Vorm V1 - Maksu- ja Tolliamet

Vorm V1 - Maksu- ja Tolliamet

Vorm V1 - Maksu- ja Tolliamet

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

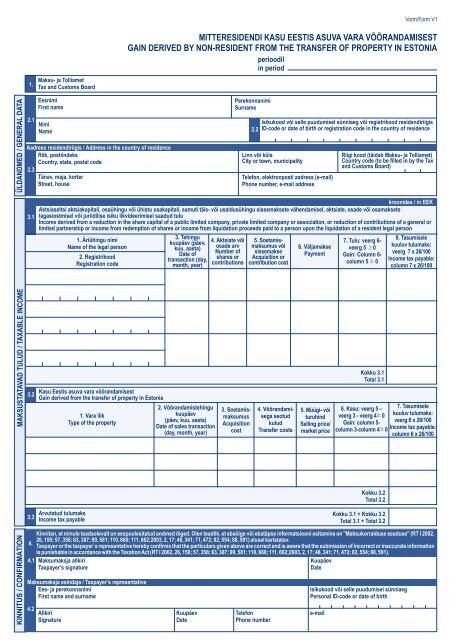

1.<strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>Tax and Customs Board<strong>Vorm</strong>/Form <strong>V1</strong>MITTERESIDENDI KASU EESTIS ASUVA VARA VÕÕRANDAMISESTGAIN DERIVED BY NON-RESIDENT FROM THE TRANSFER OF PROPERTY IN ESTONIAperioodilin periodÜLDANDMED / GENERAL DATA2.12.3EesnimiFirst nameNimiNameAadress residendiriigis / Address in the country of residenceRiik, postiindeksCountry, state, postal codeTänav, ma<strong>ja</strong>, korterStreet, housePerekonnanimiSurname2.2Isikukood või selle puudumisel sünniaeg või registrikood residendiriigisID-code or date of birth or registration code in the country of residenceLinn või külaCity or town, municipalityTelefon, elektronposti aadress (e-mail)Phone number, e-mail addressRiigi kood (täidab <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>)Country code (to be filled in by the Taxand Customs Board)3.1kroonides / in EEKAktsiaseltsi aktsiakapitali, osaühingu või ühistu osakapitali, samuti täis- või usaldusühingu sissemaksete vähendamisel, aktsiate, osade või osamaksetetagasiostmisel või juriidilise isiku likvideerimisel saadud tuluIncome derived from a reduction in the share capital of a public limited company, private limited company or association, or reduction of contributions of a general orlimited partnership or income from redemption of shares or income from liquidation proceeds paid to a person upon the liquidation of a resident legal person1. Äriühingu nimiName of the legal person2. RegistrikoodRegistration code3. Tehingukuupäev (päev,kuu, aasta)Date oftransaction (day,month, year)4. Aktsiate võiosade arvNumber ofshares orcontributions5. SoetamismaksumusvõisissemakseAcquisition orcontribution cost6. Väl<strong>ja</strong>maksePayment7. Tulu: veerg 6-veerg 5 0Gain: Column 6-column 5 08. Tasumiselekuuluv tulumaks:veerg 7 x 26/100Income tax payable:column 7 x 26/100MAKSUSTATAVAD TULUD / TAXABLE INCOME3.2Kasu Eestis asuva vara võõrandamisestGain derived from the transfer of property in Estonia1. Vara liikType of the property2. Võõrandamistehingukuupäev(päev, kuu, aasta)Date of sales transaction(day, month, year)3. SoetamismaksumusAcquisitioncost4. VõõrandamisegaseotudkuludTransfer costs5. Müügi- võituruhindSelling price/market priceKokku 3.1Total 3.16. Kasu: veerg 5 –veerg 3 - veerg 4 0Gain: column 5-column 3-column 4 07. Tasumiselekuuluv tulumaks:veerg 6 x 26/100Income tax payable:column 6 x 26/100Kokku 3.2Total 3.23.3Arvutatud tulumaksIncome tax payableKokku 3.1 + Kokku 3.2Total 3.1 + Total 3.2KINNITUS / CONFIRMATIONKinnitan, et minule teadaolevalt on eespoolesitatud andmed õiged. Olen teadlik, et ebaõige või ebatäpse informatsiooni esitamine on "<strong>Maksu</strong>korralduse seaduse" (RT I 2002,4.26, 150; 57, 358; 63, 387; 99, 581; 110, 660; 111, 662;2003, 2, 17; 48, 341; 71, 472; 82, 554; 88, 591) alusel karistatav.Taxpayer or the taxpayer`s representative hereby confirms that the particulars given above are correct and is aware that the submission of incorrect or inaccurate informationis punishable in accordance with the Taxation Act (RT I 2002, 26, 150; 57, 358; 63, 387; 99, 581; 110, 660; 111, 662;2003, 2, 17; 48, 341; 71, 472; 82, 554; 88, 591).4.1 <strong>Maksu</strong>maks<strong>ja</strong> allkiriKuupäevTaxpayer’s signatureDate<strong>Maksu</strong>maks<strong>ja</strong> esinda<strong>ja</strong> / Taxpayer’s representativeEes- <strong>ja</strong> perekonnanimiFirst name and surname4.2AllkiriSignatureKuupäevDateTelefonPhone numberIsikukood või selle puudumisel sünniaegPersonal ID-code or date of birthe-mail

