You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>THINK</strong> <strong>ACT</strong> – September 2011 – Size Matters<br />

<strong>THINK</strong><br />

<strong>ACT</strong><br />

Magazine for Decision Makers N o 17<br />

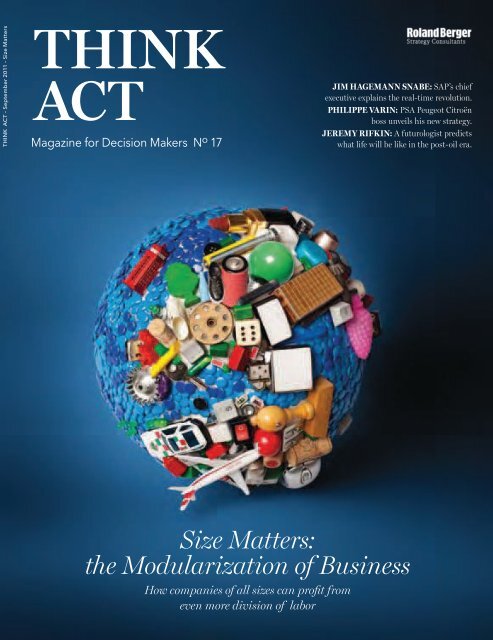

Size Matters:<br />

the Modularization of Business<br />

How companies of all sizes can profit from<br />

even more division of labor<br />

RUBRIK HIER<br />

JIM HAGEMANN SNABE: SAP’s chief<br />

executive explains the real-time revolution.<br />

PHILIPPE VARIN: PSA Peugeot Citroën<br />

boss unveils his new strategy.<br />

JEREMY RIFKIN: A futurologist predicts<br />

what life will be like in the post-oil era.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 1

PODCASTS, VIDEOS & MORE<br />

WWW.<strong>THINK</strong>-<strong>ACT</strong>.COM<br />

Password: rolandberger

Photos: Titel: Sarah Illenberger, Inhalt: Frank Bauer, Laif, SAP<br />

4 One-on-one with Wittig<br />

the founder of the dm drugstore<br />

chain, Götz Werner<br />

<strong>THINK</strong><br />

8 Brief Think<br />

10 The nudge theory<br />

Little pushes can bring big<br />

changes in people’s behavior<br />

14 Follow the money<br />

How remittances affect<br />

the global economy<br />

16 Real real-time<br />

How in-memory computing<br />

can add value<br />

20 Do bailouts work?<br />

<strong>THINK</strong> <strong>ACT</strong> columnist Nils<br />

aus dem Moore discusses whether<br />

recovery programs are a good thing<br />

REPORT<br />

23 Size matters<br />

The modular economy is creating<br />

opportunities for large and small<br />

businesses alike<br />

34 Believe in growth!<br />

Roland Berger Strategy<br />

Consultants chairman Burkhard<br />

Schwenker says there can be no<br />

prosperity without growth<br />

36 The future of work<br />

Alexi Marmot on the fl exible,<br />

mobile workplace<br />

CONTENTS<br />

4<br />

Control is good,<br />

trust is better:<br />

Götz Werner,<br />

founder of the<br />

dm drugstore<br />

chain, explains<br />

the importance<br />

of a corporate<br />

culture based<br />

on values<br />

The power of pricing,<br />

and international alliances:<br />

PSA Peugeot Citroën CEO<br />

Philippe Varin talks about the<br />

future of the car industry<br />

Real-time analysis:<br />

SAP chief executive<br />

Jim Hagemann<br />

Snabe tells us<br />

why in-memory<br />

computing will<br />

change the world<br />

40 The smaller, the better<br />

Why Virgin prefers underdog<br />

status to market leadership<br />

<strong>ACT</strong><br />

43 Brief Act<br />

46 Young Global Leaders‘<br />

Task Forces<br />

Why protecting the oceans is<br />

a good investment<br />

52 Break the rule!<br />

British company WorkSnug has<br />

banned fl ying on business<br />

54 Borussia Dortmund<br />

In 2005 they were almost<br />

bankrupt; now they’re Germany’s<br />

football league champions. How<br />

the club achieved a turnaround<br />

on and off the pitch.<br />

58 PSA Peugeot Citroën<br />

We talk to Philippe Varin,<br />

CEO of Europe’s second biggest<br />

car maker<br />

63 Banking regulation<br />

How the new defi nition of<br />

“systemically important fi nancial<br />

institutions” is affecting the<br />

banking world<br />

66 Looking forward<br />

Futurologist Jeremy Rifkin:<br />

what’s here to stay, what’s<br />

coming soon<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 3<br />

58<br />

16

One-on-one with Wittig<br />

The Detail<br />

of Retail<br />

The dm drugstore chain is a fast-growing,<br />

profitable company, with a culture based on<br />

trust, not control. dm Founder Götz Werner<br />

and Roland Berger CEO Martin Wittig talk to<br />

Thomas Ramge about success, and what other<br />

businesses can learn from dm<br />

Götz Werner, the theme of this issue<br />

of <strong>THINK</strong> <strong>ACT</strong> is “size matters”.<br />

You created a very big company<br />

made up of many small units.<br />

What’s the relationship between big<br />

and small in your business?<br />

Götz Werner: It depends on which<br />

way you look at it. Of course dm is a<br />

big company, with sales of more than<br />

EUR 5 bn, but that’s an abstraction.<br />

The reality of dm is a 550 square-<br />

meter drugstore with 25 employees<br />

and 1.500 to 2.000 customers per<br />

day, so we mustn’t lose sight of the<br />

individual branches, and if we do,<br />

we’re in trouble. As soon as we start<br />

thinking we’re a big company, we start<br />

making mistakes. It’s a fantasy image<br />

that doesn’t exist in reality. Retail is<br />

all about detail, and retailers that lose<br />

sight of this are doomed to fail.<br />

You once said: “We get hardly any<br />

economies of scale in our purchasing.”<br />

If retail is about detail, why<br />

do we need store chains at all?<br />

Mom-and-pop corner stores used<br />

to be very good at retailing, but<br />

they’ve disappeared.<br />

Werner: The real synergy in retail<br />

chains is that the individual branches<br />

don’t just sit there stewing in their<br />

own juice; they learn from the other<br />

branches. Mom-and-pop stores are<br />

often run with a great deal of passion<br />

at first, but this wears off as time<br />

goes by. Each dm store can benefit<br />

from the others’ ideas, provided that<br />

everyone is always clear regarding the<br />

company’s objectives.<br />

Wittig: That’s similar to our business;<br />

our economies of scale are in knowledge,<br />

not in buying things more<br />

cheaply than our competitors. With<br />

our flat hierarchy, we can share one<br />

specialist’s knowledge with the entire<br />

4 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

world. There’s no point having detailed<br />

expert knowledge unless it can be<br />

shared with everyone within a very<br />

large organization.<br />

So what would you say is the perfect<br />

size? Is it possible to lay down hard<br />

and fast rules?<br />

Götz Werner (right):<br />

“If you’re successful, you<br />

gain a customer base,<br />

and then you grow.”<br />

Werner: You always strive for the<br />

optimal, and everything you do<br />

is sub-optimal. Once you realize<br />

there’s a difference between the two,<br />

you move on to a new stage in your<br />

development, so growth comes from<br />

outside, not from inside. If you’re<br />

successful, you gain a customer base,<br />

and then you grow.<br />

That’s the logic of growth. But why<br />

can’t you say: “We have a very<br />

profitable company, let’s stay<br />

that way”?<br />

Wittig: I’m a strong advocate of growth,<br />

both for businesses and economies,<br />

because it creates more opportunities<br />

for more people. If you try to stop<br />

China from growing, you’re excluding<br />

a large proportion of the world’s<br />

population from prosperity. We have<br />

to live with that and find ways of<br />

dealing with the consequences of<br />

growth. But I think we should always<br />

have a growth component to our<br />

philosophy, because if you don’t grow,<br />

you stand still. Growth is the only<br />

way of coming up with new ideas and<br />

trying out new concepts.<br />

Werner: I prefer to say development<br />

rather than growth. Growth is pretty<br />

superficial, it’s about numbers, but if<br />

you have a company culture that says<br />

people must develop themselves, that’s<br />

clearly about quality. Quantitative<br />

growth is the logical consequence of<br />

development.<br />

Wittig: The automobile industry is<br />

a good example of that. In terms of<br />

numbers, western markets are largely<br />

saturated, and electric cars have<br />

relatively low development potential<br />

compared to the industry as a whole.<br />

But in quality terms, it’s a completely<br />

different picture; there’s still a lot of<br />

potential in personalizing products to<br />

individuals’ needs.<br />

Werner: We have 1.2 million customers,<br />

and we could always provide a better<br />

service to them all.<br />

In terms of customer focus, how<br />

important is it to give branches a<br />

lot of autonomy, and are there instances<br />

where a good old-fashioned<br />

hierarchy works better, even if it’s<br />

less socially acceptable?<br />

Wittig: Nearly all industries and<br />

services have completely different<br />

organizational models, and centralized<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 5

