e-IFRSline May 06 - IAS 39: Financial Instruments - Grant Thornton

e-IFRSline May 06 - IAS 39: Financial Instruments - Grant Thornton

e-IFRSline May 06 - IAS 39: Financial Instruments - Grant Thornton

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

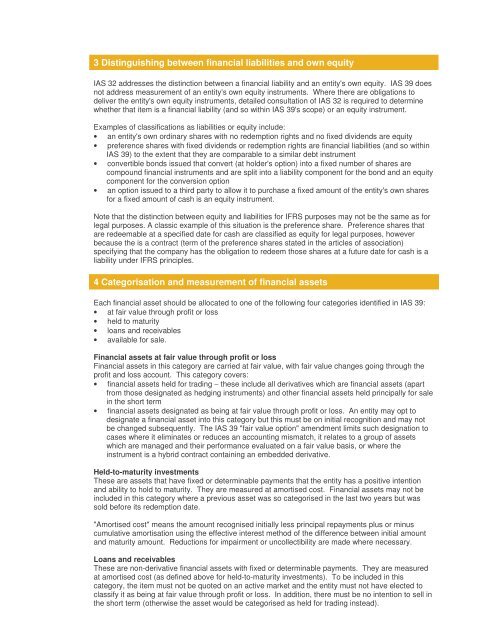

3 Distinguishing between financial liabilities and own equity<strong>IAS</strong> 32 addresses the distinction between a financial liability and an entity's own equity. <strong>IAS</strong> <strong>39</strong> doesnot address measurement of an entity's own equity instruments. Where there are obligations todeliver the entity's own equity instruments, detailed consultation of <strong>IAS</strong> 32 is required to determinewhether that item is a financial liability (and so within <strong>IAS</strong> <strong>39</strong>'s scope) or an equity instrument.Examples of classifications as liabilities or equity include:• an entity's own ordinary shares with no redemption rights and no fixed dividends are equity• preference shares with fixed dividends or redemption rights are financial liabilities (and so within<strong>IAS</strong> <strong>39</strong>) to the extent that they are comparable to a similar debt instrument• convertible bonds issued that convert (at holder's option) into a fixed number of shares arecompound financial instruments and are split into a liability component for the bond and an equitycomponent for the conversion option• an option issued to a third party to allow it to purchase a fixed amount of the entity's own sharesfor a fixed amount of cash is an equity instrument.Note that the distinction between equity and liabilities for IFRS purposes may not be the same as forlegal purposes. A classic example of this situation is the preference share. Preference shares thatare redeemable at a specified date for cash are classified as equity for legal purposes, howeverbecause the is a contract (term of the preference shares stated in the articles of association)specifying that the company has the obligation to redeem those shares at a future date for cash is aliability under IFRS principles.4 Categorisation and measurement of financial assetsEach financial asset should be allocated to one of the following four categories identified in <strong>IAS</strong> <strong>39</strong>:• at fair value through profit or loss• held to maturity• loans and receivables• available for sale.<strong>Financial</strong> assets at fair value through profit or loss<strong>Financial</strong> assets in this category are carried at fair value, with fair value changes going through theprofit and loss account. This category covers:• financial assets held for trading − these include all derivatives which are financial assets (apartfrom those designated as hedging instruments) and other financial assets held principally for salein the short term• financial assets designated as being at fair value through profit or loss. An entity may opt todesignate a financial asset into this category but this must be on initial recognition and may notbe changed subsequently. The <strong>IAS</strong> <strong>39</strong> "fair value option" amendment limits such designation tocases where it eliminates or reduces an accounting mismatch, it relates to a group of assetswhich are managed and their performance evaluated on a fair value basis, or where theinstrument is a hybrid contract containing an embedded derivative.Held-to-maturity investmentsThese are assets that have fixed or determinable payments that the entity has a positive intentionand ability to hold to maturity. They are measured at amortised cost. <strong>Financial</strong> assets may not beincluded in this category where a previous asset was so categorised in the last two years but wassold before its redemption date."Amortised cost" means the amount recognised initially less principal repayments plus or minuscumulative amortisation using the effective interest method of the difference between initial amountand maturity amount. Reductions for impairment or uncollectibility are made where necessary.Loans and receivablesThese are non-derivative financial assets with fixed or determinable payments. They are measuredat amortised cost (as defined above for held-to-maturity investments). To be included in thiscategory, the item must not be quoted on an active market and the entity must not have elected toclassify it as being at fair value through profit or loss. In addition, there must be no intention to sell inthe short term (otherwise the asset would be categorised as held for trading instead).