Märkused / Notes21. <strong>Vorm</strong>i <strong>V1</strong> täidab mitteresident, kes sai maksustamisperioodil "Tulumaksuseaduse" § 29 lõigetes 4 <strong>ja</strong> 5 loetletud tulu. Deklaratsioon täidetaksetäiskroonides, seejuures jäetakse vähem kui 50 senti ära ning 50 <strong>ja</strong> rohkem senti ümardatakse täiskrooniks.The form <strong>V1</strong> shall be filled in by a non-resident who received gains prescribed in § 29 (4) and (5) of the Income Tax Act during taxable period. The returnshall be filled in full kroons. Upon calculation, amounts less than 50 sents shall not be taken into account and amounts of 50 sents and more shall berounded to the nearest full kroon.2. Tabelis 3.1 näidatakse "Tulumaksuseaduse" § 15 lõike 2 alusel aktsiaseltsi aktsiakapitali, osaühingu või ühistu osakapitali või täis- või usaldusühingusissemaksete vähendamisel, samuti aktsiate või osade tagasiostmisel isikule tehtav väl<strong>ja</strong>makse osas, mis ületab osaluse soetamismaksumust või isikupoolt tehtud sissemakset osaluse omandamisel, ning "Tulumaksuseaduse" § 15 lõike 3 alusel juriidilise isiku likvideerimisel makstav likvideerimis<strong>ja</strong>otisosas, mis ületab osaluse soetamismaksumust või isiku poolt tehtud sissemakset osaluse omandamisel.In table 3.1, the taxpayer shall indicate payments made to the person on the basis of § 15 (2) of the Income Tax Act in the case of a reduction in the sharecapital of an Estonian resident public limited company, private limited company or association, or reduction of the contributions of a general or limitedpartnership, and also in the case of redemption of shares in the amount in which the payments made to a person exceed the acquisition cost of the holdingor the contribution made by a person upon acquisition of the holding (shares, contributions). The taxpayer shall also indicate the amount in which theliquidation proceeds paid to a person upon the liquidation of an Estonian resident legal person on the basis of § 15 (3) of the Income Tax Act exceeds theacquisition cost of the holding or the contribution made by the person upon acquisition of the holding.3. Tabelis 3.2 näidatakse mitteresidendi kasu, mis on saadud "Tulumaksuseaduse" § 15 lõikes 1 nimetatud vara võõrandamisest, kui:In table 3.2, the taxpayer shall indicate gains from the transfer of property as prescribed in § 15 (1) of the Income Tax Act, in the case:1) müüdud või vahetatud kinnisasi asub Eestis võithe sold or exchanged immovable is located in Estonia, or2) registrisse kantav vallasasi oli kuni võõrandamiseni registreeritud Eesti registris võithe movable property subject to entry in a register was in an Estonian register prior to the transfer, or3) müüdud või vahetatud vallasas<strong>ja</strong> omanda<strong>ja</strong> on Eesti riik, kohalik omavalitsusüksus või resident ning vallasasi asus enne müümist võivahetamist Eestis võithe acquirer of the sold or exchanged movable is the Estonian state, a local government or a resident and the movable was located in Estoniaprior to sale or exchange, or4) võõrandatud as<strong>ja</strong>õigus oli seotud Eestis asuva kinnisas<strong>ja</strong> või ehitise kui vallasas<strong>ja</strong>ga võithe transferred real right is related to an immovable or a building as movable, which is located in Estonia, or5) võõrandati vähemalt 10%-list osalust äriühingus, kelle varast võõrandamisele eelneva ma<strong>ja</strong>ndusaasta viimase päeva seisuga koostatudbilansi alusel üle 75% moodustasid Eestis asuvad kinnisas<strong>ja</strong>d või ehitised kui