ONE-ON-ONE WITH WITTIG<br />

and decentralized models can work<br />

equally well. If you look at a company’s<br />

maturity curve, you can see that<br />

expanding companies tend to be<br />

managed on a decentralized basis.<br />

That’s the case with the automobile<br />

industry when it’s moving into new<br />

markets, and with logistics and other<br />

service providers. These are usually<br />

developed in a decentralized way by<br />

local companies.<br />

As a company continues to develop,<br />

there’s a tendency toward centralization,<br />

with specific areas of the business being<br />

combined in accordance with central<br />

guidelines. Nearly all companies still<br />

have hierarchies, and chaos is rarely<br />

successful as an organizational principle.<br />

Of course there are very different<br />

degrees of guidelines, and you have<br />

to decide what’s going to work on a<br />

case-by-case basis, which has a lot to<br />

do with the company’s history and<br />

culture. There’s one big Chinese<br />

retailer I know that’s organized in an<br />

almost military fashion; the employees<br />

have to attend a morning videoconference<br />

and roll call. It sounds weird<br />

to us, but it works for them.<br />

Werner: You have to see management<br />

in its cultural context. When I was<br />

young, there was one successful<br />

entrepreneur I knew who had a fax<br />

machine in every branch, and he<br />

used to send them instructions every<br />

morning. Times and people change,<br />

and so must methods.<br />

I think the most successful people<br />

are those who have their finger on<br />

the pulse of the time. Of course you<br />

can be successful with old-fashioned<br />

methods, but then the question is:<br />

are you succeeding because of, or in<br />

spite of them?<br />

If a company like dm gives its<br />

branches so much freedom doesn’t<br />

that make it harder to implement<br />

difficult strategic change from the<br />

center?<br />

Werner: That’s a good question, and<br />

it’s one we’ve discussed many times in<br />

Götz Werner<br />

Biography<br />

Götz Werner<br />

was born in<br />

1944, and<br />

opened<br />

his first<br />

drugstore in<br />

Karlsruhe in 1973. Today, his<br />

company, dm-drogerie markt,<br />

has around 2,500 branches<br />

and employs nearly 40,000<br />

people across Europe. Werner<br />

headed the entrepreneurship<br />

institute at the Karlsruher<br />

Institut für Technologie from<br />

October 2003 to September<br />

2010. He is a strong believer in<br />

corporate social-responsibility,<br />

and has for many years publicly<br />

campaigned for a basic<br />

living wage.<br />

our history. Our culture is one of very<br />

slow change. Change is a very difficult<br />

process, you can only implement it in<br />

small steps, and having a hierarchy<br />

doesn’t help. You must always be<br />

willing to question paradigms. For<br />

example, we don’t just want customers<br />

to be loyal, we want a close, long-term<br />

relationship with them, and that<br />

requires a completely new form of<br />

marketing. So do you put pressure<br />

on them, or do you make yourself<br />

attractive so that you take them with<br />

you? In my experience, taking them<br />

with you works better if you’re going<br />

to develop sustainably.<br />

So how do you get them onside?<br />

Wittig: In our own business, we do<br />

it using trust. To us, marketing is<br />

about building relationships of trust<br />

with decision makers, and the best<br />

advertising is word of mouth. If<br />

you’re in a competitive situation,<br />

a lot of your products and services<br />

6 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

“People who apply to us often<br />

ask how they can use the<br />

company to do good. That just<br />

wasn’t an issue ten years ago.”<br />

Martin Wittig<br />

are similar to other companies’. Of<br />

course, one good example of getting<br />

customers onside is Apple; they<br />

don’t push their products in their<br />

stores, but people are still happy to<br />

wait for them. They get customers<br />

onside by creating needs that they<br />

want to satisfy.<br />

But a lot of business models are still<br />

based on scaling and push. How<br />

do you move away from just massproducing<br />

things towards a more<br />

customer-centered approach?<br />

Werner: We’re obviously a massmarket<br />

provider, but if you don’t<br />

want to push all the time, you need<br />

stable performance. It’s a question of<br />

attitude. Do you want rapid success,<br />

or long-term relationships with your<br />

customers? In the old days, we had a<br />

slogan, “Big brands, small prices,” but<br />

18 years ago, we changed it to “I’m an<br />

individual here, this is where I shop.”<br />

This was a major turning point. Our<br />

marketing strategy begins: “We want<br />

regular customers who make a point<br />

of shopping with us because they’re<br />

convinced they’ve done the right<br />

thing.” Often, the first mistake is<br />

talking about customers when you<br />

should be talking about people.<br />

That’s a people-centered approach,<br />

but is it suitable for a company that’s<br />

very growth – and profit – oriented?<br />

Werner: The better you know people,<br />

the better you can respond to their<br />

needs. If you can gain a better understanding<br />

of what drives people, you<br />

can be a better manager, know your<br />

customers and suppliers better, and<br />

predict the future more effectively.<br />

Wittig: I think having a transparent<br />

value system is an important part of<br />

managing a company, particularly<br />

when it’s about the long-term survival<br />

of the business.<br />

You don’t have a bonus system for<br />

dm employees. Why not?<br />

ONE-ON-ONE WITH WITTIG<br />

Werner: We do things because they<br />

make sense, not because I’ve promised<br />

my wife a Christmas bonus.<br />

Wittig: I don’t think bonuses and the<br />

whole pull idea are a contradiction<br />

in terms. Bonuses are a pull for employees,<br />

not a push. If they don’t get<br />

a bonus, I’m not punishing them, I’m<br />

giving them the chance to earn one.<br />

Werner: I’m with you on that. I<br />

don’t believe in extrinsic motivation;<br />

management must create a situation<br />

in which employees are intrinsically<br />

motivated – I’d even go so far as<br />

to say that bonus systems penalize<br />

workers. Employees need an income<br />

so they can live, and they need their<br />

work so they can grow.<br />

You’re also trying to remove the<br />

link between work and income, and<br />

you’ve been publicly campaigning<br />

for a basic living wage for years.<br />

Why, as an entrepreneur, are you<br />

so involved in social issues?<br />

Werner: Because entrepreneurs<br />

need to see the forest for the trees.<br />

If a company’s sole raison d’être is<br />

making society better, it must have<br />

an interest in how society develops.<br />

Social involvement is one of the most<br />

important roles of an entrepreneur,<br />

particularly when you get older. All<br />

entrepreneurs should aim to create<br />

scope for people within the business<br />

to become active outside of it.<br />

Wittig: People who apply to us often<br />

ask how they can use the company to<br />

do good, for example, by volunteering<br />

and taking sabbaticals. That just<br />

wasn’t an issue ten years ago, but<br />

today it’s a pull, and as a company,<br />

we have to be socially involved if<br />

we’re going to attract young people.<br />

Our charitable trust is an example<br />

of this; we spend around 2% of<br />

