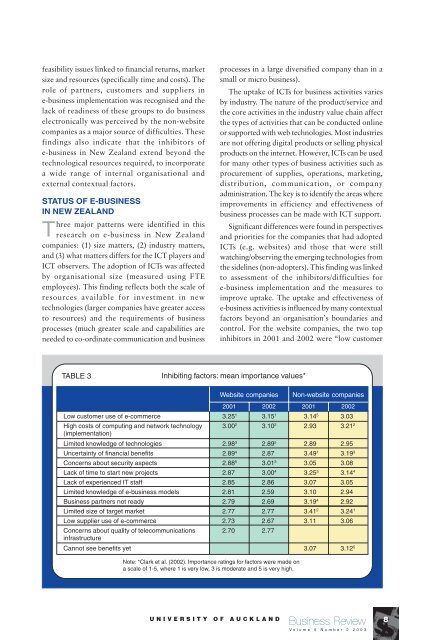

feasibility issues l<strong>in</strong>ked to f<strong>in</strong>ancial returns, marketsize and resources (specifically time and costs). Therole of partners, customers and suppliers <strong>in</strong>e-<strong>bus<strong>in</strong>ess</strong> implementation was recognised and thelack of read<strong>in</strong>ess of these groups to do <strong>bus<strong>in</strong>ess</strong>electronically was perceived <strong>by</strong> the non-websitecompanies as a major source of difficulties. Thesef<strong>in</strong>d<strong>in</strong>gs also <strong>in</strong>dicate that the <strong>in</strong>hibitors ofe-<strong>bus<strong>in</strong>ess</strong> <strong>in</strong> <strong>New</strong> <strong>Zealand</strong> extend beyond thetechnological resources required, to <strong>in</strong>corporatea wide range of <strong>in</strong>ternal organisational andexternal contextual factors.STATUS OF E-BUSINESSIN NEW ZEALANDhree major patterns were identified <strong>in</strong> thisT research on e-<strong>bus<strong>in</strong>ess</strong> <strong>in</strong> <strong>New</strong> <strong>Zealand</strong>companies: (1) size matters, (2) <strong>in</strong>dustry matters,and (3) what matters differs for the ICT players andICT observers. The adoption of ICTs was affected<strong>by</strong> organisational size (measured us<strong>in</strong>g FTEemployees). This f<strong>in</strong>d<strong>in</strong>g reflects both the scale ofresources available for <strong>in</strong>vestment <strong>in</strong> newtechnologies (larger companies have greater accessto resources) and the requirements of <strong>bus<strong>in</strong>ess</strong>processes (much greater scale and capabilities areneeded to co-ord<strong>in</strong>ate communication and <strong>bus<strong>in</strong>ess</strong>processes <strong>in</strong> a large diversified company than <strong>in</strong> asmall or micro <strong>bus<strong>in</strong>ess</strong>).The uptake of ICTs for <strong>bus<strong>in</strong>ess</strong> activities varies<strong>by</strong> <strong>in</strong>dustry. The nature of the product/service andthe core activities <strong>in</strong> the <strong>in</strong>dustry value cha<strong>in</strong> affectthe types of activities that can be conducted onl<strong>in</strong>eor supported with web technologies. Most <strong>in</strong>dustriesare not offer<strong>in</strong>g digital products or sell<strong>in</strong>g physicalproducts on the <strong>in</strong>ternet. However, ICTs can be usedfor many other types of <strong>bus<strong>in</strong>ess</strong> activities such asprocurement of supplies, operations, market<strong>in</strong>g,distribution, communication, or companyadm<strong>in</strong>istration. The key is to identify the areas whereimprovements <strong>in</strong> efficiency and effectiveness of<strong>bus<strong>in</strong>ess</strong> processes can be made with ICT support.Significant differences were found <strong>in</strong> perspectivesand priorities for the companies that had adoptedICTs (e.g. websites) and those that were stillwatch<strong>in</strong>g/observ<strong>in</strong>g the emerg<strong>in</strong>g technologies fromthe sidel<strong>in</strong>es (non-adopters). This f<strong>in</strong>d<strong>in</strong>g was l<strong>in</strong>kedto assessment of the <strong>in</strong>hibitors/difficulties fore-<strong>bus<strong>in</strong>ess</strong> implementation and the measures toimprove uptake. The uptake and effectiveness ofe-<strong>bus<strong>in</strong>ess</strong> activities is <strong>in</strong>fluenced <strong>by</strong> many contextualfactors beyond an organisation’s boundaries andcontrol. For the website