vallasas<strong>ja</strong>d.the transferred holding is a holding of at least 10 per cent in a company of whose property, according to the balance sheet as of the last day ofthe preceding financial year, more than 75 per cent is made up of immovables or buildings as movables, which are located in Estonia.4. Tabeli 3.2 veerus 1 näidatakse vara liigi koodid lähtudes järgmisest loetelust:In column 1 of table 3.2, the taxpayer shall indicate the types of the property from the following:1) kinnisasi ning ehitis või korter kui vallasasi;immovable, structure or apartment as a movable;2) registrisse kantav vallasasi;a movable property subject to entry in a register;3) vallasasi, mida ei kanta registrisse;a movable property not subject to entry in a register;4) kinnisas<strong>ja</strong>ga või ehitise kui vallasas<strong>ja</strong>ga seotud as<strong>ja</strong>õigus;a real right related to an immovable or a building as movable;5) vähemalt 10%-line osalus äriühingus, kelle varast on üle 75% Eestis asuvad kinnisas<strong>ja</strong>d või ehitised kui vallasas<strong>ja</strong>d.a holding in a company of whose property more than 75 per cent is made up of immovables or buildings as movables, which are located inEstonia.5. Kui kinnisas<strong>ja</strong>, ehitist või korterit kui vallasas<strong>ja</strong> kasutati peale maksumaks<strong>ja</strong> elukoha osaliselt ka muul otstarbel (näiteks ettevõtluses, üüriti väl<strong>ja</strong>), siisrakendatakse maksuvabastust proportsionaalselt elukohana <strong>ja</strong> muul otstarbel kasutatavate ruumide pindala suhtega.If an immovable, building or apartment as a movable was partly used for purposes other than the taxpayer's residence (e.g., in business, for lease), the taxexemption is applied according to the proportion of the area of the rooms used as residence and the area of the rooms used for other purposes.6. Kasu vara müügist on müüdud vara soetamismaksumuse <strong>ja</strong> müügihinna vahe. Kasu vara vahetamisest on vahetatava vara soetamismaksumuse ningvahetuse teel vastu saadud vara turuhinna vahe. <strong>Maksu</strong>maks<strong>ja</strong>l on õigus kasust maha arvata vara müügi või vahetamisega otseselt seotuddokumentaalselt tõendatud kulud. Alates 2004. aastast on maksumaks<strong>ja</strong>l õigus vara müügi või vahetamisega otseselt seotud dokumentaalselttõendatud kulud arvesse võtta ka juhul, kui tehingust saadi kahju.Gain from selling of property is the difference between the acquisition cost and the selling price of the property. Gain from exchange of property is thedifference between the acquisition cost and the market price of the property. Taxpayer has a right to deduct from the gain expenses which are directlyrelated to the selling or exchange of the property. As from year 2004, a taxpayer has the right to add certified expenses directly related to the sale orexchange of property to the loss from transfer of property.7. Soetamismaksumus ("Tulumaksuseaduse" § 38) on:According to § 38 of the Income Tax Act, the acquisition cost is deemed to be:1) kõik maksumaks<strong>ja</strong> poolt vara omandamiseks ning selle parendamiseks <strong>ja</strong> täiendamiseks tehtud dokumentaalselt tõendatud kulud,sealhulgas makstud komisjonitasud <strong>ja</strong> lõivud;all certified expenses which a taxpayer makes in order to obtain, improve, or supplement property, including any commissions and fees paid;2) kapitalirendi (liisingu) korras soetatud vara lepingujärgsete tegelikult makstud rendi- või väl<strong>ja</strong>ostumaksete kogusumma ilma intressideta;