our sales on these forms of social<br />

involvement, and I think this is a<br />

wonderful trend.<br />

This interview was conducted by Thomas Ramge<br />

Photos Frank Bauer<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 7

��������������<br />

�����������<br />

�����<br />

�����<br />

RUBRIK HIER<br />

BRIEF<br />

<strong>THINK</strong><br />

�������������<br />

��������������<br />

�����<br />

�����������������<br />

������������<br />

������<br />

��������������������<br />

������������<br />

���������������<br />

������������<br />

������<br />

�����<br />

����������������<br />

�������������<br />

�����<br />

����<br />

���������������<br />

�����<br />

����������<br />

�����<br />

�������<br />

����������<br />

�����<br />

����������������<br />

������������<br />

�����<br />

The world’s<br />

knowledge is<br />

in the northern<br />

hemisphere<br />

The world’s fi ve<br />

top-selling daily<br />

newspapers are<br />

all Japanese.<br />

WHERE IS THE WORLD’S KNOWLEDGE<br />

concentrated? That’s the question posed<br />

in The Geography of World Knowledge,<br />

published by two think-tanks, Convoco and<br />

the Oxford Internet Institute. In the midst of<br />

a new media revolution, the publication maps<br />

things like worldwide Internet use, newspaper<br />

readership and centers of academic knowledge,<br />

and even includes a revealing breakdown of<br />

the geographic distribution of geocoded photographs<br />

uploaded to Flickr. In almost every case,<br />

the knowledge is concentrated in Europe and<br />

North America – which are also the regions<br />

where the largest number of Wikipedia<br />

biographies are written.<br />

+www.oii.ox.ac.uk<br />

Ideas for crisis-ridden<br />

companies<br />

NO TWO BUSINESS CRISES ARE THE SAME. Sometimes you just need<br />

to tweak your strategy; sometimes it’s time to call in the receivers.<br />

In nearly all cases, turning a company around demands a holistic<br />

approach that carefully considers all recovery options. Drawing up a<br />

restructuring plan that identifi es the causes and possible solutions is<br />

just as important as complying with the relevant legal requirements.<br />

This review by Roland Berger Strategy Consultants’ Bernd<br />

Brunke, Sascha Haghani and Thomas Knecht, entitled “Restructuring<br />

and Re-launching Crisis-Ridden Companies,” is a sound, up-todate<br />

and comprehensive guide on the subject. It takes into account<br />

current statute and case law, and discusses the latest approaches to<br />

various aspects of restructuring and insolvency.<br />

The review is aimed at company managers, bankers, other investors,<br />

and students and teachers of business studies and law.<br />

“DRAWING UP A<br />

RESTRUCTURING PLAN<br />

THAT IDENTIFIES THE<br />

CAUSES AND POSSIBLE<br />

SOLUTIONS IS JUST AS<br />

IMPORTANT AS COMPLYING<br />

WITH THE RELEVANT<br />

LEGAL REQUIREMENTS.”<br />

“Restructuring and Re-launching Crisis-Ridden Companies”<br />

8 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

Photos: DPA (2)<br />

Project 2012<br />

Global Wind of Change?<br />

2012 WILL BE A BUMPER YEAR for elections worldwide.<br />

Voters in the world’s two biggest economies, the<br />

United States and China, will go to the polls – though<br />

one election will be rather more democratic than the<br />

other. Russia and France will elect new presidents, and<br />

India, Spain and Mexico will also be voting.<br />

If the balance of power shifts in any of these key<br />

nations, it will happen at a diffi cult time. With issues<br />

like US debt and the euro crisis high on the agenda,<br />

elections have the potential to bring political change.<br />

Roland Berger has therefore set up Project 2012, a<br />

cooperative consultancy platform for companies and<br />

politicians, providing support to top decision makers<br />

whose agendas could be affected by the poll results<br />

over the coming year.<br />

The project will develop scenarios allowing businesses<br />

to prepare for a variety of possible outcomes.<br />

Roland Berger is working in close partnership with<br />

universities and think-tanks around the world, including<br />

the Yale World Fellows Program and HEC Paris,<br />

and will present the results of the project as a series of<br />

strategic proposals during the coming year. There is<br />

also a wiki for anyone wishing to be involved in this<br />

project. If you are interested, please register at<br />

+www.theproject2012.org<br />

Nicolas Sarkozy<br />

Dmitri Medwedew<br />

Russia<br />

11 March 2012<br />

France<br />

5 May 2012<br />

China<br />

October 2012<br />

USA<br />

6 November 2012<br />

Hu Jintao<br />

It’s still not clear who will be contending in<br />

next year’s presidential elections. Incumbent<br />

Dmitry Medvedev will probably<br />

stand for a second term, but the possibility<br />

of a job swap with Prime Minister<br />

Vladimir Putin is still under discussion.<br />

France is likely to shift rightwards, with<br />

President Nicolas Sarkozy<br />

standing for reelection. Polls indicate<br />

that Marine Le Pen, the right-wing Front<br />

National candidate, will attract a signifi -<br />

cant share of the vote.<br />

President Hu Jintao and Prime Minister<br />

Wen Jiabao are expected to pass on<br />

their respective batons at the 18 th<br />

national party congress in October. Their<br />

potential replacements are Xi Jinping<br />

and Li Keqiang.<br />

President Barack Obama wants<br />

a second term in the White House.<br />

Among the potential Republican challengers<br />

are Michele Bachmann and<br />

Rick Perry.<br />

Barack Obama<br />

Up for re-election:<br />

Four<br />

global<br />

elections<br />

leaders<br />

that<br />

who<br />

could<br />

could<br />

change<br />

be out of<br />

the<br />

a job.<br />

world economy

<strong>THINK</strong>: NUDGE<br />

Sometimes you need<br />

a little push<br />

Two leading US academics say that small pushes in the right direction<br />

can overcome people’s natural inertia and bring about large-scale<br />

social change; they call this effect nudge theory. Barack Obama is a big<br />

advocate of nudge theory, and it is catching on in companies<br />

IT WAS A SIMPLE yet groundbreaking<br />

experiment. Three hundred households<br />

in San Marcos, California were<br />

divided into two groups. Half were sent<br />

normal electricity bills and the other<br />

half had a smiley face on their bills if<br />

their consumption was below average,<br />

and a frowning face if their usage was<br />

higher than average.<br />

The results could not have been more conclusive:<br />

within the group with faces on their<br />

bills, high users reduced their electricity consumption,<br />

and low users consumed even less<br />

than before.<br />

The difference was a little yellow circle on<br />

a piece of paper, but it had a big effect. US<br />

academics Richard Thaler and Cass Sunstein<br />

By Anne Hansen Illustration Lutz Widmaier<br />

cite the smiley experiment as a simple example<br />

of their theory that people can be gently encouraged<br />

to behave in socially desirable ways.<br />

Likewise, even small incentives can improve<br />

employees’ productivity. The two researchers call<br />

it nudge theory, quietly shepherding people in<br />

what, to the nudger at least, is the right direction.<br />

Why should society need a nudge in the first<br />

place? Thaler and Sunstein question one of the<br />

major assumptions of neoclassical economic<br />

theory, homo economicus, which is the idea that<br />

humans act in an enlightened and rational way<br />

to maximize their wellbeing, with emotions<br />