companies, the two top<strong>in</strong>hibitors <strong>in</strong> 2001 and <strong>2002</strong> were “low customerTABLE 3Inhibit<strong>in</strong>g factors: mean importance values*Website companies2001 <strong>2002</strong> 2001 <strong>2002</strong>Low customer use of e-commerce 3.25 1 3.15 1 3.14 5 3.03High costs of comput<strong>in</strong>g and network technology 3.00 2 3.10 2 2.93 3.21 2(implementation)Limited knowledge of technologies 2.98 3 2.89 5 2.89 2.95Uncerta<strong>in</strong>ty of f<strong>in</strong>ancial benefits 2.89 4 2.87 3.49 1 3.19 3Concerns about security aspects 2.88 5 3.01 3 3.05 3.08Lack of time to start new projects 2.87 3.00 4 3.25 3 3.14 4Lack of experienced IT staff 2.85 2.86 3.07 3.05Limited knowledge of e-<strong>bus<strong>in</strong>ess</strong> models 2.81 2.59 3.10 2.94Bus<strong>in</strong>ess partners not ready 2.79 2.69 3.19 4 2.92Limited size of target market 2.77 2.77 3.41 2 3.24 1Low supplier use of e-commerce 2.73 2.67 3.11 3.06Concerns about quality of telecommunications 2.70 2.77<strong>in</strong>frastructureCannot see benefits yet 3.07 3.12 5Note: *<strong>Clark</strong> et al. (<strong>2002</strong>). Importance rat<strong>in</strong>gs for factors were made ona scale of 1-5, where 1 is very low, 3 is moderate and 5 is very high.Non-website companiesUNIVERSITY OF AUCKLANDBus<strong>in</strong>ess ReviewVolume 5 Number 2 20038

Lack of read<strong>in</strong>ess for e-<strong>bus<strong>in</strong>ess</strong> <strong>by</strong> other key players,<strong>in</strong>clud<strong>in</strong>g partners, customers and suppliers, wasperceived as a major difficulty <strong>by</strong> non-website <strong>bus<strong>in</strong>ess</strong>esuse of e-commerce” and the “high costs ofcomput<strong>in</strong>g and network technology”. Companieswithout websites were more concerned withfeasibility issues l<strong>in</strong>ked to f<strong>in</strong>ancial returns, marketsize and resources (specifically time and costs). Thelack of read<strong>in</strong>ess for e-<strong>bus<strong>in</strong>ess</strong> <strong>by</strong> other key players,<strong>in</strong>clud<strong>in</strong>g partners, customers and suppliers, wasperceived as a major difficulty <strong>by</strong> the non-website<strong>bus<strong>in</strong>ess</strong>es. The most important measures to improveuptake and effectiveness of e-<strong>bus<strong>in</strong>ess</strong> <strong>in</strong> <strong>New</strong><strong>Zealand</strong> were improv<strong>in</strong>g “telecommunications<strong>in</strong>frastructure”, “consumer access to the <strong>in</strong>ternet”and “improved security”, accord<strong>in</strong>g to thecompanies with websites <strong>in</strong> <strong>2002</strong>. Top priorities forthe non-website companies were “improvedsecurity”, “telecommunications <strong>in</strong>frastructure” andthe provision of “tra<strong>in</strong><strong>in</strong>g for e-<strong>bus<strong>in</strong>ess</strong>”.READINESS FOR THEDIGITAL ECONOMYeyond identification of current e-<strong>bus<strong>in</strong>ess</strong>Bpractices, another approach to assess<strong>in</strong>g“read<strong>in</strong>ess” is to evaluate the areas that are identifiedas most critical for successful participation <strong>in</strong> thedigital economy. For these types of measurements,specific “scorecards” focus on read<strong>in</strong>ess at variouslevels of analysis, e.g. national economies or<strong>in</strong>dividual <strong>bus<strong>in</strong>ess</strong>es. The Asia Pacific EconomicCo-operation (APEC) E-Commerce Read<strong>in</strong>essAssessment Guide (APEC, <strong>2000</strong>) was designed forcompletion at government level. This