with the commitment cannot be ascertained except that as of December 31, 2005 these <strong>we</strong>re estimated worth $45.66 million orapproximately more than 2.34 billion. Additions thereafter, including the newly completed building utilized as PPA Head Officewith allocated contract cost of 520 million cannot be determined as of December 31, 2008.Further as discussed in Audit Observation No. 3, the computation of the dividend due to the Bureau of Treasury (BTr) was not inaccordance with the provision of Section 3 of RA 7656, resulting in the understatement of the retained earnings and overstatementof dividends payable by 179.70 million for income earned in 2007 and the non-recognition of dividends of 1.01 billion for incomeof 2008 that is due for payment in 2009. In conformity with PAS 21 Gain/Loss on Revaluation is recognized as of reporting date torecognize the effects of foreign exchange fluctuations on PPA’s outstanding foreign loans and dollar savings deposit. This recordedgain or loss adjusting the peso equivalent of the foreign denominated accounts is treated as a non-taxable income and nonallowablededuction, respectively in determining the corporate income subject to tax. In the computation of the dividend basesubject to the rate of 50% mandated in RA 7656, the net loss on revaluation in 2008 which is a non-allowable deduction under theInternal Revenue Code was not added back while, the non-taxable net gain on revaluation in 2007 was not excluded.Also as disclosed in Audit Observation No. 8, various assets amounting to 214.72 million and a miscellaneous liability accountof 1.96 million still carried in the books as of December 31, 2008, are doubtful and unreliable. Further, the related Provision forDoubtful Accounts Receivable is understated by 13.11 million. The inflow or outflow of economic benefit on some of theaccounts which have been unidentified, dormant or inactive and unrealized for several years more likely is no longer probable.We <strong>we</strong>re unable to obtain from management sufficient appropriate audit evidence about the reasonable value of the unrecordedassets and depreciation, the inactive and unidentified subsidiary accounts, and those covered with the concession arrangementhaving no access to the records of the concession Service Operator. Consequently, the financial information that may be necessaryin determining the over/understatement on the value of property and equipment account, the reliability and validity of the inactiveaccounts, and to assist in assessing the certainty of cash inflow or benefit that may be derived from the assets under arrangementcannot be provided.Qualified OpinionIn our opinion, except for the effects of such adjustments and disclosures, if any, as might had been necessary on the mattersreferred to in the preceding paragraphs the financial statements present fairly, in all material respects, the financial position of the<strong>Philippine</strong> <strong>Ports</strong> <strong>Authority</strong> as of December 31, 2008, and of its financial performance and its cash flows for the year then ended inaccordance with accounting principles generally accepted in the <strong>Philippine</strong>s.Emphasis of MatterWithout further qualifying our opinion, <strong>we</strong> draw attention to the contingent accounts which had amounted to a significant 903.03million as of December 31, 2008. In conformity with PAS 37, the contingent accounts comprised mostly of contested accountsreceivable on lease where the inflow of cash is not virtually certain of collection <strong>we</strong>re not presented in the financial statements but<strong>we</strong>re adequately disclosed in accompanying Note 47 and partially discussed in Audit Observation No. 4. Relatively, the net lossof the PPA for CY 2008 will be significantly reduced and its Retained Earnings will significantly increase had the contestability anduncertainty of said Accounts Receivable been settled or resolved.<strong>Philippine</strong> <strong>Ports</strong> <strong>Authority</strong> • Annual Report 2008 3 4Other MatterAs part of our audit of the 2008 financial statements, <strong>we</strong> also audited the adjustments described in Note 45 that <strong>we</strong>re applied toamend the 2007 financial statements. In our opinion, such adjustments are appropriate and have been properly applied.July 8, 2009BY:COMMISSION ON AUDITDIVINIA M. ALAGONDirector IV

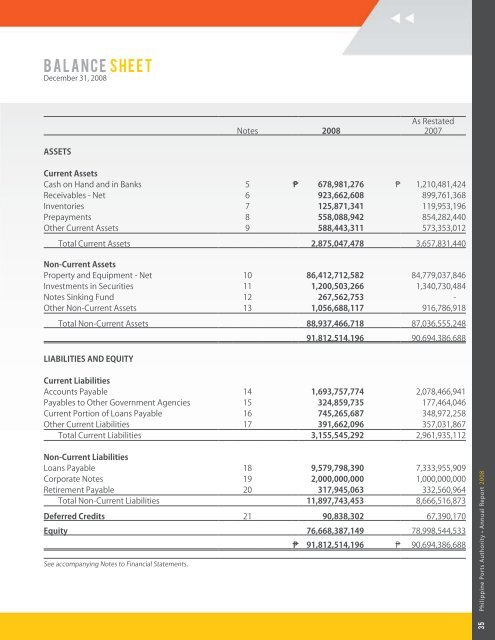

B A L A N C E S H E E TDecember 31, 2008Notes 2008As Restated2007ASSETSCurrent AssetsCash on Hand and in Banks 5 678,981,276 1,210,481,424Receivables - Net 6 923,662,608 899,761,368Inventories 7 125,871,341 119,953,196Prepayments 8 558,088,942 854,282,440Other Current Assets 9 588,443,311 573,353,012Total Current Assets 2,875,047,478 3,657,831,440Non-Current AssetsProperty and Equipment - Net 10 86,412,712,582 84,779,037,846Investments in Securities 11 1,200,503,266 1,340,730,484Notes Sinking Fund 12 267,562,753 -Other Non-Current Assets 13 1,056,688,117 916,786,918Total Non-Current Assets 88,937,466,718 87,036,555,248LIABILITIES AND EQUITY91,812,514,196 90,694,386,688Current LiabilitiesAccounts Payable 14 1,693,757,774 2,078,466,941Payables to Other Government Agencies 15 324,859,735 177,464,046Current Portion of Loans Payable 16 745,265,687 348,972,258Other Current Liabilities 17 391,662,096 357,031,867Total Current Liabilities 3,155,545,292 2,961,935,112Non-Current LiabilitiesLoans Payable 18 9,579,798,390 7,333,955,909Corporate Notes 19 2,000,000,000 1,000,000,000Retirement Payable 20 317,945,063 332,560,964Total Non-Current Liabilities 11,897,743,453 8,666,516,873Deferred Credits 21 90,838,302 67,390,170Equity 76,668,387,149 78,998,544,533See accompanying Notes to Financial Statements.91,812,514,196 90,694,386,688<strong>Philippine</strong> <strong>Ports</strong> <strong>Authority</strong> • Annual Report 20083 5