ICABC Awards for Early Achievement - Institute of Chartered ...

ICABC Awards for Early Achievement - Institute of Chartered ...

ICABC Awards for Early Achievement - Institute of Chartered ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Is this enough to secure your data?The practical guidance you need to preventdata breaches in today’s high-speed world.The Canadian Privacy and Data Security Toolkit<strong>for</strong> Small and Medium Enterprises by Claudiu PopaThis easy-to-use Toolkit features:• Self-assessments to help determine your organization'sdata security and privacy risks• Advice on privacy and security risks in areas such asaccounts payable, sales and marketing• A CD-ROM containing checklists, in<strong>for</strong>mative articles,training templates and a customizable privacy policy• Foreword by Jennifer Stoddart, Privacy Commissioner<strong>of</strong> Canada• Introductory chapter by Ann Cavoukian, Ph.D,In<strong>for</strong>mation and Privacy Commissioner <strong>of</strong> OntarioCheck out the CICA'sPrivacy Resource Centre<strong>for</strong> more privacy toolsand aids such as:• Generally AcceptedPrivacy Principles(updated in 2009)• Privacy RiskAssessment Tool• 20 Questions BusinessesShould Ask About Privacy2 ica.bc.ca June/Summer ’09Order your copy today!Visit www.cica.ca/privacy or call the CICAorder department at 1-800-268-3973.

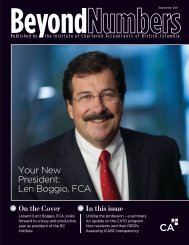

contentsOn the Cover8Meet Our <strong>Early</strong><strong>Achievement</strong> AwardWinners!14<strong>Awards</strong> <strong>for</strong> CommunityService16Ritchie W. McCloyAward <strong>for</strong> Volunteerismin the Pr<strong>of</strong>ession18Regional BC Check-UpReport ReleasedSee how your region stackedup in 200831Demystifying CPDDispelling the myths aboutCPD requirementsFSC logo RRDto placeCert no. SCS-COC-008674 Notes from the PresidentA look back at 2008/20095 For the Pr<strong>of</strong>essionGAAP <strong>for</strong> private enterprisesis here!6 Research CornerThe uncertain nature <strong>of</strong>university research22 Tax Traps & TipsThe greening <strong>of</strong> tax26 Financial Facts &Money MattersSelling privately ownedbusinesses in a pooreconomic climate29 PD NewsSummer PD highlights34 Plugged InNews <strong>for</strong> and about members& students Movers & shakers in thepr<strong>of</strong>ession 50 and 60-year members In Memoriam Did you know...? A note fromMember Services AGM Reminder38 Ethical DilemmasWhat’s in a name? Trouble,potentially.10%Want to getthe word out?Advertise in Beyond Numbers!Here’s why:90% <strong>of</strong> BC CAs surveyed readBeyond NumbersBeyond Numbers goes out tomore than 9,000 members,more than 1,600 students,and over 200 externalstakeholders—includingother institutes, associations,and pr<strong>of</strong>essional organizationsBeyond Numbers has wonawards <strong>for</strong> both contentand design, includingBlue Wave <strong>Awards</strong> <strong>of</strong> Meritfrom the InternationalAssociation <strong>of</strong> BusinessCommunications – BC BranchTo place an ad inBeyond Numbers, contact ourrepresentatives at:Advertising in PrintTel: 604-681-1811710 – 938 Howe St.Vancouver, BC V6Z 1N9Fax: 604-681-0456Email:info@advertisinginprint.comJune/Summer ’09 ica.bc.ca 3

June/Summer 2009, No.480Published eight times annually by the<strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong> Accountants<strong>of</strong> British Columbia.A look back at 2008/09EditorMichelle McRaeDesignBlindfolio Design604-761-9212AdvertisingAdvertising In PrintPhone: 604-681-1811Fax: 604-681-0456Senior Director <strong>of</strong> External AffairsLesley MacGregor<strong>Institute</strong> CouncilDoug Murphy, FCAPresidentKaren Keilty, FCA1st Vice-PresidentPeter Norwood, CA2nd Vice-PresidentRobert Wicks, CA, CFPTreasurerJack Arnold, CALenard Boggio, FCALindalee Brougham, CAKyman Chan, CAKaren Christiansen, CAJohn Craw<strong>for</strong>d, CADavid HughesMichael Macdonell, CAAnthony Mayer, CAAl McNairJohn Sims, FCAJames Topham, CAKenneth TungPraveen Vohora, CAChief Executive OfficerRichard Rees, FCABeyond Numbers is printed in British Columbia andmailed eight times annually to more than 9,000chartered accountants and more than 1,600 CA studentsin public practice, industry, education, and governmentservice throughout BC, Canada, and other countries.Beyond Numbers’ editorial and business <strong>of</strong>ficesare located at:Suite 500, One Bentall Centre, 505 Burrard St., Box 22Vancouver, BC V7X 1M4Phone: 604-681-3264Toll-free in BC: 1-800-663-2677Fax: 604-681-1523Internet: www.ica.bc.caOpinions expressed are not necessarilyendorsed by the <strong>Institute</strong>.Beyond Numbers supports the CA pr<strong>of</strong>ession in BCby sharing news from the <strong>Institute</strong> and news aboutmembers, by sharing viewpoints on issues <strong>of</strong> specificinterest to members, and by promoting memberinvolvement in <strong>Institute</strong> activities.Publications Mail Agreement No: 40062742Notes from the PresidentWhen I started my presidential term in June 2008, I waslooking <strong>for</strong>ward to leading the <strong>Institute</strong> during a time <strong>of</strong> great change. I wasn’tdisappointed. To begin with, I am walking away with an appreciation <strong>for</strong> howpr<strong>of</strong>essionally the <strong>Institute</strong> is run—everything, and I mean everything, is wellplanned and thought out, from events like convocation and the Executive Tourto more ad hoc, time-sensitive events such as those relating to regulatoryissues.Having served on Council <strong>for</strong> nine years, I’ve come to appreciate the fact thatsignificant change can’t be made overnight, as issues tend to be far morecomplex than they might seem at first. So it was particularly gratifying to seethe implementation <strong>of</strong> expanded training opportunities <strong>for</strong> students, and to playa part in reengineering our complicated regulatory processes to make themmore transparent and ensure that they are best practices. I also saw atremendous ef<strong>for</strong>t go into providing excellent PD courses in response to theincreased CPD requirements and the changes in accounting and auditing rules.I can assure you that our <strong>Institute</strong> is responsive to change, takes a long-termview, and strives to get it right. I can also assure you that the Canadian CApr<strong>of</strong>ession continues to make big strides in harmonizing processes andimproving efficiencies.During the Executive Tour, I was very pleased to see so many members—especially young members—attend the various stops across BC anddemonstrate their keen interest in the evolution <strong>of</strong> our accounting standards.With over 1,600 members signed up <strong>for</strong> our free PD sessions on new standardsin May and June, it’s clear that members are engaged.Finally, I have to say that I’m impressed with the ability <strong>of</strong> <strong>Institute</strong> staff towork so well with an ever-changing roster <strong>of</strong> volunteers. Volunteers are treatedwith the utmost respect, as staff members honestly seek their views and make ahuge ef<strong>for</strong>t to provide comprehensive background in<strong>for</strong>mation to assist in thedecision-making process. And <strong>of</strong> course, I’m impressed with the volunteersthemselves, who give so much <strong>of</strong> their time, and <strong>of</strong>fer such value to <strong>Institute</strong>initiatives. Thank you <strong>for</strong> all that you do!I also thank Council and the <strong>Institute</strong> staff—Richard Rees in particular—<strong>for</strong> theirsupport this past year, and their wisdom. It has been an illuminating andenjoyable experience, and I wish the same <strong>for</strong> my successor, your new presidentKaren Keilty, FCA.—Doug Murphy, FCA4 ica.bc.ca June/Summer ’09