3The total amount of contractual lease payments or down payments of property acquired by way of a finance lease, without interest;3) omavalmistatud as<strong>ja</strong> valmistamiseks tehtud dokumentaalselt tõendatud kulude summa, sealhulgas ka eelmistel maksustamisperioodideltehtud kulutused (näiteks poolelioleva ma<strong>ja</strong> ehituskulu).the total amount of certified expenses incurred in manufacturing a self-manufactured object, including the expenses made during the previousperiods of taxation (e.g., the construction costs of an unfinished building).8. Vara müügi või vahetamisega seotud kulud on vara võõrandamisega otseselt seotud dokumentaalselt tõendatud kulutused.The costs related to the sale or exchange of property are the certified expenses directly related to the transfer.9. <strong>Maksu</strong>maks<strong>ja</strong> või tema esinda<strong>ja</strong> on kohustatud <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>i nõudmisel esitama maksu määramiseks va<strong>ja</strong>likke täiendavaid dokumente.Upon request, the taxpayer or the taxpayer's representative is required to provide the Tax and Customs Board with additional documentation necessary fortax assessment.10. Vara müügist saadud tulu kuulub maksustamisele kogu ulatuses, kui varal puudub soetamismaksumus ning vara müük ei ole vastavalt"Tulumaksuseadusele" tulumaksuvaba. Füüsilisele isikule riigi poolt väl<strong>ja</strong> antud, pärandina või abikaasalt, vanemalt või lapselt saaduderastamisväärtpaberite eest soetatud vara soetamismaksumuse arvutamisel võetakse aluseks erastamisväärtpaberite noteeritud keskmine müügihindvara soetamise päeval. Enne erastamisväärtpaberite väärtpaberibörsil noteerimise alustamist soetatud vara soetamismaksumuseks loetakseerastamisväärtpaberite keskmine kohalik müügihind vara soetamise päeval.Income tax is charged on gain from the transfer of property to the full extent, if the property has no acquisition cost and the transfer of property is notexempted from income tax on the bases of the Income Tax Act. The acquisition cost of property acquired for privatization securities issued to a naturalperson by the state or received by succession or from his or her spouse, parent or child is deemed to be the average selling price of the privatizationsecurities as quoted on the stock exchange on the date of acquiring the property. The acquisition cost of property acquired before privatization securitiescame to be quoted on the stock exchange is deemed to be the average local selling price of the privatization securities on the date of acquiring the property.11. Tuludeklaratsioonile kirjutab alla maksukohustuslane või tema esinda<strong>ja</strong>. Esinda<strong>ja</strong> peab <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>i nõudmisel esitama esindust tõendavavolikir<strong>ja</strong>.The income tax return shall be signed by the taxpayer or his or her representative. The representative shall, if required by the Tax and Customs Board,produce a document certifying the right of representation.12. Kinnisas<strong>ja</strong>, ehitise või korteri kui vallasas<strong>ja</strong> võõrandamisel on mitteresident kohustatud esitama tuludeklaratsiooni kuu a<strong>ja</strong> jooksul pärast tehingutoimumist võõrandatud vara asukohajärgsele <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>i kohalikule asutusele. Teiste "Tulumaksuseaduse" § 29 lõigetes 4 <strong>ja</strong> 5 toodud varadevõõrandamisest saadud kasu kohta tuleb tuludeklaratsioon <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>ile esitada hiljemalt järgmise aasta 31.märtsiks.Upon transfer of an immovable, structure or apartment as a movable a non-resident shall submit the income tax return within one month following thetransaction. The income tax return is filed with the local office of the Tax and Customs Board of the location of the transferred property. Concerning gainsfrom transfer of other property prescribed in § 29 (4) and (5) of the Income Tax Act, an income tax return must be filed with the Tax and Customs Board byMarch 31 of the following year at the latest.13. Mitteresident arvutab tuludeklaratsiooni alusel maksmisele kuuluva maksusumma ning tasub selle tuludeklaratsiooni esitamise tähtpäevaks <strong>Maksu</strong>- <strong>ja</strong><strong>Tolliamet</strong>i pangakontole. Mitteresidendile maksuteadet ei väl<strong>ja</strong>stata.A non-resident shall calculate the tax amount payable on the basis of the income tax return and shall pay this amount into the bank account of the Tax andCustoms Board by the due date for submitting the income tax return. A tax notice will not be issued to a non-resident.14. <strong>Maksu</strong> tasumiseks va<strong>ja</strong>liku viitenumbri saamiseks tuleb peale deklaratsiooni esitamist pöörduda <strong>Maksu</strong>- <strong>ja</strong> <strong>Tolliamet</strong>i piirkondliku maksukeskusepoole.In order to obtain the reference number necessary for the payment of income tax, the Regional Tax Centre of the Tax and Customs Board has to becontacted.

