <strong>exploration</strong> focusedon simple anticlines <strong>and</strong> faulted anticlines, more recent<strong>exploration</strong> has involved untested structural downdip flanks,stratigraphic plays <strong>and</strong> areas <strong>of</strong> tight gas reservoirs withpotential for large reserves. As the search has become morerefined, improved seismic acquisition (including 3D) <strong>and</strong>processing has helped to produce better results (Heath,1989). New technologies have also proved important,especially in areas <strong>of</strong> poor quality oil <strong>and</strong> gas reservoirs (Ch.11).The discoveries in the 1980s <strong>and</strong> 1990s included theSturt, Taloola <strong>and</strong> Tantanna oil fields near the edge <strong>of</strong> theCooper Basin. Significantly, Sturt 6 discovered oil inCambrian volcanics <strong>and</strong> Lycosa 1 <strong>and</strong> Moolalla 1 tested gasin the Ordovician. Although the source rocks for thesehydrocarbons are Permian, the reservoirs are in WarburtonBasin rocks, conventionally regarded as basement (Taylor etal., 1991). Each discovery by the Producers <strong>of</strong>fset thedecline in the oil <strong>and</strong> gas reserves <strong>of</strong> the region.From the early 1990s Santos, perhaps recognising thatthe expected end in 1999 to the company’s monopolisingrole in the Cooper <strong>and</strong> Eromanga Basins would present itwith fresh challenges, began to diversify its <strong>exploration</strong> <strong>and</strong><strong>development</strong> activities beyond PELs 5 <strong>and</strong> 6. As 1999 drewcloser, however, Santos re-asserted its interest in theprospectivity <strong>of</strong> the Cooper Basin. In South Australia in1997 it carried out 2419 km <strong>of</strong> 2D <strong>and</strong> 1888 km 2 <strong>of</strong> 3Dseismic <strong>and</strong> drilled 62 wells comprising 22 <strong>exploration</strong> wells(9 for gas <strong>and</strong> 1 for oil were successful), 13 appraisal wells<strong>and</strong> 27 <strong>development</strong> wells. Santos's <strong>exploration</strong> program for1998 was <strong>of</strong> a similar magnitude.CONCLUSIONTraps in the Cooper Basin <strong>and</strong> the overlying EromangaBasin are seismically mappable <strong>and</strong> the identification <strong>of</strong> oil<strong>and</strong> gas reservoirs has been protracted. One result withimportant repercussions for <strong>petroleum</strong> <strong>exploration</strong> <strong>and</strong><strong>development</strong> was that the initial success, notably gas at35