For the Pr<strong>of</strong>essionLong AwaitedPrivate EnterpriseGAAP Is Here!By Amy Lam, CASenior Director <strong>of</strong> MemberServicesAs detailed in CAmagazine’s May 2009cover story, the Accounting StandardsBoard (AcSB) recently issued an ExposureDraft on generally accepted accountingprinciples <strong>for</strong> private enterprises. In the ExposureDraft, the AcSB proposes a set <strong>of</strong> stand-alonestandards that would be available <strong>for</strong> use by allprivate enterprises. Private enterprises would alsohave the choice <strong>of</strong> using international financialreporting standards.The proposed standards <strong>for</strong> private enterpriseswould be effective <strong>for</strong> annual financial statementsrelating to fiscal years beginning on or afterJanuary 1, 2011, but early adoption would bepermitted. The AcSB expects that the finalstandards will be issued in time to permit their use<strong>for</strong> 2009 calendar-year end financial statements.In the meantime, parties interested in providingfeedback on the Exposure Draft are invited tosend written comments to the AcSB by July 31,2009.Basic approachThis exposure draft is the culmination <strong>of</strong> approximatelythree years <strong>of</strong> research, consultationwith stakeholders, and deliberation by the AcSB.During the consultation process, stakeholders toldthe AcSB that standards <strong>for</strong> private enterprisesneed to be developed in a timely manner. Inorder to do this, the AcSB used the existingCICA Handbook as a starting point as it set aboutdeveloping a set <strong>of</strong> principles-based standards.The AcSB retained a significant number <strong>of</strong>recognition and measurement requirements—those it determined would not cause substantiveconcern <strong>for</strong> private enterprises—and removedcertain sections and guidelines deemed irrelevant<strong>for</strong> this sector. The AcSB also reconsideredthose issues in the Handbook identified assignificantly problematic <strong>for</strong> private enterprises,and the proposed alternatives are highlighted inthe Exposure Draft.In addition, the AcSB re-examined existingdisclosure requirements to focus on the needs<strong>of</strong> private company financial statement users,recognizing that users in this sector generallyhave the ability to obtain additional in<strong>for</strong>mationfrom the enterprises in question.Proposals – recognition andmeasurementThe Exposure Draft includes proposed changesto the existing recognition and measurementrequirements. These proposed changes can becategorized into three general categories: significantchanges, moderate changes, and no changes.Significant changes:The Exposure Draft proposes significant changesto the existing recognition and measurementrequirements in the following areas:• Financial instruments;• Employee future benefits;• Asset retirement obligations;• Internally developed intangible assets;• Impairment testing <strong>for</strong> goodwill and otherintangible assets; and• Stock-based compensation.The most significant <strong>of</strong> these changes <strong>for</strong> themajority <strong>of</strong> private enterprises is the proposedfinancial instruments standard, which wouldprovide <strong>for</strong> a much simpler approach than thatset out in section 3855 <strong>of</strong> the Handbook.Moderate changes:The Exposure Draft proposes moderate changesto the following:• Future income taxes; and• Investments (subsidiaries, significantly influencedinvestees, and joint ventures).Differential reporting options are being incorporatedin these two sections. Because thesedifferential reporting options already exist in thecurrent Handbook, the changes are expected tohave only a moderate impact.No changes:The Exposure Draft proposes that no changes bemade to the following:• Leases; and• Callable debt (EIC 122).Private enterprises planning to adopt thisproposed set <strong>of</strong> standards need to review theproposals first and assess the impact <strong>of</strong> thesechanges on their operations and financial reporting.Disclosure requirementsOne <strong>of</strong> the goals in developing the proposedstandards <strong>for</strong> private enterprises is to reduce thenumber <strong>of</strong> specific disclosure requirementswhile, at the same time, providing sufficientin<strong>for</strong>mation to give a fair presentation <strong>of</strong> anenterprise’s financial position and operatingresults, and to help users gauge when to ask<strong>for</strong> further in<strong>for</strong>mation on specific issues ortransactions.Users <strong>of</strong> private enterprise financial statementshave stated that disclosures on accountingpolicies, risks and uncertainties, and unusualevents are vital when it comes to understandingand analysing financial statements. In focusingon these users and their needs, the AcSB haseffectively reduced the number <strong>of</strong> disclosurerequirements by about half.In the Exposure Draft, the AcSB added twonew disclosure requirements viewed as importantby users in the private enterprise sector: thedisclosure <strong>of</strong> the amount payable at the end <strong>of</strong>the period in respect <strong>of</strong> government remittances(and whether any such remittances are in arrears)and the compensation <strong>of</strong> key management personnelas a group.EIC abstractsIn creating a principles-based financial reportingsystem, the AcSB concluded that it would notbe appropriate to include the type <strong>of</strong> detailedguidance contained in the EIC Abstracts;there<strong>for</strong>e, abstracts have been excluded from theproposed standards. However, some abstracts docontain guidance that is important to this sector;accordingly, this guidance was incorporated intothe appropriate sections <strong>of</strong> the proposed standards.Share your feedbackIf or when finalized as standards, the proposalscontained in the Exposure Draft will have ahuge impact on financial reporting by privateenterprises. This being the case, it is vitallyimportant that stakeholders in this sector weighin with comments, suggestions, and/or concerns.A copy <strong>of</strong> the Exposure Draft is now available atwww.acsbcanada.org/edpegaap.Access the Exposure Draft onGAAP <strong>for</strong> private enterprisesat www.acsbcanada.org/edpegaap.June/Summer ’09 ica.bc.ca 5

Research CornerThe UncertainNature <strong>of</strong> UniversityResearchBy Dr. Kin Lo, CA, Ph.D.While researchers do have specific goals<strong>for</strong> their research programs, those goalsdo not define or limit the eventual impact<strong>of</strong> the researchOver the last few months, I have readseveral books on topics ranging fromneurology and cognition to geneticsand evolution. Each one has been fascinating inits own right, but even more so were the ideasand concepts that transcended these fields,particularly those that reached into accounting,business, and economics.In particular, the intersection <strong>of</strong> neurology andaccounting is currently spawning an intriguingline <strong>of</strong> research I would have considered a mereflight <strong>of</strong> fancy only a few months ago. For example,soon after reading Predictably Irrational, 1 inwhich a pr<strong>of</strong>essor with over 20 years <strong>of</strong> researchin behavioural economics explains why peopletend to behave irrationally in predictable ways,and How We Decide, 2 which examines thebrain’s various roles in the decision-makingprocess, I had the opportunity to attend aworkshop entitled “NeuroAccounting,” givenby Pr<strong>of</strong>essor Greg Waymire 3 from EmoryUniversity in Atlanta, Georgia. Another exampleis The Geography <strong>of</strong> Thought: How Asians andWesterners Think Differently...and Why, in whicha pr<strong>of</strong>essor <strong>of</strong> social psychology discusses theinter-dependent development <strong>of</strong> culture, language,and thought processes. 4 Importantly, the bookhighlights the significant differences that havearisen between the “East” and “West” in terms<strong>of</strong> how people think. These differences certainlyhave implications <strong>for</strong> evaluating the appropriateness<strong>of</strong> uni<strong>for</strong>m global accounting standardsand how we educate students with diversecultural backgrounds.A fourth example involves many ideas in The Selfish Gene, 5 which have had similar applications inbusiness. Many readers are likely to be familiar with the idea <strong>of</strong> “economic Darwinism”—or survival <strong>of</strong>the fittest in terms <strong>of</strong> businesses, products, and practices; but research is revealing that there are manymore such commonalities.Consider, <strong>for</strong> example, the well-known “prisoner’s dilemma” in mathematical game theory, whichhas remarkable applications <strong>for</strong> the understanding <strong>of</strong> business competition as well <strong>for</strong> the prediction <strong>of</strong>animal behaviour and evolutionary development. Another idea is that organisms are merely “vehicles”that carry “replicators” called genes—an idea largely equivalent to the notion that a business/firm is justa “nexus <strong>of</strong> contracts” among individuals. As explained in The Selfish Gene, successful genes are thosethat are able to continue replicating <strong>for</strong> many generations by programming useful functions <strong>for</strong> theorganism in the context <strong>of</strong> the organism’s other genes and environmental conditions. Genes that donot cooperate with other genes in the same vehicle lead to the death and end <strong>of</strong> the replicator. Theanalogy to individuals in business organizations should be clear.My recent readings highlight the highly unpredictable nature <strong>of</strong> scientific research. While researchersdo have specific goals <strong>for</strong> their research programs, those goals do not define or limit the eventual impact<strong>of</strong> the research. However, many who are not familiar with research do not understand the randomnature <strong>of</strong> research output. Among them are the key policy makers in the current federal government,as demonstrated in a series <strong>of</strong> decisions in the last two years:• The 2008 federal budget cut $148 million from the three federal research councils over three years,at a time when the federal government is attempting to stimulate the economy. 6• Instead <strong>of</strong> using peer review, the Minister <strong>of</strong> Industry will now identify the projects that will receivepriority funding from the Canadian Foundation <strong>for</strong> Innovation.• The 2009 federal budget allocated $87.5 million from the budget <strong>of</strong> the Social Science andHumanities Research Council <strong>for</strong> graduate scholarships solely <strong>for</strong> candidates who are pursuingbusiness-related degrees.1Daniel Ariely, Predictably Irrational, HarperCollins 2008. Ariely is the James B. Duke Pr<strong>of</strong>essor <strong>of</strong>Behavioural Economics at Duke University in North Carolina and a visiting pr<strong>of</strong>essor at theMassachusetts <strong>Institute</strong> <strong>of</strong> Technology.2Jonah Lehrer, How We Decide, Houghton Mifflin Harcourt 2009.3Pr<strong>of</strong>essor Waymire’s current research focuses the history <strong>of</strong> accounting measurement anddisclosure.4Richard Nisbett, The Geography <strong>of</strong> Thought, Free Press, 2003. Nisbett is the Theodore M.Newcomb Distinguished Pr<strong>of</strong>essor <strong>of</strong> social psychology and co-director <strong>of</strong> the Culture andCognition program at the University <strong>of</strong> Michigan.5Richard Dawkins, The Selfish Gene, 30th anniversary edition, 2006.6The three research councils are the Natural Sciences and Engineering Research Council <strong>of</strong> Canada,the Social Sciences and Humanities Research Council <strong>of</strong> Canada, and the Canadian <strong>Institute</strong>s <strong>for</strong>Health Research.6 ica.bc.ca June/Summer ’09

