Russian Journal of Agricultural and Socio-Economic Sciences ...

Russian Journal of Agricultural and Socio-Economic Sciences ...

Russian Journal of Agricultural and Socio-Economic Sciences ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

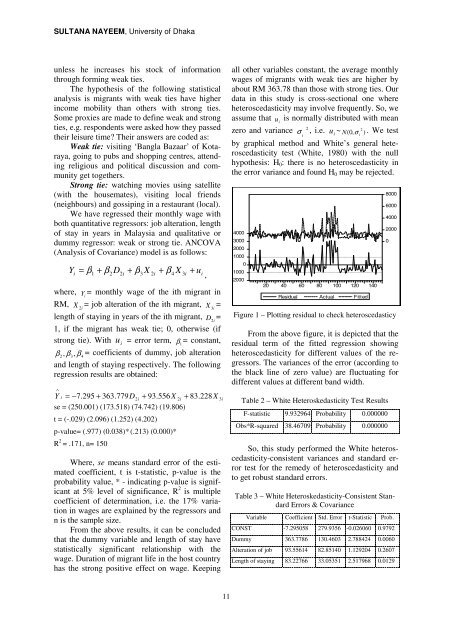

SULTANA NAYEEM, University <strong>of</strong> Dhakaunless he increases his stock <strong>of</strong> informationthrough forming weak ties.The hypothesis <strong>of</strong> the following statisticalanalysis is migrants with weak ties have higherincome mobility than others with strong ties.Some proxies are made to define weak <strong>and</strong> strongties, e.g. respondents were asked how they passedtheir leisure time? Their answers are coded as:Weak tie: visiting ‘Bangla Bazaar’ <strong>of</strong> Kotaraya,going to pubs <strong>and</strong> shopping centres, attendingreligious <strong>and</strong> political discussion <strong>and</strong> communityget togethers.Strong tie: watching movies using satellite(with the housemates), visiting local friends(neighbours) <strong>and</strong> gossiping in a restaurant (local).We have regressed their monthly wage withboth quantitative regressors: job alteration, length<strong>of</strong> stay in years in Malaysia <strong>and</strong> qualitative ordummy regressor: weak or strong tie. ANCOVA(Analysis <strong>of</strong> Covariance) model is as follows:Yi= β1 + β2D2i+ β3X2i+ β4X3i+ ui,where, Y = monthly wage <strong>of</strong> the ith migrant iniRM, X 2= job alteration <strong>of</strong> the ith migrant,iX 3=ilength <strong>of</strong> staying in years <strong>of</strong> the ith migrant, D 2=i1, if the migrant has weak tie; 0, otherwise (ifstrong tie). With ui= error term, β = constant,1β2, β3,β = coefficients <strong>of</strong> dummy, job alteration4<strong>and</strong> length <strong>of</strong> staying respectively. The followingregression results are obtained:∧Y i = −7 .295 + 363.779D2i+ 93.556X2i+ 83. 228X3ise = (250.001) (173.518) (74.742) (19.806)t = (-.029) (2.096) (1.252) (4.202)p-value= (.977) (0.038)* (.213) (0.000)*R 2 = .171, n= 150Where, se means st<strong>and</strong>ard error <strong>of</strong> the estimatedcoefficient, t is t-statistic, p-value is theprobability value, * - indicating p-value is significantat 5% level <strong>of</strong> significance, R 2 is multiplecoefficient <strong>of</strong> determination, i.e. the 17% variationin wages are explained by the regressors <strong>and</strong>n is the sample size.From the above results, it can be concludedthat the dummy variable <strong>and</strong> length <strong>of</strong> stay havestatistically significant relationship with thewage. Duration <strong>of</strong> migrant life in the host countryhas the strong positive effect on wage. Keepingall other variables constant, the average monthlywages <strong>of</strong> migrants with weak ties are higher byabout RM 363.78 than those with strong ties. Ourdata in this study is cross-sectional one whereheteroscedasticity may involve frequently. So, weassume that u is normally distributed with meani22zero <strong>and</strong> variance σ , i.e. u ~ii N(0,σi) . We testby graphical method <strong>and</strong> White’s general heteroscedasticitytest (White, 1980) with the nullhypothesis: H 0 : there is no heteroscedasticity inthe error variance <strong>and</strong> found H 0 may be rejected.4000300020001000-1000-2000020 40 60 80 100 120 140Residual Actual FittedFigure 1 – Plotting residual to check heteroscedasticyFrom the above figure, it is depicted that theresidual term <strong>of</strong> the fitted regression showingheteroscedasticity for different values <strong>of</strong> the regressors.The variances <strong>of</strong> the error (according tothe black line <strong>of</strong> zero value) are fluctuating fordifferent values at different b<strong>and</strong> width.Table 2 – White Heteroskedasticity Test ResultsF-statistic 9.932964 Probability 0.000000Obs*R-squared 38.46709 Probability 0.0000008000600040002000So, this study performed the White heteroscedasticity-consistentvariances <strong>and</strong> st<strong>and</strong>ard errortest for the remedy <strong>of</strong> heteroscedasticity <strong>and</strong>to get robust st<strong>and</strong>ard errors.Table 3 – White Heteroskedasticity-Consistent St<strong>and</strong>ardErrors & CovarianceVariable Coefficient Std. Error t-Statistic Prob.CONST -7.295058 279.9356 -0.026060 0.9792Dummy 363.7786 130.4603 2.788424 0.0060Alteration <strong>of</strong> job 93.55614 82.85140 1.129204 0.2607Length <strong>of</strong> staying 83.22766 33.05351 2.517968 0.0129011