assessmentwas developed for use <strong>in</strong> partnership mode <strong>by</strong>governments and stakeholders to identify the areaswhere further development is needed: to developpolicies to promote e-commerce or to removebarriers to electronic trade. The assessment<strong>in</strong>cludes factors such as the levels of technological<strong>in</strong>frastructure, <strong>in</strong>ternet access, <strong>in</strong>ternet usage, ITeducation, and the regulatory framework fore-commerce.Another national economy level read<strong>in</strong>essmeasure has been developed <strong>by</strong> the EconomistIntelligence Unit (EIU). EIU has a proprietarymethodology that it uses to rank 60 countries <strong>in</strong>tofour levels of e-<strong>bus<strong>in</strong>ess</strong> preparedness – e-<strong>bus<strong>in</strong>ess</strong>leaders, e-<strong>bus<strong>in</strong>ess</strong> contenders, e-<strong>bus<strong>in</strong>ess</strong> followersand e-<strong>bus<strong>in</strong>ess</strong> laggards (EIU, 2001). TheseE-Read<strong>in</strong>ess rank<strong>in</strong>gs are published on thee<strong>bus<strong>in</strong>ess</strong>forum.com website and are used forevaluat<strong>in</strong>g geographic markets and for <strong>in</strong>ternationalbenchmark<strong>in</strong>g purposes. EIU employs analysts tocomb<strong>in</strong>e quantitative data and qualitativeassessments <strong>by</strong> country specialists <strong>in</strong>to six weightedcategories for their E-Read<strong>in</strong>ess measure:connectivity (30 per cent), <strong>bus<strong>in</strong>ess</strong> environment (20per cent), e-commerce consumer and <strong>bus<strong>in</strong>ess</strong>adoption (20 per cent), legal and regulatoryenvironment (15 per cent), support<strong>in</strong>g e-services (10per cent) and social and cultural <strong>in</strong>frastructure (fiveper cent). Assum<strong>in</strong>g successful e-<strong>bus<strong>in</strong>ess</strong> is notpossible without a positive <strong>bus<strong>in</strong>ess</strong> climate overall,EIU screen 70 <strong>in</strong>dicators for the <strong>bus<strong>in</strong>ess</strong>environment scores that provide projections for thenext five years.To provide a company-level measure of read<strong>in</strong>ess,Hartman, Sifonis and Kadir (<strong>2000</strong>) developed ascorecard us<strong>in</strong>g a series of factors identified froman <strong>in</strong>-depth analysis of Cisco Systems and a seriesof other “net” companies as critical for success ofan enterprise <strong>in</strong> the <strong>in</strong>ternet-based economy.Accord<strong>in</strong>gly, this Net Read<strong>in</strong>ess Scorecard evaluatesattributes of four ma<strong>in</strong> drivers of change:Leadership, Governance, Competencies andTechnology. There are two versions of thisscorecard: a short version, <strong>in</strong> which 20 factors areassessed to provide an approximate measure of NetRead<strong>in</strong>ess; and a longer and more detailed versionthat can be completed electronically at thewww.netread<strong>in</strong>ess.com website. The extendedmeasure is designed to profile the company’s currentstate of Net Read<strong>in</strong>ess, to assess its position relativeto others <strong>in</strong> the same <strong>in</strong>dustry (US-based) and toprovide prescriptive recommendations to improveits competitive position<strong>in</strong>g.NET READINESS IN NEWZEALAND INDUSTRIEShe short version of the Net Read<strong>in</strong>ess ScorecardTwas adapted for research on <strong>New</strong> <strong>Zealand</strong>companies <strong>in</strong> a series of different <strong>in</strong>dustries (<strong>Clark</strong>,9