As someone working in a business school, Ishould probably applaud this last policy, but as amatter <strong>of</strong> principle, targeted funding is misguidedand short-sighted, as I believe I have illustratedabove.Much research is highly technical and noteasily penetrable <strong>for</strong> non-academics. Consequently,the use <strong>of</strong> peer review to allocate funds is anecessary and effective means <strong>of</strong> identifying theresearch that is worthy <strong>of</strong> funding. As both arecipient <strong>of</strong> these funds and a reviewer <strong>of</strong> others’applications, I can attest to the thoroughness <strong>of</strong>the peer review process. The outcome <strong>of</strong> thisprocess is that only one third <strong>of</strong> all applicationsare accepted—a far cry from the seemingmisperception that every research proposalreceives public funding. 7The alternative—letting politicians and bureaucratsmake these choices—is a recipe <strong>for</strong> failure,as far as I’m concerned, especially when I thinkabout the choices that might be made by ourMinister <strong>of</strong> State <strong>for</strong> Science and Technology,Gary Goodyear, whose remarks in March <strong>of</strong> thisyear suggest that he does not understand thegenetic science behind the theory <strong>of</strong> evolution.I believe the research granting system that hasbeen in place in Canada is a good one. Thegranting councils serve as a marketplace <strong>for</strong> ideasthat compete with other ideas. Each applicationis adjudicated by knowledgeable peers—theconsumers <strong>of</strong> that research, in a sense. There isno doubt that this approach is superior to acentrally controlled system in which one entitydirects thousands <strong>of</strong> researchers across the country.To rein<strong>for</strong>ce my point about the interconnectedness<strong>of</strong> ideas, let me approach it from adifferent angle: How do we explain the origin <strong>of</strong>species and the diversity <strong>of</strong> life on earth? Is itthe result <strong>of</strong> evolutionary trial and error orintelligent design, which requires an omnipotentdesigner? And what arrogance must an individualhave to think they alone can handle the role <strong>of</strong>the designer?Whether we use the analogy <strong>of</strong> capitalism vs.central planning or evolution vs. intelligentdesign <strong>for</strong> university research funding, I believethe evidence is overwhelming and the choice clear.Helping future CAsHave you ever wondered how you could help students who are interested inbecoming members <strong>of</strong> our proud pr<strong>of</strong>ession? Consider donating to the CAEducation Foundation (CAEF).The CAEF is a registered charity established by the BC <strong>Institute</strong> <strong>of</strong> CAs in1990 to support the endeavours <strong>of</strong> current and future CAs.One <strong>of</strong> the Foundation’s important activities is to ensure that scholarshipsare available to students at every university and college in BC. The 25scholarships currently available each year are administered either directlyby the universities or by the CAEF itself. Some <strong>of</strong> these scholarships helpstudents with financial need; others recognize academic excellence and/orleadership; all go to students who’ve indicated their intentions to become CAs.There are different ways to donate:• General donations – Mail, fax, or drop <strong>of</strong>f a donation at the <strong>ICABC</strong>’s<strong>of</strong>fices in downtown Vancouver. (Did you know that many <strong>of</strong> our Pr<strong>of</strong>essionalDevelopment Program instructors donate their fees?)• Planned giving – Consider naming the CAEF as a beneficiary in your will.This legacy could be a fixed sum or estate residue. Alternatively, youcould name the CAEF as a primary or secondary beneficiary <strong>of</strong> an annuity,RRSP, or other financial instrument <strong>of</strong> your estate.• Giving in memoriam – The CAEF was originally set up as the <strong>Institute</strong>’sMemorial Scholarship Fund in 1969/70, when colleagues and familymembers <strong>of</strong> Desmond O’Brien, CA, sought to acknowledge and maintainhis contributions to the pr<strong>of</strong>ession. This tradition has continued, withmany such gifts being made over the past 30+ years.• Matching Scholarship Program <strong>for</strong> CA firms and associations – The CAEFhas set aside funds to encourage a matching program <strong>for</strong> CA firms andassociations in order to fund new scholarships at educational institutionsthroughout BC.Please visit the CA Education Foundation’s website at www.caef.bc.ca <strong>for</strong>more in<strong>for</strong>mation about past donors, a listing <strong>of</strong> our most recent scholarshipwinners, and a summary <strong>of</strong> the other valuable activities undertaken by theCAEF each year.Kin Lo, CA, Ph.D., holds the CA Pr<strong>of</strong>essorship inAccounting in the Sauder School <strong>of</strong> Business atUBC. The CA Pr<strong>of</strong>essorship is funded by the CAEducation Foundation <strong>of</strong> BC. Send your questionson accounting research to Kin at kin.lo@sauder.ubc.ca.7Gwyn Morgan, “Not all research deservespublic funding,” Globe and Mail, April 27,2009.June/Summer ’09 ica.bc.ca 7

On the Cover<strong>Early</strong> <strong>Achievement</strong> Award WinnersBy Michelle McRae, EditorEach year, the <strong>Institute</strong> grants awards <strong>for</strong> early achievement to CAs who have made significant pr<strong>of</strong>essionalaccomplishments and community contributions within ten years <strong>of</strong> earning the CA designation. Three CAshave been chosen <strong>for</strong> this year’s awards: Lenora Lee, CA; Mike Parker, CA; and Nolan Watson, CA.Lenora Lee, CALenora Lee is a very busy individual. In additionto managing a full client load, the seniormanager at KPMG LLP in Victoria oversees andparticipates in her firm’s recruiting activities,teaches at the University <strong>of</strong> Victoria, and volunteersextensively in the community.It’s hard to believe she earned her CA only fouryears ago.Lenora began articling with KPMG in 2002,after completing a bachelor <strong>of</strong> commerce fromthe University <strong>of</strong> Victoria (along the way, earninga Faculty <strong>of</strong> Business Award <strong>of</strong> Excellence <strong>for</strong>having the highest GPA).“When I began articling, I was aware <strong>of</strong> thestereotypes regarding accountants,” Lenora remembers.“But soon after starting, I was happy todiscover that every day is dynamic and unique.”After earning her CA in 2005, she stayed onwith KPMG as a manager. Partners and clientsalike were impressed with her abilities. Theywere so impressed, in fact, that the firm decidedto promote her to senior manager in 2007—twoyears ahead <strong>of</strong> the typical schedule.Lenora has risen to the task, taking on a high level<strong>of</strong> responsibility that includes a considerable anddiverse client roster.“Maintaining this client mix requires me tocontinue learning about different businesses andthe applicable accounting standards,” she says.“I’ve worked with fantastic clients in a variety <strong>of</strong>industries so far, and I’ve found it particularlyrewarding to gain such a breadth <strong>of</strong> knowledgeand experience.”Lenora also manages the firm’s recruitmentprogram in Victoria, and says she “enjoys stayingconnected with local post-secondary institutionsand seeing new students join the firm each year.”So far, she has played a major role in the hiring<strong>of</strong> approximately 40 students.She also participates as a speaker at panels and<strong>for</strong>ums on post-secondary education, speakingto secondary and post-secondary students about8 ica.bc.ca June/Summer ’09

