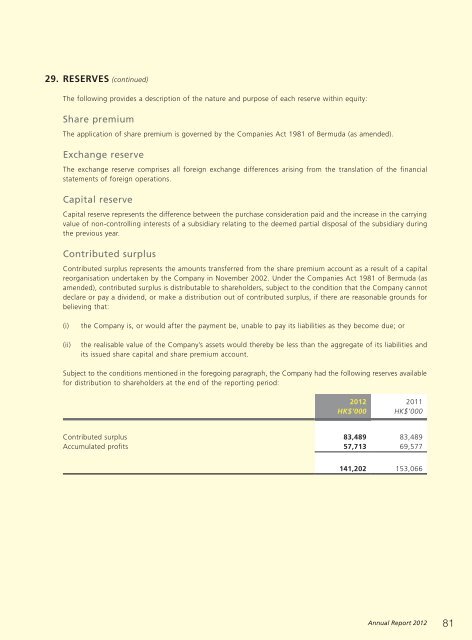

29. RESERVES (continued)The following provides a description of the nature and purpose of each reserve within equity:Share premiumThe application of share premium is governed by the Companies Act 1981 of Bermuda (as amended).Exchange reserveThe exchange reserve comprises all foreign exchange differences arising from the translation of the financialstatements of foreign operations.Capital reserveCapital reserve represents the difference between the purchase consideration paid and the increase in the carryingvalue of non-controlling interests of a subsidiary relating to the deemed partial disposal of the subsidiary duringthe previous year.Contributed surplusContributed surplus represents the amounts transferred from the share premium account as a result of a capitalreorganisation undertaken by the Company in November 2002. Under the Companies Act 1981 of Bermuda (asamended), contributed surplus is distributable to shareholders, subject to the condition that the Company cannotdeclare or pay a dividend, or make a distribution out of contributed surplus, if there are reasonable grounds forbelieving that:(i)(ii)the Company is, or would after the payment be, unable to pay its liabilities as they become due; orthe realisable value of the Company’s assets would thereby be less than the aggregate of its liabilities andits issued share capital and share premium account.Subject to the conditions mentioned in the foregoing paragraph, the Company had the following reserves availablefor distribution to shareholders at the end of the reporting period:<strong>2012</strong> 2011HK$’000 HK$’000Contributed surplus 83,489 83,489Accumulated profits 57,713 69,577141,202 153,066<strong>Annual</strong> <strong>Report</strong> <strong>2012</strong> 81

e-<strong>KONG</strong> GROUP LIMITEDNotes to the Consolidated Financial Statements (continued)For the year ended 31 December <strong>2012</strong>30. CASH GENERATED FROM / (USED IN) OPERATIONSConsolidated<strong>2012</strong> 2011HK$’000 HK$’000Loss before taxation:Continuing operations (552) (9,098)Discontinued operation – (5,190)(552) (14,288)Interest income (510) (624)Interest expenses 218 1,327Interest on obligations under finance leases 18 115Depreciation of property, plant and equipment 12,538 11,519Amortisation of intangible assets 3,615 1,804Share of results of an associate (39) (84)Exchange differences 76 (453)Loss on disposal of property, plant and equipment 59 141Allowance for doubtful debts 2,252 2,949Impairment loss on property, plant and equipment 75 –Gain on bargain purchase (796) –Changes in working capital:Inventories (269) (1,454)Trade and other receivables 5,107 11,721Trade and other payables 3,414 (33,782)Cash generated from / (used in) operations 25,206 (21,109)31. CONTRIBUTION OF A SUBSIDIARY TO A JOINTLY-CONTROLLED ENTITY INRETURN FOR 50% EQUITY INTERESTS IN JOINTLY-CONTROLLED ENTITYDuring 2011, the <strong>Group</strong> contributed a subsidiary with a net asset value of HK$84,234,000 (including cash and bankbalances of HK$69,726,000, other assets of HK$99,962,000 and total liabilities of HK$85,454,000) to a jointlycontrolledentity, in return for a 50% equity interest in the jointly-controlled entity valued at HK$173,311,000for the businesses contributed by the two venturers. After the effect of the release from exchange reserves ofHK$1,878,000, the gross gain on disposal of the subsidiary was HK$90,955,000, which represented a realisedgain of HK$52,412,000 and an unrealised gain of HK$38,543,000. The unrealised gain was eliminated against theunderlying assets contributed to the jointly-controlled entities under the proportionate consolidation accountingmethod.The above transaction was effectively an exchange of 50% interests in the subsidiary with the 50% interests inthe business contributed by the other venturer from the <strong>Group</strong>’s perspective. The calculation below presents thetransaction in this way and, thereby, excludes the unrealised portion of the contribution of the 50% interests inthe subsidiary from the transaction.No tax expense arose in 2011 in respect of the gain on disposal from the above transaction.82<strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>