playing no part in their behavior. This construct,<br />

say the two scientists, is like Mr. Spock<br />

in Star Trek. This person would have the brain<br />

of Albert Einstein, the data storage capacity of a<br />

10 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

<strong>THINK</strong>: NUDGE<br />

“We are all Homer Simpson, but little<br />

things, like other people interfering<br />

ever so slightly in our lives, can help to<br />

push us along the right path”<br />

supercomputer, and the patience of Mahatma Gandhi – which<br />

is all very well, but bears no relation to reality.<br />

Real people are more like Homer Simpson. They smoke even<br />

though they know it’s bad for them, and they eat junk food even<br />

though it makes them fat. They buy unsuitable insurance policies<br />

and fail to save for their old age. There are lots of words you<br />

could use to describe humans, but rational isn’t one of them.<br />

This is the central thesis of behavioral economics, which<br />

disagrees with the neoclassical model and asserts that emotion<br />

is an important factor in market behavior. It asserts that<br />

people make decisions on the basis of gut feelings rather than<br />

careful analysis of all the available options.<br />

Also, they’re lazy. People could save money by switching to<br />

another electricity provider, but they can’t be bothered. They<br />

could personalize their cell phones, but they stick with the<br />

factory settings for years on end because reading the instruction<br />

manual is too much trouble. Sunstein freely admits that<br />

he’s no exception; for decades, he’s received newspapers he<br />

no longer wants, simply because he hasn’t gotten around to<br />

canceling his subscription.<br />

Comparing people to Homer Simpson may not be the<br />

most positive view of humanity, but Thaler and Sunstein are<br />

optimists. Little things, like other people interfering ever so<br />

slightly in our lives, can help to push us along the right path.<br />

Nudge theory isn’t just about helping Californians to save<br />

energy, it has many applications. For instance, if employees<br />

smell cleaning products on the tables in common or break<br />

areas, they will keep these areas cleaner. If you announce (as<br />

the Internal Revenue Service did in Minnesota) that 90% of<br />

people have paid their taxes in full and on time, the other 10%<br />

are more likely to pay up as well. The 10% were procrastinating<br />

because they assumed everyone else was.<br />

Libertarian paternalism: it’s not for everyone<br />

So far, so good – but nudging can also be an intrusion into<br />

someone’s personal life. In Austria, people have to opt out of<br />

organ donation by specifically stating that they do not want<br />

their organs removed when they die. Other countries follow an<br />

opt-in system, in which you carry a card stating that you wish<br />

to donate your organs. The opt-out method is problematic from<br />

an individual moral perspective, but it significantly increases<br />

the number of donor organs.<br />

Nudge theory follows the principles of libertarian paternalism.<br />

People must be free to make their own decisions – that’s<br />

the libertarian bit – but it’s also OK to influence their<br />

behavior in a paternalistic way. Freedom and paternalism<br />

are not contradictory terms. Displaying fruit at eye level<br />

in a cafeteria to encourage people to eat better is a nudge.<br />

Removing burgers from the menu, say the theorists, is<br />

unacceptable interference. Carrots are a good thing (to<br />

continue the healthy eating theme), but sticks are bad. It all<br />

sounds pretty simple, but is life really this black and white?<br />

12 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

To critics, nudging often crosses into<br />

the realm of manipulation. The nudgers say<br />

they’re acting in the public interest and trying<br />

to make the world a better place, but do they<br />

really know what individuals want? Driving<br />

to work is not very good for the environment,<br />

but it’s considerably more comfortable than a<br />

sweaty, crowded subway. Cigarettes will kill<br />

you in the long run, but they’ll give you a buzz<br />

for five minutes. Shouldn’t people be able to<br />

achieve their own balance between short and<br />

long-term happiness? Could a well-intentioned<br />

nudge overstep the boundaries; could someone<br />

end up getting hurt?<br />

In spite of the criticism, libertarian paternalism<br />

is the flavor of the month. Richard Thaler,<br />

who lectures at Chicago University, is an advisor<br />

to Barack Obama’s economics team. Cass<br />

Sunstein, one of the country’s most high-profile<br />

lawyers, is Head of the Office of Information<br />

and Regulatory Affairs at the White House.<br />

The Democrats have jumped enthusiastically<br />

onto the nudge-theory bandwagon because<br />

it provides a theoretical justification for state<br />

intervention. In a positive way that is, like a<br />

smiley on your electricity bill.<br />

<strong>ACT</strong><br />

<strong>THINK</strong>: NUDGE<br />

Make it easy! That’s the mantra of nudge theorist and<br />

Obama adviser Richard Thaler, who admits that even<br />

he needs motivation sometimes.<br />

Mr. Thaler, why do you love nudging other people?<br />

Because it’s fun (laughs). No, mainly because it helps<br />

people. In some situations you need help making a<br />

decision – and that’s what we call a nudge.<br />

What kind of nudges are there?<br />

There are many possibilities. But all nudges have one<br />

characteristic in common: we want things to be as easy as possible for<br />

everyone. If you want people to eat healthier food, then the nudge is<br />

quite simple: place the healthy food more prominently in the cafeteria. If<br />

you want people to exercise, make the stairwell more inviting. There was a<br />

great experiment done about this in Stockholm. Each step made a sound<br />

once you stepped on it. The result: people took the stairs instead of the<br />

elevator which was right next to it.<br />

Is it possible to give employees a nudge to advance their motivation?<br />

Absolutely! Many businesses still think that money is the best way to<br />

motivate employees. Motivation and nudging are in some ways the same<br />

thing. What behavioral economics brings to the table is a longer list of<br />

methods one can use to motivate people… Sometimes people will work<br />

harder to win a nice holiday trip than an amount of money of equivalent<br />

value. Even adults sometimes behave like kids and have a playful instinct.<br />

Defaults play a major role in your theory, can you explain this?<br />

By nature people are lazy. That’s why they profit from a default. Actually,<br />

lazy may not be the right word. We are also busy, distracted, impatient,<br />

and sometimes confused. All these and other factors contribute to the<br />

power of the default option. If you want employees to take out a pension<br />

plan, make it so that they automatically have one and that they have to<br />

actually sign out if they no longer want it… Going back to my mantra:<br />

Make it easy.<br />

Are there any nudges you use in your personal life?<br />

Of course, we all do. As a young professor I learned that an excellent way<br />

to prevent procrastination on a project was to commit to giving a presentation<br />

of the paper at a future conference. I am still using the same tricks.<br />

I recently signed a book contract to write another book. The publisher will<br />

soon start asking about my progress, so I better get back to work.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 13