P L A T I N U M M E M B E R“I’ve worked with fantastic clients in a variety <strong>of</strong> industries so far, and I’ve found it particularly rewarding to gain such a breadth <strong>of</strong>knowledge and experience,” says Lenora Lee, CA. Photo by Deddeda Stemler <strong>of</strong> Victoria.09.OBRTurnbullAd4 5/21/09 9:15 AM Page 1Disciplined InvestmentManagementRoss Turnbull, CA, CBV, CFADirector, Portfolio Manager604 844 5363Toll Free 1 888 886 3586rturnbull@odlumbrown.comMEMBER CIPFThe OB Report is Odlum Brown’s monthly newsletter featuringtimely market commentary and insight into our investmentstrategies. To receive a complimentary copy, call 604 844 5363.June/Summer ’09 ica.bc.ca 9

career opportunities <strong>for</strong> CAs.“The recruiting and teaching aspects <strong>of</strong> mycareer have been particularly rewarding as well,”Lenora says. “I’ve worked with many teachers,all with different backgrounds, who’ve sharedtheir experiences with me and taught me atremendous amount about all aspects <strong>of</strong>business. I appreciate the time and patience thatothers spent with me as an articling student, andI hope to pass this same philosophy on to others.”Accordingly, she serves as a mentor to herfirm’s students, guiding them through the entireCASB experience, from Module 1 registrationto UFE prep.“The time I spend with our articling studentswill help them learn new skills and knowledge,which, in turn, will help them become successful,”she says. “Celebrating with them when they earntheir designations is always one <strong>of</strong> the highlights<strong>of</strong> the year—there’s so much excitement as theyget ready to start their careers as new CAs.”If that weren’t enough, in 2008, Lenorabecame a sessional instructor with her almamater, teaching financial and managementaccounting <strong>for</strong> specialists. She is also deeplyinvolved in the community.“Community service is an opportunity <strong>for</strong> meto give back to all the organizations that haveshaped me as a person,” she says.A member <strong>of</strong> the executive <strong>of</strong> the AlumniAssociation <strong>for</strong> the Faculty <strong>of</strong> Business at UVic<strong>for</strong> the past seven years, Lenora helped organizethe Association’s launch and continues to helpwith networking events while also serving as theAssociation’s secretary-treasurer. She is alsoan active member <strong>of</strong> the Victoria ChineseCommerce Association, a cross-cultural businessassociation that promotes business growthwithin Victoria and facilitates Chinese andCanadian commercial enterprise.In 2008, Lenora participated as a communityleader in the Minerva Foundation’s Victoria“Follow a Leader” program, which pairsemerging leaders with ten established leaders<strong>for</strong> training workshops and job-shadowingopportunities. And during a term as a member<strong>of</strong> the Victoria Foundation’s Community Fundand Arts and Heritage Committee, she hasreviewed and communicated on financial-relatedmatters, screened Fund applicants, and maderecommendations on grant recipients.“I believe it’s my responsibility to give back toorganizations that do so much with limitedresources and recognition,” she says. “If I cancontribute time, knowledge, or resources to helpan organization that would not otherwise beable to operate as successfully, I will gladly doso.”As <strong>for</strong> her <strong>Early</strong> <strong>Achievement</strong> Award? Lenora ismindful <strong>of</strong> those who’ve helped her get so far insuch a short time.“This award is not something I could haveobtained without the support <strong>of</strong> all those I’veworked with throughout my career,” she says.“Many mentors have taken time out <strong>of</strong> very busyschedules to teach me, and they’ve helped me tobe successful. I thank them <strong>for</strong> providing mewith opportunities to be challenged and <strong>for</strong>having confidence in my abilities. I’m grateful aswell <strong>for</strong> the many family members and friendswho have supported me during my educationand career.”Looking ahead, Lenora is looking <strong>for</strong>ward totravelling and enjoying quality time with friendsat a number <strong>of</strong> upcoming weddings. When itcomes to the long-term, she says simply: “I look<strong>for</strong>ward to more challenges, opportunities, andlifelong learning.”<strong>ICABC</strong> Benevolent Fund <strong>of</strong>fersfinancial support to members in needAll in<strong>for</strong>mation is held in the strictest confidenceTo apply <strong>for</strong> financial assistance, contact:Amy Lam, CASenior Director <strong>of</strong> Member Services & Fund SecretaryPhone: 604-488-2629Toll Free: 1-800-663-2677Email: lam@ica.bc.ca10 ica.bc.ca June/Summer ’09

Michael D. H. Parker, CAWhen Mike Parker graduated from high schoolin Terrace in 1991, he knew one thing <strong>for</strong>certain: The best way to protect himself in adifficult economy would be to build a strongskill set. He has continued building on his skillset ever since.Today, Mike is the partner in charge <strong>of</strong> taxationadvisory services at Daley & Company LLP<strong>Chartered</strong> Accountants, the largest independentfirm in Kamloops.No one is more surprised than he that publicpractice has become his niche.In 1995, Mike was a 22-year-old working ona bachelor <strong>of</strong> commerce at the University <strong>of</strong>Victoria, majoring in entrepreneurship, when hegot an exciting opportunity to start his ownbusiness as a retail/wholesale specialty c<strong>of</strong>feeimporter. Eager <strong>for</strong> the challenge, Mike put hisundergraduate studies on hold to open andmanage GroundWorks C<strong>of</strong>fee Co. He oversawthe entire operation from conception, includingfinancing, construction, and operations management.“Terrace had been under-exploited in terms <strong>of</strong>specialty c<strong>of</strong>fee, so I saw a real market <strong>for</strong> it,” herecounts. “It ended up being an extraordinarylearning experience. I gained a firsthand understanding<strong>of</strong> the small business retail andwholesale marketplace, and I discovered whatkind <strong>of</strong> <strong>for</strong>titude it takes to be an entrepreneur.”After two years spent working tirelessly to getGroundWorks up and running, Mike decided itwas time to complete his business degree. So hesold his company and went back to schoolfull-time, graduating from UVic in 1999.That same year, he joined the Kamloops <strong>of</strong>fice<strong>of</strong> KPMG LLP in pursuit <strong>of</strong> the CA designation,which he saw as a valuable stepping-stone toa career in industry. Within his first year <strong>of</strong>articling, however, he had a completely newvision <strong>for</strong> his future.“I was shocked to discover how much I enjoyedpublic practice,” he remembers. “I thought Iwould get my CA training and move on, butpublic practice was much more dynamic thanI’d expected. I loved the learning curve, andthere were so many smart, talented people towork with—I actually loved getting up andgoing to work in the morning!”So when Mike qualified as a CA in 2002, hestayed with KPMG, working as a member <strong>of</strong> itstaxation advisory services team and advisingclients on a variety <strong>of</strong> taxation issues. That sameyear, he completed the CICA’s In-Depth TaxCourse.Then in 2005, another pivotal opportunitypresented itself: a partnership <strong>of</strong>fer with Daley“Even while I was articling, I knew I wanted to be a partner—I wanted to be at the front<strong>of</strong> client relationships,” says Mike Parker, CA. Photo by Tyler Meade <strong>of</strong> Tyler MeadePhotography in Kamloops.June/Summer ’09 ica.bc.ca 11

