- Page 2 and 3:

Maryland State Department of Educat

- Page 4 and 5:

~ Note ~The following acronyms and

- Page 7:

Table of Contents - AppendicesSUBJE

- Page 10 and 11:

Introductionconcluded that school-b

- Page 13 and 14:

In 1979, the National Council onGov

- Page 15:

(2) Investment Trust Fund - A fund

- Page 18 and 19:

Accounting & Reporting Requirements

- Page 21 and 22:

The structure of the Maryland State

- Page 23 and 24:

Coding & Reporting StructureCODING

- Page 25 and 26:

Coding & Reporting StructureRevenue

- Page 27 and 28:

Coding & Reporting StructureRevenue

- Page 29 and 30:

Coding & Reporting StructureExpendi

- Page 31 and 32:

Coding & Reporting StructureObject-

- Page 33 and 34:

Coding & Reporting StructureThis pa

- Page 35 and 36:

Coding & Reporting StructureCurrent

- Page 37 and 38:

Coding & Reporting StructureCurrent

- Page 39 and 40:

Coding & Reporting StructureObject-

- Page 41 and 42:

Coding & Reporting StructureClassIn

- Page 43 and 44:

Coding & Reporting StructureCurrent

- Page 45 and 46:

Coding & Reporting StructureCapital

- Page 47:

Coding & Reporting StructureCurrent

- Page 51 and 52:

The Assets, Liabilities, and Fund B

- Page 53 and 54:

LEAs receive funding from many sour

- Page 55 and 56:

Definitions: Revenue & Other Source

- Page 57:

Definitions: Revenue & Other Source

- Page 60 and 61:

Definitions: Expenditure AcctExecut

- Page 62 and 63:

Definitions: Expenditure Acctcommun

- Page 64 and 65: Definitions: Expenditure AcctCatego

- Page 66 and 67: Definitions: Expenditure AcctExampl

- Page 68 and 69: Definitions: Expenditure Acctcreati

- Page 70 and 71: Definitions: Expenditure Acct203122

- Page 72 and 73: Definitions: Expenditure Acctbetwee

- Page 74 and 75: Definitions: Expenditure Acctshall

- Page 77 and 78: The Objects classification is used

- Page 79 and 80: Object/Subobject Dimension322 Libra

- Page 81 and 82: Object/Subobject Dimension552 Build

- Page 83 and 84: BackgroundThe Maryland Public Chart

- Page 85 and 86: Maryland’s State Superintendent o

- Page 87: Bi-Annual ReportBi-Annual Reporting

- Page 90 and 91: Maintenance of Effort78

- Page 93 and 94: Non-RecurringCost Waiver RequestIn

- Page 95 and 96: SAMPLE83Exhibit B: Non-Recurring Co

- Page 97 and 98: Exhibit B: Non-Recurring Cost Waive

- Page 99: Exhibit B: Non-Recurring Cost Waive

- Page 103 and 104: Appendix AInstructions for Completi

- Page 105 and 106: Appendix AThe Annual Financial Repo

- Page 107 and 108: Appendix AEncumbrances. They are ap

- Page 109 and 110: Appendix AFiling the Consolidated R

- Page 111 and 112: Appendix ADecember 31, after the cl

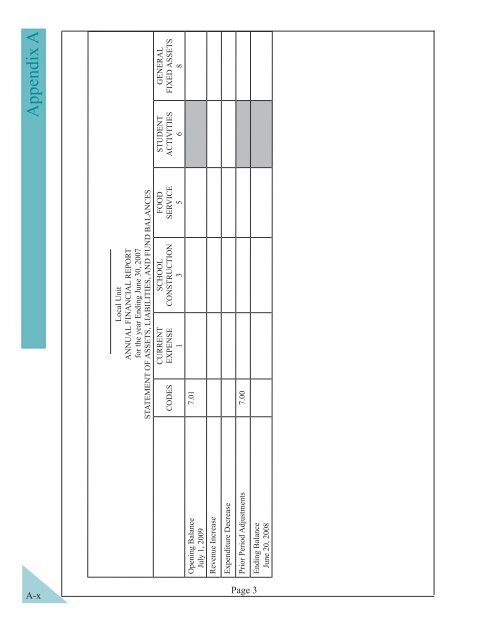

- Page 113: Appendix AGENERALFIXED ASSETS8STUDE

- Page 119 and 120: Appendix BSection 5-101 of the Educ

- Page 121 and 122: Appendix B(Local Unit)ANNUAL BUDGET

- Page 123 and 124: Appendix BCategoryANNUAL BUDGET____

- Page 125 and 126: Appendix BPOSITION TYPESuperintende

- Page 127 and 128: Appendix BANNUAL BUDGETLocal Unit20

- Page 129: Appendix CThe Annual Financial Repo

- Page 132 and 133: Appendix Cc. provide standard repor

- Page 134 and 135: Appendix CThe LEA user must use the

- Page 136 and 137: Appendix CPayment GenerationThe Gra

- Page 138 and 139: Appendix C2. Grant Included in Indi

- Page 141: Supplies and EquipmentAppendix D

- Page 144 and 145: Appendix D• it retains its origin

- Page 147 and 148: Appendix EFund (revenue) source cod

- Page 149 and 150: Appendix EMANDATORY GRANT PROVISION

- Page 151: Cost PrinciplesandState-Funded Gran

- Page 154 and 155: Appendix FRestricted Award - State

- Page 156 and 157: Appendix FIndirect Costs are those:

- Page 158 and 159: Appendix F(3) When a grantee uses t

- Page 160 and 161: Appendix F(4) are allowable under t

- Page 162 and 163: Appendix F(a) the capitalization le

- Page 164 and 165:

Appendix F(4) Accounting records, a

- Page 166 and 167:

Appendix Fb. Retainer fees supporte

- Page 170:

Financial Rep orting Manualf orMary