The top ten countries from which migrants remit money (in USD bn)<br />

RUBRIK HIER<br />

-8.1 -9.9 -10.6 -12.6 -13 -15.9 -18.6 -19.6 -26 -48.3<br />

INDIA<br />

CHINA<br />

SPAIN<br />

LUXEMBOURG<br />

KUWAIT<br />

ITALY<br />

NETHERLANDS<br />

GERMANY<br />

SWITZERLAND<br />

RUSSIA<br />

Follow the money:<br />

SAUDI ARABIA<br />

Rich relatives<br />

Migrants feed many families in their home countries, and play<br />

a major part in economic development. Many poor countries earn<br />

more from remittances than from aid and foreign investment<br />

PHILIPPINES<br />

MEXICO<br />

FRANCE<br />

SPAIN<br />

BELGIUM<br />

BANGLADESH<br />

GERMANY<br />

NIGERIA<br />

14 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011<br />

USA

+55 +51 +22.6 +21.3 +15.9 +11.6 +11.1 +10.4 +10.2 +10<br />

Remittance economies<br />

The top ten countries to which migrants send money (in USD bn)<br />

Improved working conditions<br />

Globalization<br />

86.5 71.6 70.0<br />

States with the<br />

highest proportions<br />

of immigrants,<br />

2010<br />

QATAR MONACO UTD. ARAB<br />

EMIRATES<br />

28.0 25.0<br />

35.0<br />

States where remittances<br />

account for the highest<br />

proportion of GDP,<br />

2009<br />

The problems often begin with the<br />

recruitment process: agencies in the<br />

workers’ home countries charge<br />

commissions. The cost of fl ights, visas<br />

and medical tests must also be taken<br />

into account. Saudi Arabia and Indonesia<br />

have taken steps to improve the working<br />

conditions of Indonesian workers, and<br />

there are also changes afoot in Abu<br />

Dhabi, which has set up an independent<br />

employment regulatory body.<br />

The boom in Saudi Arabia and the<br />

United Arab Emirates has attracted<br />

hundreds of thousands of guestworkers<br />

from Southeast Asia. According to Human<br />

Rights Watch, around 600,000 migrants<br />

from that region work in the UAE alone,<br />

300,000 of them in Dubai. By far the<br />

majority work in construction and<br />

unskilled jobs, and both groups often<br />

suffer poor pay and living conditions.<br />

TAJIKISTAN TONGA LESOTHO<br />

Immigrants and emigrants<br />

in these countries (million)<br />

RUBRIK HIER<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 15<br />

+10.8<br />

+6.9<br />

+6.7<br />

+5.4<br />

Immigrants<br />

BELGIUM SPAIN NIGERIA<br />

BANGLADESH<br />

GERMANY<br />

FRANCE<br />

PHILIPPINES<br />

MEXICO<br />

CHINA<br />

INDIA<br />

Emigrants<br />

-5.4<br />

-4.3<br />

-8.3<br />

-11.9<br />

-11.4<br />

Sfd 2009 / 2010 Source: World Bank, Illustration: Jörg Block

<strong>THINK</strong>: IN-MEMORY-COMPUTING<br />

Power to<br />

the Processors<br />

SAP claims to have found something as big as client-server architecture<br />

was in the 1990s – in-memory computing. Never heard of it? You will soon.<br />

We talk to SAP’s CEO Jim Hagemann Snabe about the next big thing in<br />

business intelligence<br />

Jim Hagemann Snabe, tell us about<br />

your killer app. Can you give us an<br />

example that demonstrates the full<br />

potential of in-memory technology?<br />

Take the financial crisis. The lack of<br />

real-time risk measurement by banks,<br />

and the failure to track its causes,<br />

made the system, as a whole, too<br />

risky and eventually it broke down.<br />

Traditional risk management systems<br />

need to evaluate vast amounts of<br />

data, but much of this is only collected<br />

at night and then analyzed in the<br />

morning.<br />

What if you could do this in real<br />

time? What if you could do this every<br />

time a transaction happened? This<br />

was virtually impossible with previous<br />

technology, since you needed to read<br />

millions of items of data to aggregate<br />

the total risk of a bank. Today, inmemory<br />

computing allows you to<br />

complete this analysis in one second.<br />

Does that mean that in-memory<br />

computing could have prevented<br />

the financial crisis?<br />

We can’t prove this, of course, but I’m<br />

convinced that it would have helped<br />

us find solutions earlier.<br />

Impressive. But in-memory computing<br />

is not just for banking, correct?<br />

To put a technological trend into a<br />

business context, things have always<br />

been relatively unpredictable, and they<br />

still are. But a recent development<br />

is that companies must manage<br />

resources according to expectations<br />

no matter what happens. As we<br />

witnessed following the devastating<br />

tragedy in Japan, companies are now<br />

expected to manage and respond to<br />

extreme situations, which has not<br />

always been the case. For example,<br />

after 9/11, the world stood still for a<br />

moment. Nowadays we can’t allow<br />

anything to stand still. This means<br />

increased pressure on businesses to<br />

predict what’s going to happen, and<br />

to be much faster in responding to<br />

changes in the market.<br />

As a consequence, you have to be able<br />

to analyze very large volumes of data<br />

in real time. I noticed this ten years<br />

ago when I was doing a lot of cost<br />

accounting and financial consulting.<br />

Many companies were already<br />

considering moving away from<br />

annual planning and had rolling<br />

quarterly plans. This trend has now<br />

been taken to extremes.<br />

How is this possible?<br />

Traditional systems store data on<br />

a disk, and the disk is a relatively slow<br />

medium. Data stored in the main<br />

memory of a computer can<br />

be read ten thousand times faster.<br />

Today we even have parallel<br />

processing, which enables you to<br />

read data simultaneously on<br />

hundreds of processors and also<br />

allows you to read billions of records<br />

in just one second. This means that<br />

you can do on-the-fly calculations<br />

instead of calculating pre-aggregated<br />

data stored on disks. For the sake of<br />

visualization: in the time it takes<br />

you to carry a piece of information on<br />

a disk a distance of one meter,<br />

16 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

RUBRIK HIER<br />

Big Data, big business. SAP CEO Jim Hagemann Snabe wants to analyze the world in real time.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 17