& Company (then Becker Daley LLP).“It was a difficult decision to leave KPMG,” hesays, “but ultimately I saw it as an opportunity Icouldn’t pass up. Even while I was articling, Iknew I wanted to be a partner—I wanted to beat the front <strong>of</strong> client relationships.”Today, he advises a broad range <strong>of</strong> clients onbusiness, accounting, and taxation issues. He’salso in charge <strong>of</strong> his firm’s financial management.“When I first joined Daley & Company, thefirm had no tax department,” he says. “I had theopportunity to lead in its development, andtoday our tax department has four full-timemembers in tax.”In his work with clients, Mike has found hisentrepreneurial background invaluable.“I can really identify with business owners,” hesays. “I’ve experienced what it’s like to be ontheir side <strong>of</strong> things, and I remember what it waslike to work with an accountant and not fullyunderstand what they were telling me. So I havea good understanding <strong>of</strong> my clients’ point <strong>of</strong>view, which helps me give them the in<strong>for</strong>mationthey need to make truly in<strong>for</strong>med decisions.”“I get to know my clients on a personal level,” headds, “and I want to go above and beyond <strong>for</strong>them. As a tax practitioner, that means staying updap_beyondnumbers_jan23.eps 1/26/2009 2:28:16 PMUBC DAPThe gateway to accountingAccelerate your future with the Diploma in AccountingProgram (DAP) at the University <strong>of</strong> British Columbia.to date and continually learning. It’s challenging,but it’s the kind <strong>of</strong> challenge I enjoy. I likebuilding a skill set that is useful and in demand.”That skill set has made him highly desirable inthe community as well. In 2008, Mike wasappointed chair <strong>of</strong> the finance committee <strong>for</strong> theboard <strong>of</strong> governors <strong>of</strong> Thompson Rivers University.Past community service includes serving on theboard <strong>of</strong> directors <strong>of</strong> the Kamloops West RotaryClub and as treasurer on the board <strong>of</strong> directors<strong>of</strong> the Kamloops and District Crime Stoppers.With so much on his plate, Mike is extremelygrateful <strong>for</strong> the love and support <strong>of</strong> family. “Myparents have always supported me,” he says. “Andmy wife, Melanie is very supportive as well.”He and Melanie have a six-year-old daughter,Ellie, <strong>of</strong> whom they are extremely proud. “I tryto spend as much time with her as possible,”Mike says. “It seems like just last week she was atoddler. Time passes so quickly.”This <strong>Early</strong> <strong>Achievement</strong> Award is really justicing on the cake.“The biggest reward,” Mike says, “is that I havea challenging career that I thoroughly enjoy.”DAP prepares university graduates with limited or no training in accounting<strong>for</strong> entry into a pr<strong>of</strong>essional accounting designation. DAP's curriculum isrecognized by the <strong>Chartered</strong> Accountants School <strong>of</strong> Business (CASB)and satisfies most <strong>of</strong> the program requirements.APPLICATION DEADLINESMay start: Mar 1 (International applicants)Apr 1 (Canadian applicants)Sep start: Jul 1 (International applicants)Aug 1 (Canadian applicants)Find out how DAP can accelerate your future: www.sauder.ubc.ca/dapTHE UNIVERSITY OF BRITISH COLUMBIANolan Watson, CA, CFA“The most rewarding part <strong>of</strong> my career has beenthe satisfaction associated with attaining goalsI’ve set <strong>for</strong> myself,” says Nolan Watson. “I tendto ignore the goals that other people set <strong>for</strong> me.I prefer to focus on goals that I believe are bothhighly challenging and attainable.”It’s fair to say that he sets these goals very high.Asked what drives him, he answers: “I’m drivenby an awareness that life is very short, and sinceyou only live once, you had better make itcount.”After earning a bachelor <strong>of</strong> commerce withhonours from the University <strong>of</strong> British Columbiain 2001, Nolan entered the CA program as anarticling student with Deloitte LLP in Vancouver.In 2002, he excelled on the UFE, placing fourthnationally and first in BC, which netted him agold medal and the role <strong>of</strong> valedictorian at the2003 Convocation ceremony.While working with Deloitte, Nolan found avaluable mentor in Glenn Ives, CA, one <strong>of</strong> thefirm’s partners.“Glenn definitely had an impact on my careerdevelopment,” he says. “He was an early rolemodel <strong>for</strong> me who helped me develop a passion<strong>for</strong> client service, as well as an eagerness tochallenge and extend myself.”Nolan qualified as a CA in 2003, and stayedwith Deloitte <strong>for</strong> another two years, workingin the firm’s corporate finance departmentper<strong>for</strong>ming business valuations and merger andacquisition support services. In 2005, he becamea chartered financial analyst charter holder.It was also in 2005 that Nolan left publicpractice to join Silver Wheaton Corp. as itscontroller. He was the company’s first employee.Ian Telfer, the company’s founder, becameanother influential mentor.“The knowledge and experience I obtainedfrom becoming a CA is a critical foundation <strong>for</strong>effective business decision-making,” Nolan says.“Ian has helped me build on that foundation,teaching me a lot about various aspects <strong>of</strong>business, including acquisitions, and aboutmentoring others to help them reach theirpotential.”Nolan was promoted to CFO at the beginning<strong>of</strong> 2006. During his three years with SilverWheaton, Nolan was part <strong>of</strong> the team that listedthe company on the New York Stock Exchange.He subsequently became the youngest CFO <strong>of</strong>an NYSE-listed company, at just 26 years old.By the age <strong>of</strong> 28, he had raised over $1 billion indebt and equity <strong>for</strong> acquisition purposes. Underhis leadership, Silver Wheaton grew from a marketcapitalization <strong>of</strong> $0.3 billion to $3 billion.In 2008, Nolan left Silver Wheaton to become12 ica.bc.ca June/Summer ’09

“I’m driven by an awareness that life is very short, and since you only live once, you had better make it count,” says Nolan Watson, CA.Photo by Kent Kallberg <strong>of</strong> Kent Kallberg Studios Ltd. in Vancouver.the president and CEO <strong>of</strong> a new company,Sandstorm Resources.“I made the move because I wanted to be part<strong>of</strong> building a company from the ground flooragain,” he explains.Listed on the TSX-V, the company is lookingto build a metal-streaming business plan similarto that <strong>of</strong> Silver Wheaton, but in metals otherthan silver. In April 2009 alone, Nolan raised$47 million <strong>for</strong> the company.In addition to his role at Sandstorm Resources,Nolan currently serves as a director <strong>of</strong> anotherTSX-V listed company, Gold Wheaton GoldCorp., another company founded by his mentorIan Telfer.Nevertheless, Nolan downplays his accomplishments,saying: “To be candid, I’m notoverly impressed with my accomplishments yet.”This, despite the fact that he was named toBusiness in Vancouver’s Top 40 under 40 list in2006, and voted one <strong>of</strong> the most motivatedCFAs in the world by CFA Magazine in 2008.Asked what has been most challenging so far inhis career, Nolan says, “ensuring that my careergoals are consistent with my life goals.”These life goals include making a difference inthe community. Passionate about communitydevelopment, Nolan founded an internationalhumanitarian organization called Nations Cryin 2004. The organization builds schools toprovide education <strong>for</strong> orphans in Sierra Leone,Africa.“Our goal is to provide youth with a sense<strong>of</strong> hope,” he says, “as well as the tools andeducation needed to help them move out <strong>of</strong>poverty and change their lives and the lives<strong>of</strong> their families, as well as helping futuregenerations.”Nolan continues to serve as the president <strong>of</strong>Nations Cry.“I want to make the world a better place,” hesays. “We shouldn’t just focus on doing thosethings that make us feel good, we should als<strong>of</strong>ocus on things that will actually make a permanentdifference, and education is at the top <strong>of</strong>that list.”Another key life goal is making time <strong>for</strong> thosewho matter most.“There is no question that my family, mydaughters, and my wife Dana are the most importantpeople in my life,” Nolan says, addingthat support <strong>of</strong> his loved ones is invaluable.“They ensure that I work towards attaining mypotential, while also keeping me grounded.”June/Summer ’09 ica.bc.ca 13

