Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter

Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter

Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

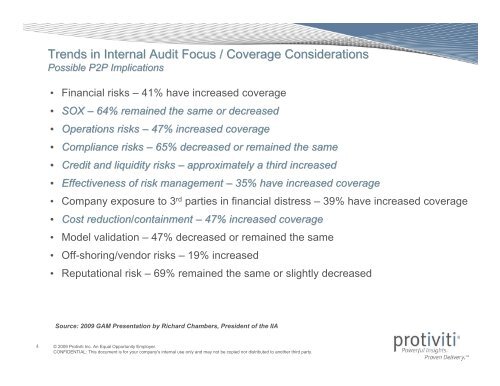

Trends <strong>in</strong> Internal Audit Focus / Coverage ConsiderationsPossible P2P Implications• F<strong>in</strong>ancial risks – 41% have <strong>in</strong>creased coverage• SOX – 64% rema<strong>in</strong>ed <strong>the</strong> same or decreased• Operations risks – 47% <strong>in</strong>creased coverage• Compliance risks – 65% decreased or rema<strong>in</strong>ed <strong>the</strong> same• Credit and liquidity risks – approximately a third <strong>in</strong>creased• Effectiveness of risk management – 35% have <strong>in</strong>creased coverage• Company exposure <strong>to</strong> 3 rd parties <strong>in</strong> f<strong>in</strong>ancial distress – 39% have <strong>in</strong>creased coverage• Cost reduction/conta<strong>in</strong>ment – 47% <strong>in</strong>creased coverage• Model validation – 47% decreased or rema<strong>in</strong>ed <strong>the</strong> same• Off-shor<strong>in</strong>g/vendor risks – 19% <strong>in</strong>creased• Reputational risk – 69% rema<strong>in</strong>ed <strong>the</strong> same or slightly decreasedSource: 2009 GAM Presentation by Richard Chambers, President of <strong>the</strong> <strong>IIA</strong>4 © 2009 Protiviti Inc. An Equal Opportunity Employer.CONFIDENTIAL: This document is <strong>for</strong> your company's <strong>in</strong>ternal use only and may not be copied nor distributed <strong>to</strong> ano<strong>the</strong>r third party.