<strong>THINK</strong>: IN-MEMORY-COMPUTING<br />

“We urgently need better forecasts to respond more<br />

quickly to change. So we need to analyze very large<br />

quantities of data in real time.”<br />

Jim Hagemann<br />

Snabe<br />

Biography<br />

Jim Hagemann<br />

Snabe, born in<br />

Denmark in 1965,<br />

has been co-chief<br />

executive of SAP AG<br />

with American Bill<br />

McDermott since<br />

February 2010. He<br />

began his career with<br />

the German software<br />

giant after graduating,<br />

and worked in<br />

various management<br />

positions in sales and<br />

development consultancy.<br />

He worked<br />

for IBM Denmark for<br />

two years, and then<br />

became a director of<br />

SAP in 2008. As an<br />

IT manager, he has a<br />

particular interest in<br />

you can carry it to Mars and back again<br />

with in-memory computing.<br />

All thanks to the falling price of<br />

memory?<br />

In technology, sometimes several trends<br />

come together and suddenly you have a<br />

whole new basis for innovation. The trends<br />

that coincide here are the falling price and<br />

increasing size of memory, combined with<br />

processing power and unique technology<br />

that allows us to compress information.<br />

All this together makes things unbelievably<br />

fast. The business impact of this is<br />

that you can start to do very advanced<br />

analytics, and you’re more able to anticipate<br />

the future based on statistical<br />

information. And, most importantly, you<br />

can start simulating the future. If you only<br />

have one second of response time, you can<br />

easily look at various scenarios.<br />

The ability to forecast seems to be crucial<br />

to in-memory technology. Can you<br />

explain how and why?<br />

I’ll give you an example. One of the main<br />

differences between a successful product<br />

and an unsuccessful one is production<br />

management: which product you choose<br />

to make, at what price and at what time.<br />

It’s proven that 80% of production planning<br />

is not productive. The demand is<br />

often higher or lower than expected, and<br />

you end up with either a shortage of supply<br />

or full warehouses. The ability to predict<br />

a trade promotion and its impact by<br />

location and product will make the differ-<br />

ence between successful and unsuccessful<br />

consumer goods companies.<br />

Have you carried out any studies on<br />

how in-memory computing can improve<br />

that rate?<br />

We’re actually working with some of the<br />

leading consumer product companies in<br />

the world – SAP customers. They’re using<br />

this new technology to reinvent management<br />

and planning. What used to take a<br />

couple of hours now happens in seconds,<br />

so you can start optimizing price and volume<br />

for any given product. Early adopters<br />

of the technology are reporting significant<br />

benefits and, on average, companies that<br />

have implemented such systems are seeing<br />

revenue gains of 21% and cost reductions<br />

of 19%.<br />

Is it true that you can now balance<br />

your supply chain management to the<br />

extent that you eliminate the need for<br />

additional storage?<br />

Yes, one of our clients is doing so now.<br />

What we consider to be a major consequence<br />

of this is what I would call a<br />

demand-driven supply chain. So far,<br />

the human interaction in this process<br />

has been putting information into the<br />

system. Now it’s all about optimizing the<br />

supply chain within companies and reacting<br />

quickly to changing demand.<br />

What makes you so certain that inmemory<br />

technology can really change<br />

the game?<br />

The whole thing started as a technological<br />

technology trends. Photo: SZ Photo<br />

18 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

innovation. What convinced me was<br />

what happened when we took the<br />

technology to fifty customers. We<br />

worked on very different scenarios<br />

customer by customer, industry by<br />

industry. And their feedback? “This<br />

is beyond belief.” They were stunned<br />

that you can simply push the enter<br />

button and get an immediate<br />

response to users’ reactions. In the<br />

past this would have taken hours of<br />

calculation.<br />

This was a real ‘wow’ moment for<br />

all of them. We recently presented<br />

in-memory computing to a whole<br />

series of companies who have now<br />

seen a massive increase in their<br />

opportunities, be it in production<br />

management or probability analysis<br />

by product. One utility company<br />

that employs dynamic pricing for<br />

electricity can now predict when<br />

capacity will be needed on its<br />

network. This saves the utility<br />

company a lot of money and helps<br />

consumers to minimize their use<br />

of electricity.<br />

This technology is clearly a musthave.<br />

What are the downsides?<br />

Implementation, perhaps?<br />

I wouldn’t call it a downside, it’s<br />

more of a challenge. If you don’t<br />

have consistent data, it doesn’t<br />

help that you can analyze it in one<br />

second. Many of the stories about<br />

the difficulty of implementing<br />

SAP technology are related to the<br />

fact that the SAP system requires<br />

a high degree of data consistency.<br />

We’ve been developing our system<br />

to acquire that consistency.<br />

If there aren’t any big drawbacks<br />

and the technology is so powerful,<br />

then why have only a few decision-<br />

makers in business heard about it?<br />

Initial conversations about inmemory<br />

focused exclusively on<br />

technology, making it irrelevant for<br />

business people. It’s only recently,<br />

with the results from those fifty<br />

customers, that we can communicate<br />

how this technology can<br />

solve business problems that were<br />

previously unsolvable. Also, there’s<br />

a lot of confusion about the topic.<br />

Many people talk about in-memory<br />

computing, but they all mean different<br />

things. We’re working on<br />

this. In-memory computing is a<br />

technological advance that we’re<br />

now translating into distinct business<br />

value. We can articulate how<br />

this will change the game in every<br />

single industry. This is the moment<br />

that it becomes relevant to business<br />

people, and then they need to try it,<br />

because most of them can’t believe<br />

it’s true. I’ve been in the industry for<br />

20 years and sometimes I’ve seen<br />

technology improving cost effectiveness<br />

by a factor of 5. With this,<br />

we’re talking about a factor of 200.<br />

It’s not only about reporting much<br />

faster: it’s about solving problems<br />

that you couldn’t solve before.<br />

What comes after in-memory<br />

computing?<br />

In the next five to ten years, we’ll<br />

see similar developments to those<br />

that followed our introduction<br />

of the client-server system in the<br />

1990s, when networks became<br />

faster and more powerful. Now<br />

we’re riding the wave of in-memory<br />

computing combined with multicore<br />

processors. Google has taught<br />

the world how to search for information,<br />

but we still haven’t learned<br />

how to find it. This technology can<br />

bring us much closer to finding not<br />

only the hay in the haystack, but<br />

also the needle.<br />

Five years from now, how much<br />

of the SAP portfolio will involve<br />

in-memory computing?<br />

All of it.<br />

Interview by Thomas Ramge<br />

Illustration Smetek<br />

<strong>THINK</strong>: IN-MEMORY-COMPUTING<br />

<strong>ACT</strong><br />

The digital revolution is<br />

transferring more and<br />

more data onto company<br />

databases.<br />

The more data there is,<br />

the harder it is to analyze<br />

using traditional IT methods.<br />

With time in increasingly<br />

short supply, managers<br />

with rapid access to data-<br />

based analysis can achieve<br />

a significant competitive<br />

advantage. In-memory<br />

computing promises to<br />

analyze the business world<br />

in real time, since data<br />

retrieval is no longer limited<br />

by the relatively slow speed<br />

of hard disks.<br />

Instead, information is<br />

analyzed by increasingly<br />

powerful memory chips.<br />

This is not just a nerdy IT<br />

issue; data-based processes<br />

are increasingly important<br />

to the success or failure of<br />

businesses in a growing<br />

number of sectors. Big data<br />

is a huge opportunity, but<br />

only for those who can sort<br />

the wheat from the chaff and<br />

draw the right conclusions.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 19

Do bailouts work?<br />

Comeback kid<br />

Keynes?<br />

Government bailouts enjoyed a worldwide renaissance during<br />

the recession, but what do they actually achieve? Nils aus dem Moore<br />

asks whether the kind of intervention favored by British economist<br />

John Meynard Keynes serves any purpose<br />

RESCUE PLANS: Do they work? There’s<br />

never been a better time to ask this<br />

question, never in human history have<br />

these plans been used on such a large<br />

scale by so many countries. On average,<br />

they cost around 2% of GDP in<br />

2009, and 1.6% in 2010. An IMF<br />

analysis shows that the biggest bailouts<br />

were in the United States, with a budgeted total of<br />

4.8% of GDP in 2009 and 2010, followed by China (4.4%)<br />

and Germany (3.4%). Another study, by the Brookings<br />

Institution in Washington, D.C., shows that the nature and<br />

size of the rescue packages varied a great deal. For example,<br />

Brazil and Russia relied almost entirely on tax cuts, while<br />

China and India focused on investment. In the European<br />

Union alone, over 350 individual programs had been agreed<br />

upon by February 2009.<br />

A detailed study by the Brussels think-tank Bruegel found<br />

that countries varied a great deal in their emphasis on the<br />

fi ve key components of a bailout: government investment,<br />

temporary or permanent tax cuts, welfare increases, employment<br />

programs, and aid for specifi c sectors. Germany<br />

implemented a large package of all fi ve, Britain relied mainly<br />

on a temporary reduction in VAT, Austria created permanent<br />

tax cuts, and Poland relied solely on infrastructure<br />

investment.<br />

So were the programs successful? At first<br />

sight, Germany appears to tick all the boxes; the<br />

Eurozone’s biggest economy saw a 5% slump<br />

in output during 2009, launched the EU’s<br />

biggest bailout at a cost of EUR 85 bn, and<br />

staged a spectacular comeback in 2010. Since<br />

then, unemployment has reached new lows<br />

and output has risen to pre-recession levels.<br />

This does not prove that the rapid recovery<br />

was caused by the bailout, or prove that<br />

the more money you put into a bailout, the<br />

more you get out. The United States’ experience<br />

has been quite different; according to the Congressional<br />

Budget Office, the American Recovery and Reinvestment<br />

Act (ARRA), passed in February 2009, will have cost USD<br />

830 bn by 2019. In spite of the program’s huge size, the<br />

recovery has been much slower than previous recoveries.<br />

To find out whether bailouts work, it’s not enough simply<br />

to compare different countries and their economies. To<br />

analyze their effectiveness, you have to isolate their impact<br />

20 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

<strong>THINK</strong>: BAILOUTS<br />

“Bailouts make sense<br />

only in historically<br />

exceptional situations”<br />

on GDP from all other factors involved; factors like<br />

monetary policy, the dynamics of world trade, and<br />

the price of key commodities like oil.<br />

Once you’ve broken down GDP into its<br />

component parts, you must analyze what<br />

would have happened without the bailout.<br />

This what-if analysis involves a degree of<br />

speculation, but it is the only convincing<br />

way of deciding whether bailouts work, so<br />

economists use macro models to simulate<br />

their effect.<br />

Optimistic simulations in the spring of<br />

2009 found that US gross domestic product<br />

was 3.6% higher at the end of 2010 than it<br />

would have been without tax cuts. Other economists<br />

using more downbeat assumptions concluded that it had<br />

increased by only 0.7% over the same period. More recent<br />

evaluations, using a wide variety of assumptions, have<br />

shown widely differing results. For example, the Congressional<br />

Budget Office estimates that the ARRA program<br />

has increased GDP by between 1.1% and 3.1% in the first<br />

quarter of this year, and has cut unemployment by 0.6 to<br />

1.8 percentage points.<br />

John Maynard Keynes: Return to<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 21<br />

favor, or last hurrah?