Community Service Award WinnersBy Michelle McRae, EditorThe <strong>Institute</strong>’s Community Service Award recognizes CAs who’ve gone above and beyond in volunteering their skills<strong>for</strong> the betterment <strong>of</strong> the community. This year’s winners are: Dennis Cojuco, CA; Michael (Mike) Mah, CA; JaimeRoberts, CA; and Cecil Schmidt, CA.Dennis Cojuco,CADennis Cojuco says hemade his first real <strong>for</strong>ayinto volunteerism whileattending the University<strong>of</strong> BC, where he actedas vice-president <strong>of</strong> theFilipino Student Association(FSA), and served as humanitarian projectcoordinator <strong>for</strong> UBC ONE (another studentassociation). With the <strong>for</strong>mer, he led an initiativeto provide support to various soup kitchens inthe Downtown Eastside; with the latter, heorganized fundraising events <strong>for</strong> Sunny HillHealth Centre <strong>for</strong> Children in Vancouver.Then in 1999, Dennis and four friends fromFSA and UBC ONE created Enspire Foundation.They had two primary goals in mind: to supportthe education <strong>of</strong> children living in substandardconditions, and to inspire others to make adifference in the global community.“Growing up in the Philippines, I saw firsthandthe lives <strong>of</strong> those who are less <strong>for</strong>tunate,” saysDennis, who describes Enspire’s mission as“empowering and uplifting through educationand encouragement.”The group began their outreach program byorganizing soup kitchens, hosting severalfundraisers, and <strong>for</strong>ging a partnership with thePag-aalay Ng Puso Foundation (PPF) in thePhilippines. Between 1999 and 2002, they sentfunds, through PPF, to help pay <strong>for</strong> the education<strong>of</strong> children in Navotas, a poverty-stricken city inMetro Manila.In 2002, the Enspire team launched “Resonance,”an annual amateur choir festival and fundraisingevent that features choirs from across the LowerMainland. Enspire’s last six festivals have raisedmore than $62,000—money that has goneoverseas toward the tuition fees <strong>of</strong> indigentstudents in Navotas, and locally to RichmondHigh’s Global Perspectives Program. This moneyalso enabled Enspire to fund and build thefirst stand-alone library in Norzagaray, in thePhilippines’ Bulacan province. Dennis was one<strong>of</strong> 15 Canadians to help build the facility in2006.“After Resonance 2002, we had the idea <strong>of</strong>building a community on land that had beendonated to PPF,” he explains. “The library nowprovides a venue <strong>for</strong> people from nearby regionsto congregate, and it’s conducive to learning <strong>for</strong>local children, including children whose familiesare nomadic and living in the mountains.”Enspire continues to support families in Navotasand help build the community in Norzagaray.In May 2009, Dennis and a group <strong>of</strong> Canadianpr<strong>of</strong>essionals and students (from UBC, SimonFraser University, and Capilano University)helped fund and build the first two homes <strong>of</strong> anew housing community <strong>for</strong> 130 low-incomefamilies.“In the long term, we hope to undertakesimilar projects in other developing countries,”Dennis says. “It’s very rewarding to meet theindividuals who’ve received an education, and tosee them succeed in their chosen careers. Andit’s always rewarding when people tell us they’vefound hope and when we see others give back totheir communities.”Dennis has served as vice-president and adirector <strong>of</strong> Enspire since its inception, and asone <strong>of</strong> the lead event coordinators <strong>for</strong> Resonancesince 2002. He remained committed to theseresponsibilities throughout his articling period,and his commitment has only intensified sincehe became a CA in 2008.“The support provided by my family andfriends, and our volunteers, has given me theextra energy to continue volunteering during thebusiest times,” he says. “It has involved somesacrifices, but it’s all worth it knowing that we’rehelping to improve the lives <strong>of</strong> others.”A senior associate at PricewaterhouseCoopers LLP,Dennis has been recognized as a PwC CanadaFoundation champion <strong>for</strong> his volunteerism.Mike Mah, CAFor the past 56 years,Mike Mah has lived inNanaimo. It’s a long wayfrom his birthplace—asmall village in the province<strong>of</strong> Guangdong, inChina, which his familyfled in 1949 in search <strong>of</strong> a better life. After fouryears in Hong Kong, the family immigrated toCanada. Already home to Mike’s paternalgrandparents, Nanaimo was the obvious choice.“Life has been very good to me here,” he says.“Especially coming from the old country… lifehas been very good.”Gratitude is one <strong>of</strong> the reasons <strong>for</strong> Mike’stireless volunteerism in Nanaimo, which extendedthroughout his 38-year career with ChurchPickard & Co., and continued after his retirementas managing partner <strong>of</strong> the firm in 2000.“I feel it’s my duty to give back,” he says.“I want to do my part in making a difference,because there is so much need in the world.”Mike has given back in numerous ways, includingserving as a director and audit committeemember <strong>for</strong> BCAA; as an advisor and director<strong>for</strong> Malaspina International High School; as adirector and treasurer <strong>of</strong> the Nanaimo SymphonySociety; and as a director and <strong>of</strong>ficer <strong>of</strong> both theGreater Nanaimo Chamber <strong>of</strong> Commerce andthe Nanaimo District Hospital Foundation. Forthe latter, he also served as president.For the CA pr<strong>of</strong>ession, Mike chaired the<strong>ICABC</strong>’s Annual Conference Committee in1977, and served as one <strong>of</strong> its members in the1980s. In the 1970s, he also served as the firstpresident <strong>of</strong> the Nanaimo CA Association.“We called our first social event the ‘T4 Frolic,’”he laughs. “It was a lot <strong>of</strong> fun. The CA clubreally <strong>of</strong>fered a chance <strong>for</strong> members in our areato come together.”A long-time charter member <strong>of</strong> the NanaimoNorth Rotary Club, Mike was recognized asRotarian <strong>of</strong> the Year in 1979. He served as Clubpresident in 1983, and led a successful initiativein 1995 to have women members admitted tohis Rotary Club.14 ica.bc.ca June/Summer ’09

Deeply committed to helping immigrants inhis community, Mike worked with the CathaySenior Citizens Housing Society to providehousing <strong>for</strong> residents displaced by a fire thatdestroyed Nanaimo’s entire Chinatown districtin 1960. With the Chinese Memorial Society, hehelped raise funds to restore a neglected Chinesecemetery; on completion <strong>of</strong> the reconstruction,this cemetery was donated to the City <strong>for</strong> publicuse. Mike also helped establish a garden commemoratingthe area’s Chinese pioneers.In 1999, the City recognized his myriad ef<strong>for</strong>tswith a Certificate <strong>of</strong> Recognition.Today, Mike is a committee member <strong>of</strong> theNanaimo Dragonboat Festival Society, whichhe helped to establish. The Society raises fundsto donate to the Nanaimo Regional GeneralHospital <strong>for</strong> the purchase <strong>of</strong> breast cancerdiagnostic equipment. He is also the currentpresident <strong>of</strong> the Nanaimo Chinese CulturalSociety.“Volunteering has brought me a lot <strong>of</strong> joy andsome wonderful friendships,” Mike says. “I’msure I have gained more than I have given.”Jaime Roberts,CAJaime Roberts has participatedin Victoria-areasoccer programs since1996, when she moved toVictoria from her hometown<strong>of</strong> Campbell River(where her father DennisBerntson, CA, is a public practitioner) to attendthe University <strong>of</strong> Victoria. Over the past 13years, Jaime has contributed to the BC GovernmentEmployees Co-Ed Soccer Society as aplayer and a team manager, has competed intwo women’s summer leagues, and has coacheda local girls team. But her most extensiveinvolvement has been with the Gordon HeadSoccer Association (GHSA), a community-basedsoccer club with approximately 1,200 members.Jaime was invited to join the club’s board <strong>of</strong>directors as treasurer in 2004, shortly after shequalified as a CA.“I’d enjoyed the benefits <strong>of</strong> being a player withthe club <strong>for</strong> approximately eight years at thatpoint, so it seemed only reasonable that I shouldgive something back,” Jaime remembers. “Also,I’d just taken a job as controller <strong>of</strong> the VictoriaGolf Club, and I thought the added hands-onaccounting and board experience I would get frombeing treasurer at GHSA would be beneficial inmy new job.”After serving as treasurer <strong>for</strong> three years, Jaimedidn’t step down from the board—instead, shetransitioned into a new role as the club’s volunteercoordinator. With only a handful <strong>of</strong> peoplevolunteering in the club’s day-to-day operationsat the time, the workload was becomingdifficult to manage. In her new role, Jaime wastasked with increasing the number <strong>of</strong> volunteersand linking them to jobs.One <strong>of</strong> her first coups was to recruit RichardHalliburton, CA, the father <strong>of</strong> two childrenin the GHSA program, to serve as the board’snew treasurer. Many other calls, however, wentunanswered. So Jaime helped the boardimplement a new participation fee and policy inan ef<strong>for</strong>t to turn things around.As a result <strong>of</strong> this new, <strong>for</strong>mal policy, volunteerparticipation is up dramatically. In addition toredistributing the workload, this increasedinvolvement has helped keep costs down,making the club more af<strong>for</strong>dable and accessible<strong>for</strong> kids in the community.Jaime’s many other contributions to theGHSA include serving as team coordinator <strong>of</strong>the Division 2 Women’s team since 2007, andhelping with everything from funding and grantapplications to facilities usage and communications.In 2008, she also helped the club’sFundraising Committee raise $85,000 towardbuilding an $800,000 artificial turf soccer field.“I’ve enjoyed seeing these things happen,”Jaime says. “And I’ve enjoyed meeting all <strong>of</strong> thedifferent people at the GHSA. This experiencehas given me a greater appreciation <strong>for</strong> what ittakes to make a club like this run smoothly. Ihave a lot <strong>of</strong> respect <strong>for</strong> the dedication <strong>of</strong> everycoach, manager, board member, and volunteer—theyare the heart <strong>of</strong> these organizations.”Since joining BC Ferries as a senior financial analystin 2006, Jaime has participated in the BCFerry Employees Community Breakfast program,which provides hot meals to the homeless severaltimes per year.Cecil Schmidt,BA, CACecil Schmidt has beenan active volunteer inthe Vernon Community<strong>for</strong> more than 40 years.His dedication is attributable,in large part, tothe example set by hisparents. As a young boy growing up in thePrairies in the 1930s and ’40s, Cecil watched hisparents eke out a living farming on rented landand working <strong>for</strong> others.“They never had much <strong>of</strong> a chance,” he says,“but they were determined to provide a bettereducation <strong>for</strong> their family.”In tenth grade, Cecil’s parents sent him to aboarding school run by Benedictine monks. Themonks, he says, “provided excellent teachingand character building,” and their dedication toservice made a lasting impression.Cecil initially pursued social work as a career,but shifted his focus to accounting after movingto Calgary and entering a five-year studentprogram with what was then Collins & Collins.In 1968, he accepted an invitation to moveto Vernon and work with the same firm,which later became Collins Barrow (now BDODunwoody LLP). He retired from the firm’spartnership 20 years ago, and from the <strong>of</strong>fice 15years ago.One <strong>of</strong> the first clients with whom Cecilworked was the Vernon & District Association<strong>for</strong> the Mentally Handicapped. This provedpivotal, he says, as it introduced him tolocal-area charities. He is still involved with theAssociation, and his 30+ years <strong>of</strong> service haveincluded acting as president <strong>for</strong> one term and astreasurer <strong>for</strong> several years.Over the years, he has volunteered withmultiple organizations in almost every sector<strong>of</strong> Vernon life. These include the Vernon &District Per<strong>for</strong>ming Arts Centre (foundingmember), the North Okanagan CommunityConcert Association, the Vernon Curling Club(now a life member), the North Okanagan CAAssociation (<strong>for</strong> which he served as presidentfrom 1985 to 1987), the United Way, theVernon & District Immigration Services Society(VDISS), and the Boys and Girls Club.In addition, Cecil is an active member <strong>of</strong> St.James Catholic Church, and has served as amember <strong>of</strong> the church’s finance committee. Healso served on the board <strong>of</strong> St. James School, andserved as president <strong>for</strong> one term. Today, he continuesto serve as a lay assistant at Sundaycontinued on page 37June/Summer ’09 ica.bc.ca 15

