Police News April 05.indd - New Zealand Police Association

Police News April 05.indd - New Zealand Police Association

Police News April 05.indd - New Zealand Police Association

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

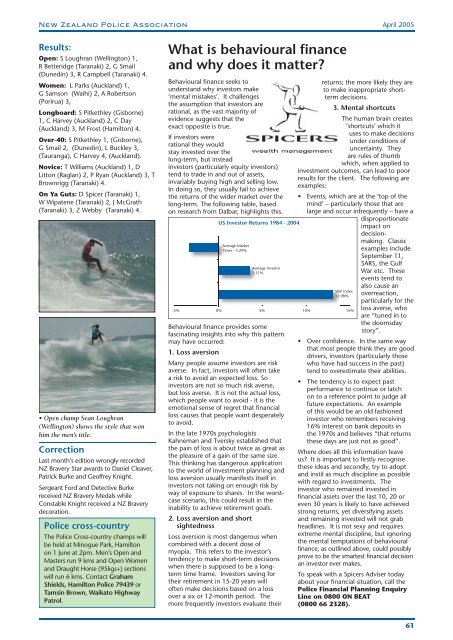

<strong>New</strong> <strong>Zealand</strong> <strong>Police</strong> <strong>Association</strong><strong>April</strong> 2005Results:Open: S Loughran (Wellington) 1,R Betteridge (Taranaki) 2, G Smail(Dunedin) 3, R Campbell (Taranaki) 4.Women: L Parks (Auckland) 1,G Samson (Waihi) 2, A Robertson(Porirua) 3,Longboard: S Pitkethley (Gisborne)1, C Harvey (Auckland) 2, C Day(Auckland) 3, M Frost (Hamilton) 4.Over-40: S Pitkethley 1, (Gisborne),G Smail 2, (Dunedin), L Buckley 3,(Tauranga), C Harvey 4, (Auckland).Novice: T Williams (Auckland) 1, DLitton (Raglan) 2, P Ryan (Auckland) 3, TBrownrigg (Taranaki) 4.On Ya Guts: D Spicer (Taranaki) 1,W Wipatene (Taranaki) 2, J McGrath(Taranaki) 3, Z Webby (Taranaki) 4.• Open champ Sean Loughran(Wellington) shows the style that wonhim the men’s title.CorrectionLast month’s edition wrongly recordedNZ Bravery Star awards to Daniel Cleaver,Patrick Burke and Geoffrey Knight.Sergeant Ford and Detective Burkereceived NZ Bravery Medals whileConstable Knight received a NZ Braverydecoration.<strong>Police</strong> cross-countryThe <strong>Police</strong> Cross-country champs willbe held at Minogue Park, Hamiltonon 1 June at 2pm. Men’s Open andMasters run 9 kms and Open Womenand Draught Horse (95kgs+) sectionswill run 6 kms. Contact GrahamShields, Hamilton <strong>Police</strong> 79439 orTamsin Brown, Waikato HighwayPatrol.What is behavioural financeand why does it matter?Behavioural finance seeks tounderstand why investors make‘mental mistakes’. It challengesthe assumption that investors arerational, as the vast majority ofevidence suggests that theexact opposite is true.If investors wererational they wouldstay invested over thelong-term, but insteadinvestors (particularly equity investors)tend to trade in and out of assets,invariably buying high and selling low.In doing so, they usually fail to achievethe returns of the wider market over thelong-term. The following table, basedon research from Dalbar, highlights this.Behavioural finance provides somefascinating insights into why this patternmay have occurred:1. Loss aversionMany people assume investors are riskaverse. In fact, investors will often takea risk to avoid an expected loss. Soinvestors are not so much risk averse,but loss averse. It is not the actual loss,which people want to avoid - it is theemotional sense of regret that financialloss causes that people want desperatelyto avoid.In the late 1970s psychologistsKahneman and Tversky established thatthe pain of loss is about twice as great asthe pleasure of a gain of the same size.This thinking has dangerous applicationto the world of investment planning andloss aversion usually manifests itself ininvestors not taking on enough risk byway of exposure to shares. In the worstcasescenario, this could result in theinability to achieve retirement goals.2. Loss aversion and shortsightednessLoss aversion is most dangerous whencombined with a decent dose ofmyopia. This refers to the investor’stendency to make short-term decisionswhen there is supposed to be a longtermtime frame. Investors saving fortheir retirement in 15-20 years willoften make decisions based on a lossover a six or 12-month period. Themore frequently investors evaluate theirreturns; the more likely they areto make inappropriate shorttermdecisions.3. Mental shortcutsThe human brain creates‘shortcuts’ which ituses to make decisionsunder conditions ofuncertainty. Theyare rules of thumbwhich, when applied toinvestment outcomes, can lead to poorresults for the client. The following areexamples:• Events, which are at the ‘top of themind’ – particularly those that arelarge and occur infrequently – have adisproportionateimpact ondecisionmaking.Classicexamples includeSeptember 11,SARS, the GulfWar etc. Theseevents tend toalso cause anoverreaction,particularly for theloss averse, whoare “tuned in tothe doomsdaystory”.• Over confidence. In the same waythat most people think they are gooddrivers, investors (particularly thosewho have had success in the past)tend to overestimate their abilities.• The tendency is to expect pastperformance to continue or latchon to a reference point to judge allfuture expectations. An exampleof this would be an old fashionedinvestor who remembers receiving16% interest on bank deposits inthe 1970s and believes “that returnsthese days are just not as good”.Where does all this information leaveus? It is important to firstly recognisethese ideas and secondly, try to adoptand instil as much discipline as possiblewith regard to investments. Theinvestor who remained invested infinancial assets over the last 10, 20 oreven 30 years is likely to have achievedstrong returns, yet diversifying assetsand remaining invested will not grabheadlines. It is not sexy and requiresextreme mental discipline, but ignoringthe mental temptations of behaviouralfinance, as outlined above, could possiblyprove to be the smartest financial decisionan investor ever makes.To speak with a Spicers Adviser todayabout your financial situation, call the<strong>Police</strong> Financial Planning EnquiryLine on 0800 ON BEAT(0800 66 2328).61