<strong>THINK</strong>: BAILOUTS<br />

<strong>ACT</strong><br />

Keynes is back, but<br />

probably not for long.<br />

In a recession, fi nancial<br />

decision-makers should<br />

realize that:<br />

1/ Monetary policy and<br />

the stabilizing role of<br />

tax and transfers are the<br />

best way to smooth<br />

the economic cycle.<br />

2/ Few governments<br />

are able to reduce debt<br />

created by defi cit spending<br />

once the good times<br />

return.<br />

3/ Structural problems<br />

need structural solutions.<br />

Nils aus dem Moore<br />

Columnist<br />

Nils heads the policy and communications<br />

department at the<br />

Berlin offi ce of the economic<br />

research body RWI Essen.<br />

He was formerly an associate<br />

of the Stiftung Neue Verant-<br />

wortung, and worked with<br />

RWI president Christoph M.<br />

Schmidt on the Bundestag’s<br />

commission of inquiry on<br />

growth, prosperity and quality<br />

of life. From 2005 to 2007, aus<br />

How does debt add value?<br />

Similar analysis of other countries’ economic programs has<br />

also been positive. In spite of all the imponderable variables<br />

involved, the bottom line is that without government intervention,<br />

the collapse in output would have been even more<br />

dramatic, and the job losses even greater. So what does this<br />

conclusion mean for future economic policy? In 2009, the<br />

historian and Keynes biographer Robert Skidelsky published<br />

an I-told-you-so tome, “Keynes, the Return of the Master,”<br />

proclaiming a new era of Keynesian government intervention.<br />

Economist Jeffrey Sachs, of Columbia University, contends that<br />

the success of recent bailouts was “the last hurrah of Keynesianism.”<br />

In the foreseeable future, he says, the huge increase in<br />

government debt will limit fi scal room for maneuver.<br />

Sachs may well be right. Many OECD economies are in an<br />

abysmal state, and there are three other reasons why Keynesianism<br />

is unlikely to make a lasting comeback:<br />

First, empirical research indicates that cyclical highs and<br />

lows can be smoothed out by a combination of monetary<br />

policy and the stabilizing effects of tax and transfers. Bailouts<br />

can be counterproductive if they’re slow to take effect, and<br />

in some cases they can actually make the troughs deeper.<br />

Second, during the postwar decades, Keynesian policies<br />

(2)<br />

usually failed in good times to reduce debt caused by defi cit<br />

spending in bad times. Third, current and future challenges Getty<br />

like emissions and demographic change are primarily struc- (2),<br />

tural, and structural problems need structural solutions.<br />

So the message is a nuanced one. During the normal eco- Akhtar<br />

nomic cycle, governments should rely on monetary policy, tax Amin<br />

and transfers to improve their fi nances. Big bailouts should<br />

be an absolute last resort for serious recessions. Photo:<br />

dem Moore edited the business<br />

section of the political<br />

magazine Cicero, and this year<br />

he won the Ludwig Erhard<br />

business journalism prize for<br />

his columns in the magazine.

REPORT<br />

Size matters in<br />

the modular economy

REPORT: THE MODULAR ECONOMY<br />

THE MODULAR ECONOMY The division of labor in the world<br />

economy continues apace. Small, agile, networked entities are<br />

increasingly successful, but big industrial giants are also profiting<br />

from the de-linking of the supply chain. In many sectors, clearly<br />

defined interfaces make cooperation with suppliers and service<br />

providers much easier than it used to be. The age of business ecosystems<br />

has begun. It is an age of collaboration between companies of very<br />

different sizes, and resurrecting one of the oldest questions in business:<br />

“How big should my company be?” There is no one-size-fits-all<br />

solution; rather, there are many different approaches to answering it.<br />

By Thomas Ramge Illustration & photos Sarah Illenberger<br />

Small versus big?<br />

A whole new army of Davids is on the rampage, some<br />

Goliaths are being slain, and small is the new big.<br />

US journalist, law professor and star blogger, Glenn<br />

Reynolds, has raised this subject a couple of times on<br />

his blog, instapundit.com. During the middle of the<br />

last decade, he pointed out that digital technology<br />

and the Internet were creating new opportunities<br />

for small businesses. Geeky students could run flourishing<br />

online businesses from their dorm rooms, and<br />

microbreweries were taking significant market share<br />

from giants like Miller and Budweiser.<br />

Reynolds described how 20th-century mass<br />

production, with its obsessive quest for economies<br />

of scale, no longer met the needs of 21st-century customers.<br />

Small was suddenly cool and, as he pointed<br />

out somewhat immodestly, a small blog founded in<br />

2001 could attract more readers in a day than many<br />

big local papers attracted in a week.<br />

The army of Davids began making inroads into<br />

big business. The image caught on, and in 2006<br />

Reynolds summarized his thoughts on the shift of<br />

power from big to small organizations in a small,<br />

pamphlet-like book, The Army of Davids. This<br />

promptly became a bestseller, and Reynolds became<br />

the chief exponent of a new economic philosophy;<br />

small is beautiful again, and the inexorable march<br />

of big corporations since the industrial revolution<br />

appears to have been halted. Economies of scale<br />

are no longer compatible with economies of scope.<br />

The mantras of 20th-century manufacturing were<br />

past their sell-by date, Reynolds said. In the past,<br />

if you doubled the number of items you made, you<br />

reduced your unit costs by 20 to 30%, but what’s<br />

the point when nobody wants to buy mass-produced<br />

goods any more, and the act of consumption is<br />

becoming increasingly individual? For Davids, tailormade<br />

products are where the big opportunities lie.<br />

One man, millions in profits<br />

The list of small-company-made-good stories is a<br />

long and rich canon. In 2007 the dating website<br />

plentyoffish.com, based in its Canadian creator’s<br />

home office, became what may have been the first<br />

one-person company to make an operating profit of<br />

more than USD 10 m.<br />

24 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

RUBRIK HIER<br />

SMALL<br />

versus BIG<br />

Small is beautiful... again. The<br />

inexorable rise of big organizations<br />

since the industrial revolution<br />

seems to have come to a temporary<br />

halt. Today, equipped with the<br />

sophisticated tools of the digital<br />

economy, and with limited<br />

overheads, small businesses can do<br />

things that were once done only by<br />

big corporations.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 25

RUBRIK HIER<br />

ONE MAN – millions in profits<br />

Tiny companies are everywhere you look. They market<br />

themselves globally, have almost no capital and, thanks to the<br />

Internet, can market their products and services worldwide.<br />

26 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

UNTANGLING<br />

those transaction costs<br />

Sports like kite surfing, which is enjoying a rapid<br />

worldwide increase in popularity, are supplied almost<br />

exclusively by small companies. Much of the<br />

innovation is being driven by fans rather than big<br />

design departments. Elsewhere, sales at the world’s<br />

biggest online platform for handicrafts, etsy.com,<br />

are approaching USD 500 m. Smaller manufacturers<br />

are enjoying a renaissance throughout the Western<br />

world. Anyone can buy Gucci, but true connoisseurs<br />

can make a statement by buying an ethical fashion<br />

label from Amsterdam.<br />

You might expect the world’s biggest seller of<br />

Darjeeling tea to be Unilever or some other food<br />

giant, yet it’s the Berlin company Teekampagne,<br />

founded by a professor of entrepreneurship and run<br />

by a handful of people. Perhaps the most impressive<br />

victory over the industry giants has been by a<br />

multitude of small and medium-sized companies<br />

with no names; over 50% of the world motorcycle<br />

market is now controlled by a network of suppliers<br />

and assemblers in China. Even the biggest are not<br />

exactly household names – Qingqi, Jialing, Zhejiang,<br />

Jincheng, Xindazhou – but these companies make<br />

very good bikes at affordable prices and sell them<br />

under eminently forgettable brand names. In the<br />

developing countries, they easily outsell the Japanese<br />

giants Yamaha, Honda and Kawasaki.<br />

Untangling those transaction costs<br />

In a standardized, networked world of flat hierarchies,<br />

small companies can often fight way above their<br />

weight class. It’s also an appealing idea, since Davids<br />

RUBRIK HIER<br />

To every action, there is an equal and opposite reaction.<br />

The online world is populated not only by tiny businesses, but also<br />

by juggernauts like Google, Facebook and eBay. The economies<br />

of scale apply just as much to clicks-and-mortar business models.<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 27