Ritchie W. McCloy Award <strong>for</strong> CAVolunteerism Goes to Susan K. BurnsBy Michelle McRae, EditorThe Ritchie W. McCloy Award <strong>for</strong> CA Volunteerism recognizes the value <strong>of</strong> a CA or non-CA’s contributions to the CA pr<strong>of</strong>ession, whether through an individualproject or a series <strong>of</strong> activities. In addition to their dedication to the pr<strong>of</strong>ession, award recipients must embody values such as openness, honesty, and generosity.If Susan Burns looksfamiliar, it’s probablybecause you’veseen her face in BeyondNumbers be<strong>for</strong>e—severaltimes in fact, becauseSusan served as a publicrepresentative on the<strong>Institute</strong>’s Council <strong>for</strong>seven years, contributing time and energy to thebetterment <strong>of</strong> the CA pr<strong>of</strong>ession.Susan was invited to join Council in 2001, thefinal year be<strong>for</strong>e the provincial governmentbegan appointing public representatives. She’dbeen brought to the attention <strong>of</strong> Council byReverend Bob Burrows, CA (Hon), who wasthen serving as a public representative himself.The two had a long-standing connectionthrough volunteerism.“There was a vacancy <strong>for</strong> a public rep andcouncil members were encouraged to suggestnames,” Bob recalls. “I had just learned thatSusan was stepping down from her positionwith the SFU Executive MBA Program. Havingworked with her on various committees andprojects, I believed she would make a greatcontribution to the <strong>ICABC</strong>. I am sure the<strong>Institute</strong> and the general public have benefitedenormously from her remarkable gifts duringthe past several years.”In joining Council, Susan was motivated bythe same impetus that has driven her involvementwith every organization: to help others effectand manage change.“I have an abiding passion <strong>for</strong> sound publicpolicy,” she told us back in 2005. “On Council,I try always to ask the question: ‘What is reallyin the best interest <strong>of</strong> the public?’”Look back now on her experience, Susanexplains why she stayed involved with Council<strong>for</strong> more than a full term.“Council was engaged in so many seminaland interesting issues—issues such as education,good governance, strategic planning, and harmonization,”she says. “It was fascinating to seeand be a part <strong>of</strong> this process. And in terms <strong>of</strong> thelevel <strong>of</strong> operation, I’d never seen an organizationso well run. There is great planning, but also openness to change and innovation.”While serving on Council, Susan also volunteered on the <strong>Institute</strong>’s Recruiting & Training TaskForce and the Task Force on the CA Life Cycle <strong>of</strong> Pr<strong>of</strong>essional Learning, both <strong>of</strong> which set direction<strong>for</strong> the <strong>Institute</strong>, helping to position these issues nationally.Since 2008, the year she stepped down from Council, Susan has been serving on the <strong>Institute</strong>’sDiscipline Tribunal and on the board <strong>of</strong> governors <strong>of</strong> the <strong>Chartered</strong> Accountants Education Foundation.To all <strong>of</strong> these various endeavours, Susan brings a unique perspective, in<strong>for</strong>med by a truly diversebackground. She holds, <strong>for</strong> example, three post-secondary degrees: a bachelor <strong>of</strong> arts in home economicsfrom the University <strong>of</strong> BC (1968); a master <strong>of</strong> science in business administration (majoring in policyanalysis), also from UBC (1981); and a master <strong>of</strong> arts in theological studies from the Vancouver School<strong>of</strong> Theology (2006).Her employment history is equally diverse. Prior to her retirement in 2002, she served <strong>for</strong> 11 years as theexecutive director <strong>of</strong> the Executive MBA Program (EMBA) <strong>for</strong> the Faculty <strong>of</strong> Business Administration atSimon Fraser University (Harbour Centre). During her tenure, she successfully planned and introduceda weekend EMBA program; built a new <strong>of</strong>fice team to manage the two EMBA programs from onedowntown location; initiated curriculum updating and course revision; and managed the applicationreview and credential assessment <strong>of</strong> EMBA applicants.Prior to her role with the EMBA program, Susan worked in a number <strong>of</strong> different fields. This includedworking as a consultant in strategic planning and marketing, providing advice to pr<strong>of</strong>essional organizationsand educational institutions, and as a sessional lecturer <strong>for</strong> both UBC and SFU. At UBC, she also servedas director <strong>of</strong> the real estate division <strong>for</strong> the Faculty <strong>of</strong> Commerce and Business Administration in 1988.Susan’s resume also includes several years with VanCity Savings Credit Union, during which sheserved as manager <strong>of</strong> planning, research, and development, and oversaw the management and administration<strong>of</strong> an 11-person department. Her work be<strong>for</strong>e VanCity included five years on the board <strong>of</strong>examiners with the Canada Land Surveyors, a one-year term as the alderman <strong>of</strong> the City <strong>of</strong> Whitehorse,and a four-year stint as a radio commentator with CBC Radio in the Yukon.Susan’s volunteer activities have been extensive. Prior to volunteering with the <strong>Institute</strong>, she served onthe board <strong>of</strong> directors <strong>of</strong> the Vancouver Chapter <strong>of</strong> the International Society <strong>for</strong> Planning and StrategicManagement, and participated in annual conferences hosted by the EMBA Council.Passionate about her faith, Susan is a past board member <strong>of</strong> the Contemplative Society, an inclusivenon-pr<strong>of</strong>it association that encourages a deepening <strong>of</strong> contemplative prayer, and a past coordinator <strong>of</strong>Living Presence, a centering prayer and spiritual growth group. Her longest-standing commitment,however, has been to the United Church, both at the provincial and national levels. This has includedserving on the executive committee <strong>of</strong> the Division <strong>of</strong> Finance at the national level; as a member <strong>of</strong> theCamping Committee and the Camp Fircom Society; and as chair <strong>of</strong> the Staff Model Review Team <strong>for</strong>the BC Conference Office. She also served <strong>for</strong> many years as a member <strong>of</strong> the <strong>of</strong>ficial board <strong>for</strong>Dunbar Heights United Church. Today, she continues to serve on both the Finance Advisory Counciland the Grants Committee <strong>of</strong> the BC Conference Office.“I’ve been given a lot <strong>of</strong> wonderful opportunities in my life,” Susan says. “Working with the <strong>Institute</strong>is one <strong>of</strong> them. CAs have such integrity—they work so hard, but they also like to have fun. I’ve reallyfound <strong>Institute</strong> volunteers to be a delightful group.”Photo by Vincent L. Chan <strong>of</strong> Invisionation Photography.The Ritchie W. McCloy Award provides a cash prize to the recipient’s charity <strong>of</strong> choice,courtesy <strong>of</strong> the Vancouver Foundation. Susan has chosen the Camp Fircom Society.16 ica.bc.ca June/Summer ’09