4<strong>Vorm</strong>/Form <strong>V1</strong> lisa<strong>Maksu</strong>maks<strong>ja</strong> / TaxpayerEesnimiFirst nameNimiNamePerekonnanimiSurnameIsikukood või selle puudumisel sünniaeg või registrikood residendiriigisID-code or date of birth or registration code in the country of residence3.1kroonides / in EEKAktsiaseltsi aktsiakapitali, osaühingu või ühistu osakapitali, samuti täis- või usaldusühingu sissemaksete vähendamisel, aktsiate, osade või osamaksetetagasiostmisel või juriidilise isiku likvideerimisel saadud tuluIncome derived from a reduction in the share capital of a public limited company, private limited company or association, or reduction of contributions of a general orlimited partnership or income from redemption of shares or income from liquidation proceeds paid to a person upon the liquidation of a resident legal person1. Äriühingu nimiName of the legal person2. RegistrikoodRegistration code3. Tehingukuupäev (päev,kuu, aasta)Date oftransaction (day,month, year)4. Aktsiate võiosade arvNumber ofshares orcontributions5. SoetamismaksumusvõisissemakseAcquisition orcontribution cost6. Väl<strong>ja</strong>maksePayment7. Tulu: veerg 6-veerg 5 0Gain: Column 6-column 5 08. Tasumiselekuuluv tulumaks:veerg 7 x 26/100Income tax payable:column 7 x 26/100TABELI 3.1 LISALEHED / ANNEX TO TABLE 3.1Kokku 3.1Total 3.1<strong>Maksu</strong>maks<strong>ja</strong> allkiriTaxpayer´s signatureKuupäevDate

5<strong>Vorm</strong>/Form <strong>V1</strong> lisa<strong>Maksu</strong>maks<strong>ja</strong> / TaxpayerEesnimiFirst nameNimiNamePerekonnanimiSurnameIsikukood või selle puudumisel sünniaeg või registrikood residendiriigisID-code or date of birth or registration code in the country of residence3.2Kasu Eestis asuva vara võõrandamisest/Gain derived from the transfer of property in Estonia1. Vara liikType of the property2. Võõrandamistehingukuupäev(päev, kuu, aasta)Date of sales transaction(day, month, year)3. SoetamismaksumusAcquisitioncost4. VõõrandamisegaseotudkuludTransfer costs5. Müügi- võituruhindSelling price/market pricekroonides / in EEK6. Kasu: veerg 5 –7. Tasumiselekuuluv tulumaks:veerg 3 - veerg 4 0veerg 6 x 26/100Gain: column 5- Income tax payable:column 3-column 4 0 column 6 x 26/100TABELI 3.2 LISALEHED / ANNEX TO TABLE 3.2Kokku 3.2Total 3.2<strong>Maksu</strong>maks<strong>ja</strong> allkiriTaxpayer´s signatureKuupäevDate