REPORT: THE MODULAR ECONOMY<br />

“When should companies outsource parts of their<br />

production to others who do certain things better,<br />

than they do?”<br />

have traditionally attracted more sympathy than<br />

Goliaths. Of course, Glenn Reynolds’ opinions are<br />

generalizations. Yes, these success stories do exist,<br />

and technological standardization and the Internet<br />

make life easier for small businesses, but the army of<br />

David’s theory is based largely on anecdotes.<br />

Look more closely and you soon realize that<br />

mass production and distribution are expanding<br />

inexorably. The online world is dominated by behemoths<br />

like Amazon, Google, Facebook and Zynga,<br />

and they’re getting bigger by the month. Offline,<br />

car manufacturers form alliances with big players<br />

in the electrochemical industry, and the insurance<br />

industry continues to consolidate, McDonald’s<br />

has cruised out of the doldrums and is expanding<br />

globally, and many big banks are riding the crest<br />

of a wave again.<br />

Reynolds’ opinions are still thought-provoking.<br />

They prompt us to ask an old but important business<br />

question from a new perspective: how vertically<br />

integrated do companies need to be in order to<br />

collaborate effectively in ecosystems? Or to put it<br />

another way, when should they outsource part of<br />

their production to others who do a better job?<br />

One person who tried to answer this question<br />

was awarded a Nobel Prize for his efforts. The<br />

British economist Ronald Coase won the Nobel<br />

Prize in 1991 for his essay The Nature of the Firm,<br />

written more than fifty years prior in 1937. In his<br />

work, he expressed doubts about the Ford business<br />

model, which involved doing everything in-house<br />

from start to finish. In those days, Ford didn’t<br />

just concentrate on building good cars; it made its<br />

own steel, generated its own power, made its own<br />

windshield glass, and sold cars directly to customers.<br />

To a socialist economist, this was inefficient, and<br />

the solution was the Coase theorem, a milestone in<br />

economic history.<br />

The theorem says that there are always transaction<br />

costs involved in the division of labor and that<br />

these can be divided into categories. There are search<br />

costs, the cost of finding things such as employees,<br />

capital, materials, and information about production<br />

processes; there are contract costs, the costs<br />

of negotiating agreements, such as lawyers’ fees;<br />

finally, there are coordination costs which are the<br />

costs of the effort involved in ensuring that everyone<br />

involved works together efficiently. Coase concluded<br />

that companies would always seek vertical integration<br />

if their bottom-line external transaction costs<br />

were higher than the cost of the employees doing<br />

the job in-house.<br />

The Power of small parts<br />

The one thing that has changed since Coase analyzed<br />

Ford’s vertically integrated production is transaction<br />

costs. Today’s economy works on the Lego principle;<br />

the bricks snap neatly together, they don’t fall apart,<br />

and they can be combined in many different ways.<br />

Over the last few decades, the supply chain has<br />

28 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

THE POWER<br />

of small parts<br />

The supply chain<br />

has gone modular.<br />

Today‘s technology and<br />

business processes are<br />

highly standardized.<br />

This opens up big<br />

opportunities for large<br />

and small organizations<br />

working together<br />

in ecosystems.<br />

RUBRIK HIER<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 29

RUBRIK HIER<br />

The ideal<br />

SIZE<br />

What‘s the ideal size for a<br />

company? There‘s no single answer<br />

to this question; it depends on the<br />

individual context. These days,<br />

small companies can quickly get<br />

big, and vice versa.<br />

30 <strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011

REPORT: THE MODULAR ECONOMY<br />

been organized in an increasingly modular way<br />

because the cost of working with other businesses<br />

has become so low. Count the components of your<br />

cell phone, and you’ll find out how many suppliers were<br />

involved in its production. Battery, microphone, antenna,<br />

display, chip, SIM card; each comes from a<br />

hidden champion in one particular industry.<br />

In a modular world, interfaces are increasingly<br />

well defined: technological, logistical, legal, and<br />

administrative. Hard disks fit any laptop, products and<br />

parts arrive on time, and contracts and processes are<br />

standardized. Transferring money between almost<br />

any two countries on Earth is no longer a barrier<br />

to trade.<br />

At the same time, companies can now rely on<br />

business-to-business providers for almost any stage<br />

in their production process. A company with half a<br />

dozen workers like Teekampagne can become the<br />

world’s biggest seller of Darjeeling by outsourcing<br />

nearly all of its processes, including its call center,<br />

accounts, packing and dispatch – all done by<br />

outsiders.<br />

In the networked world, Davids can have their<br />

cake and eat it. It’s never been easier to supply<br />

modules such as cell phone antennas to the Goliath<br />

ecosystem, and you can even assemble the modules<br />

yourself as medium-sized locomotive builders do.<br />

If you play your cards right, and are sufficiently flexible,<br />

you can often be extremely competitive with an<br />

overweight Goliath.<br />

David Teece, director of the Institute of Management,<br />

Innovation and Organization at the University<br />

of California, Berkeley, says that in the modular<br />

economy, a clever David can orchestrate a network.<br />

It can score points with its dynamic capabilities<br />

and its ability to respond to market change, but it<br />

can also get knocked out. These capabilities, Teece<br />

believes, are the key to a business’ success or failure.<br />

The ideal size<br />

Take a few steps back, and it’s clear that the debate<br />

about big or small, insourcing or outsourcing, hierarchies<br />

or networks, has been going on since long<br />

before the Internet was invented. “The issue of the<br />

ideal business size crops up more and more often,”<br />

observes management scientist Stefan Kühl. “Sometimes<br />

the management pendulum swings one way,<br />

sometimes the other.”<br />

<strong>THINK</strong> <strong>ACT</strong> SEPTEMBER 2011 31

REPORT: THE MODULAR ECONOMY<br />

“In a market economy, only the Goliaths can<br />

shoulder the big risks – though this won’t stop<br />

the army of Davids from coming up with lots<br />

of good ideas”<br />

Traditional hierarchies do have their advantages,<br />

he points out. They can help organizations to make<br />

and implement decisions more quickly. They allow<br />

certain forms of behavior to be sanctioned and they<br />

are less susceptible to one of the key problems of<br />

networked systems: everyone wants to profit, but<br />

no one is willing to contribute money upfront. Also,<br />

in many sectors, innovation is a capital-intensive<br />

process; Davids cannot build the networks of<br />

hydrogen fuel stations needed to make environmentfriendly<br />

fuel-cell vehicles more popular, nor can<br />

they afford the expensive and uncertain process of<br />

obtaining drug licenses. In a market economy, only<br />

the giants can shoulder the big risks – though this<br />

won’t stop the army of Davids from coming up with<br />

lots of good ideas.<br />

This brings us back to the crux of the matter;<br />

what is the ideal size for a company? This is one of<br />

the eternal questions of business, and it’s impossible<br />

to generalize; however, because today’s interfaces<br />

are so clearly defined, the supply chain so highly<br />

segmented, and outsourcing so much more effective<br />

than it used to be, it has never been easier to set up<br />

a successful new business with limited capital. That<br />

said, the David versus Goliath image is misleading.<br />

Big and small at the same time<br />

Big and small are not a contradiction in terms,<br />

either from a business or a macroeconomic point of<br />

view; you can be both simultaneously. For example,<br />

you can insource your administration and production<br />

to take advantage of economies of scale, and<br />

outsource your innovation and value creation. If you<br />

do this successfully, it resolves a classic management<br />

conf lict: hierarchies are no longer a barrier to<br />

innovation and customer focus, and decentralization<br />

does not stop you from profiting as a result<br />

economies of scale.<br />

At the macro level, a healthy economy needs<br />

a mix of small, midsized and large companies.<br />