NEWthe ABCs <strong>of</strong>A complimentary e-learning course is nowavailable to help you get started on the transitionto International Financial Reporting Standards.This four part on-line program will provide you with thefoundation you need to build your IFRS knowledge. Visit ourdedicated web site and get started today.Your trusted source <strong>for</strong> everything IFRS.www.cica.ca/IFRS1297IFRS ABC ad.indd 110/15/2008 10:19:29 AM

Investing in Regional BC cont’dAccording to the BC Major Projects Inventory (MPI), between September and December 2008, there were 461 major projects proposed in BC and 370underway, worth approximately $165.2 billion. 6 Residential/commercial projects accounted <strong>for</strong> 53% <strong>of</strong> all projects cited in the MPI, 7 with the rest <strong>of</strong> theprojects occurring in utilities, transportation and warehousing, public services, energy and mining, manufacturing, and other services. 8Most <strong>of</strong> the projects proposed or underway were concentrated in the Mainland/Southwest, Vancouver Island/Coast, and Thompson-Okanagan DevelopmentRegions. In 2008, these regions accounted <strong>for</strong> almost 70% <strong>of</strong> all estimated capital costs in BC. 9Incorporations and bankruptciesBC’s business incorporations rose steadily between 2003 and 2007, but declined in 2008 as investor and entrepreneurial confidence wavered in the face <strong>of</strong> asharp economic recession. Last year, all <strong>of</strong> the Development Regions except the North Coast saw a decline in the number <strong>of</strong> business incorporations, withthe provincial average decreasing by 11.6%. Such a sharp downturn reflects a more pessimistic investment climate than we’ve seen in several years. The greatestdeclines in business incorporations occurred in the Northeast (-18.1%) and Mainland/Southwest (-12.6%) Development Regions.In 2008, the only gain in the province occurred in the North Coast, where business incorporations rose by 1.9%, as a number <strong>of</strong> major projects were eitherunderway or pending, and growth occurred in a number <strong>of</strong> service sector industries.Table 3: Business Incorporations in all Development Regions, 2003 to 2008Job Creation (000)5-Year 1-YearRegion 2003 2004 2005 2006 2007 2008 2003-08 2007-08Cariboo 344 428 511 601 560 557 61.9% -0.5%Kootenay 365 450 536 603 730 644 76.4% -11.8%Mainland/Southwest DR 16,930 18,167 22,467 24,114 24,538 21,445 26.7% -12.6%Nechako 99 110 108 137 131 118 19.2% -9.9%North Coast 77 70 88 90 106 108 40.3% 1.9%Northeast 291 377 564 669 542 444 52.6% -18.1%Thompson-Okanagan 1,820 2,039 2,948 3,196 3,446 3,124 71.6% -9.3%Vancouver Island/Coast 2,605 3,062 3,715 3,863 3,983 3,645 39.9% -8.5%British Columbia 22,531 24,703 30,937 33,273 34,036 30,085 33.5% -11.6%Number <strong>of</strong> business establishmentsBetween 2003 and 2008, the number <strong>of</strong> business establishments in BC increased by 22,277, reaching 354,695. However, in 2008, the number <strong>of</strong> businessestablishments declined by 4,619, or 1.3%, reflecting a downturn in business activity that was felt throughout the province.In 2008, the Northeast and Nechako Development Regions experienced the biggest downturn in the number <strong>of</strong> business establishments, with losses <strong>of</strong>2.7% and 2.2% respectively; the Cariboo and North Coast Development Regions both declined by 1.2%; and the Mainland/Southwest declined by 0.6%.But not all <strong>of</strong> the news was bad, as the number <strong>of</strong> establishments in the Thompson-Okanagan, Vancouver Island/Coast, and Kootenay Development Regionssaw small, positive gains <strong>of</strong> less than 1% last year.In most Development Regions, the greatest losses took place among business establishments with “no employees.” 10 In 2008, this category declined by 2.4%to 185,273 (just over half <strong>of</strong> all business establishments in BC). An ongoing decline in the number <strong>of</strong> larger establishments (those with 50+ employees) alsocontinued in 2008, with slightly more than 200 major employers closing down. In absolute terms, the greatest loss <strong>of</strong> large employers occurred in the Caribooand Mainland/Southwest Development Regions (-12 and -24 respectively).Living in Regional BCEducational attainmentEducational attainment has a significant impact on productivity, purchasing power, and quality <strong>of</strong> life. Between 2003 and 2008, BC’s share <strong>of</strong> the labour<strong>for</strong>ce with post-secondary education rose from 58.9% to 62.7%, a gain <strong>of</strong> 3.8 percentage points. In the long-term, this will improve BC’s position in anincreasingly knowledge-based global economy.6BC Major Projects Inventory, December 2008. This estimate excludes the capital cost <strong>of</strong> projects that were completed or on hold.7“All projects” includes those that were proposed, started, completed, and on hold as <strong>of</strong> December 2008.8Ibid.9Ibid.10This includes self-employed entrepreneurs.20 ica.bc.ca June/Summer ’09

In 2008, the largest gains in labour <strong>for</strong>ce educational attainment were made in the Cariboo, Northwest BC, 11 and Vancouver Island/Coast (3.8%, 3.2%,and 2.4% respectively). This boosted educational attainment in the Cariboo and Northwest to 56.1% and 48% respectively last year—a positive sign thatthese regions are starting to catch up to the rest <strong>of</strong> the province. At the other end <strong>of</strong> the spectrum, the Mainland/Southwest Development Region continuedto have the highest level <strong>of</strong> educational attainment in the province at 65.3%.Dependence on the social safety netIn 2008, after two years <strong>of</strong> little change, social safety net dependency started to inch up in most <strong>of</strong> BC’s Development Regions. The global financial meltdown<strong>of</strong> 2008 and slumping demand <strong>for</strong> our province’s exports led to significant lay<strong>of</strong>fs, with the greatest job losses occurring in <strong>for</strong>estry and minerals. The share<strong>of</strong> BC’s work<strong>for</strong>ce-age adults who depended on basic income assistance and employment insurance increased from 3.2% in 2007 to 3.6% in 2008.Generally speaking, social safety net dependency in 2008 was lowest (4% or less) in BC’s more urbanized Developments Regions—the Mainland/Southwest,Vancouver Island/Coast, and Thompson-Okanagan—but all three regions saw a slight increase last year (up 0.2, 0.3, and 0.5 percentage points respectively).The most dramatic increase in social safety net dependency occurred in the Nechako Development Region, which rose by 1.6 percentage points, to 6.4%,while the Kootenay, Northeast, and North Coast Development Regions increased by 0.2 percentage points.Real incomeReal income growth is a measure <strong>of</strong> relative purchasing power and, to some extent, change in economic well-being. We use real pre-tax income per capita asour indicator <strong>for</strong> the BC Check-Up. 12 Regional income data is only available to 2006, but by looking at other factors, such as the unemployment rate and jobcreation, we can make reasonable predictions about how real income has changed since then.Between 2003 and 2006, BC saw extraordinary real income gains due to robust economic activity. The most dramatic three-year increase occurred inthe Northeast Development Region, where average real pre-tax income per capita rose 25%, to $43,990—the highest income level in the province. Thisdramatic gain was driven by the booming oil and gas industry. The Nechako (9.8%) and Thompson-Okanagan (9.3%) Development Regions ranked secondand third <strong>for</strong> growth in this indicator. Even in the Vancouver Island/Coast Development Region, where real income growth was the slowest in BC, there wasa significant real income gain <strong>of</strong> 5.2%.Given the export growth and brisk construction activity that has occurred since 2006, it is probable that real income grew in all <strong>of</strong> BC’s DevelopmentRegions in 2007 and 2008.Full report available onlineThe full version <strong>of</strong> the BC Check-Up, Regional Edition is available on the BC Check-Up website at www.bccheckup.com under “Regional Edition.” For morein<strong>for</strong>mation about the report, contact Kerri Brkich, the <strong>Institute</strong>’s manager <strong>of</strong> public affairs, at brkich@ica.bc.ca.Marlyn Chisholm is the principal <strong>of</strong> Chisholm Consulting and the lead economist on the <strong>ICABC</strong>’s annual BC Check-Up report.11Northwest BC comprises both the Nechako and North Coast Development Regions.12To obtain real values, nominal pre-tax income per taxfiler is deflated by the Consumer Price Index, with a base year <strong>of</strong> 2002. Data is from StatisticsCanada.June/Summer ’09 ica.bc.ca 21