18food sector is very difficult to extend, however, generally due to the fact that the main companies involvedare quite small; incorporating them in an union or organisation is difficult, although it is theonly means to reduce the cost of promotion and to be competitive in this mass market. Individualismand the lack of innovation are the main characteristics of this sector. To develop these small local foodcompanies, owners have to develop networks with other companies to create new organisations fordevelopment and to have a counter-power against the main distribution brands. (Rastoin JL, 2001)Therefore, only companies which are profitable in this sector are innovating companies. Innovationseems to be a bit paradoxical when you mention tradition and old culture for local products, but theinnovation of packaging and especially the sale location will be the foundations for the profitability ofthis type of company.These companies were also successful since they understood that consumer needs are in “contact”with the producers. This underlines and explains why only small companies make local food. It is impossibleto have an international brand making local food for consumers. In some companies likeRaymond Geoffroy with regards to “la brandade de morue de Nîmes” or Marius Bernard “la bouillabaisse”,consumers can directly visit the company and discover how the product is produced. In thisway, it resembles the close proximity which is possible when one can visit production on a farm, forexample.(Rastoin JL, 2001, 1999)Producers are more affected and involved with the process of labelling than transformers or distributors,who generally are not compatible with the policy of CCP, which is more adapted for supply chainthan production.2.3 The Terroir companiesThree main types of manufacturing of local food exist. One type involves manufacturing directly bythe producer, which often lacks labelling since in most cases it involves a direct sale on his/her ownfarm or in a cooperative. This producer may discuss and ensure the product and its quality to the consumer,as opposed to conventional quality-assurance methods represented by the Official Signs ofQuality. Currently, there are more than 120 000 producers who manufacture a PDO or PGI product,which represent approximately 15% of the professional producers in France. However, it is also possiblethat there are a lot of other producers of local food who are not using appellations, making it difficultto know the real number of producers who directly sell on their farm without the Official Signs ofquality.The second type of manufacturing involves organisation within a Union of producers which also managesthe product’s commercialisation (i.e. Roquefort PDO). This organisation with an administrationboard can be a means to counter-balance the power of distributors when the products are not sold bythe producers themselves. It also manages advertisement with a common budget, as well as future orientationsfor the appellation or products.Finally, local companies may also manufacture local food, with local or regional area influence (territorywhere the raw materials are bought). However, these companies may also produce products forstore brands, which explains why some local companies have increased their production capacity sincethe introduction of these store brands.

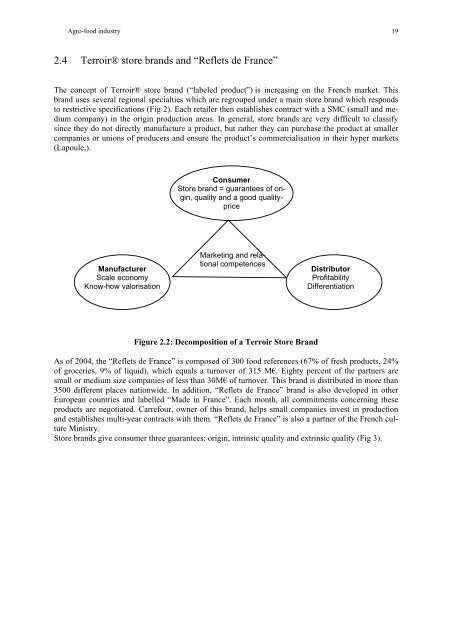

Agro-food industry 192.4 Terroir® store brands and “Reflets de France”The concept of Terroir® store brand (“labeled product”) is increasing on the French market. Thisbrand uses several regional specialties which are regrouped under a main store brand which respondsto restrictive specifications (Fig 2). Each retailer then establishes contract with a SMC (small and mediumcompany) in the origin production areas. In general, store brands are very difficult to classifysince they do not directly manufacture a product, but rather they can purchase the product at smallercompanies or unions of producers and ensure the product’s commercialisation in their hyper markets(Lapoule,).ConsumerStore brand = guarantees of origin,quality and a good qualitypriceManufacturerScale economyKnow-how valorisationMarketing and relationalcompetencesDistributorProfitabilityDifferentiationFigure 2.2: Decomposition of a Terroir Store BrandAs of 2004, the “Reflets de France” is composed of 300 food references (67% of fresh products, 24%of groceries, 9% of liquid), which equals a turnover of 315 M€. Eighty percent of the partners aresmall or medium size companies of less than 30M€ of turnover. This brand is distributed in more than3500 different places nationwide. In addition, “Reflets de France” brand is also developed in otherEuropean countries and labelled “Made in France”. Each month, all commitments concerning theseproducts are negotiated. Carrefour, owner of this brand, helps small companies invest in productionand establishes multi-year contracts with them. “Reflets de France” is also a partner of the French cultureMinistry.Store brands give consumer three guarantees: origin, intrinsic quality and extrinsic quality (Fig 3).